|

市場調查報告書

商品編碼

2062028

400系列不鏽鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Stainless Steel 400 Series - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

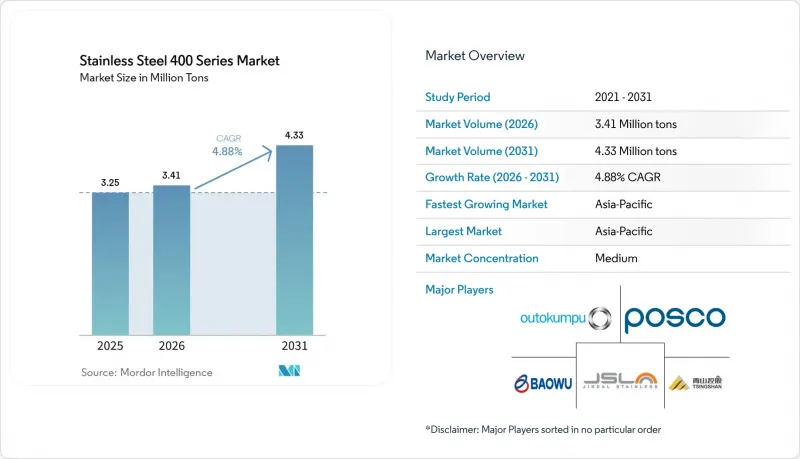

根據 Mordor Intelligence 預測,400 系列不鏽鋼的市場規模預計將從 2025 年的 325 萬噸增加到 2026 年的 341 萬噸,到 2031 年達到 433 萬噸。

預計 2026 年至 2031 年的年複合成長率(CAGR)為 4.88%。

本報告按鋼材等級(409、410 及其他)、產品類型(板材、捲材及其他)、應用領域(汽車排氣系統及其他)、終端用戶行業(汽車及交通運輸、建築及其他)以及地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

全球400係不鏽鋼市場趨勢及洞察

建築和基礎設施支出增加

中國2026年中央預算包括7,550億元人民幣(約1,092.2億美元)用於城市建設累計,以及8,000億元人民幣(約1,157.3億美元)用於發行超長期政府債券,這些債券優先考慮不銹鋼結構產品,從而提振了橋樑、輸水管道和公共運輸維修等領域對鐵素鋼體的需求。 430牌號的不鏽鋼含鉻量為16-18%,兼具優異的耐腐蝕性和成形性,正在橋面和農業機械領域取代鍍鋅鋼。印度的生產連結獎勵計畫計畫對長條類產品的增量銷售提供4-15%的補貼,鼓勵新建鐵素體鐵廠。中國農村供水安全計畫的推進,透過將不銹鋼管道推廣到先前缺乏供水基礎設施的地區,擴大了潛在市場規模。沿岸地區和東南亞的大型企劃正在擴大其地理範圍,但它們的實施仍然取決於公共財政週期和投入價格的穩定性。

在鎳價波動的情況下,與奧氏體鋼相比具有成本優勢

409級鎳礦的交易價格為每噸1800至2200美元,而304級鎳礦的交易價格為每噸3000至3500美元。當鎳價超過每噸18,000美元時,這一價格差距將進一步擴大。印尼供應全球約70%的鎳礦,在2026年配額收緊後,鎳價從2021年的尖峰時段下跌了40%,目前已回升。含鎳量極低或不含鎳的鐵素體鋼不會對原始設備製造商(OEM)的預算造成壓力,反而刺激了排氣系統、家用電器面板和軋延原料等領域的替代需求。隨著鎳價下跌,奧氏體鋼在耐腐蝕性要求較高的領域重新奪回市場佔有率,終端市場的價格彈性驅動的價格波動也變得更加明顯。

鉻和鉻鐵的價格波動

2026年初,印度鉻鐵價格達到每噸74,000至75,000印度盧比(約784.17至794.77美元)。同時,由於南非減產導致供應受限,中國的進口報價約為每磅0.84美元。碳邊境調節機制(CBAM)對檢驗的進口產品採用3.5至4噸的預設二氧化碳(CO2)係數,導致高爐不銹鋼被徵收課稅,電弧爐(EAF)產品溢價上漲。為因應潛在的價格波動,中國國有礦業公司已從海外採購超過5億噸鉻鐵礦。隨著鉻鐵價格上漲,沒有自有礦產資源的鋼鐵廠面臨利潤率壓力,促使垂直一體化生產商之間進行整合。

細分市場分析

截至2025年,409牌號不鏽鋼將佔400系列不鏽鋼市佔率的41.11%,預計到2031年將以5.45%的複合年成長率成長。 409牌號不鏽鋼具有優異的耐熱性(可耐受高達600度C的氣體),這得益於其10.5-11.75%的鉻含量以及僅為304牌號不銹鋼一半的價格,因此其在汽車排氣管領域的市場規模得以支撐。 430牌號不銹鋼在家用電器和建築板材市場的需求不斷成長,這主要得益於中國電力更換補貼政策的推動。馬氏體410、420和440牌號不銹鋼的硬度可達55 HRC或更高,因此帶動了外科器械和工業刀具的需求。 446 鋼種是一種小眾鋼種,其鉻含量為 23-27%,用於爐襯和熱交換器,但面臨較高的合金附加費。

新型鐵素體鋼牌號,例如T4003和SOLEIL 4003,透過將鉻含量控制在13%或以下,並添加鈦穩定劑,提高了列車車體和橋面板的焊接性和延展性。日本製鐵的取得專利的表面活化處理技術增強了氧化膜的穩定性,將600 度C下氧化引起的重量增加抑制至0.3 mg/cm²,並延長了潮濕環境下熱交換器的使用壽命。製造商們正日益注重產品差異化,不僅體現在金屬結構上,也體現在塗層和酸洗技術方面。

到2025年,板材將佔總銷售量的42.32%,這主要得益於消費性電子產品外殼、覆層和汽車面板等領域對光滑表面和精確厚度的要求。鋼筋預計將實現最高的複合年成長率(CAGR),達到5.67%,這主要受精密加工閥門和齒輪以及含硫量為0.15%至0.30%的易切削416級鋼的需求驅動。卷材滿足了服務中心和復軋延的需求,尤其注重多噸批次產品化學成分的一致性。管材服務於建築和能源行業,而厚度為0.1毫米或更薄的箔材則用於固體氧化物燃料電池(SOFC)和電解槽堆,在400系列不銹鋼市場中形成了一個高利潤細分市場。

中國鋼鐵企業正在提升產業標竿。撫順鋼鐵透過巨量資料控制將鋼板精度提高了65%;溧陽德龍運作全球最寬的2680毫米軋延機;山西福建引進了1550毫米20輥軋延機,實現了微米級公差。 2B至8K表面光潔度可帶來10%至30%的溢價,這推動了拋光製程的投資。電弧直接能量沉積(DED)技術在大規模修復中可減少78%的原料用量,但與傳統軋延相比,其板材加工效率仍較低,傳統軋延仍是主流製程。

區域分析

預計到2025年,亞太地區將佔全球不鏽鋼產量的52.34%,並在2031年前以5.72%的複合年成長率持續成長。這主要得益於中國7,550億元人民幣(約1,092.2億美元)的基礎建設預算以及2,500億元人民幣(約361.6億美元)的家電以舊換新計畫。到2024年,中國三大鋼廠的不銹鋼產量將佔全球總產量的67.30%,這將鞏固市場供應並提升其議價能力。印度的運轉率徘徊在其750萬噸總產能的60%左右,這意味著鐵素體鋼的增產空間仍然存在。此外,金達爾集團在印尼的120萬噸煉鋼廠正在增強該地區的鋼鐵自給能力。浦項鋼鐵與青山集團在印尼的合資企業正在利用其自有礦石新增200萬噸產能,這將使印尼成為一個低成本的鋼鐵生產中心。

儘管409不銹鋼在美國汽車產業中仍佔據主導地位,但電動車的普及正在減少每輛車所需的不銹鋼用量。美國、加拿大和墨西哥之間錯綜複雜的關稅使貿易更加複雜,促使買家轉向區域性鋼廠。

歐洲正面臨碳邊境調節機制(CBAM),該機制透過設定預設的二氧化碳係數,推高了高排放進口產品的成本。 Autokump公司斥資2億歐元(約2.2965億美元)對其位於托爾尼奧的工廠維修,重點在於將其生產線改造為生產雙相鋼和沈澱硬化鋼。同時,Acerinox和Aperham公司正投資1.6億歐元(約1.8372億美元)以應對疲軟的需求,降低能源消耗。德國和北歐國家在電解槽的應用方面處於主導,尤其偏好金屬雙極板電解槽。儘管面臨外匯風險,南美洲、中東和非洲地區的市場佔有率仍然較小,但受益於當地消費性電子產品和建築業的需求。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築和基礎設施支出增加

- 鎳價波動下奧氏體鋼的成本優勢

- 擴大在廚具和家用電器的應用

- 在電解槽採用雙極板製取綠色氫氣

- 固體氧化物燃料電池和金屬支撐電池對超薄鐵氧體箔的需求

- 市場限制因素

- 鉻和鉻鐵價格波動

- 積層製造中的裂痕和製造品質問題

- 由於碳邊境調整和生命週期二氧化碳排放法規,合規成本增加。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 409

- 410

- 420

- 430

- 440

- 其他等級(446,其他)

- 依產品類型

- 座板

- 線圈

- 鋼筋和鋼條

- 管道和管材

- 其他產品類型(超薄箔等)

- 透過使用

- 汽車排氣系統

- 廚房用具和烹飪用具

- 工業設備

- 建築/建築設計

- 家用電器

- 發電

- 其他應用(氫電解槽板等)

- 按最終用途行業分類

- 汽車和交通運輸

- 建築/施工

- 消費品

- 工業機械

- 能源和發電

- 航太/國防

- 其他終端用戶產業(醫療保健等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- Strategic Initiatives

- 市佔率和排名分析

- 公司簡介

- Acerinox

- Aperam

- Baosteel Desheng Stainless Steel Co., Ltd.

- Eternal Tsingshan Group Co., Ltd.

- Fushun Special Steel Co., Ltd.

- Jindal Steel

- NIPPON STEEL CORPORATION

- Outokumpu

- POSCO

- Shanxi Taigang Stainless

- Shyam Metalics

- Viraj Profiles Pvt. Ltd.

- Yieh Corp.

- China Baowu Steel Group

- TSINGSHAN HOLDING GROUP

第7章 市場機會與未來展望

According to Mordor Intelligence, the stainless steel 400 series market size is projected to grow from 3.25 million tons in 2025 to 3.41 million tons in 2026 to reach 4.33 million tons by 2031, growing at a CAGR of 4.88% from 2026 to 2031.

This report is Segmented by Grade (409, 410, and More), Product Type (Sheets and Plates, Coils, and More), Application (Automotive Exhaust Systems, and More), End-Use Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Stainless Steel 400 Series Market Trends and Insights

Growth in Construction and Infrastructure Spending

China's 2026 central budget sets aside CNY 755 billion (USD 109.22 billion) for municipal works and CNY 800 billion (USD 115.73 billion) in ultra-long treasury bonds that favor stainless structural products, propelling demand for ferritic grades in bridges, water pipelines, and public-transit upgrade. Grade 430, with 16-18% chromium, replaces galvanized steels in bridge decks and agricultural equipment because it balances corrosion resistance and formability. India's production-linked incentive scheme grants 4-15% on incremental stainless long-product sales, encouraging new ferritic melt shops. Rural water-safety rollouts in China extend stainless piping into previously untreated counties, enlarging the addressable base. Mega-projects in the Gulf and Southeast Asia broaden geographic exposure, though execution still hinges on public-finance cycles and input-price stability.

Cost Advantage Over Austenitic Grades Amid Nickel Volatility

Grade 409 trades at USD 1,800-2,200 per ton versus USD 3,000-3,500 for 304, a gap that widens when nickel surpasses USD 18,000 per ton. Indonesia supplies roughly 70% of global nickel ore, yet stricter 2026 quotas revived pricing after a 40% slide from 2021 peaks. Ferritic grades, containing little to no nickel, insulate OEM budgets and trigger substitution in exhausts, appliance panels, and re-rollers' feedstock. When nickel retreats, austenitic grades claw back share where higher corrosion thresholds are essential, underscoring a price-elastic see-saw across end markets.

Chromium and Ferrochrome Price Volatility

In early 2026, India's ferrochrome prices reached INR 74,000-75,000 (USD 784.17-794.77) per ton. Meanwhile, Chinese import offers were around USD 0.84 per pound, reflecting supply constraints due to production curtailments in South Africa. The Carbon Border Adjustment Mechanism (CBAM) applies default carbon dioxide (CO2) factors of 3.5-4.0 tons to unverified imports, resulting in taxes on blast-furnace stainless steel and higher Electric Arc Furnace (EAF) premiums. To address potential price fluctuations, China's state-owned mining companies secured over 500 million tons of chromite from international sources. Mills without captive ore resources face margin pressures during ferrochrome price increases, driving consolidation among vertically integrated producers.

Other drivers and restraints analyzed in the detailed report include:

- Rising Usage in Kitchenware and Home Appliances

- Adoption in Bipolar Plates for Green-Hydrogen Electrolyzers

- Additive-Manufacturing Cracking and Printability Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grade 409 accounted for 41.11% of the stainless steel 400 series market share in 2025 and is projected to expand at 5.45% CAGR to 2031. The stainless steel 400 series market size for automotive exhaust lines benefits from grade 409's 10.5-11.75% chromium chemistry that withstands 600°C gases at half the cost of 304. Grade 430 capitalizes on appliance and architectural panels, buoyed by China's appliance-trade-in bounty. Martensitic 410, 420, and 440 grades deliver greater than or equal to 55 HRC hardness, fueling surgical-instrument and industrial-knife demand. Niche grade 446 services furnace linings and heat exchangers thanks to 23-27% chromium, but trades at a higher alloy surcharge.

Emerging ferritic variants such as T4003 and SOLEIL 4003 marry smaller than or equal to 13% chromium with titanium stabilizers, improving weldability and ductility for train shells and bridge decks. Patented surface activation by Nippon Steel enhances oxide-film stability, shrinking oxidation weight gain to 0.3 mg/cm2 at 600°C and extending service life in humid heat exchangers. Producers increasingly differentiate through coating and pickling know-how rather than raw metallurgy alone.

In 2025, sheets and plates accounted for 42.32% of the volume, reflecting their application in appliance skins, cladding, and body panels that require smooth surfaces and precise gauges. Bars and rods are projected to achieve the highest compound annual growth rate (CAGR) of 5.67%, driven by demand for precision-machined valves, gears, and the free-cutting 416 variant containing 0.15-0.30% sulfur. Coils address the needs of service centers and re-rollers, focusing on consistent chemistry across multi-ton lots. Pipes and tubes cater to the construction and energy sectors, while foils thinner than 0.1 mm support solid oxide fuel cell (SOFC) and electrolyzer stacks, creating a high-margin segment within the stainless steel 400 series market.

China's mills are advancing industry benchmarks: Fushun's big-data controls have improved plate precision by 65%, Liyang Delong operates the world's widest 2,680 mm hot mill, and Shanxi Fujian has implemented a 1,550 mm 20-roll cold mill, achieving micron-level tolerances. Surface finishes ranging from 2B to 8K command premiums of 10-30%, driving investments in polishing processes. While wire-arc directed energy deposition (DED) technology reduces raw material usage by 78% during large repairs, it remains less efficient in sheet throughput compared to conventional rolling, which continues to dominate.

Geography Analysis

Asia-Pacific commanded 52.34% of 2025 volume and is advancing at a 5.72% CAGR to 2031, underscored by China's CNY 755 billion (USD 109.22 billion) infrastructure budget and CNY 250 billion (USD 36.16 billion) appliance-trade-in plan. China's top three mills captured 67.30% of 2024 stainless output, consolidating supply and raising bargaining power. India's utilization hovers near 60% against 7.5 million t capacity, giving headroom for ferritic ramp-ups; Jindal's 1.2 million ton Indonesian melt shop reinforces regional self-sufficiency. Indonesia's POSCO-Tsingshan venture adds 2 million t of captive-ore-fed capacity, positioning the archipelago as a low-cost hub.

U.S. automotive still pulls grade 409, but EV diffusion trims per-vehicle stainless loadings. Tariff layers across the U.S., Canada, and Mexico entangle trade, steering buyers toward regional mills.

Europe confronts CBAM, allocating default CO2 factors that inflate landed costs for high-emission imports. Outokumpu's EUR 200 million (USD 229.65 million) Tornio upgrade pivots to duplex and precipitation-hardened grades, while Acerinox and Aperam sink EUR 160 million (USD 183.72 million) to curb energy use amid soft demand. Germany and the Nordics spearhead electrolyzer rollouts, favoring metallic bipolar plates. South America and MEA remain smaller slices but gain from localized appliance and construction needs despite currency risk.

- Acerinox

- Aperam

- Baosteel Desheng Stainless Steel Co., Ltd.

- Eternal Tsingshan Group Co., Ltd.

- Fushun Special Steel Co., Ltd.

- Jindal Steel

- NIPPON STEEL CORPORATION

- Outokumpu

- POSCO

- Shanxi Taigang Stainless

- Shyam Metalics

- Viraj Profiles Pvt. Ltd.

- Yieh Corp.

- China Baowu Steel Group

- TSINGSHAN HOLDING GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in construction and infrastructure spending

- 4.2.2 Cost advantage over austenitic grades amid nickel volatility

- 4.2.3 Rising usage in kitchenware and home appliances

- 4.2.4 Adoption in bipolar plates for green-hydrogen electrolyzers

- 4.2.5 Demand for ultra-thin ferritic foils in solid-oxide fuel cells and metal-supported batteries

- 4.3 Market Restraints

- 4.3.1 Chromium and ferro-chrome price volatility

- 4.3.2 Additive-manufacturing cracking and printability issues

- 4.3.3 Carbon-border-adjustment and lifecycle-CO2 rules raising compliance costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 409

- 5.1.2 410

- 5.1.3 420

- 5.1.4 430

- 5.1.5 440

- 5.1.6 Other Grades (446, etc.)

- 5.2 By Product Type

- 5.2.1 Sheets and Plates

- 5.2.2 Coils

- 5.2.3 Bars and Rods

- 5.2.4 Pipes and Tubes

- 5.2.5 Other Product Types (Ultra-thin foil, etc.)

- 5.3 By Application

- 5.3.1 Automotive Exhaust Systems

- 5.3.2 Kitchenware and Cookware

- 5.3.3 Industrial Equipment

- 5.3.4 Construction and Architecture

- 5.3.5 Electrical Appliances

- 5.3.6 Energy Generation

- 5.3.7 Other Applications (Hydrogen Electrolyzer Plates, etc.)

- 5.4 By End-User Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Consumer Goods

- 5.4.4 Industrial Machinery

- 5.4.5 Energy and Power

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-user Industries (Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Acerinox

- 6.4.2 Aperam

- 6.4.3 Baosteel Desheng Stainless Steel Co., Ltd.

- 6.4.4 Eternal Tsingshan Group Co., Ltd.

- 6.4.5 Fushun Special Steel Co., Ltd.

- 6.4.6 Jindal Steel

- 6.4.7 NIPPON STEEL CORPORATION

- 6.4.8 Outokumpu

- 6.4.9 POSCO

- 6.4.10 Shanxi Taigang Stainless

- 6.4.11 Shyam Metalics

- 6.4.12 Viraj Profiles Pvt. Ltd.

- 6.4.13 Yieh Corp.

- 6.4.14 China Baowu Steel Group

- 6.4.15 TSINGSHAN HOLDING GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

不鏽鋼市場-2026-2032年全球市場預測

不鏽鋼市場-2026-2032年全球市場預測 2026-2030年全球不鏽鋼市場

2026-2030年全球不鏽鋼市場 不鏽鋼冷軋捲市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年不鏽鋼棋盤格市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年

不鏽鋼冷軋捲市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年不鏽鋼棋盤格市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年 不銹鋼市場規模、佔有率、趨勢和預測:按產品、等級、應用和地區分類,2026-2034年不銹鋼護柱市場:按產品類型、最終用戶、應用和分銷管道分類,全球預測(2026-2032年)不銹鋼校準砝碼市場按重量等級、精度等級、材料等級、最終用途行業和分銷管道分類,全球預測,2026-2032年不鏽鋼校準砝碼套裝市場(依產品類型、最終用戶、通路和材料等級分類)-全球預測,2026-2032年

不銹鋼市場規模、佔有率、趨勢和預測:按產品、等級、應用和地區分類,2026-2034年不銹鋼護柱市場:按產品類型、最終用戶、應用和分銷管道分類,全球預測(2026-2032年)不銹鋼校準砝碼市場按重量等級、精度等級、材料等級、最終用途行業和分銷管道分類,全球預測,2026-2032年不鏽鋼校準砝碼套裝市場(依產品類型、最終用戶、通路和材料等級分類)-全球預測,2026-2032年 2026-2030年全球400係不鏽鋼市場

2026-2030年全球400係不鏽鋼市場 不鏽鋼市場分析及預測(至2035年):類型、產品類型、應用、形式、材質類型、最終用戶、技術、製程、組件、安裝類型

不鏽鋼市場分析及預測(至2035年):類型、產品類型、應用、形式、材質類型、最終用戶、技術、製程、組件、安裝類型