|

市場調查報告書

商品編碼

2062009

Montan Wax:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Montan Wax - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

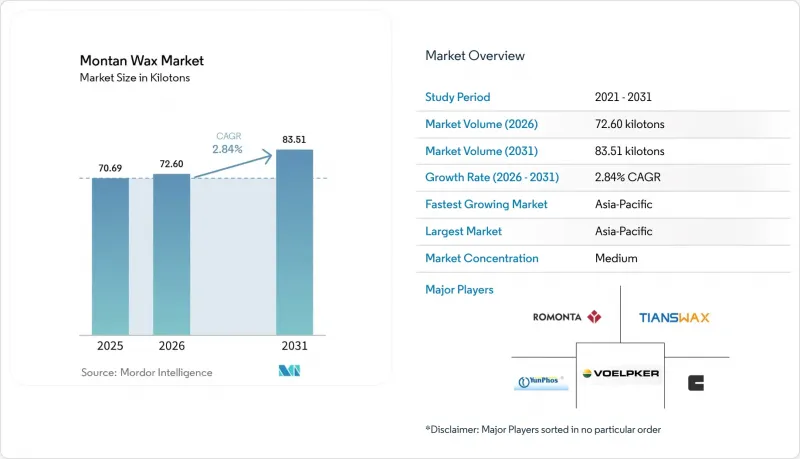

根據 Mordor Intelligence 預測,山地蠟市場規模將從 2025 年的 70.69 千噸成長到 2026 年的 72.60 千噸,到 2031 年達到 83.51 千噸,2026 年至 2031 年的複合年成長率為 2.84%。

本報告按類型(原礦、漂白/精煉礦、改質/酯化礦)、應用領域(磨料、塑膠、造紙、化妝品、電子產品及其他)、最終用戶(汽車、塑膠、個人護理、包裝、電子、工業)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

全球蒙坦蠟市場趨勢與洞察

擴大在汽車拋光劑和汽車美容組合藥物。

隨著車輛美觀日益受到重視,市場對具有深邃光澤、抗紫外線和快速施工性能的高級車蠟的需求激增。在此背景下,配方研發人員對高熔點蒙丹蠟表現出越來越濃厚的興趣。這類蠟不僅能抵抗清潔劑的侵蝕,還能在自動洗車過程中保持保護膜的完整性,進而延長保養週期,提升顧客價值。蒙丹蠟市場受益於符合低VOC標準的水性分散技術,且不會影響光澤度。這對於受監管的北美和歐洲地區的零售商尤其重要。同時,在中國和印度,不斷壯大的中產階級推動了專業汽車美容的需求,帶動了區域混合中心消費量的兩位數成長。此外,拋光膏生產商正在利用蒙丹蠟與二氧化矽、氧化鋁和聚合物基細磨料的協同效應。這使得他們能夠生產出一步式拋光膏,不僅能修復漆面瑕疵,還能起到保護作用,從而提高每單位拋光膏中蠟的含量。

熱塑性塑膠對潤滑劑/脫模劑的需求不斷成長

從事大批量生產的塑膠加工商優先考慮熔體流動的穩定性和快速的生產週期。添加0.5%至3%的蒙丹蠟可以實現這些目標,並顯著減少脫模現象,尤其是在聚氯乙烯和聚對苯二甲酸乙二醇酯(PET)型材等高剪切應用中。在亞太地區,擠出和射出成型工廠正滿載運作,以滿足包裝和電子產業激增的需求。這些工廠擴大採用漂白和氧化蒙丹蠟。這些蠟在不影響透明度或機械強度的前提下,提供內部潤滑。改質等級的蒙丹蠟,特別是蒙丹酸鈣,不僅有助於顏料分散,而且重振了蒙丹蠟市場,為母粒生產商提供了設計柔軟性。隨著聚乳酸等生物聚合物的普及,酯化蒙丹蠟因其與極性材料的相容性而脫穎而出,確保加工商能夠利用現有設備維持生產效率。

褐煤蘊藏量限制和採礦限制

以生產粗蒙坦蠟而聞名的德國褐煤產區正面臨資源枯竭和日益嚴格的環境法規的雙重挑戰。與此同時,下游需求卻不斷多元化。儘管ROMONTA採用一體化營運模式,但由於可開採礦石儲量有限,其垂直一體化結構也面臨限制。此外,歐盟碳定價法規將於2025年將二氧化碳價格從每噸45歐元提高至55歐元。生產成本的增加推高了現貨價格,引發了依賴進口原料的北美和亞洲加工商的擔憂。因此,蒙坦蠟市場前置作業時間延長,整個分銷網路中的庫存和期貨交易量都在增加。

細分市場分析

到2025年,粗蠟將佔據蒙丹蠟市場60.24%的佔有率,其成本效益將使其在瀝青改質劑、石膏板防水處理劑和脫模劑等領域獲得合約。然而,市場正在向酯化和氧化衍生物轉變。這些衍生物在化妝品、生質聚合物和電子產業越來越受歡迎,因為這些產業對顏色更鮮豔、氣味更低、熔點範圍更窄等特性非常重視。改質等級蒙丹蠟以3.45%的複合年成長率成長,也推動了整個蒙丹蠟市場的發展,這主要得益於3D列印和高溫纖維紡絲技術的進步。透過酸值調節和部分皂化等化學改性,配方設計師可以獲得粗蠟無法實現的特定流變性能,從而實現更高的定價,並在某些情況下獲得長期採購合約。

即使成本差異超過30%,優先考慮法規遵循和品牌定位的終端用戶也願意承擔額外的成本。當替代方案需要徹底重新設計配方以適應不同的流變改性劑時,情況尤其如此。因此,改質蒙丹蠟的利潤率超過了其銷售量貢獻,從而保護供應商免受原料成本波動的影響,並為蒙丹蠟市場的持續研發投入提供了合理依據。

區域分析

到2025年,亞太地區將佔全球總銷售量的42.20%。這主要得益於中國和日本強大的汽車供應鏈,以及印度和東南亞國協快速成長的個人護理用品製造業。在亞太地區,汽車美容耗材正轉向高階噴蠟和陶瓷拋光劑,這兩種產品都依賴蒙丹蠟來維持漆膜強度。韓國美妝品牌正在將蒙丹蠟與米糠蠟混合使用,力求在永續性和性能之間取得平衡,這反映了一種共存而非完全替代的趨勢。

在北美,儘管陶瓷塗層產品日益普及,但蒙丹蠟的需求仍然強勁,這得益於成熟的分銷管道和蓬勃發展的DIY汽車護理文化。為了符合嚴格的VOC(揮發性有機化合物)和PFAS(全氟烷基物質)法規,配方開發商正轉向水性蒙丹分散體,在不使用溶劑的情況下實現與傳統蒙丹蠟相當的光澤度,從而推動了該地區蒙丹蠟市場的發展。此外,墨西哥蓬勃發展的塑膠加工產業正在進口精製蒙丹蠟用於射出成型成型的消費品,進一步鞏固了北美大陸的蒙丹蠟消費市場。

歐洲既是蒙坦蠟市場的發源地,也是其試驗場。德國生產商如ROMONTA和Volpker已建立起全球品質和技術標準,但碳定價和褐煤資源枯竭等挑戰阻礙了它們的擴張。同時,歐盟的監管挑戰正推動著旨在生產低多環芳烴(PAH)含量和食品接觸級蒙坦蠟的研發工作。在此方面成功轉型可望開闢新的成長機會。未來,隨著替代品威脅的加劇,歐洲企業可能傾向於在亞洲建立合資企業,因為亞洲的原料限制相對寬鬆。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大在汽車拋光劑和汽車美容組合藥物。

- 熱塑性塑膠對潤滑劑和脫模劑的需求不斷成長。

- 在化妝品和個人護理乳液中的應用日益廣泛

- 3D列印耗材表面改質劑的快速普及

- 用於封裝危險廢棄物屏障

- 市場限制因素

- 褐煤蘊藏量有限,且有採礦限制。

- 合成蠟和生物基蠟的替代品威脅

- 加強歐盟REACH法規對蠟中微量多環芳烴的規定

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 粗蒙坦蠟

- 漂白精製蒙坦蠟

- 改質/酯化蒙坦蠟

- 透過使用

- 磨料和塗料

- 塑膠加工

- 紙張塗層

- 化妝品和個人護理

- 電子線材的漆包與焊錫掩膜

- 其他應用(橡膠、電絕緣、3D列印)

- 按最終用戶行業分類

- 車

- 塑膠和聚合物

- 個人護理化妝品

- 包裝/紙張

- 電氣和電子設備

- 工業與建築

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- AmeriLubes LLC

- Blended Waxes Inc.

- Brother(Japan)

- Carmel Industries

- Clariant

- Deurex AG

- Dhariwal Corp Ltd.

- Excel International

- Huber Engineered Materials

- Koster Keunen

- Paraffinwaxco Inc.

- Poth Hille

- Pramelt BV

- ROMONTA Group

- Strahl & Pitsch Inc.

- Ter Hell & Co. GmbH

- TianshiWax

- Volpker Spezialprodukte GmbH

- Volwax(Yunnan Shangcheng)

- Yunphos

第7章 市場機會與未來展望

According to Mordor Intelligence, the montan wax market size is expected to increase from 70.69 kilotons in 2025 to 72.60 kilotons in 2026 and reach 83.51 kilotons by 2031, growing at a CAGR of 2.84% over 2026-2031.

This report is Segmented by Type (Crude, Bleached/Refined, Modified/Esterified), Application (Polishes, Plastics, Paper, Cosmetics, Electronics, Other), End-User (Automotive, Plastics, Personal Care, Packaging, Electronics, Industrial), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Montan Wax Market Trends and Insights

Growing Use in Automotive Polishes and Detailing Formulations

As vehicle aesthetics gain prominence, the demand for premium wax blends that offer deep gloss, UV resistance, and quick application has surged. In this landscape, formulators are increasingly gravitating toward high-melting montan grades. These grades not only resist detergent attacks but also uphold protective films during automated washes, leading to extended service intervals and heightened perceived value. The montan wax market is reaping the benefits of water-borne dispersion technology, which adheres to low-VOC standards without compromising on shine. This is particularly important for retailers in North America and Europe, where regulatory oversight is strict. Meanwhile, in China and India, a growing middle class is fueling a professional detailing surge, bolstering double-digit consumption growth in regional blending centers. Additionally, manufacturers of polishing pastes are capitalizing on montan wax's synergy with silica, alumina, and polymer micro-abrasives. This allows them to craft single-step compounds that not only correct but also safeguard paint surfaces, resulting in increased per-unit wax loadings.

Expanding Demand as Lubricant/Release Agent in Thermoplastics

High-volume plastics processors prioritize consistent melt flow and rapid cycle times. By adding 0.5% to 3% montan wax, they achieve these objectives and notably reduce plate-out, especially in high-shear applications like polyvinyl chloride and polyethylene terephthalate profiles. In the Asia-Pacific region, extrusion and injection-molding facilities are running at full capacity to meet the surging demands of packaging and electronics. These facilities are increasingly turning to bleached and oxidized montan waxes. These waxes offer internal lubrication benefits without sacrificing clarity or mechanical strength. Modified grades, especially calcium montanate, not only facilitate easy pigment dispersion but also bolster the montan wax market, granting color-masterbatch producers greater design flexibility. As biopolymers like polylactic acid gain popularity, esterified montan wax stands out for its polar compatibility, ensuring processors can maintain productivity on their current equipment.

Limited Lignite Reserves and Mining Restrictions

Germany's lignite belts, known for their crude montan wax production, are facing resource depletion and tighter environmental regulations. These challenges come at a time when downstream demand is diversifying. While ROMONTA operates with an integrated approach, its vertically aligned structure struggles against the finite limits of accessible ore. Furthermore, EU carbon-pricing regulations are set to rise from EUR 45 to EUR 55 per tonne of CO2 by 2025. This increase in production costs is pushing spot prices higher, causing concern among converters in North America and Asia who depend on imported feedstock. As a result, the montan wax market is experiencing extended lead times, leading to inventory hoarding and forward-buying across distributor networks.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption in Cosmetics and Personal-Care Emulsions

- Rapid Uptake in 3-D-Printing Filament Surface Modifiers

- Substitution Threat from Synthetic and Bio-Based Waxes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, crude material clinched 60.24% of the montan wax market share, leveraging its cost-effectiveness to secure contracts in asphalt modifiers, gypsum-board hydrophobization, and foundry release agents. However, the market is shifting toward esterified and oxidized derivatives. These derivatives are increasingly favored by the cosmetic, biopolymer, and electronics sectors, which prioritize attributes like lighter color, reduced odor, and specific melting-point ranges. Modified grades, growing at a 3.45% CAGR, are also driving advancements in 3-D printing and high-temperature fiber-spinning, bolstering the overall montan wax market. Through chemical tailoring such as acid-number adjustment and partial saponification, formulators can achieve niche rheological targets unattainable by crude wax, justifying premium pricing and, in certain instances, securing long-term offtake agreements.

Even when the cost difference can surpass 30%, end users, prioritizing regulatory compliance and brand positioning, willingly absorb the extra expense. This is particularly true when the alternative involves overhauling an entire formulation to fit a different rheology modifier. As a result, modified montan wax enjoys a profit margin that exceeds its volume contribution, shielding suppliers from fluctuations in raw material costs and underscoring the rationale for sustained R&D investments in the montan wax market.

Geography Analysis

In 2025, Asia-Pacific accounted for 42.20% of the volume, driven by a robust automotive supply chain in China and Japan, coupled with a burgeoning personal-care manufacturing sector in India and ASEAN. In the region, automotive detailing consumables are gravitating toward premium spray waxes and ceramic-infused polishes, both of which depend on montan wax for their film integrity. South Korean K-beauty brands are blending montan wax with rice-bran wax, striking a balance between sustainability and performance, indicating a trend of coexistence over outright substitution.

North America, with its established distribution channels and a strong DIY car care culture, continues to see robust demand, even with the rise of ceramic coatings. In response to stringent VOC and PFAS regulations, formulators are pivoting to water-borne montan dispersions, achieving similar gloss without solvents, bolstering the regional montan wax market. Additionally, Mexico's expanding plastics processing sector is importing refined grades for its injection-molded consumer goods, solidifying the continent's consumption.

Europe stands as both the birthplace and a testing ground for the montan wax market. While German producers like ROMONTA and Volpker set global standards for quality and expertise, challenges like carbon-pricing schemes and lignite depletion hinder their expansion. Concurrently, EU regulatory challenges are spurring R&D initiatives aimed at producing low-PAH, food-contact-compliant grades. A successful pivot here could pave the way for new growth opportunities. Looking ahead, potential substitution threats might drive European firms to forge joint ventures in Asia, where feedstock limitations are less pronounced.

- AmeriLubes LLC

- Blended Waxes Inc.

- Brother ( Japan )

- Carmel Industries

- Clariant

- Deurex AG

- Dhariwal Corp Ltd.

- Excel International

- Huber Engineered Materials

- Koster Keunen

- Paraffinwaxco Inc.

- Poth Hille

- Pramelt B.V.

- ROMONTA Group

- Strahl & Pitsch Inc.

- Ter Hell & Co. GmbH

- TianshiWax

- Volpker Spezialprodukte GmbH

- Volwax (Yunnan Shangcheng)

- Yunphos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing use in automotive polishes and detailing formulations

- 4.2.2 Expanding demand as lubricant/release agent in thermoplastics

- 4.2.3 Rising adoption in cosmetics and personal-care emulsions

- 4.2.4 Rapid uptake in 3-D-printing filament surface modifiers

- 4.2.5 Utilisation in encapsulating hazardous-waste barriers

- 4.3 Market Restraints

- 4.3.1 Limited lignite reserves and mining restrictions

- 4.3.2 Substitution threat from synthetic and bio-based waxes

- 4.3.3 Tightening EU-REACH limits on PAH traces in waxes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Crude Montan Wax

- 5.1.2 Bleached / Refined Montan Wax

- 5.1.3 Modified / Esterified Montan Wax

- 5.2 By Application

- 5.2.1 Polishes and Coatings

- 5.2.2 Plastic Processing

- 5.2.3 Paper Coatings

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Electronics Wire-Enamelling and Solder-Mask

- 5.2.6 Other Applications (Rubber, Electrical Insulation, 3-D Printing)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Plastics and Polymers

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Packaging and Paper

- 5.3.5 Electrical and Electronics

- 5.3.6 Industrial and Construction

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AmeriLubes LLC

- 6.4.2 Blended Waxes Inc.

- 6.4.3 Brother ( Japan )

- 6.4.4 Carmel Industries

- 6.4.5 Clariant

- 6.4.6 Deurex AG

- 6.4.7 Dhariwal Corp Ltd.

- 6.4.8 Excel International

- 6.4.9 Huber Engineered Materials

- 6.4.10 Koster Keunen

- 6.4.11 Paraffinwaxco Inc.

- 6.4.12 Poth Hille

- 6.4.13 Pramelt B.V.

- 6.4.14 ROMONTA Group

- 6.4.15 Strahl & Pitsch Inc.

- 6.4.16 Ter Hell & Co. GmbH

- 6.4.17 TianshiWax

- 6.4.18 Volpker Spezialprodukte GmbH

- 6.4.19 Volwax (Yunnan Shangcheng)

- 6.4.20 Yunphos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Smart functional coatings for recyclable paper-based packaging

蒙坦蠟市場:按類型、形態、等級、應用、終端用戶產業和分銷管道分類-2026-2032年全球市場預測蠟市場:2026-2032年全球市場預測(依產品類型、製造流程、實體形態、應用及分銷通路分類)

蒙坦蠟市場:按類型、形態、等級、應用、終端用戶產業和分銷管道分類-2026-2032年全球市場預測蠟市場:2026-2032年全球市場預測(依產品類型、製造流程、實體形態、應用及分銷通路分類) 蠟市場機會、成長要素、產業趨勢分析及2026-2035年預測

蠟市場機會、成長要素、產業趨勢分析及2026-2035年預測 蠟市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

蠟市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 蠟市場報告:按類型、形態、應用和地區分類 2026-2034 年

蠟市場報告:按類型、形態、應用和地區分類 2026-2034 年 合成蠟市場:按類型、應用和地區分類

合成蠟市場:按類型、應用和地區分類 全球小燭樹蠟市場規模、佔有率、趨勢和成長分析報告(2026-2034年)Ceres In Wax 市場:2026-2032 年全球市場預測(按產品類型、應用、終端用戶產業和分銷管道分類)小燭樹蠟市場:依形態、原料、等級、通路和應用分類-2026-2032年全球市場預測地板蠟市場:按類型、形態、配方、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

全球小燭樹蠟市場規模、佔有率、趨勢和成長分析報告(2026-2034年)Ceres In Wax 市場:2026-2032 年全球市場預測(按產品類型、應用、終端用戶產業和分銷管道分類)小燭樹蠟市場:依形態、原料、等級、通路和應用分類-2026-2032年全球市場預測地板蠟市場:按類型、形態、配方、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測