|

市場調查報告書

商品編碼

2062008

凝聚劑和固化劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Flocculant And Coagulant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

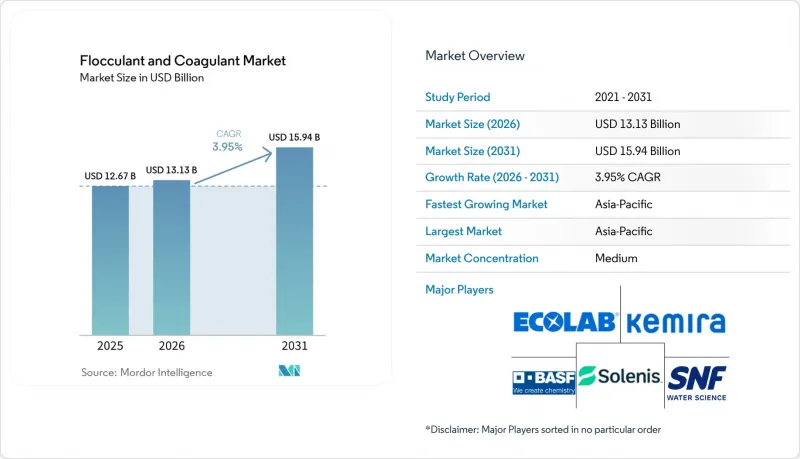

根據 Mordor Intelligence 預測,凝聚劑和混凝劑市場預計將從 2025 年的 126.7 億美元成長到 2026 年的 131.3 億美元,到 2031 年達到 159.4 億美元,2026 年至 2031 年的複合年成長率為 3.95%。

本報告按類型(混凝劑:無機、有機/合成、天然/生物基;凝聚劑:陽離子、陰離子、非離子)、應用(水處理、工業污水處理(紙漿和造紙、石油和天然氣等))和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行分類。市場預測以美元計價。

全球凝聚劑和混凝劑市場趨勢及洞察

新興市場工業叢集更嚴格的排放標準

在東南亞和南亞,新的法規迫使工廠大幅提升其化學品處理能力,以符合更嚴格的化學需氧量(COD)和懸浮固體含量限制。自2025年1月起,越南的QCVN 40:2025法規將紡織及食品加工產業廢水的COD限值降至50毫克/公升。同時,印尼2024年的生活污水處理法規要求移除80%的固態,促使雅加達、泗水和萬隆等城市升級處理設備。土耳其、韓國和印度的法規也在收緊,縮短了交貨週期,並有利於擁有本地庫存的供應商,導致這些地區的需求激增,超過了整體複合年成長率。

零液體排放(ZLD)電廠和石化廠建設快速擴張

零液體排放 (ZLD) 系統利用絮凝、逆滲透和結晶技術,實現近乎完全的水回收。為了保護膜,混凝劑的使用被視為一項重要的預處理步驟。威立雅已在殼牌的 Pearl GTL 工廠實施了該系統,成功處理了每天 12,000 立方公尺的排污水,回收率高達 99.5%。到 2025 年,中國陝西和內蒙古的煤化工項目以及印度的一個紡織產業叢集都計劃實現零排放。這種緊迫性促使這些項目簽訂長期化學品服務契約,而這些合約的價格往往過高。

監管毒性:重點關注丙烯醯胺單體殘留物

2024年,美國環保署(EPA)將丙烯醯胺列入其「候選污染物清單」。世界衛生組織(WHO)將飲用水中丙烯醯胺殘留量的上限設定為0.5毫克/公斤,日本已將食品接觸材料的丙烯醯胺基準值降低至0.05毫克/公斤。歐盟計畫限制使用單體殘留量超過0.1%的配方。製造商面臨每公斤0.10至0.30美元的精煉成本。提供經認證的低殘留量等級產品有助於製造商保持市場競爭力。

細分市場分析

2025年,混凝劑銷售額佔總銷售額的57.89%,預計到2031年,該細分市場將以4.56%的複合年成長率成長。在混凝劑細分市場中,無機產品(如聚合氯化鋁、硫酸鋁和氯化鐵)在產量方面佔據主導地位。這項優勢體現在,2025年中國聚合氯化鋁產量將達231.23萬噸,國內平均價格為每噸1636元人民幣(約230美元)。有機混凝劑(如聚二甲基二烯丙基二甲基氯化銨和環氧二甲基二甲基丙烯酸酯)的價格溢價為15-30%。這些有機產品在高鹼性水體中表現良好,其減少污泥量的能力使其高成本。生物基替代品(如幾丁聚醣和辣木萃取物)在實驗室測試中顯示出85-95%的濁度去除率。然而,供應鏈和品質穩定性方面的挑戰限制了它們的市場佔有率。

凝聚劑在污泥脫水和礦物處理中發揮至關重要的作用。陽離子聚丙烯醯胺佔據了凝聚劑銷售的大部分佔有率,因為排放城市污泥和礦山廢料中的水分需要高電荷聚合物。陰離子型混凝劑在紙漿和造紙業用作助留劑,而非離子型混凝劑則用於洗煤。旨在將飲用水應用中殘留單體含量限制在0.5 mg/kg以下的監管措施增加了生產成本。然而,這些措施也為超低單體含量產品創造了機會,這些產品可以高價出售。

區域分析

預計到2025年,亞太地區將佔據凝聚劑和混凝劑市場31.20%的佔有率,到2031年將以4.98%的複合年成長率成長。中國是聚合氯化鋁(PAC)市場的主要參與者,為該地區的紡織、造紙和煤化工企業提供產品。同時,越南、印尼和印度更嚴格的排放標準使某些區域叢集的加工量增加了兩倍。日本和韓國走在前列,採用人工智慧驅動的加藥系統來滿足0.2毫克/公升的磷含量限制。在東南亞國協在多邊組織的支持下升級用水和污水系統的同時,採購趨勢正轉向中國和印度等成本效益更高的生產商。

在北美,儘管污水處理量成長緩慢,但每噸污水在特種混凝劑和雲端連接控制平台上的支出卻在增加。加州2025年直接飲用水水資源再利用計畫和亞利桑那州12億美元的水資源再利用計畫等關鍵措施正在提振需求。此外,根據新墨西哥州2024年的法案,二疊紀盆地正在將生產用水用於灌溉。在加拿大,供水事業正在採用低處理量PAC策略來應對掩埋的污水污泥掩埋成本,從而在處理量成長放緩的情況下確保收入穩定。

歐洲的需求保持穩定,尤其是在德國、英國、法國和北歐國家。能源價格的波動正推動著低劑量混合肥料的使用。法國正透過一項5億歐元(約5.8506億美元)的補貼計畫來鼓勵這種轉型,該計畫旨在扶持小規模供水事業,尤其關注那些獲得ISO 9001和NSF 60認證的公司。西班牙新的灌溉回用法規正在增加穆爾西亞和阿爾梅里亞地區混凝劑的使用,而俄羅斯的預算限制則將年成長率限制在1-2%。在南美洲、中東和非洲,巴西更嚴格的廢水法規、智利的銅尾礦處理以及沙烏地阿拉伯的大規模海水淡化項目,正在為採礦、海水淡化和市政零液體排放(ZLD)項目創造新的市場機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興市場工業叢集更嚴格的排放標準

- 零液體排放(ZLD)發電廠和石化廠建設快速擴張

- 在缺水地區強制重複利用

- 北美和歐洲公共產業支出週期的成熟

- 人工智慧驅動的劑量控制平台提高了化學品的使用效率。

- 市場限制因素

- 關注丙烯醯胺單體殘留物的監管毒性

- 鋁鹽和鐵鹽等原物料價格上漲

- 人們對混合膜和電凝技術的興趣日益濃厚

- 價值鏈分析

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 凝血劑

- 無機混凝劑

- 有機/合成混凝劑

- 天然和生物衍生的凝結劑

- 凝聚劑

- 陽離子凝聚劑

- 陰離子凝聚劑

- 非離子凝聚劑

- 凝血劑

- 透過使用

- 水處理

- 工業污水處理

- 紙漿和造紙

- 採礦和礦物加工

- 石油和天然氣

- 發電

- 建築和基礎設施

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐的

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- Ashland Global Holdings Inc.

- BASF

- Buckman

- Chemtrade Logistics

- Dow

- Ecolab Inc.

- Feralco AB

- Grasim Industries Ltd.

- IXOM

- Kemira

- Kurita Water Industries Ltd.

- Nouryon

- SNF

- Solenis

- Solvay

- USALCO LLC

- Veolia Water Technologies

第7章 市場機會與未來展望

According to Mordor Intelligence, the flocculant and coagulant market size is expected to increase from USD 12.67 billion in 2025 to USD 13.13 billion in 2026 and reach USD 15.94 billion by 2031, growing at a CAGR of 3.95% over 2026-2031.

This report is Segmented by Type (Coagulants: Inorganic, Organic/Synthetic, Natural/Bio-based; Flocculants: Cationic, Anionic, Non-Ionic), Application (Municipal Water Treatment, Industrial Wastewater Treatment: Pulp and Paper, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Flocculant And Coagulant Market Trends and Insights

Stricter Discharge Norms for Emerging-Market Industrial Clusters

In Southeast and South Asia, new regulations compel factories to significantly boost their chemical throughput to comply with stricter limits on Chemical Oxygen Demand (COD) and suspended solids. Starting January 2025, Vietnam's QCVN 40:2025 regulation reduced COD allowances for effluents from textile and food-processing industries to 50 mg/L. Meanwhile, Indonesia's 2024 rule on domestic wastewater mandates an 80% removal of solids, leading to necessary upgrades in municipalities like Jakarta, Surabaya, and Bandung. Turkey, South Korea, and India have also tightened regulations, shortening procurement windows, favoring suppliers with local stock, and creating demand spikes that exceed the headline CAGR in these regions.

Rapid Build-Out of Zero-Liquid-Discharge (ZLD) Power and Petrochem Plants

Zero Liquid Discharge (ZLD) systems utilize coagulation, reverse osmosis, and crystallization techniques to achieve near-total water recovery. Coagulants are embedded as a mandatory pretreatment step to safeguard the membranes. Veolia has implemented a system at Shell's Pearl GTL plant, successfully treating 12,000 m3/day of blowdown with a 99.5% recovery rate. China's coal-chemical initiatives in Shaanxi and Inner Mongolia, along with textile clusters in India in 2025, are aimed at zero discharge. This urgency is steering them towards long-term chemical service contracts, often at a premium price.

Regulatory Toxicity Spotlight on Acrylamide Monomer Residues

In 2024, the U.S. EPA added acrylamide to its Contaminant Candidate List. WHO set a cap of 0.5 mg/kg for residual acrylamide in drinking water and Japan reduced food-contact limits to 0.05 mg/kg. The EU plans to restrict formulations with over 0.1 percent residual monomer. Producers face purification costs of USD 0.10 to 0.30 per kg. Offering certified low-residue grades may assist producers in maintaining a competitive position within the market.

Other drivers and restraints analyzed in the detailed report include:

- Re-Use Mandates in Water-Scarce Regions

- Mature Utility Spending Cycles in North America and Europe

- Growing Preference for Membrane and Electro-Coagulation Hybrids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, coagulants captured a 57.89% share of the revenue pie, and projections indicate this segment will grow at a 4.56% CAGR through 2031. Within the coagulant segment, inorganic variants like PAC, aluminum sulfate, and ferric chloride lead in tonnage. This dominance is supported by China's 2025 output of 2.3123 million tons of PAC, fetching an average domestic price of CNY 1,636/ton (approximately USD 230/ton). Organic coagulants, such as polyDADMAC and EPI-DMDA, have a price premium of 15-30%. These organic variants perform well in high-alkalinity waters, where their ability to reduce sludge volume justifies the elevated costs. Bio-based alternatives like chitosan and Moringa extracts have shown 85-95% turbidity removal in lab tests. However, challenges in the supply chain and consistency have limited their market share.

Flocculants play a critical role in sludge dewatering and mineral processing. Cationic polyacrylamides account for the majority of flocculant revenue, driven by the need for high-charge polymers in municipal sludge and mining tailings to facilitate water release. Anionic variants are used as retention aids in the pulp-and-paper industry, while non-ionic grades are applied in coal washing. Regulatory initiatives aiming to limit residual monomer content to below 0.5 mg/kg in potable applications have increased production costs. However, they also create opportunities for ultra-low-monomer products, which can be marketed at a premium price point.

Geography Analysis

In 2025, Asia-Pacific commands the flocculant and coagulant market with a 31.20% revenue share and is expected to grow at a 4.98% CAGR through 2031. China's PAC base, a dominant player, caters to regional textile, paper, and coal-chemical plants. Meanwhile, tighter discharge norms in Vietnam, Indonesia, and India have led to a threefold increase in chemical throughput in specific clusters. Japan and South Korea are at the forefront, employing AI-driven dosing to adhere to phosphorus caps of 0.2 mg/L. ASEAN nations, with backing from multilaterals, are upgrading municipal systems, yet procurement trends lean towards cost-effective producers from China and India.

North America may be expanding its volume at a slower pace, but it's spending more per ton on specialty coagulants and cloud-connected control platforms. Key initiatives like California's 2025 direct-potable-reuse rollout and Arizona's USD 1.2 billion water-reuse program are bolstering demand. Additionally, under New Mexico's 2024 act, the Permian Basin is reclaiming produced water for irrigation. In Canada, utilities are adopting low-dose PAC strategies to counter rising landfill fees for sludge, ensuring steady revenue despite only modest volume increases.

Europe's demand remains stable, particularly in Germany, the United Kingdom, France, and the Nordic countries. Energy price fluctuations are pushing a shift towards low-dose blends. France is incentivizing this shift with a EUR 500 million (~USD 585.06 million) subsidy plan for small utilities, especially rewarding those with ISO 9001 and NSF 60 certifications. While Spain's new irrigation reuse regulations boost coagulant use in Murcia and Almeria, budget limitations in Russia are restraining growth to a modest 1-2% annually. In South America and the Middle-East and Africa, niche opportunities arise in mining, desalination, and municipal zero liquid discharge (ZLD) projects, spurred by tightening effluent regulations in Brazil, copper tailings in Chile, and grand desalination initiatives in Saudi Arabia.

- Ashland Global Holdings Inc.

- BASF

- Buckman

- Chemtrade Logistics

- Dow

- Ecolab Inc.

- Feralco AB

- Grasim Industries Ltd.

- IXOM

- Kemira

- Kurita Water Industries Ltd.

- Nouryon

- SNF

- Solenis

- Solvay

- USALCO LLC

- Veolia Water Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter discharge norms for emerging-market industrial clusters

- 4.2.2 Rapid build-out of zero-liquid-discharge (ZLD) power and petrochem plants

- 4.2.3 Re-use mandates in water-scarce regions

- 4.2.4 Mature utility spending cycles in North America and Europe

- 4.2.5 AI-enabled dosing control platforms boosting chemical efficiency

- 4.3 Market Restraints

- 4.3.1 Regulatory toxicity spotlight on acrylamide monomer residues

- 4.3.2 Input price spikes for aluminium and ferric salts

- 4.3.3 Growing preference for membrane and electro-coagulation hybrids

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Coagulants

- 5.1.1.1 Inorganic Coagulants

- 5.1.1.2 Organic/Synthetic Coagulants

- 5.1.1.3 Natural/Bio-based Coagulants

- 5.1.2 Flocculants

- 5.1.2.1 Cationic Flocculants

- 5.1.2.2 Anionic Flocculants

- 5.1.2.3 Non-ionic Flocculants

- 5.1.1 Coagulants

- 5.2 By Application

- 5.2.1 Municipal Water Treatment

- 5.2.2 Industrial Wastewater Treatment

- 5.2.2.1 Pulp and Paper

- 5.2.2.2 Mining and Mineral Processing

- 5.2.2.3 Oil and Gas

- 5.2.2.4 Power Generation

- 5.2.2.5 Construction and Infrastructure

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordics

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ashland Global Holdings Inc.

- 6.4.2 BASF

- 6.4.3 Buckman

- 6.4.4 Chemtrade Logistics

- 6.4.5 Dow

- 6.4.6 Ecolab Inc.

- 6.4.7 Feralco AB

- 6.4.8 Grasim Industries Ltd.

- 6.4.9 IXOM

- 6.4.10 Kemira

- 6.4.11 Kurita Water Industries Ltd.

- 6.4.12 Nouryon

- 6.4.13 SNF

- 6.4.14 Solenis

- 6.4.15 Solvay

- 6.4.16 USALCO LLC

- 6.4.17 Veolia Water Technologies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rise of fully bio-based coagulants for hypersaline wastewater

凝聚劑和混凝劑市場:全球市場預測,2026-2032年有機凝聚劑市場:全球市場預測,2026-2032年

凝聚劑和混凝劑市場:全球市場預測,2026-2032年有機凝聚劑市場:全球市場預測,2026-2032年 凝血劑市場:按類型、應用、最終用途、形態、功能、國家和地區分類-全球產業分析、市場規模及佔有率和未來預測(2026-2033)凝聚劑市場:按類型、形態、聚合物原料、分銷管道和應用分類-2026-2032年全球市場預測無機凝聚劑市場:按類型、形態、等級、應用、分銷管道和最終用途行業分類-2026-2032年全球市場預測

凝血劑市場:按類型、應用、最終用途、形態、功能、國家和地區分類-全球產業分析、市場規模及佔有率和未來預測(2026-2033)凝聚劑市場:按類型、形態、聚合物原料、分銷管道和應用分類-2026-2032年全球市場預測無機凝聚劑市場:按類型、形態、等級、應用、分銷管道和最終用途行業分類-2026-2032年全球市場預測 全球有機凝聚劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球有機凝聚劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 凝聚劑和混凝劑市場:按產品類型、最終用途和地區分類全球絮凝劑市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)

凝聚劑和混凝劑市場:按產品類型、最終用途和地區分類全球絮凝劑市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年) 凝聚劑市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測

凝聚劑市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測 全球有機凝結劑市場

全球有機凝結劑市場