|

市場調查報告書

商品編碼

2062040

抗凝血滅鼠劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Anticoagulant Rodenticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

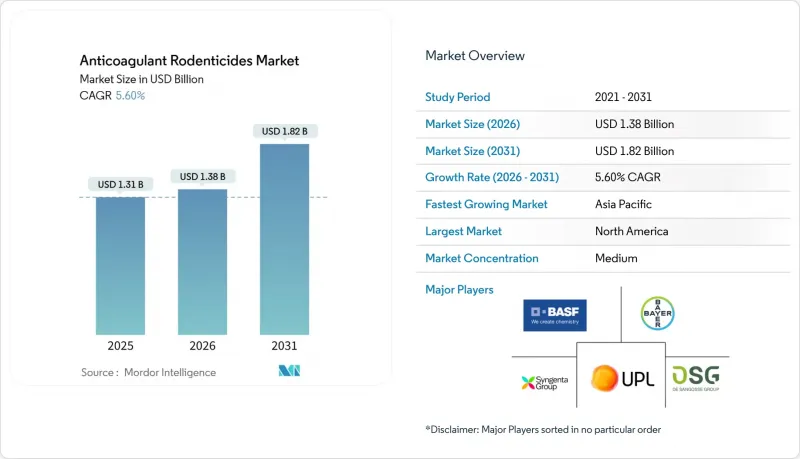

根據 Mordor Intelligence 預測,抗凝血滅鼠劑的市場規模預計將從 2025 年的 13.1 億美元成長到 2026 年的 13.8 億美元,到 2031 年將達到 18.2 億美元,2026 年至 2031 年的複合年成長率為 5.60%。

本報告按類型(第一代和第二代抗凝血劑)、劑型(顆粒劑、塊劑等)、應用領域(穀物、油籽和豆類等)、配銷通路(直銷等)和地區(北美、歐洲、南美、亞太地區等)進行細分。市場預測以美元計價。

全球抗凝血滅鼠劑市場趨勢及洞察

人們越來越關注如何防止農產品倉儲中的收穫後損失

人們日益關注如何最大限度地減少農業收穫後的損失,這是抗凝血滅鼠劑市場的主要驅動力。倉儲設施、筒倉和農場倉庫中的鼠患會導致穀物、豆類和油籽的大量數量和品質損失,對農場盈利和國家糧食安全產生負面影響。隨著農業生產的擴大,保護儲存中的作物已成為一項至關重要的營運要務。大規模糧食處理系統正擴大實施系統性的滅鼠方案,以減少糧食腐敗、污染和基礎設施損壞。抗凝血滅鼠劑已被證明能有效控制封閉迴路境中的持續性鼠群,並常用於周邊誘餌投放和內部儲存保護策略。它們能夠持續減少鼠群數量,有助於打破鼠患反覆發生的循環,從而減輕長期儲存損失。

氣候變遷導致溫帶糧食產區囓齒動物數量迅速增加。

由於冬季氣溫升高,囓齒類動物的繁殖季節延長,導致其數量高峰期提前出現在農業生產週期中。多年研究證實,在基於通用社會經濟發展路徑的氣候情境下,鼠屬和褐家鼠屬的分佈範圍正在向更高緯度地區擴展。隨著倉儲設施中囓齒動物蟲害的加劇,經營者開始從第一代殺蟲劑轉向使用單劑量第二代活性成分殺蟲劑,以快速控制蟲害。因此,氣候變遷的影響正在直接擴大糧食生產國對抗凝血滅鼠劑的需求,因為飼料總用量增加,補給週期縮短。

促進生物安全食品供應鏈的監管

監管機構對確保生物安全食品供應鏈的日益重視是推動抗凝血滅鼠劑市場發展的主要動力。主要農業經濟體的監管機構強制執行嚴格的食品安全標準,要求在整個價值鏈(包括收穫前、儲存和分銷階段)採取有效的滅鼠措施。美國環保署 (EPA) 強制要求在瀕危物種棲息地記錄誘餌放置情況並進行動物屍體調查,迫使經營者採用能夠自動記錄感測器資料的防篡改裝置。在澳大利亞,消費者獲取第二代產品的管道有限,且強制使用著色劑和苦味劑,實際上限制了銷售管道,使其主要集中在專業管道。

細分市場分析

第二代抗凝血滅鼠劑是目前最大的細分市場,預計到2025年將佔據抗凝血滅鼠劑市場63%的佔有率,其中成長最快的細分市場預計將在2026年至2031年間以8.8%的複合年成長率成長。其市場主導地位主要歸功於其高效性和單劑量致死性,這使得它們能夠有效清除農田、倉儲設施和城市環境中的抗藥性囓齒動物種群。其廣泛應用主要源自於對快速可靠的害蟲防治解決方案的需求,尤其是在糧食倉儲和食品加工等大規模、高風險應用領域。

第一代抗凝血劑市場的主要驅動力是第二代化合物因環境風險和二次中毒問題而受到更嚴格的監管。因此,人們正在轉向更安全、毒性更低的替代品,尤其是在嚴格監管的地區。第一代抗凝血劑在綜合蟲害管理(IPM)計畫中越來越受歡迎,因為在這些計畫中,重複且可控的給藥方式更有利於減少對生態系統的影響。這一趨勢凸顯了更廣泛的市場轉型:雖然療效仍然至關重要,但永續性和合規性在塑造產品需求方面也變得同樣重要。

顆粒劑是目前最大的細分市場,預計到2025年將佔抗凝血劑市場佔有率的41%。其廣泛應用源自於其易於使用、經濟高效,且適用於大規模農業作業,特別適用於需要快速部署的露天田間和噴灑作業。農民和害蟲防治人員更傾向於使用顆粒劑,因為柔軟性覆蓋範圍廣,且對多種囓齒動物有效。

塊狀滅蟲劑是成長最快的細分市場,預計2026年至2031年間的複合年成長率將達到9.4%。這一成長主要得益於其耐用性、耐候性以及與誘餌站的兼容性,尤其是在倉庫、食品加工廠和倉儲設施等受控環境中。塊狀滅蟲劑非常適合滿足嚴格的食品安全法規,因為它們在潮濕和惡劣環境中不易崩壞,且藥效持續時間更長。隨著系統化和可監控的蟲害控制解決方案(例如物聯網誘餌站)在市場上的日益普及,預計對塊狀滅蟲劑的需求將顯著成長。

區域分析

北美是最大的市場區域,預計到2025年將佔據抗凝血滅鼠劑市場38%的佔有率。這一主導地位歸功於該地區成熟的農業和食品倉儲產業、完善的食品安全法規以及現代害蟲防治技術的廣泛應用。此外,人們對收穫後損失的高度重視以及主要滅鼠劑生產商的存在,進一步鞏固了北美作為主要市場的地位。例如,在美國中西部,愛荷華州和伊利諾伊州的糧食倉儲設施正在增加第二代抗凝血滅鼠劑的使用,以控制日益嚴重的鼠患並防止糧食損失,這支撐了穩定的市場需求。

亞太地區是成長最快的地區,預計2026年至2031年複合年成長率將達到8.5%。這一成長主要得益於大規模農業的擴張、糧食倉儲和加工基礎設施投資的增加,以及人們對作物保護和糧食安全意識的提高。此外,人口成長和對主糧及高價值作物需求的增加,也推動了亞太地區新興經濟體對抗凝血滅鼠劑的使用,使該地區成為市場的重要成長區域。澳洲為期一年的消費者銷售禁令旨在引導市場需求流向獲得許可的公司,而非消除市場需求,從而在維持銷售量的同時加強數據收集能力。

歐洲受惠於其完善的糧食倉儲基礎設施和成熟的專業病蟲害防治網。更嚴格的控制體系和能力認證要求,以及持續的硬體升級,使供應商能夠維持利潤率。抗藥性的蔓延正促使人們轉向使用Flocoumafen和非抗凝血劑產品,這為配方改進創造了機會。在非洲和中東,隨著各國政府部署現代化糧倉以減少收穫後損失並增強糧食安全,市場正在擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人們越來越關注如何防止農產品倉儲中的收穫後損失

- 與氣候變遷相關的囓齒動物數量在溫帶糧食產區激增。

- 農業管理服務提供者的整合

- 引入與物聯網 (IoT) 相容的遠端測量技術用於飼餵站

- 基因編輯的穀物品種提高了囓齒動物的偏好。

- 資產所有者為脊椎動物害蟲福利管理而製定的環境、社會和管治(ESG) 準則。

- 市場限制因素

- 促進生物安全食品供應鏈的監管

- 對第一代活性成分的各種抗藥性不斷擴大

- 區域主導的禁令源自於涉及猛禽的二次中毒事件

- 維生素K拮抗劑前驅物的價格波動

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 第一代抗凝血劑

- 第二代抗凝血劑

- 按劑型

- 顆粒

- 堵塞

- 粉末

- 液體

- 透過使用

- 穀類和穀類食品

- 油籽/豆類

- 水果和蔬菜

- 其他用途

- 透過分銷管道

- 直接銷售(從製造商到合作社)

- 農業化學品零售商

- 線上平台

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Bayer AG

- Syngenta Group

- UPL Limited

- Reckitt Benckiser Group plc

- Rentokil Initial plc

- Anticimex AB

- Neogen Corporation

- Kemin Industries, Inc.

- Fumakilla Limited

- Bell Laboratories, Inc.

- PelGar International Limited

- De Sangosse SAS

- Vetoquinol SA

- JT Eaton & Co., Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the anticoagulant rodenticides market size is projected to grow from USD 1.31 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at 5.60% CAGR over 2026-2031.

This report is Segmented by Type (First-Generation Anticoagulants and Second-Generation Anticoagulants), by Formulation (Pellets, Blocks, and More), by Application (Cereals and Grains, Oilseeds and Pulses, and More), by Distribution Channel (Direct and More), by Geography (North America, Europe, South America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Anticoagulant Rodenticides Market Trends and Insights

Increasing Focus on Post-Harvest Loss Prevention in Agricultural Storage

The growing emphasis on minimizing post-harvest losses in agriculture is a significant driver for the anticoagulant rodenticides market. Rodent infestations in grain storage facilities, silos, and farm warehouses result in substantial quantitative and qualitative losses of cereals, pulses, and oilseeds, adversely affecting farmer profitability and national food security. As agricultural production scales up, safeguarding harvested crops during storage has become a critical operational priority. Large-scale grain handling systems are increasingly adopting structured rodent management programs to reduce spoilage, contamination, and infrastructure damage. Anticoagulant rodenticides are commonly employed in perimeter baiting and internal storage protection strategies due to their proven effectiveness in controlling persistent rodent populations in enclosed environments. Their ability to achieve sustained population reduction helps break recurring infestation cycles, thereby mitigating long-term storage losses.

Climate-Linked Rodent Population Surges in Temperate Grain Belts

Warmer winters are extending breeding windows, so rat colonies reach peak numbers earlier in the agricultural calendar. Multiyear studies confirm that Mus and Rattus genera are expanding their geographic ranges toward higher latitudes under shared socioeconomic pathway climate scenarios. When rodent pressure escalates inside storage facilities, operators shift from first-generation to single-feed second-generation actives to curb damage rapidly. Climate amplification, therefore, enlarges the total quantity of bait deployed and reduces waiting time between replenishment cycles, directly expanding the Anticoagulant Rodenticides Market demand in cereal-growing nations.

Regulatory Push for Bio-Secure Food Supply Chains

The increasing regulatory focus on ensuring bio-secure food supply chains is a key driver for the anticoagulant rodenticides market. Strict food safety standards enforced by regulatory authorities in major agricultural economies require effective rodent control measures across the value chain, including pre-harvest, storage, and distribution stages. The United States Environmental Protection Agency requires baiting records and carcass searches in endangered-species zones, forcing operators to adopt tamper-resistant stations that automatically log sensor data. Australia has restricted consumer access to second-generation products and insists on the use of dyes and bittering agents, effectively professionalizing sales channels.

Other drivers and restraints analyzed in the detailed report include:

- Internet of Things (IoT)-Enabled Bait-Station Telemetry Adoption

- Environmental, Social, and Governance (ESG) Guidelines Set by Asset Owners for Managing Vertebrate Pest Welfare

- Volatile Vitamin K Antidote Precursor Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Second-generation anticoagulants hold the largest segment, capturing 63% of the anticoagulant rodenticides market share in 2025, while the fastest-growing segment is with an 8.8% CAGR through 2026-2031. This dominance is primarily due to their high efficacy and single-feed lethality, which enable them to control resistant rodent populations across agricultural fields, storage facilities, and urban environments. Their widespread adoption is driven by demand for rapid, reliable pest control solutions, particularly in large-scale, high-risk applications such as grain storage and food processing.

The first-generation anticoagulants market is largely driven by increasing regulatory restrictions on second-generation compounds due to concerns about environmental and secondary poisoning risks. Consequently, there is a shift toward safer, lower-toxicity alternatives, particularly in regions with stringent regulatory frameworks. First-generation anticoagulants are gaining popularity within integrated pest management (IPM) programs, where repeated, controlled dosing is preferred to reduce ecological impact. This trend highlights a broader market transition in which efficacy remains essential, but sustainability and regulatory compliance are becoming equally significant in shaping product demand.

Pellets hold the largest segment, accounting for 41% of the anticoagulant rodenticides market share in 2025. Their widespread use is attributed to their ease of application, cost-effectiveness, and suitability for large-scale agricultural operations, particularly in open fields and broadcast applications where rapid deployment is critical. Farmers and pest control operators prefer pellets for their flexibility in covering extensive areas and their effectiveness in targeting a wide range of rodent species.

The blocks segment is the fastest-growing segment, projected to grow at a 9.4% CAGR between 2026 and 2031. This growth is driven by their durability, resistance to weather conditions, and compatibility with bait stations, particularly in controlled environments such as warehouses, food processing units, and storage facilities. Blocks are less susceptible to disintegration in moist or harsh conditions and provide longer-lasting efficacy, making them well-suited for compliance with stringent food safety regulations. As the market increasingly adopts structured, monitored pest control solutions, including IoT-enabled bait stations, demand for block formulations is projected to grow significantly.

Geography Analysis

North America held the largest region, accounting for 38% of the anticoagulant rodenticides market size in 2025. This dominance is attributed to the region's well-established agricultural and food storage industries, food safety regulations, and widespread adoption of modern pest management practices. Additionally, high awareness of post-harvest losses and the presence of major rodenticide manufacturers further strengthen North America's position as the leading market. For instance, in the United States Midwest, grain elevators in Iowa and Illinois have increased the use of second-generation anticoagulant rodenticides during the storage season to control rising rodent infestations and prevent grain losses, supporting consistent market demand.

Asia-Pacific is the fastest-growing region, projected to grow at a 8.5% CAGR between 2026 and 2031. This growth is driven by the expansion of large-scale farming, increased investments in grain storage and processing infrastructure, and rising awareness of crop protection and food security. Furthermore, the growing population and increasing demand for staple and high-value crops are driving the adoption of anticoagulant rodenticides across emerging economies in the Asia-Pacific region, positioning the region as a critical growth area for the market. Australia's one-year consumer suspension channels demand into licensed firms rather than eliminating it, sustaining volumes while improving data capture.

Europe benefits from an extensive grain storage infrastructure and well-established professional pest management networks. The implementation of stricter stewardship schemes and proof-of-competence requirements, along with ongoing hardware upgrades, helps vendors maintain profit margins. The prevalence of resistance has led to a shift toward flocoumafen and non-anticoagulant products, creating opportunities for reformulation. In Africa and the Middle East, the market is expanding as governments implement modern silos to reduce post-harvest losses and enhance food security.

- BASF SE

- Bayer AG

- Syngenta Group

- UPL Limited

- Reckitt Benckiser Group plc

- Rentokil Initial plc

- Anticimex AB

- Neogen Corporation

- Kemin Industries, Inc.

- Fumakilla Limited

- Bell Laboratories, Inc.

- PelGar International Limited

- De Sangosse SAS

- Vetoquinol SA

- JT Eaton & Co., Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing focus on post-harvest loss prevention in agricultural storage

- 4.2.2 Climate-linked rodent population surges in temperate grain belts

- 4.2.3 Consolidation of farm-management service providers

- 4.2.4 Internet of Things (IoT)-enabled bait-station telemetry adoption

- 4.2.5 Gene-edited cereal cultivars increasing rodent palatability

- 4.2.6 Environmental, Social, and Governance (ESG) Guidelines set by asset owners for managing vertebrate pest welfare

- 4.3 Market Restraints

- 4.3.1 Regulatory push for bio-secure food supply chains

- 4.3.2 Escalating multi-species resistance to first-generation actives

- 4.3.3 Community-led bans after raptor secondary-poisoning events

- 4.3.4 Volatile vitamin K antidote precursor pricing

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 First-generation anticoagulants

- 5.1.2 Second-generation anticoagulants

- 5.2 By Formulation

- 5.2.1 Pellets

- 5.2.2 Blocks

- 5.2.3 Powders

- 5.2.4 Liquids

- 5.3 By Application

- 5.3.1 Cereals and Grains

- 5.3.2 Oilseeds and Pulses

- 5.3.3 Fruits and Vegetables

- 5.3.4 Other Applications

- 5.4 By Distribution Channel

- 5.4.1 Direct (Manufacturers to Co-operatives)

- 5.4.2 Agro-chemical Retailers

- 5.4.3 Online Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Japan

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Syngenta Group

- 6.4.4 UPL Limited

- 6.4.5 Reckitt Benckiser Group plc

- 6.4.6 Rentokil Initial plc

- 6.4.7 Anticimex AB

- 6.4.8 Neogen Corporation

- 6.4.9 Kemin Industries, Inc.

- 6.4.10 Fumakilla Limited

- 6.4.11 Bell Laboratories, Inc.

- 6.4.12 PelGar International Limited

- 6.4.13 De Sangosse SAS

- 6.4.14 Vetoquinol SA

- 6.4.15 JT Eaton & Co., Inc.

7 Market Opportunities and Future Outlook

抗凝血滅鼠劑市場:全球市場預測(2026-2032 年)滅鼠劑市場:依作用機制、劑型、活性成分、應用、通路和最終用戶分類-2026-2032年全球市場預測

抗凝血滅鼠劑市場:全球市場預測(2026-2032 年)滅鼠劑市場:依作用機制、劑型、活性成分、應用、通路和最終用戶分類-2026-2032年全球市場預測 非抗聚集性滅鼠劑市場規模、佔有率和成長分析:按產品類型、劑型、活性成分、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

非抗聚集性滅鼠劑市場規模、佔有率和成長分析:按產品類型、劑型、活性成分、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 滅鼠劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用方式、囓齒動物類型、最終用途、地區和競爭格局分類,2021-2031年

滅鼠劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用方式、囓齒動物類型、最終用途、地區和競爭格局分類,2021-2031年 滅鼠劑市場:依產品、劑型、應用及地區分類

滅鼠劑市場:依產品、劑型、應用及地區分類 全球滅鼠劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球滅鼠劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球滅鼠劑市場報告

2026年全球滅鼠劑市場報告 滅鼠劑市場規模、佔有率和趨勢分析報告:按產品、劑型、應用、地區和細分市場預測,2026-2033年全球Bromadiolone市場-2026-2031年預測

滅鼠劑市場規模、佔有率和趨勢分析報告:按產品、劑型、應用、地區和細分市場預測,2026-2033年全球Bromadiolone市場-2026-2031年預測 滅鼠劑市場規模、佔有率和成長分析(按類型、應用方法、最終用途、目標囓齒動物種類和地區分類)-2026-2033年產業預測

滅鼠劑市場規模、佔有率和成長分析(按類型、應用方法、最終用途、目標囓齒動物種類和地區分類)-2026-2033年產業預測