|

市場調查報告書

商品編碼

2062015

可拉伸導電材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Stretchable Conductive Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

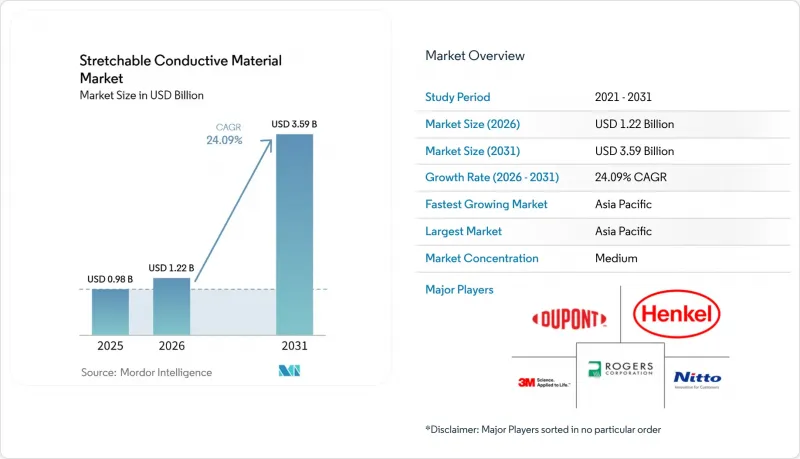

據 Mordor Intelligence 稱,2025 年可拉伸導電材料的市場規模為 9.8 億美元,預計到 2031 年將從 2026 年的 12.2 億美元成長到 35.9 億美元,預測期(2026-2031 年)的複合年成長率為 24.09%。

本報告按材料類型(石墨烯基、銀基等)、形態(油墨、薄膜/箔等)、應用(穿戴式電子產品、醫療/生物電子設備等)、最終用戶(家用電子電器、醫療等)和地區(亞太地區、北美地區、歐洲地區等)進行細分。市場預測以美元計價。

全球可拉伸導電材料市場趨勢及洞察

穿戴式電子設備和智慧紡織品的需求日益成長

隨著持續健康監測在大眾市場日益普及,可拉伸導體的地位正從專業研究應用提升至消費品領域。 2025年獲得FDA核准後,臨床級貼片式奈米銀線電極正式實用化。印製在熱塑性聚氨酯上的奈米銀線Panasonic可承受10萬次彎曲循環,使得整合於服裝的感測器能夠承受工業洗滌。工業安全法規的不斷完善也推動了對智慧紡織品的需求,例如松下公司於2025年下半年推出的用於6G天線服裝的「覆銅拉伸」材料。隨著5G頻寬運算的興起,需要能夠維持吉赫訊號品質的可拉伸互連材料,而剛性銅箔在10%或更高的拉伸率下無法應對這項挑戰。符合ISO 13485標準正引導材料選擇更重視已驗證的生物相容性和耐洗滌性,品質標準也正納入設計流程。

軟性拉伸電子技術的進步

材料科學的突破性進展正在縮小剛性矽材料和可拉伸有機材料之間的差距。瑞士洛桑聯邦理工學院(EPFL)展示了即使在300%的應變下仍能保持95%導電性的液態金屬纖維,為實現具有觸覺保真度的仿生皮膚鋪平了道路。基於MXene的應變不變裝置在0-50%的應變範圍內保持穩定的電阻,並將電子機械滯後降低至2%。韓國科學技術院(KAIST)和浦項科技大學(POSTECH)的聯合研究團隊在30%應變下實現了25%的可拉伸OLED的外部量子效率,從而將軟性顯示器的應用範圍擴展到汽車儀錶板和AR頭盔。商業性可行性的關鍵在於採用卷對卷印刷技術,以低於平方公尺5美元的成本實現亞10微米微結構,漢高和杜邦正在利用人工智慧最佳化油墨來實現這一目標。總而言之,這些進展正在拓展可拉伸導電材料的市場,使其從低電流感測器擴展到高功率密度致動器和能源採集模組。

先進奈米材料和製造技術高成本

單壁奈米碳管和石墨烯的成本分別超過每公斤500美元和200美元,因此它們的應用僅限於高階領域。一級汽車供應商的目標是將感測器模組的價格控制在每公斤2美元以下,但目前奈米材料的定價使得這一目標難以實現。精度低於5微米的捲對卷(R2R)印刷機需要超過1000萬美元的資本支出(CAPEX),這阻礙了新進者的競爭。 DexMat公司的連續碳奈米管合成技術已將成本降低至2024年的每公斤150美元,但由於加工商缺乏油墨流變學的專業知識,該技術的推廣應用較為緩慢。隨著中國和韓國的大規模製造廠達到噸級產能,預計2028年後價格壓力將有所緩解。

細分市場分析

預計2026年至2031年間,液態金屬和混合系統將以25.67%的複合年成長率成長,隨著鎵銦合金克服奈米線薄膜中濕度引起的氧化劣化問題,它們在可拉伸導電材料市場的佔有率將進一步擴大。銀基材料仍保持其主導地位,預計到2025年將佔據42.44%的市場佔有率,這得益於日東電工(Nitto Denko)對C3Nano公司1500萬美元的產能投資。石墨烯-金屬奈米薄膜展現出即使在100%應變下也能保持吉赫級穩定性的能力,從而推動了6G穿戴天線的發展。碳奈米管(CNT)受益於OCSiAl公司150噸TUBALL的生產,這使得能夠實現可靠性長達15年的電池膨脹感測器。

目前,材料的選擇因應用領域而異。生物相容性銀是醫療設備的首選材料;液態金屬因其自癒特性而被用於國防領域;銅由於成本原因成為家用電子電器的標準材料;碳奈米管-聚合物複合材料則用於軟體機器人領域,以增強柔軟性。從2027年起,隨著Panasonic「覆銅拉伸」技術確立製造設計規範,結合剛性島狀晶片和可拉伸導線的混合結構的可拉伸導電材料的市場佔有率預計將會擴大。

到2025年,油墨銷售額佔總銷售額的51.50%,主要得益於低成本網版印刷技術的應用,使得成本低於0.10美元的醫用貼片得以實現。然而,到2031年,彈性體複合材料預計將以25.74%的複合年成長率(CAGR)實現最高成長,因為原始設備製造商(OEM)需要無需投資印刷設備的層壓板模組。諸如Panasonic“FineX”之類的薄膜和箔材,在50%的拉伸率下電阻值低於10 Ω/sq,可用於折疊式顯示器的鉸鏈。膠帶和塗層則應用於研發領域,3M公司計劃在2025年推出導電膠帶,即使在20%的剪切力下,其接觸電阻仍低於1 Ω。隨著捲對卷生產能力的提升,用於軟性機器人驅動器和汽車感測器的彈性體複合複合材料中可拉伸導電材料的市場規模預計將逐漸超過油墨市場。

區域分析

預計到2025年,亞太地區將佔全球銷售額的41.6%,並在2031年之前維持25.45%的複合年成長率。這主要得益於中國對軟性顯示器的補貼、韓國效率高達25%的可拉伸OLED以及PanasonicCCS在日本的推出。垂直整合的供應鏈,例如江蘇康諾500噸的石墨烯產能和台灣超過20億美元的PCB投資,正在鞏固該地區的主導地位。雖然材料創新仍集中在東北亞,但印度和東南亞國協正在崛起為低成本組裝中心。

在北美,美國國防高級研究計劃局 (DARPA) 和美國陸軍對電子皮膚原型研發的資助正在推動這項技術的發展,預計在 2028 年前將其商業化應用於醫療和汽車領域。美國食品藥物管理局 (FDA) 的核准流程和 ISO 13485 認證工廠吸引了 3M 和杜邦等頂級供應商,這兩家公司都投入數十億美元用於研發以維持其市場佔有率。加拿大和墨西哥正效仿美國汽車產業的應用趨勢,評估用於監測電動車電池的可拉伸感測器。

歐洲的成長與強制性回收利用密切相關。 2025年修訂的IEC TC-111標準將把材料回收指標納入採購流程,這將使漢高的脫模黏合劑和賀利氏的可回收膠黏劑更具優勢。德國和法國在學術領域取得了突破性進展,而北歐國家正在職業安全領域開展試點項目,從而催生了對能夠承受工業洗滌的感測器的早期應用需求。俄羅斯的參與受到製裁的限制。南美洲和中東及非洲地區仍在發展中,但巴西的公共衛生系統和沙烏地阿拉伯的智慧城市計畫正在考慮制定降低成本的藍圖,以期在2028年後實現廣泛應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 穿戴式電子設備和智慧紡織品的需求日益成長

- 軟性拉伸電子技術的進步

- 醫療監測設備的普及

- 美國國防部資助的「電子皮膚」研發項目

- 促進可回收印刷電子產品的永續發展

- 市場限制因素

- 先進奈米材料和製造技術高成本

- 重複載重下的疲勞行為

- 由於電子機械滯後效應,感測器精度受到限制。

- 價值鏈分析

- 監理情勢

- 波特五力分析

第5章:預測市場規模與成長率

- 依材料類型

- 石墨烯基材料

- 銀質材料

- 奈米碳管(CNTs)

- 銅基材料

- 導電聚合物

- 液態金屬和混合系統

- 按形狀

- 墨水

- 薄膜

- 彈性體複合材料

- 膠帶和塗層

- 透過使用

- 穿戴式電子產品

- 醫療和生物電位設備

- 軟體機器人和驅動器

- 可拉伸顯示器和感測器

- 能量儲存和回收

- 電子皮膚和智慧紡織品

- 按最終用戶行業分類

- 家用電子產品

- 醫療保健

- 航太/國防

- 汽車和電動旅行

- 能源公用事業

- 工業自動化、運動和健身

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ACS Material

- ANP CORPORATION

- Dow

- DuPont

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- Indium Corporation

- ITOCHU Corporation

- Liquid Wire Inc.

- NextFlex

- Nissha Co., Ltd.

- Nitto Denko Corporation

- Panasonic Corporation

- Priways Co., Ltd.

- Rogers Corporation

- Shanghai Huzheng Industrial Co., Ltd.

- Sun Chemical Corporation

- TOYOBO CO., LTD.

- Vorbeck Materials Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the stretchable conductive material market size was valued at USD 0.98 billion in 2025 and is estimated to grow from USD 1.22 billion in 2026 to reach USD 3.59 billion by 2031, at a CAGR of 24.09% during the forecast period (2026-2031).

This report is Segmented by Type of Material (Graphene-Based, Silver-Based, and More), Form (Inks, Films and Foils, and More), Application (Wearable Electronics, Medical and Biopotential Devices, and More), End-User (Consumer Electronics, Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Stretchable Conductive Material Market Trends and Insights

Growing Demand for Wearable Electronics and Smart Textiles

Mass-market acceptance of continuous health tracking is elevating stretchable conductors from specialty research to consumer staples, with FDA clearances in 2025 validating silver-nanowire electrodes for clinical-grade patches. Silver-nanowire inks printed on thermoplastic polyurethane survive 100,000 flex cycles, enabling garment-integrated sensors that withstand industrial laundry. Industrial safety mandates are adding smart-textile demand, illustrated by Panasonic's Copper Clad Stretch material launched in late 2025 for 6G antenna garments. The rise of 5G edge computing requires stretchable interconnects that maintain gigahertz integrity, a task rigid copper foils cannot meet beyond 10% elongation. ISO 13485 compliance is guiding material selection toward proven biocompatibility and wash durability, embedding quality benchmarks into design workflows.

Advancements in Flexible and Stretchable Electronics

Material-science milestones are closing the gap between rigid silicon and stretchable organics. EPFL demonstrated liquid-metal fibers retaining 95% conductivity at 300% strain, opening a path to prosthetic skin with tactile fidelity. MXene-based strain-invariant devices sustain stable resistance across 0-50% strain, reducing electromechanical hysteresis to 2%. South Korea's KAIST-POSTECH consortium achieved 25% external quantum efficiency in stretchable OLEDs at 30% strain, pivoting flexible displays toward automotive dashboards and AR visors. Commercial viability hinges on roll-to-roll printing at sub-10 µm features under USD 5 per m2, targets Henkel and DuPont pursue via AI-optimized inks. These developments collectively expand the stretchable conductive material market beyond low-current sensors to power-dense actuators and energy-harvesting modules.

High Cost of Advanced Nanomaterials and Production Technology

Single-walled carbon nanotubes at USD 500 per kg and graphene above USD 200 per kg confine usage to premium sectors. Automotive Tier 1 suppliers target sub-USD 2 sensor modules, a hurdle current nanomaterial pricing cannot meet. Roll-to-roll printers with sub-5 µm registration exceed USD 10 million CAPEX, deterring entrants. DexMat's continuous CNT synthesis cut costs to USD 150 per kg in 2024, yet adoption lags as converters lack ink-rheology expertise. Price pressure will relax post-2028 when large-scale Chinese and Korean fabs reach multi-ton capacities.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Monitoring Devices Proliferation

- Defense-Funded Electronic Skin Research and Development Programs

- Performance Fatigue Under Cyclic Strain

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid metals and hybrid systems are projected to grow at 25.67% CAGR during 2026-2031 and will capture an incremental stretchable conductive material market size as gallium-indium alloys overcome humidity-induced oxidation failures in nanowire films. Silver-based materials maintain dominance with a 42.44% 2025 share, supported by Nitto Denko's USD 15 million capacity investment in C3Nano. Graphene-metal nanomembranes demonstrated gigahertz-level stability under 100% strain, advancing 6G wearable antennas. CNTs benefit from OCSiAl's 150-ton TUBALL output, enabling battery-swelling sensors that demand 15-year reliability.

Material choice now segments by end-use: medical devices prefer biocompatible silver; defense favors liquid metals for self-healing; consumer electronics default to copper for cost; soft robotics adopts CNT-polymer composites for compliance. The stretchable conductive material market share of hybrid architectures combining rigid-island chips with stretchable interconnects will widen post-2027 as Panasonic's Copper Clad Stretch formalizes manufacturing design-rules.

Inks retained 51.50% of 2025 revenue owing to low-cost screen printing that delivers sub-USD 0.10 medical patches. Yet elastomeric composites will log the highest 25.74% CAGR through 2031 as OEMs seek laminate-ready modules that bypass printer investment. Films and foils such as Panasonic's FineX provide foldable-display hinges with less than 10 Ω/sq resistance at 50% elongation. Tapes and coatings serve research and development, with 3M's 2025 conductive-tape expansion keeping less than 1Ω contact resistance under 20% shear. As roll-to-roll capacity scales, the stretchable conductive material market size for elastomeric composites in soft-robotic actuators and automotive sensors will increasingly outpace inks.

Geography Analysis

Asia-Pacific generated 41.6% of 2025 revenue and is projected to achieve a 25.45% CAGR through 2031, driven by China's flexible-display subsidies, South Korea's 25%-efficient stretchable OLEDs, and Panasonic's CCS launch in Japan. Vertically integrated supply chains, such as Jiangsu Cnano's 500-ton graphene output and Taiwan PCB investments topping USD 2 billion, anchor regional leadership. India and ASEAN nations emerge as low-cost assembly hubs, although material innovation remains Northeast-Asian-centric.

North America benefits from DARPA and U.S. Army funding of electronic-skin prototypes, pulling technologies into commercial healthcare and automotive by 2028. FDA pathways and ISO 13485 plants attract premium suppliers like 3M and DuPont, both channeling multibillion-dollar research and development to defend shares. Canada and Mexico follow U.S. automotive adoption curves, evaluating stretchable sensors for EV battery monitoring.

Europe's growth aligns with recyclability mandates; IEC TC-111's 2025 update embeds material-recovery metrics in procurement, advantaging Henkel's debonding adhesives and Heraeus's recyclable pastes. Germany and France drive academic breakthroughs, while Nordic pilots in occupational safety offer early-adopter demand for industrial-laundry-proof sensors. Sanctions limit Russia's participation; South America and MEA remain nascent, with Brazil's public health system and Saudi smart-city projects monitoring cost-down roadmaps for post-2028 uptake.

- 3M

- ACS Material

- ANP CORPORATION

- Dow

- DuPont

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- Indium Corporation

- ITOCHU Corporation

- Liquid Wire Inc.

- NextFlex

- Nissha Co., Ltd.

- Nitto Denko Corporation

- Panasonic Corporation

- Priways Co., Ltd.

- Rogers Corporation

- Shanghai Huzheng Industrial Co., Ltd.

- Sun Chemical Corporation

- TOYOBO CO., LTD.

- Vorbeck Materials Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for wearable electronics and smart textiles

- 4.2.2 Advancements in flexible and stretchable electronics

- 4.2.3 Healthcare monitoring devices proliferation

- 4.2.4 Defense-funded "electronic skin" research and development programs

- 4.2.5 Sustainability push toward recyclable printed electronics

- 4.3 Market Restraints

- 4.3.1 High cost of advanced nanomaterials and production tech

- 4.3.2 Performance fatigue under cyclic strain

- 4.3.3 Electromechanical hysteresis limiting sensor precision

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type of Material

- 5.1.1 Graphene-based Materials

- 5.1.2 Silver-based Materials

- 5.1.3 Carbon Nanotubes (CNTs)

- 5.1.4 Copper-based Materials

- 5.1.5 Conductive Polymers

- 5.1.6 Liquid Metals and Hybrid Systems

- 5.2 By Form

- 5.2.1 Inks

- 5.2.2 Films and Foils

- 5.2.3 Elastomeric Composites

- 5.2.4 Tapes and Coatings

- 5.3 By Application

- 5.3.1 Wearable Electronics

- 5.3.2 Medical and Biopotential Devices

- 5.3.3 Soft Robotics and Actuators

- 5.3.4 Stretchable Displays and Sensors

- 5.3.5 Energy Storage and Harvesting

- 5.3.6 Electronic Skin and Smart Textiles

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Healthcare

- 5.4.3 Aerospace and Defense

- 5.4.4 Automotive and e-Mobility

- 5.4.5 Energy and Utilities

- 5.4.6 Industrial Automation and Sports/Fitness

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACS Material

- 6.4.3 ANP CORPORATION

- 6.4.4 Dow

- 6.4.5 DuPont

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Heraeus Holding GmbH

- 6.4.8 Indium Corporation

- 6.4.9 ITOCHU Corporation

- 6.4.10 Liquid Wire Inc.

- 6.4.11 NextFlex

- 6.4.12 Nissha Co., Ltd.

- 6.4.13 Nitto Denko Corporation

- 6.4.14 Panasonic Corporation

- 6.4.15 Priways Co., Ltd.

- 6.4.16 Rogers Corporation

- 6.4.17 Shanghai Huzheng Industrial Co., Ltd.

- 6.4.18 Sun Chemical Corporation

- 6.4.19 TOYOBO CO., LTD.

- 6.4.20 Vorbeck Materials Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth in e-Healthcare, Smart Clothing and Personalized Wearables

2026年全球可拉伸導電材料市場報告

2026年全球可拉伸導電材料市場報告 可拉伸導電材料市場規模、佔有率和成長分析:按材料類型、形狀、導電類型、製造技術、應用、終端用戶產業和地區分類-2026-2033年產業預測

可拉伸導電材料市場規模、佔有率和成長分析:按材料類型、形狀、導電類型、製造技術、應用、終端用戶產業和地區分類-2026-2033年產業預測 可拉伸導電材料市場報告:按產品、應用和地區分類(2026-2034 年)

可拉伸導電材料市場報告:按產品、應用和地區分類(2026-2034 年) 可拉伸導電材料市場:依材料類型、形狀、製造技術和終端應用產業分類-2026-2032年全球預測

可拉伸導電材料市場:依材料類型、形狀、製造技術和終端應用產業分類-2026-2032年全球預測 全球可拉伸導電材料市場規模研究與預測,依產品(石墨烯、碳奈米管、銀)、應用(穿戴式裝置、生物醫學、光電)及區域分類(2025-2035年)

全球可拉伸導電材料市場規模研究與預測,依產品(石墨烯、碳奈米管、銀)、應用(穿戴式裝置、生物醫學、光電)及區域分類(2025-2035年) 可拉伸導體市場報告:2031 年趨勢、預測與競爭分析

可拉伸導體市場報告:2031 年趨勢、預測與競爭分析 伸縮性導體:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)

伸縮性導體:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)