|

市場調查報告書

商品編碼

2062060

智慧地板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smart Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

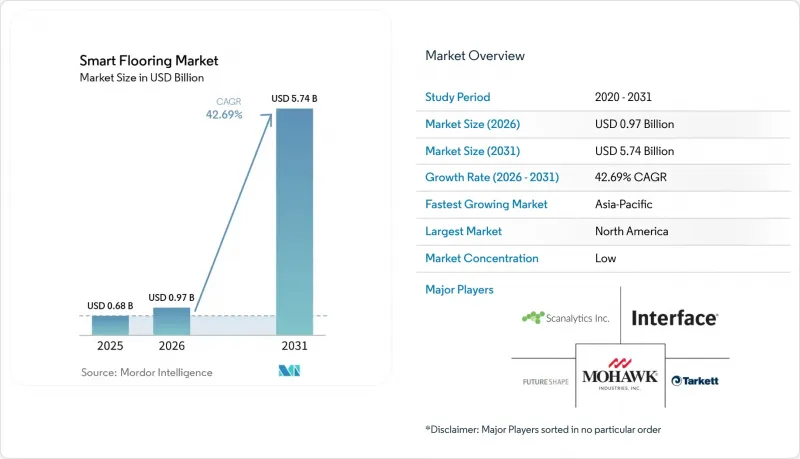

據 Mordor Intelligence 稱,2025 年智慧地板市場價值 6.8 億美元,預計到 2031 年將從 2026 年的 9.7 億美元成長至 57.4 億美元,預測期(2026-2031 年)複合年成長率為 42.69%。

本報告按組件(硬體和軟體)、技術(整合感測器的地磚、智慧地暖、能源採集地板材料等)、最終用戶(住宅、商業、工業/物流等)、應用(佔用率和空間利用率分析、暖通空調和能源管理等)以及地區進行細分。市場預測以價值(美元)表示。

全球智慧地板市場趨勢及洞察

辦公空間佔用率分析在商業性的快速應用

商業房地產開發商正利用基於地面的感測技術來彌合預留空間與實際使用空間之間的差距,企業佔用平台持續指出,這種差異可能高達總座位容量的30-40%。這在智慧地板市場至關重要,因為地面感測可以提供徽章系統和吸頂式被動紅外線設備無法企及的亞平方公尺解析度。這種更精細的行動數據有助於設施管理團隊根據實際使用模式調整佈局,並改善佔用資訊與建築管理工作流程的整合方式。當區域級佔用訊號是連續的而非二進位的時,按需控制的暖通空調程序的效率會更高。這進一步強化了智慧地板在辦公室環境中的應用前景。凱捷英國公司引用的西門子整合實施案例表明,匿名化的地面監控如何在不識別個人身份的情況下支援建築營運。這項設計原則對企業負責人正變得越來越重要。因此,市場佔有率分析已成為智慧地板市場將技術能力轉化為清晰商業性價值的最快路徑之一。

智慧家庭改造和維修項目日益增多

住宅對智慧地板的需求成長速度超過了傳統智慧家庭普及曲線的預期。這是因為維修成本不再與大規模翻新週期掛鉤。模組化設計和無線控制層的出現,使得住宅無需進行大規模施工即可添加智慧功能,從而減少了對承包商主導專案的依賴。因此,購買決策正從大規模資本項目轉向更易於管理的住宅升級,尤其是在舒適度、暖氣控制和居住感知功能整合於一體的情況下。 2025年10月,Warmup推出了“7iE Smart Matter WiFi恆溫器”,該產品兼容Apple Home、Google Home和Amazon Alexa,進一步加強了地暖與主流連網家庭生態系統的聯繫。產品發布表明,SmartGeo技術在實際測試中可將能耗降低高達25%,有助於解決住宅智慧地暖市場運行成本的主要擔憂之一。因此,智慧地暖正逐漸成為普通家庭,特別是豪華住宅和維修工程主導的翻新項目中引入智慧地暖的實用切入點。

較高的初始設定和調整成本

高昂的初始成本仍然是智慧地板材料市場最明顯的短期限制。全感測器地板系統的成本為每平方英尺 75 至 150 美元,而傳統地毯的成本僅為每平方英尺 15 至 40 美元。此外,由於底層改造和佈線的複雜性,維修工程還會額外增加 40% 的成本。儘管潛在客戶群更廣泛,包括許多中型買家,但這種成本差距限制了智慧地板在大型企業、醫療機構和公共部門預算之外的普及。校準也是推廣應用的一大障礙。感測器陣列需要根據特定場所的振動、氣流和設備特性進行調整;否則,就會出現誤報,降低分析結果的可靠性。三菱地產和 Aeterlink 於 2025 年 10 月聯合開展的一項示範項目凸顯了無線電力傳輸在該領域的重要性,因為無需佈線的地板下感測器可以減輕維修項目的部分安裝負擔。在適用於維修工程的智慧地板材料變得像傳統地板材料一樣經濟實惠之前,成本可能仍將是決定哪些買家能夠大規模進入智慧地板市場的關鍵因素。

細分市場分析

2025年,整合感測器的地磚繼續保持其在智慧地板市場的領先地位,佔據44.38%的市場佔有率。這一地位得益於其久經考驗的可靠性、與現有商業佈線基礎設施的便捷整合,以及對辦公、醫療和零售項目需求的高度適用性。這些環境中的買家往往更傾向於選擇與現有安裝方式相容的系統,尤其是在安裝速度和維護便利性會影響投資報酬率的情況下。智慧地暖在智慧地板市場中獨樹一幟,實現了舒適性、能源效率和家庭自動化三者的完美組合。 Warmup於2025年10月發布的「7iE」展示了Matter控制系統如何將地暖與主流智慧家庭生態系統連接起來,從而提升其在豪華住宅和維修項目中的吸引力。

能源採集地板材料是成長最快的技術領域,預計2031年複合年成長率將達到44.57%。這主要得益於材料成本的下降和電源管理電路的改進,從而推動了自發電感測器節點的商業化。一項發表於2024年的研究表明,一種原型地磚每塊可回收高達246毫瓦的能量,材料成本僅為10.20美元,這表明其在高人流量應用場景中的經濟效益正在迅速提升。此外,對低成本、無電池智慧鋪裝系統的研究也支持了這一觀點,即隨著無線通訊負載的降低,發電表面變得越來越實用化。蘇黎世聯邦理工學院的「LignoVolt」計畫透過將羅謝爾鹽晶體嵌入改質木材中,製造出可回收的壓電地板,為智慧地板市場開闢了新的維度,引領智慧地板市場進入高階室內設計和以永續性為導向的維修。雖然靜電耗散智慧地板和互動式 LED 地板仍屬於小眾領域,但智慧地板市場的技術基礎正在擴展到電子製造、資料中心、零售和娛樂設施。

截至2025年,硬體在智慧地板市佔率中佔比65.53%,而軟體預計到2031年將以43.92%的複合年成長率成長。這一起點反映了早期部署的物理特性,因為感測器地毯、閘道器集線器和邊緣處理器構成了每個安裝環境中必不可少的基礎層。在智慧地板市場的早期階段,買家必須投資購買整套數據採集設備,才能從分析、警報或與建築系統的整合中獲益。這有利於那些能夠提供硬體、本地運算和安裝支援一體化解決方案的供應商,尤其是在商業設施中,可靠性比模組化更為重要。這也意味著早期收入集中在實體產品供應商而非持續的軟體供應商手中。

軟體的重要性日益凸顯,因為無需進行新的施工週期,即可將分析服務、視覺化工具和建築管理API的訂閱添加到現有地板系統中。這種模式對智慧地板產業至關重要,因為它能夠帶來持續的收入,並提升每平方英尺的生命週期價值。此外,隨著感測器成本的降低,利潤率結構也在發生變化,硬體價格將面臨長期壓力,而分析服務的定價則相對容易。隨著使用者群體的擴大,能夠管理佔用率儀錶板、警報邏輯和工作流程整合的供應商,比僅提供硬體機殼的供應商更有可能建立更強大的商業性地位。因此,智慧地板市場的下一階段將取決於供應商如何將開放的互通性與客戶願意定期付費的專有軟體價值相結合。

區域分析

北美繼續保持在主導地位,預計到2025年將佔據智慧地板市場42.73%的佔有率。該地區受益於眾多企業技術買家、積極執行綠色建築法規以及已習慣於合規主導採購的醫療保健系統。在美國,CMS 42 CFR §483.25(d)對護理機構的要求持續推動著對防跌倒技術的投資,從而強化了智慧地板市場中最具監管相關性的細分領域之一。需量反應暖通空調(HVAC)計畫也增強了該地區採用地板感測技術的合理性,因為設施營運商可以將佔用數據與可衡量的節能效果和營運效率聯繫起來。歐洲仍然是智慧地板市場的重要區域,這得益於《建築能源性能指令》下的建築能源效率法規以及在注重隱私的職場環境中對匿名感測方法的青睞。

預計到2031年,亞太地區將以44.54%的複合年成長率成長,成為智慧地板市場成長最快的區域市場。在中國,智慧感測地板已在辦公大樓等商業場所廣泛應用,並與照明和暖通空調系統整合。例如,壽城國際中心夜間電力消耗量減少了40%。日本對養老服務的需求強勁,Magic Shields公司報告稱,截至2026年4月,其「Koroyawa Sensor Mat III」已在1600家機構安裝。印度也是智慧地板市場的重要需求來源,工業園區的現代化和智慧建築的普及,為該地區的商業和工業設施帶來了對智慧地板的需求。韓國、澳洲和紐西蘭也透過智慧城市和互聯建築項目,支持感測器主導的基礎設施現代化,從而推動了該地區的市場發展。

儘管南美、中東和非洲在智慧地板市場中所佔佔有率仍然較小,但這些地區具有重要的戰略意義,因為一旦大規模基礎設施項目開始採購,需求可能會迅速成長。巴西和阿根廷仍專注於商業智慧建築的試點項目,而南非則是非洲商業房地產領域最早採用智慧地板的國家。在海灣國家,城市規模的發展項目正在推動對動態和互動式地板材料的需求,Pavegen 強調,人們對能夠支持城市基礎設施目標的能源自給自足型公共空間地板材料的興趣日益濃厚。土耳其、奈及利亞、埃及和類似市場能否更廣泛地採用智慧地板,取決於持續的城市投資、可靠的整合能力以及大規模部署帶來的明確投資回報。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧家居改造和維修項目的興起。

- 辦公空間入住率分析技術的快速商業化

- 養老機構跌倒檢測系統的法律要求

- 透過嵌入式電源管理演算法實現節能效果

- 採用成熟的壓電材料進行印刷,可降低物料清單成本。

- 城市交通地板在多模態樞紐中的整合

- 市場限制因素

- 缺乏全球互通性標準

- 初始設定和校準成本相對較高。

- 關於連續運動檢測的資料隱私問題

- 能源採集瓦片的機械耐久性局限性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 透過技術

- 內建感應器的地板磚

- 智慧地暖(電地暖熱水地暖)

- 能源採集地板材料

- 靜電耗散/ESD智慧地板

- 互動式LED/視覺化地板

- 最終用戶

- 住宅

- 商業

- 工業與物流

- 運動和健身設施

- 公共基礎建設/智慧城市建設

- 其他

- 透過使用

- 入住率和空間利用率分析

- 跌倒檢測和老年護理監測

- 暖通空調和能源管理

- 安全和存取控制

- 客戶參與與尋路

- 遊戲和互動娛樂

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SensingTex SL

- Pavegen Systems Ltd.

- Future-Shape GmbH

- Tarkett SA

- Mohawk Industries Inc.

- Shaw Industries Group Inc.

- Forbo Holding AG

- Interface Inc.

- Gerflor Group

- Beaulieu International Group

- Warmup PLC

- nVent Electric plc

- nora Systems GmbH

- Flowcrete Group Ltd.

- Sensora PLC

- Electroroute Ltd.

- Huawei Technologies Co. Ltd.(Smart Campus Flooring)

- ABB Ltd.(Motion and Smart Buildings Division)

- Siemens AG(Smart Infrastructure)

- Honeywell International Inc.(Building Technologies)

第7章 市場機會與未來展望

According to Mordor Intelligence, the smart flooring market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.97 billion in 2026 to reach USD 5.74 billion by 2031, at a CAGR of 42.69% during the forecast period (2026-2031).

This report is Segmented by Component (Hardware, and Software), Technology (Sensor-Embedded Floor Tiles, Smart Heated Flooring, Energy-Harvesting Flooring, and More), End-User (Residential, Commercial, Industrial and Logistics, and More), Application (Occupancy and Space-Utilization Analytics, HVAC and Energy Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Flooring Market Trends and Insights

Rapid Commercial Adoption for Occupancy Analytics in Office Spaces

Commercial real-estate operators are using floor-based sensing to narrow the gap between booked space and actual usage, and enterprise occupancy platforms continue to place that mismatch at 30-40% of total seat inventory. In the smart flooring market, this matters because floor sensing can deliver sub-square-meter resolution that badge systems and ceiling-mounted passive infrared devices do not. That sharper movement data helps facilities teams adjust layouts based on real usage patterns and also improves how occupancy information is fed into building management workflows. Demand-controlled HVAC programs become more effective when zone-level occupancy signals are continuous rather than binary, which strengthens the operating case for the smart flooring market in office environments. A Siemens-integrated deployment cited by Capgemini UK demonstrated how anonymized floor monitoring can support building operations without identifying individuals, a design principle becoming increasingly important to enterprise buyers. This makes occupancy analytics one of the fastest ways for the smart flooring market to convert technical capability into clear commercial value.

Rising Smart-Home Renovations and Retrofit Projects

Residential demand in the smart flooring market is rising faster than older smart-home adoption curves suggested because retrofit costs are becoming less tied to full renovation cycles. Modular formats and wireless control layers have made it easier for homeowners to add smart functionality without major construction disruption, which reduces dependence on contractor-led projects. This changes the purchase decision from a large capital project into a more manageable home upgrade, especially when comfort, heating control, and occupancy awareness are packaged together. Warmup launched its 7iE Smart Matter WiFi Thermostat in October 2025, with compatibility with Apple Home, Google Home, and Amazon Alexa, strengthening the connection between underfloor heating and mainstream connected-home ecosystems. The same launch stated that SmartGeo technology reduced energy consumption by up to 25% during use testing, helping address one of the main running-cost objections in the residential smart flooring market. As a result, smart heated flooring is emerging as a practical entry point for household adoption, especially in premium homes and retrofit-led renovations.

High Initial Installation and Calibration Costs

High upfront cost remains the clearest near-term restraint on the smart flooring market. Full-sensor floor systems were priced at USD 75-150 per square foot, compared with USD 15-40 per square foot for conventional carpet, and retrofit work added 40% premium due to subfloor modifications and cabling complexity. That cost gap limits adoption outside larger enterprises, healthcare networks, and public-sector budgets, even though the broader addressable base includes many mid-market buyers. Calibration adds another layer of friction because sensor arrays must be tuned for site-specific vibration, airflow, and equipment signatures, or false positives will reduce trust in the analytics output. Mitsubishi Estate's October 2025 demonstration with Aeterlink showed why wireless power matters for this category, since under-floor sensors that avoid cabling can reduce part of the installation burden in retrofit settings. Until retrofit-ready formats move closer to conventional flooring economics, cost will continue to shape which buyers can enter the smart flooring market at scale.

Other drivers and restraints analyzed in the detailed report include:

- Legal Mandates for Fall-Detection Systems in Senior-Care Facilities

- Energy Savings from Embedded Power-Management Algorithms

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensor-embedded floor tiles commanded a 44.38% share in 2025, maintaining their lead in the smart flooring market. Their position was driven by proven reliability, easier integration with existing commercial wiring infrastructure, and a better fit for the needs of office, healthcare, and retail projects. Buyers in these settings tend to prefer systems that already work with established installation practices, especially when deployment speed and maintenance simplicity affect payback. Smart heated flooring remains a distinct technology path in the smart flooring market because it addresses comfort, energy efficiency, and home automation simultaneously. Warmup's October 2025 7iE launch demonstrated how Matter-compatible controls can connect underfloor heating to major smart-home ecosystems, strengthening the appeal of heated flooring in premium homes and retrofit projects.

Energy-harvesting flooring is the fastest-growing technology segment, with a 44.57% CAGR projected through 2031, driven by falling material costs and improved power-management circuits that are advancing self-powered sensor nodes toward commercial viability. Research published in 2024 demonstrated a prototype tile capable of harvesting up to 246 mW per tile at a material cost of USD 10.20, demonstrating how quickly the economics are improving for high-footfall use cases. Additional work on low-cost battery-free smart pavement systems also supports the idea that power-generating surfaces are becoming more practical as wireless communication loads fall. ETH Zurich's LignoVolt project adds another dimension by embedding Rochelle salt crystals into modified wood to create recyclable piezo-parquet, bringing the smart flooring market into premium interior design and sustainability-led renovation conversations. Static-dissipative smart flooring and interactive LED flooring remain small niches, but they broaden the smart flooring market's technology base into electronics production, data centers, retail, and entertainment venues.

Hardware retained 65.53% of the smart flooring market share in 2025, while software is projected to expand at a 43.92% CAGR through 2031. That starting point reflected the physical nature of early deployments, because sensor carpets, gateway hubs, and edge processors formed the non-negotiable base layer of each installation. In the first phase of the smart flooring market, buyers had to fund the full data-collection stack before they could benefit from analytics, alerts, or building-system integration. This favored vendors that could deliver hardware, local compute, and installation support as one package, especially in commercial sites where reliability mattered more than modularity. It also meant that early revenue concentration sat with physical product suppliers rather than with recurring software providers.

Software is now gaining weight because analytics subscriptions, visualization tools, and building management APIs can be layered onto installed floors without another full construction cycle. That model matters for the smart flooring industry because it creates recurring revenue and improves lifetime value per square foot. It also changes margin structure, since declining sensor costs are likely to pressure hardware pricing over time while analytics remains more defensible. As the installed base grows, vendors that control occupancy dashboards, alert logic, and workflow integration are likely to hold a stronger commercial position than those that supply only hardware shells. The next stage of the smart flooring market will therefore depend on how successfully suppliers combine open interoperability with proprietary software value that customers are willing to keep paying for.

Geography Analysis

North America held 42.73% of the smart flooring market share in 2025, maintaining its leading regional position. The region benefits from a large base of enterprise technology buyers, active green-building enforcement, and healthcare systems that are already familiar with compliance-driven procurement. In the United States, nursing-facility requirements under CMS 42 CFR § 483.25(d) continue to support fall-prevention investment, which strengthens one of the most regulation-linked parts of the smart flooring market. Demand-controlled HVAC programs also improve the regional case for floor sensing because building operators can tie occupancy data to measurable energy savings and operating efficiency. Europe remained another important region in the smart flooring market, supported by building-efficiency rules under the Energy Performance of Buildings Directive and by the appeal of anonymous sensing approaches in privacy-sensitive workplace environments.

Asia-Pacific is projected to grow at a 44.54% CAGR through 2031, which makes it the fastest-expanding regional segment in the smart flooring market. China has already demonstrated commercial-scale use in office properties, where smart sensing floors are linked to lighting and HVAC systems, including a nearly 40% reduction in evening electricity consumption at Shoucheng International Center. Japan is a strong elder-care demand center, and Magic Shields reported deployment of its Koroyawa Sensor Mat III across 1,600 facilities by April 2026. India adds another source of demand through industrial-park modernization and wider adoption of smart buildings, giving the regional smart flooring market exposure to both commercial and industrial settings. South Korea, Australia, and New Zealand are also helping the regional mix through smart-city and connected-building programs that support sensor-led infrastructure upgrades.

South America, the Middle East, and Africa remained smaller parts of the smart flooring market, but they are strategically important because large infrastructure projects can quickly scale demand once procurement begins. Brazil and Argentina are still centered on commercial smart-building pilots, while South Africa is the clearest early adopter in African commercial real estate. In the Gulf, city-scale development programs are creating openings for kinetic and interactive flooring, and Pavegen has highlighted growing interest in energy-autonomous public-realm surfaces that can support urban infrastructure goals. Wider adoption across Turkey, Nigeria, Egypt, and similar markets will depend on sustained urban investment, reliable integration performance, and clearer evidence of payback at scale.

- SensingTex S.L.

- Pavegen Systems Ltd.

- Future-Shape GmbH

- Tarkett S.A.

- Mohawk Industries Inc.

- Shaw Industries Group Inc.

- Forbo Holding AG

- Interface Inc.

- Gerflor Group

- Beaulieu International Group

- Warmup PLC

- nVent Electric plc

- nora Systems GmbH

- Flowcrete Group Ltd.

- Sensora PLC

- Electroroute Ltd.

- Huawei Technologies Co. Ltd. (Smart Campus Flooring)

- ABB Ltd. (Motion and Smart Buildings Division)

- Siemens AG (Smart Infrastructure)

- Honeywell International Inc. (Building Technologies)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Smart-Home Renovations and Retrofit Projects

- 4.2.2 Rapid Commercial Adoption for Occupancy Analytics in Office Spaces

- 4.2.3 Legal Mandates for Fall-Detection Systems in Senior-Care Facilities

- 4.2.4 Energy Savings From Embedded Power-Management Algorithms

- 4.2.5 Maturing Printed Piezoelectric Materials Lowering BOM Costs

- 4.2.6 Urban Mobility Flooring Integration in Multi-Modal Transit Hubs

- 4.3 Market Restraints

- 4.3.1 Lack of Global Interoperability Standards

- 4.3.2 High Initial Installation and Calibration Costs

- 4.3.3 Data-Privacy Concerns Around Continuous Motion Sensing

- 4.3.4 Mechanical Durability Limits in Energy-Harvesting Tiles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Technology

- 5.2.1 Sensor-Embedded Floor Tiles

- 5.2.2 Smart Heated Flooring (Electric and Hydronic)

- 5.2.3 Energy-Harvesting Flooring

- 5.2.4 Static-Dissipative / ESD Smart Flooring

- 5.2.5 Interactive LED / Visualization Flooring

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial and Logistics

- 5.3.4 Sports and Fitness Facilities

- 5.3.5 Public Infrastructure / Smart-City Installations

- 5.3.6 Other End-Users

- 5.4 By Application

- 5.4.1 Occupancy and Space-Utilization Analytics

- 5.4.2 Fall Detection and Elderly-Care Monitoring

- 5.4.3 HVAC and Energy Management

- 5.4.4 Security and Access Control

- 5.4.5 Customer Engagement and Wayfinding

- 5.4.6 Gaming and Interactive Entertainment

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Spain

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SensingTex S.L.

- 6.4.2 Pavegen Systems Ltd.

- 6.4.3 Future-Shape GmbH

- 6.4.4 Tarkett S.A.

- 6.4.5 Mohawk Industries Inc.

- 6.4.6 Shaw Industries Group Inc.

- 6.4.7 Forbo Holding AG

- 6.4.8 Interface Inc.

- 6.4.9 Gerflor Group

- 6.4.10 Beaulieu International Group

- 6.4.11 Warmup PLC

- 6.4.12 nVent Electric plc

- 6.4.13 nora Systems GmbH

- 6.4.14 Flowcrete Group Ltd.

- 6.4.15 Sensora PLC

- 6.4.16 Electroroute Ltd.

- 6.4.17 Huawei Technologies Co. Ltd. (Smart Campus Flooring)

- 6.4.18 ABB Ltd. (Motion and Smart Buildings Division)

- 6.4.19 Siemens AG (Smart Infrastructure)

- 6.4.20 Honeywell International Inc. (Building Technologies)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

Z-Wave產品市場:2026-2032年全球市場預測(按產品類型、組件、分銷管道和最終用戶分類)

Z-Wave產品市場:2026-2032年全球市場預測(按產品類型、組件、分銷管道和最終用戶分類) Z-Wave產品全球市場報告(2026年)

Z-Wave產品全球市場報告(2026年) Z-Wave產品市場:產業趨勢與全球市場預測(至2035年)2026年全球智慧時鐘市場報告

Z-Wave產品市場:產業趨勢與全球市場預測(至2035年)2026年全球智慧時鐘市場報告 智慧家庭設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類2026年全球智慧家居設備市場報告

智慧家庭設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類2026年全球智慧家居設備市場報告 智慧地板市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年)

智慧地板市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年) 智慧時鐘市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)Wi-Fi 時鐘市場按產品類型、顯示類型、連接類型、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)Z-Wave 模組市場按產品類型、通訊協定類型、應用和最終用途分類,全球預測,2026-2032 年

智慧時鐘市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)Wi-Fi 時鐘市場按產品類型、顯示類型、連接類型、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)Z-Wave 模組市場按產品類型、通訊協定類型、應用和最終用途分類,全球預測,2026-2032 年