|

市場調查報告書

商品編碼

2062061

瀝青瓦:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asphalt Shingles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

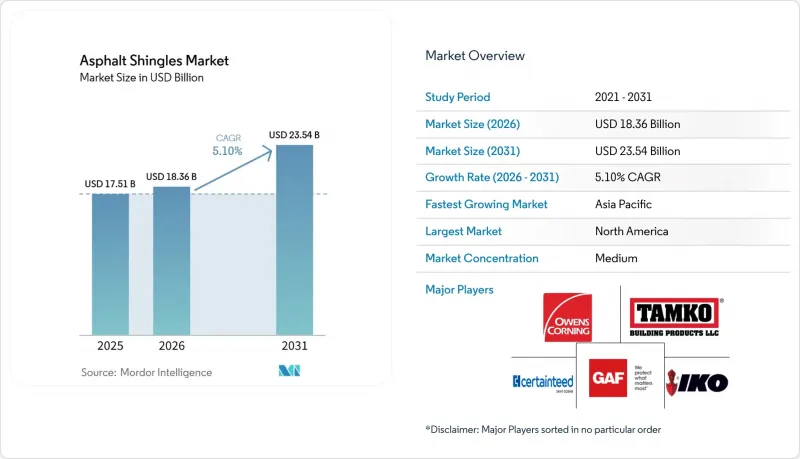

根據 Mordor Intelligence 預測,瀝青瓦市場規模將從 2025 年的 175.1 億美元和 2026 年的 183.6 億美元成長到 2031 年的 235.4 億美元,2026 年至 2031 年的複合年成長率為 5.10%。

本報告按產品類型(例如,三片式單片地毯、豪華/設計師款單片地毯)、增強材料(玻璃纖維氈和有機氈)、分銷管道(例如,直接銷售給承包商)、應用領域(例如,新建住宅)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元(USD)計價。

全球瀝青瓦市場趨勢及洞察

住宅建設和屋頂更換的需求不斷成長。

在瀝青瓦市場,更換需求佔主導地位,在美國每年約500萬套的安裝量中,更換需求佔85%。此外,日益惡化的氣候條件已將瀝青瓦的平均使用壽命縮短至19年。到2025年,風暴造成的屋頂損壞將佔屋頂更換總量的33%,與漏水造成的損壞比例相同,凸顯了氣候變遷加劇如何加速了資本投資。印度的都市化正在催生新的需求。政府住宅計畫和地鐵網路的擴建預計將使該國的屋頂市場規模在2033年達到117億美元。勞動力短缺推高了薪資水平,預計到2026年,39%的北美建築商將採用人工智慧驅動的調度工具。這些因素共同作用,將維持對屋頂更換的高需求,並確保瀝青瓦市場的價格穩定。

經濟高效的施工和全生命週期經濟性

瀝青瓦的安裝成本為每平方英尺 3.50 美元至 5.50 美元,而金屬板的成本為每平方英尺 7 美元至 14 美元。此外,一個兩人團隊只需兩天即可安裝 2,000 平方英尺的屋頂。這種快速安裝有助於緩解預計在 2024 年至 2025 年間人事費用上漲 8% 至 12% 的影響。訂購 100 噸或以上大宗訂單的買家可節省 10% 至 15% 的材料成本,進一步增強了成本優勢。雖然金屬屋頂的使用壽命為 40 至 70 年,但 50 年內更換兩個瀝青屋頂的總成本仍然低於或接近金屬屋頂的較高成本,從而維持了瀝青瓦在市場上的價值。

易受極端天氣和風壓的影響而發生抬升。

颶風後的調查顯示,30%至40%的瀝青瓦屋頂缺陷並非材料本身缺陷,而是由於安裝錯誤造成的,而且這些缺陷大多發生在不到10年的屋頂上。人手不足導致釘子排列不當和瓦片密封不嚴的可能性增加。佛羅裡達州等州強制規定沿海地區的屋頂抗風能力達到110英里/小時(約177公里/小時),迫使製造商提高黏合劑強度並增加緊固件的數量。這使得材料成本增加了高達10%。

細分市場分析

截至2025年,建築用和複合瓦佔瀝青瓦市場總量的57.8%。 4級產品價格高出10-15%,但預計保險費用的節省將在七年內彌補差價。高階/設計師屋頂材料預計在預測期(2026-2031年)內將以6.2%的複合年成長率成長。這主要是因為北美和歐洲的高所得買家更傾向於選擇具有50年保固的仿石板外觀產品。雖然在價格敏感地區以外,對三片式屋頂材料的需求正在下降,但在拉丁美洲和東南亞部分地區,它仍然能夠滿足預算限制。

成長潛力在於兼具發電功能和美觀外型的太陽能複合板材產品。 GAF Energy 的 Timberline Solar ES 2 和 CertainTeed 的 Solstice Shingle 都展現了創新如何推動高利潤產品的需求。因此,即使瀝青瓦總面積逐步增加,由複合板材產品驅動的瀝青瓦市場預計到 2031 年仍將維持成長。

到2025年,玻璃纖維氈將佔出貨量的78.5%,這主要得益於其A級防火性能和輕質特性。有機氈的市佔率正以6.1%的複合年成長率成長,預計到2031年將持續成長,這主要歸功於其在凍融循環中的良好適應性。雖然聚合物改質瀝青正在縮小這兩種基材之間的性能差距,但由於資本投資的慣性,北美大部分生產線仍以生產玻璃纖維氈為主。

由於纖維素纖維是一種可再生資源,人們對永續性的日益關注提高了有機墊材的吸引力。然而,瀝青的高飽和度抵消了部分減少碳排放的益處。由於兩種基材都無法完全取代市場,預計在整個預測期內,瀝青瓦市場中玻璃纖維和有機墊材的比例將穩定在75:25左右。

區域分析

到了2025年,北美將佔全球整體銷售額的42.3%,其中北美地區佔美國屋頂更換工程的85%。 4級抗衝擊瓦片在德克薩斯州、奧克拉荷馬州和科羅拉多已佔據約18%的市場佔有率,而東南部地區產能的提升正是為了滿足颶風災後重建的高峰需求。在加拿大,對有機墊的需求集中在較冷的省份,而墨西哥的成長則與該行業的近岸外包有關,從而便於在低坡度屋頂上進行安裝。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到6.24%。僅印度的市場佔有率預計就將擴大,因為都市區化進程推動了對經濟適用住宅的需求。中國住宅市場的放緩正被國內電子商務倉儲建設所抵消,而日本颱風災害風險的增加則推動了4級聚合物改質層壓板的應用。在澳大利亞,排放「建築碳排放」報告納入建築規範可能會從2026年起促進冷屋頂和循環瀝青解決方案的採用。

在歐洲,歐盟監管的環境產品聲明(EPD)和數位護照的引入將強制要求從2027年起提高材料透明度,這將加大對高碳原料的壓力,同時也有利於進行回收示範計畫的製造商。預計斯堪地那維亞國家和德國將受益於基礎設施投資的推動,實現溫和成長,而法國和英國則可能因資金限制而面臨短期需求抑制。南美、中東和北非等新興市場雖然目前市佔率僅為個位數,但隨著城市基礎建設和氣候適應屋頂材料建築標準的提高,這些市場具有成長潛力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 住宅建設和屋頂更換的需求不斷成長。

- 安裝成本低,生命週期經濟效益好

- 建築層壓板單件的受歡迎程度

- 由於對冷屋頂和能源法規的需求,市場需求不斷成長。

- 耐候性4級聚合物改質層壓板

- 市場限制因素

- 易受極端天氣和強風的影響而發生抬升。

- 與瀝青相關的環境和廢棄物管理問題

- 人們對金屬和複合材料的替代品越來越感興趣

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 三標籤單

- 建築層壓板單層

- 豪華/設計師單間

- 單條

- 按類型分類的加固材料

- 玻璃纖維氈

- 有機墊

- 透過分銷管道

- 屋頂材料批發商

- 直接向企業銷售

- 家居建材商店

- 電子商務/線上

- 透過使用

- 新建住宅

- 住宅屋頂更換

- 商業低坡度屋頂

- 機構和公共部門

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Atlas Roofing Corporation

- BP Canada(Building Products of Canada)

- Carlisle Construction Materials

- CertainTeed

- GAF Materials LLC

- Henry Company

- IKO Industries, Inc.

- Johns Manville

- Malarkey Roofing Products

- Owens Corning

- PABCO Roofing Products

- Polyglass USA, Inc.

- Repsol

- Roofing Corp of America

- Sika AG

- Siplast Inc.

- Soprema Group

- TAMKO Building Products LLC

- Tarco Roofing

第7章 市場機會與未來展望

According to Mordor Intelligence, the asphalt shingles market size is projected to expand from USD 17.51 billion in 2025 and USD 18.36 billion in 2026 to USD 23.54 billion by 2031, registering a CAGR of 5.10% between 2026 to 2031.

This report is Segmented by Product Type (Three-Tab Shingles, Luxury/Designer Shingles, and More), Reinforcement (Fiberglass Mat and Organic Mat), Distribution Channel (Direct-To-Contractors, and More), Application (Residential-New Build, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Asphalt Shingles Market Trends and Insights

Growing Residential Construction and Reroofing Demand

Replacement dominates the Asphalt shingles market, with reroofing representing 85% of roughly five million United States installations each year, and the mean service life sliding to 19 years because of more severe weather. Storm damage matched leaks at 33% of reroof triggers in 2025, underscoring how climate volatility is pulling capital spending forward. Urbanization in India is adding greenfield demand; government housing programs and metro expansions have pushed the national roofing segment toward USD 11.7 billion by 2033. Labor scarcity is elevating wages, prompting 39% of North American contractors to adopt AI scheduling tools in 2026. These factors combine to keep reroof volumes high and sustain price discipline across the Asphalt Shingles market.

Cost-Effective Installation and Life-Cycle Economics

Asphalt shingles install for USD 3.50-5.50 per square foot versus USD 7-14 for metal panels, and a two-person crew can finish a 2,000-square-foot roof in as little as two days. Rapid installation tempers rising labor rates, which climbed 8-12% between 2024 and 2025. Buyers leveraging bulk orders of 100-plus tons secure 10-15% material savings, reinforcing the cost advantage. Although metal roofs last 40-70 years, the total outlay over 50 years for two asphalt replacements still runs below or near the metal premium, preserving value perception in the Asphalt Shingles market.

Vulnerability to Extreme Weather and Wind Uplift

Post-hurricane audits show 30-40% of asphalt shingle failures occur on roofs under 10 years old because of installation errors rather than material faults. Labor shortages raise the likelihood of missed nailing patterns and under-sealed tabs. States such as Florida now require 110 mph ratings in coastal zones, driving manufacturers to boost adhesive strength and fastener counts, which raises bill-of-materials costs by up to 10%.

Other drivers and restraints analyzed in the detailed report include:

- Architectural Laminated Shingles Popularity

- Cool-Roof and Energy-Code Driven Demand

- Bitumen-Related Environmental and Disposal Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Architectural/laminated shingles contributed 57.8% to the overall Asphalt Shingles market share in 2025. Class-4 versions cost 10-15% more yet yield insurer savings that recover the premium within seven years. Luxury/Designer shingles are expected to grow at a CAGR of 6.2% during the forecast period (2026-2031) as upscale buyers in North America and Europe favor slate-look blends that offer 50-year guarantees. Three-tab shingles are fading outside price-sensitive regions but still meet budget constraints in parts of Latin America and Southeast Asia.

Upside potential centers on solar-ready laminates that merge energy generation with curb appeal. GAF Energy's Timberline Solar ES 2 and CertainTeed's Solstice Shingle illustrate how innovation steers demand toward higher-margin SKUs. As a result, the Asphalt shingles market size attributable to laminates is projected to widen through 2031 even if total square footage grows modestly.

Fiberglass mat dominated 78.5% of shipments in 2025, helped by its Class A fire rating and lower weight. Organic mat's market share is advancing at a 6.1% CAGR to 2031, where freeze-thaw cycles favor its bendability. Polymer-modified asphalt is shrinking the performance gap between the two substrates, yet capital inertia keeps most North American lines tuned for fiberglass.

Sustainability narratives are boosting organic mat's appeal because cellulose fibers are renewable. Nevertheless, higher asphalt saturation offsets some carbon benefits. With neither substrate poised for wholesale displacement, the Asphalt shingles market is likely to stabilize near a 75-25 fiberglass-organic split over the forecast window.

Geography Analysis

North America supplied 42.3% of worldwide revenue in 2025, anchored by an 85% reroof mix in the United States. Class-4 impact-resistant shingles already hold roughly 18% share across Texas, Oklahoma, and Colorado, and southeastern capacity additions are timed to meet hurricane recovery peaks. Canadian demand skews toward organic mat in colder provinces, while Mexican growth aligns with industrial nearshoring that drives low-slope installations.

Asia-Pacific is the fastest-growing region at 6.24% CAGR to 2031. India's market share alone is on track to expand as urban migration fuels affordable housing. China's residential slowdown is counterbalanced by warehouse construction for domestic e-commerce, and Japan's typhoon exposure is lifting adoption of Class-4 polymer-modified laminates. Australia is incorporating embodied-carbon reporting into its building code, which could spur uptake of cool-roof and circular asphalt solutions beginning in 2026.

In Europe, upcoming environmental product declarations and digital passports under EU regulation will oblige material transparency from 2027, pressuring high-carbon inputs yet favoring makers with recycling pilots. Scandinavia and Germany may see modest gains tied to infrastructure spending, whereas fiscal constraints in France and the United Kingdom temper short-term volume. Emerging markets in South America, the Middle East, and North Africa contribute single-digit shares but present upside tied to urban infrastructure and climate-resilient roofing codes.

- Atlas Roofing Corporation

- BP Canada (Building Products of Canada)

- Carlisle Construction Materials

- CertainTeed

- GAF Materials LLC

- Henry Company

- IKO Industries, Inc.

- Johns Manville

- Malarkey Roofing Products

- Owens Corning

- PABCO Roofing Products

- Polyglass U.S.A., Inc.

- Repsol

- Roofing Corp of America

- Sika AG

- Siplast Inc.

- Soprema Group

- TAMKO Building Products LLC

- Tarco Roofing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing residential construction and reroofing demand

- 4.2.2 Cost-effective installation and life-cycle economics

- 4.2.3 Architectural laminated shingles popularity

- 4.2.4 Cool-roof and energy-code-driven demand

- 4.2.5 Climate-resilient Class-4 polymer-modified laminates

- 4.3 Market Restraints

- 4.3.1 Vulnerability to extreme weather and wind-uplift

- 4.3.2 Bitumen-related environmental and disposal concerns

- 4.3.3 Growing appeal of metal and composite substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Three-tab Shingles

- 5.1.2 Architectural/Laminated Shingles

- 5.1.3 Luxury/Designer Shingles

- 5.1.4 Strip Shingles

- 5.2 By Reinforcement Material

- 5.2.1 Fiberglass Mat

- 5.2.2 Organic Mat

- 5.3 By Distribution Channel

- 5.3.1 Roofing-Supply Distributors

- 5.3.2 Direct-to-Contractors

- 5.3.3 Retail Home-Center Stores

- 5.3.4 E-commerce/Online

- 5.4 By Application

- 5.4.1 Residential-New Build

- 5.4.2 Residential-Reroofing

- 5.4.3 Commercial Low-Slope

- 5.4.4 Institutional and Public

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 Australia

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Atlas Roofing Corporation

- 6.4.2 BP Canada (Building Products of Canada)

- 6.4.3 Carlisle Construction Materials

- 6.4.4 CertainTeed

- 6.4.5 GAF Materials LLC

- 6.4.6 Henry Company

- 6.4.7 IKO Industries, Inc.

- 6.4.8 Johns Manville

- 6.4.9 Malarkey Roofing Products

- 6.4.10 Owens Corning

- 6.4.11 PABCO Roofing Products

- 6.4.12 Polyglass U.S.A., Inc.

- 6.4.13 Repsol

- 6.4.14 Roofing Corp of America

- 6.4.15 Sika AG

- 6.4.16 Siplast Inc.

- 6.4.17 Soprema Group

- 6.4.18 TAMKO Building Products LLC

- 6.4.19 Tarco Roofing

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Circular-Economy Asphalt Shingle Recycling

- 7.3 Solar-Ready Reflective Shingle Formats

2026年全球瀝青瓦市場報告

2026年全球瀝青瓦市場報告 全球瀝青瓦市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球瀝青瓦市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 瀝青瓦市場規模、佔有率和成長分析(按產品類型、材料、應用、最終用途、分銷管道和地區分類)-2026-2033年產業預測

瀝青瓦市場規模、佔有率和成長分析(按產品類型、材料、應用、最終用途、分銷管道和地區分類)-2026-2033年產業預測 全球瀝青瓦市場(按類型、材料、安裝、最終用戶和分銷管道)預測(2025-2030 年)

全球瀝青瓦市場(按類型、材料、安裝、最終用戶和分銷管道)預測(2025-2030 年) 瀝青瓦市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、配銷通路、應用、地區和競爭細分,2020-2030 年

瀝青瓦市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、配銷通路、應用、地區和競爭細分,2020-2030 年 瀝青瓦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測瀝青瓦的全球市場規模:各產品類型,各材料類型,各用途,各地區,範圍及預測

瀝青瓦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測瀝青瓦的全球市場規模:各產品類型,各材料類型,各用途,各地區,範圍及預測