|

市場調查報告書

商品編碼

2062039

物聯網基礎設施安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IoT Infrastructure Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

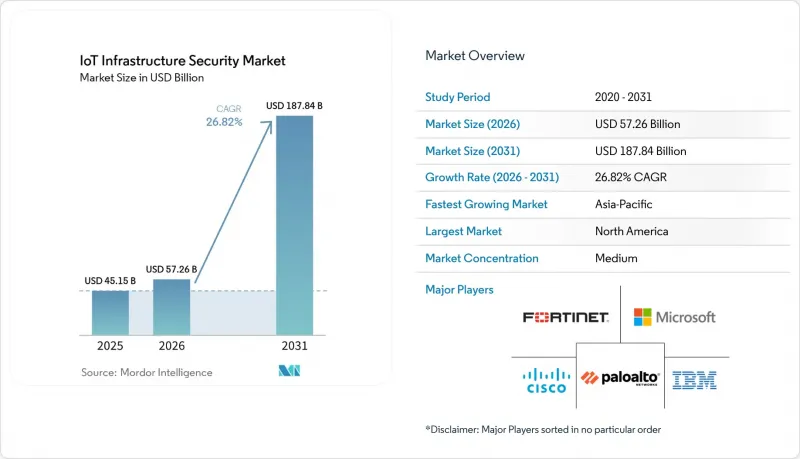

根據 Mordor Intelligence 預測,物聯網基礎設施安全市場規模將從 2025 年的 451.5 億美元成長到 2026 年的 572.6 億美元,到 2031 年達到 1878.4 億美元,2026 年至 2031 年的複合年成長率為 26.82%。

本報告按安全類型(網路安全、終端安全等)、部署方式(本地部署、雲端部署等)、基礎架構層(設備層/終端層等)、組織規模(大型企業、中小企業)、產業(製造業、醫療保健等)和地區進行細分。市場預測以美元計價。

全球物聯網基礎設施安全市場趨勢與洞察

物聯網大規模部署導致攻擊面擴大

互聯設備的龐大規模正在改變整個物聯網基礎設施安全市場的網路防禦經濟格局。 Vectra AI 的報告顯示,2025 年 1 月至 10 月期間,物聯網攻擊數量將達到 136 億次,並指出超過 50% 的連網裝置出廠時就存在嚴重的韌體漏洞。設備數量的不斷成長和預設安全措施的薄弱使得手動修補和庫存管理流程在企業環境中變得越來越不切實際。因此,市場對自動化資產發現、設備身分管理、網路分段和零信任實施的需求日益成長,尤其是在存在大量未管理或管理不善設備的環境中。 Palo Alto Networks 也強調,過去一年中暴露的設備數量增加了 332%,並指出 70% 的網路安全事件源自 IT 環境,並透過未受保護的物聯網入口點發動攻擊。這解釋了為什麼物聯網基礎設施安全市場仍然是成長最強勁的引擎。

OT網路和IT網路的融合提高了安全需求。

OT(營運技術)和IT網路的整合加劇了物聯網基礎設施安全市場的風險。企業端發生的事件現在可以直接影響工廠、公共產業和基礎設施的運作。 SANS的研究表明,58%的初始ICS(工業控制系統)和OT攻擊始於IT系統入侵,這凸顯了企業和營運環境之間的深度互聯。共用憑證、互聯通訊路徑和集中式管理工具雖然提高了效率,但也造成了通用的攻擊入口,例如網路釣魚和易受攻擊的遠端訪問,這可能會危及關鍵的生產系統。這迫使OT和IT團隊共用責任,推動從孤立的工具轉向具有更廣泛可見性和策略控制的整合平台。隨著越來越多的營運商建立整合環境,物聯網基礎設施安全市場正在見證大規模,這些合約將偵測、監控、分段、合規性報告和託管回應整合到單一採購決策中。

用於傳統工業資產的安全預算有限

傳統工業資產的更換成本對許多業者而言仍然過高,這阻礙了物聯網基礎設施安全市場的發展。據 TXOne Networks 稱,僅更換一套傳統工業控制系統,硬體成本可能高達 240 萬美元,需要六個月的重新檢驗期,並導致兩週的生產停產。 SANS 的一項調查也顯示,34% 的受訪者不清楚其整體安全預算的分配情況,41% 的受訪者僅將總預算的 0-25% 用於工業控制系統 (ICS) 和營運技術 (OT) 安全。在這種情況下,即使經營團隊意識到過時的控制系統和較長的資產生命週期所帶來的風險,也難以全面現代化。虛擬修補程式、被動監控和網路微隔離等替代控制措施可以延長安全運作時間,但它們的採用仍取決於能否證明其營運效益,而這正是阻礙物聯網基礎架構安全市場成長的因素。

細分市場分析

到 2025 年,網路安全將佔物聯網基礎設施安全市場的 35.4%,反映出物聯網從連接層開始就持續面臨風險。路由器、閘道器和其他面向網路的元件仍然是企業識別未管理設備、隔離風險行為和遏制橫向移動的第一道防線。對於許多買家而言,初始投資仍然集中於可見性、分段和協議感知監控,因為這些功能能夠在各種混合設備環境中立即產生價值。網路安全格局表明,買家仍然將網路層視為大規模物聯網防禦的主要實施基礎。物聯網基礎設施安全市場的整體趨勢也表明,企業正在從傳統的邊界防禦工具轉向能夠以線速分析工業流量的網路發現和回應平台。

雲端安全是成長最快的安全領域,預計到 2031 年將以 31.2% 的複合年成長率成長。這主要歸因於企業對集中管理、持續更新和託管支援的需求日益成長。這種成長與雲端原生零信任模型密切相關,該模型能夠更有效率地協調跨分散式位置的策略管理、裝置上下文和自動回應。 Palo Alto Networks 已將其傳統的物聯網安全入口網站遷移到 Strata Cloud Manager 中的「裝置安全」模組,並將入口網站的關閉日期設定為 2026 年 8 月。這表明領先的供應商正在將檢測、分類、虛擬修補程式和合規性報告整合到共用工作流程中。端點安全性、應用程式安全性和其他類別持續產生顯著需求,尤其是在人工智慧應用、非託管設備和受監管工作負載不斷擴展的情況下。在此背景下,物聯網基礎設施安全市場顯然正在向一個跨網路、端點、應用程式和雲端控制功能共用資產資訊的整合平台轉型。

到 2025 年,基於雲端的採用將佔總收入的 57.2%,這表明集中式可視性和訂閱模式在物聯網基礎設施安全市場仍然極具吸引力。主導的雲端採用反映了買家對彈性分析、整合威脅情報和快速功能交付的重視。這種模式對那些不希望在每個站點、工廠或分店都建立大規模內部安全團隊的公司尤其具有吸引力。雲端交付也與人工智慧驅動的安全工具日益成長的作用相契合,這些工具受益於持續的模型更新以及在供應商管理的環境中聚合大量遙測資料。將於 2026 年 2 月發布的 AWS Security Hub Extended 將進一步推動這一趨勢,它將來自 AWS保全服務和精選合作夥伴解決方案的洞察整合到一個具有標準化輸出和統一收費結構的單一介面中。

混合部署是成長最快的模式,預計到 2031 年將以 32.2% 的複合年成長率成長。這是因為許多業者仍然需要空氣間隙或嚴格控制的 OT 環境。這些買家並非拒絕雲端的經濟優勢,而是希望將本地控制與集中式威脅情報和策略管理結合。實際上,混合架構允許企業在本地維護安全關鍵流程和高度敏感的工作負載,同時利用異地工具進行分析、編配和報告。在國防、公共產業和一些醫療保健環境中,由於主權、彈性或內部策略的限制,雲端的廣泛使用仍然受到限制,因此本地部署仍然非常重要。因此,物聯網基礎設施安全市場正處於整合本地和雲端的過渡階段,而不是簡單地從本地遷移到雲端。

區域分析

北美地區繼續保持其在區域內最大的市場佔有率,在2025年佔據38.6%的市場佔有率。這反映了該地區成熟的企業安全預算、高度的監管密度以及在物聯網基礎設施安全市場中對關鍵基礎設施的廣泛應用。此外,該地區還受益於大量的公共網路安全支出,以滿足更廣泛生態系統的需求。美國國防部在2026會計年度為其網路安全計畫撥款83.1億美元,而美國網路安全和基礎設施安全局(CISA)在其持續診斷和緩解(CDM)計畫中製定了2026會計年度物聯網和營運技術(OT)資產管理的里程碑目標。預計到2030年,北美地區的5G物聯網連接數量將從2025年的500萬增加到3,900萬,這將擴大對安全邊緣連接的需求,同時也擴大供應商和通訊業者的攻擊面。在加拿大,OT 和 ICS 的預算分配更加謹慎,這為管理服務供應商和採用門檻較低的平台服務創造了機會。

歐洲在物聯網基礎設施安全市場擁有最嚴格的合規環境。這主要歸功於多個關鍵數位和營運安全框架的同步發展。 NIS2、《網路彈性法案》(Cyber Resilience Act)、DORA 和《無線電設備指令》(Radio Equipment Directive) 構成了一套多層次的要求體系,影響著該地區銷售連網產品的通訊業者、製造商和供應商。在德國,KRITIS 相關義務進一步增加了合規要求,擴大了課責範圍,並將安全性更深入地融入關鍵基礎設施的規劃階段。這種結構使得合規期限成為採購決策的直接促進因素,尤其對於那些需要在規定期限內報告漏洞、強化產品並建立正式管治流程的設備製造商和營運商而言更是如此。

在亞太地區,物聯網(IoT)基礎設施安全市場預計到2031年將以32.2%的複合年成長率成長,這反映了製造業和智慧基礎設施部署規模的擴大以及新計畫快速湧現。日本仍然是一個重要的市場,因為通訊業者將安全視為連接本身不可或缺的一部分。例如,NTT Docomo Business計劃於2025年12月推出“docomo business SIGN”,該服務整合了物聯網服務的安全功能。雖然南美、中東和非洲的市場規模較小,但成長勢頭強勁,因為工業數位化和智慧城市規劃促使安全措施比以往更早融入新計畫中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 物聯網大規模部署導致攻擊面擴大

- OT網路和IT網路的融合提高了安全需求。

- 5G賦能的物聯網的興起正在推動以邊緣為中心的安全發展。

- 諸如美國《物聯網網路安全改進法案》之類的監管要求

- 將人工智慧驅動的異常檢測功能整合到物聯網終端中

- 開發中國家物聯網平台的快速成長

- 市場限制因素

- 傳統工業資產的安全預算限制

- 物聯網生態系中標準的碎片化

- 物聯網領域缺乏具備專業網路安全知識的人員

- 實施多層安全措施的複雜度很高

- 產業價值鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按安全類型

- 網路安全

- 端點安全

- 應用程式安全

- 雲端安全

- 其他安全類型

- 按部署模式

- 現場

- 基於雲端的

- 混合

- 基礎設施層

- 設備/端點層

- 連線/網路層

- 邊緣/霧層

- 雲端和資料中心層

- 應用/平台層

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- 製造業

- 衛生保健

- 能源公用事業

- 運輸/物流

- 智慧城市和基礎設施

- 物聯網在零售和消費領域的應用

- BFSI

- 政府/國防

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- McAfee LLC

- Amazon Web Services Inc.

- Huawei Technologies Co. Ltd.

- Armis Inc.

- Broadcom Inc.(Symantec Enterprise Division)

- Thales Group

- Kaspersky Lab

- Forescout Technologies Inc.

- Rapid7 Inc.

- Zscaler Inc.

- Akamai Technologies Inc.

- Darktrace plc

- Claroty Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the ioT infrastructure security market size is expected to increase from USD 45.15 billion in 2025 to USD 57.26 billion in 2026 and reach USD 187.84 billion by 2031, growing at a CAGR of 26.82% over 2026-2031.

This report is Segmented by Security Type (Network Security, Endpoint Security, and More), Deployment (On-Premises, Cloud-Based, and More), Infrastructure Layer (Device/Endpoint Layer, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Healthcare, and More), and Geography. The Market Forecasts Provided in Terms of Value (USD).

Global IoT Infrastructure Security Market Trends and Insights

Increasing Attack Surface Due to Massive IoT Adoption

The scale of connected device growth is changing the economics of cyber defense across the IoT infrastructure security market. Vectra AI reported 13.6 billion IoT attacks between January and October 2025, and it also noted that more than 50% of connected devices ship with critical firmware vulnerabilities.That mix of rising device counts and weak default security makes manual patching and manual inventory processes increasingly unworkable in enterprise environments. The result is a stronger demand for automated asset discovery, device identity controls, network segmentation, and zero-trust enforcement, especially in environments with large fleets of unmanaged or lightly managed devices. Palo Alto Networks also highlighted a 332% rise in exposed devices over the past year and stated that 70% of cyber incidents originated in IT environments through unprotected IoT entry points, which helps explain why this remains the strongest growth engine in the IoT infrastructure security market.

Convergence of OT and IT Networks Elevating Security Needs

The convergence of OT and IT networks is increasing risk in the IoT infrastructure security market, as events that begin on the corporate side can now spread directly into plant, utility, and infrastructure operations. SANS research found that 58% of initial ICS and OT attacks began as IT compromises, underscoring how deeply enterprise and operational environments are now linked.Shared credentials, connected communication paths, and centralized management tools improve efficiency, but they also create common entry points, such as phishing or weak remote access, that can compromise critical production systems. This forces OT and IT teams to share accountability for outcomes, and that change is supporting a move away from isolated tools toward unified platforms with broader visibility and policy control. As more operators build converged environments, the IoT infrastructure security market is seeing larger enterprise deals that bundle discovery, monitoring, segmentation, compliance reporting, and managed response into a single buying decision.

Limited Security Budgets for Legacy Industrial Assets

Legacy industrial assets slow the IoT infrastructure security market because the cost of replacement is still too high for many operators. TXOne Networks stated that replacing a single legacy industrial control system can cost USD 2.4 million in hardware alone, require 6 months of revalidation, and create 2 weeks of production downtime. SANS research also showed that 34% of respondents were unsure about their overall security budget allocations, while 41% allocated only 0-25% of their total budgets to ICS and OT security. Those conditions make full modernization difficult, even when leadership understands the risk exposure tied to older control systems and long asset life cycles. Compensating controls such as virtual patching, passive monitoring, and network microsegmentation can extend the secure operating life, but adoption still depends on proving operational returns, which tempers growth in the IoT infrastructure security market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates such as US IoT Cybersecurity Improvement Act

- Integration of AI-Powered Anomaly Detection in IoT Endpoints

- Fragmented Standards Across IoT Ecosystem

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network security retained 35.4% of the IoT infrastructure security market in 2025, a position that reflects the continued exposure that begins at the connectivity layer. Routers, gateways, and other network-facing components remain the first point of control when enterprises try to identify unmanaged devices, isolate risky behavior, and contain lateral movement. For many buyers, the first wave of spending still goes to visibility, segmentation, and protocol-aware monitoring because those functions create immediate value across mixed device estates. Network security indicates that buyers still treat the network layer as the primary enforcement plane for large-scale IoT defense. The broader direction of the IoT Infrastructure Security Market also shows that organizations are shifting away from traditional perimeter tools toward network detection and response platforms that can analyze industrial traffic at wire speed.

Cloud security is the fastest-growing security type, with a projected CAGR of 31.2% through 2031, because enterprises increasingly want centralized operations, continuous updates, and managed support. This growth is closely tied to cloud-native zero-trust models, where policy management, device context, and automated response can be coordinated more efficiently across distributed sites. Palo Alto Networks moved its legacy IoT Security portal into Device Security within Strata Cloud Manager, setting August 2026 as the portal's shutdown date, demonstrating how leading vendors are consolidating discovery, classification, virtual patching, and compliance reporting into shared workflows. Endpoint security, application security, and other categories continue to drive meaningful demand, especially as AI-enabled applications, unmanaged devices, and regulated workloads expand. Across this mix, the IoT infrastructure security market is clearly moving toward unified platforms that share asset intelligence across network, endpoint, application, and cloud controls.

Cloud-based deployments accounted for 57.2% of revenue in 2025, confirming that centralized visibility and subscription economics remain highly attractive in the IoT infrastructure security market. Cloud-based deployment that leads reflects the value buyers place on elastic analytics capacity, integrated threat intelligence, and faster feature delivery. This model is especially appealing to enterprises that do not want to build large in-house security teams for every site, plant, or branch. Cloud delivery also aligns with the growing role of AI-driven security tools, which benefit from continuous model updates and broad telemetry pooling within vendor-managed environments. AWS Security Hub Extended, launched in February 2026, supports that direction by combining findings from AWS security services and curated partner solutions into a single interface with standardized outputs and unified billing.

Hybrid deployment is the fastest-growing model, with a projected CAGR of 32.2% through 2031, because many operators still need air-gapped or tightly controlled OT environments. These buyers are not rejecting cloud economics; they are blending local control with centralized threat intelligence and policy management. In practice, a hybrid architecture helps enterprises keep safety-critical processes and sensitive workloads on-site while using off-site tools for analysis, orchestration, and reporting. On-premises deployment remains relevant in defense, utilities, and some healthcare environments where sovereignty, resilience, or internal policy still limit wider cloud use. The IoT infrastructure security market is therefore undergoing a blended transition rather than a simple shift from on-premises to the cloud.

Geography Analysis

North America retained the largest regional position, with a 38.6% share in 2025, reflecting the region's mature enterprise security budgets, regulatory density, and broad critical infrastructure exposure in the IoT Infrastructure Security Market. The region also benefits from substantial public cybersecurity spending that supports broader ecosystem demand. The US Department of Defense allocated USD 8.31 billion to cybersecurity programs in fiscal year 2026, while CISA set out fiscal year 2026 milestones for IoT and OT asset management within the Continuous Diagnostics and Mitigation program. Business 5G IoT connections in North America are expected to rise from 5 million in 2025 to 39 million by 2030, expanding both demand for secure edge connectivity and the attack surface for vendors and operators. Canada offers an opportunity of a different kind because more cautious OT and ICS budget allocation leaves room for managed service providers and lower-friction platform offerings.

Europe presents the most demanding compliance environment in the IoT Infrastructure Security Market, as several major digital and operational security frameworks are advancing simultaneously. NIS2, the Cyber Resilience Act, DORA, and the Radio Equipment Directive create a layered set of requirements that affect operators, manufacturers, and vendors selling connected products into the region. Germany adds another layer through KRITIS-related obligations that broaden accountability and push security deeper into essential infrastructure planning. This structure is making compliance timelines a direct buying trigger, especially for device manufacturers and operators that need vulnerability reporting, product hardening, and formal governance processes in place before deadlines arrive.

Asia-Pacific is projected to expand at a 32.2% CAGR in the Internet of Things (IoT) infrastructure security market through 2031, reflecting both the scale of deployment and the speed of new project formation in manufacturing and smart infrastructure. Japan remains important because telecom operators are positioning security as part of connectivity itself, as shown by NTT Docomo Business launching docomo business SIGN in December 2025, with built-in security features for IoT services. South America, the Middle East, and Africa represent a smaller base, but the direction is strong because industrial digitization and smart city programs are bringing security into new projects much earlier than before.

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- McAfee LLC

- Amazon Web Services Inc.

- Huawei Technologies Co. Ltd.

- Armis Inc.

- Broadcom Inc. (Symantec Enterprise Division)

- Thales Group

- Kaspersky Lab

- Forescout Technologies Inc.

- Rapid7 Inc.

- Zscaler Inc.

- Akamai Technologies Inc.

- Darktrace plc

- Claroty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Attack Surface Due to Massive IoT Adoption

- 4.2.2 Convergence of OT and IT Networks Elevating Security Needs

- 4.2.3 Emergence of 5G-Enabled IoT Driving Edge-Focus Security

- 4.2.4 Regulatory Mandates Such as US IoT Cybersecurity Improvement Act

- 4.2.5 Integration of AI-Powered Anomaly Detection in IoT Endpoints

- 4.2.6 Rapid Growth of IIoT Platforms in Developing Economies

- 4.3 Market Restraints

- 4.3.1 Limited Security Budgets for Legacy Industrial Assets

- 4.3.2 Fragmented Standards Across IoT Ecosystem

- 4.3.3 Skill Shortage in IoT-Specific Cybersecurity Expertise

- 4.3.4 High Implementation Complexity for Multi-Layer Security

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Security Type

- 5.1.1 Network Security

- 5.1.2 Endpoint Security

- 5.1.3 Application Security

- 5.1.4 Cloud Security

- 5.1.5 Other Security Types

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Infrastructure Layer

- 5.3.1 Device / Endpoint Layer

- 5.3.2 Connectivity / Network Layer

- 5.3.3 Edge / Fog Layer

- 5.3.4 Cloud and Data Center Layer

- 5.3.5 Application / Platform Layer

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Healthcare

- 5.5.3 Energy and Utilities

- 5.5.4 Transportation and Logistics

- 5.5.5 Smart Cities and Infrastructure

- 5.5.6 Retail and Consumer IoT

- 5.5.7 BFSI

- 5.5.8 Government and Defense

- 5.5.9 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Palo Alto Networks Inc.

- 6.4.5 Fortinet Inc.

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 Trend Micro Incorporated

- 6.4.8 McAfee LLC

- 6.4.9 Amazon Web Services Inc.

- 6.4.10 Huawei Technologies Co. Ltd.

- 6.4.11 Armis Inc.

- 6.4.12 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.13 Thales Group

- 6.4.14 Kaspersky Lab

- 6.4.15 Forescout Technologies Inc.

- 6.4.16 Rapid7 Inc.

- 6.4.17 Zscaler Inc.

- 6.4.18 Akamai Technologies Inc.

- 6.4.19 Darktrace plc

- 6.4.20 Claroty Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment