|

市場調查報告書

商品編碼

2061994

特權存取管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Privileged Access Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

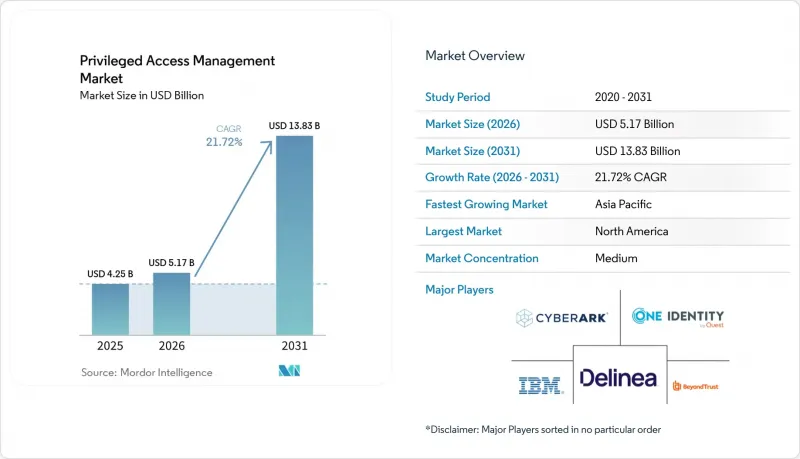

根據 Mordor Intelligence 預測,特權存取管理市場將從 2025 年的 42.5 億美元成長到 2026 年的 51.7 億美元,到 2031 年達到 138.3 億美元,2026 年至 2031 年的複合年成長率為 21.72%。

本報告按元件(解決方案和服務)、部署模式(本地部署等)、組織規模(大型企業和中小企業)、最終用戶行業(銀行、金融服務和保險等)、存取控制類型(共用/特權帳戶管理、跨應用程式密碼管理等)以及地區進行細分。市場預測以美元計價。

全球特權存取管理市場趨勢與洞察

機器 ID 的快速成長和金鑰管理的日益複雜化。

採用微服務、容器和事件驅動架構的組織現在每天都會產生數千個臨時服務帳戶,導致憑證數量激增,傳統密碼管理系統無法應付。 CyberArk 的一項研究發現,機器身分與人類身分的比例為 40:1,87% 的公司承認將金鑰儲存在多個未受管理的位置。供應商正在透過自動偵測、輪調和行為分析等功能來解決這個問題,這些功能專門針對非人類帳戶。 Saviynt 的一項研究強調了製定針對機器身分的生命週期策略的必要性。

零信任架構加速了特權會話的隔離。

諸如美國國防部的「零信任實施藍圖」等政府框架要求在2027會計年度之前實施特權存取管理 (PAM) 控制,並強調即時配置和持續會話檢驗是零信任藍圖的關鍵要素。金融和醫療保健行業的公司也面臨類似的要求,因此,PAM 供應商正在與身份聯合、微隔離閘道器和行為風險引擎整合,以便在上下文風險增加時撤銷權限。

缺乏PAM實施和生命週期管治的技能

身分安全專案需要涵蓋密碼學、目錄服務和 API 整合等方面的專業知識,而這些技能在全球範圍內長期短缺。組織者經常發現,即使是擁有紮實的傳統身分管治基礎的員工,也難以操作依賴機器學習模式的雲端原生分析模組。大型銀行和醫療保健網路透過長期託管服務合約來彌補這一缺口,而許多中小企業 (SME) 則推遲項目,直到能夠聘請外部顧問。供應商提供的應對措施包括低程式碼策略建構器和實作模板,以縮短配置時間,但這並不能完全消除對熟練專業人員的需求。

細分市場分析

解決方案板塊是特權存取管理市場的主要驅動力,預計到2025年將佔據64.10%的收入佔有率,而服務板塊預計到2031年將以24.40%的複合年成長率成長。平台整合仍然是關鍵的採購標準,因為企業更傾向於在單一主機中整合儲存庫、會話隔離和特權分析功能。解決方案板塊的特權存取管理市場規模預計將在2025年達到27.2億美元,並在2031年超過82億美元。同時,服務板塊預計同期將從15.3億美元成長至56.5億美元。 CyberArk以15.4億美元收購Venafi,體現了該公司整合機器身分管理和人工特權工作流程的策略。買家表示,降低整合成本和加快審計回應速度是選擇一體化平台而非獨立產品時的決定性因素。

該服務的成長主要受三大因素驅動:身分安全專家長期短缺、混合環境日益複雜,以及轉向基於結果的託管服務模式(這種模式將工具許可與全天候監控相結合)。託管服務供應商尤其受到中小企業的青睞,其可預測的訂閱價格與營運成本支出 (OpEx) 的安全預算相符。持續的諮詢服務也幫助企業應對季度合規性更新和新興的後量子密碼學指南,預計這將使服務合作夥伴在未來十年保持兩位數的成長。

到 2025 年,雲端採用將佔特權存取管理市場佔有率的 57.05%。這反映了買家對基於 SaaS 的密碼庫和策略引擎的偏好,這些方案可以繞過本地硬體。預計到 2025 年,雲端採用的特權存取管理市場規模將達到 24.2 億美元,到 2031 年將達到 77.5 億美元。同時,混合採用的複合年成長率 (CAGR) 最高,達到 24.10%,因為企業正在將本地大型主機和空氣間隙的OT 網路與雲端控制平面連接起來。 SSH Communications Security 的 PrivX 提供並行的密碼庫和基於憑證的仲介功能,從而實現分階段遷移,且無需停機。

國防、公共產業和支付處理等行業的持續監管要求使得本地部署至關重要,尤其是在資料主權法規禁止使用外部金鑰庫的情況下。供應商正透過運作在私有雲端中的容器化儲存設備來降低遷移風險,同時將元資料複製到 SaaS 分析叢集,從而在本地管理和雲端規模洞察之間取得平衡。在預測期內,混合部署在擁有廣泛舊有系統的行業中將超越純雲端部署,而新興的數位化原生公司將繼續選擇完全 SaaS 模式。

區域分析

預計到2025年,北美將維持38.10%的特權存取管理市場佔有率。這反映了聯邦政府強制推行零信任的監管壓力,以及人們對資料外洩高昂成本日益成長的認知。美國財政部加強了對勒索軟體洗錢活動的打擊力度,迫使銀行和保險公司將特權存取視為首要的控制機制。加拿大也透過修訂其《個人資訊保護和電子文件法》(PIPEDA) 指南展現出類似的趨勢,而墨西哥金融監理機構則對跨境支付服務供應商實施資料保險庫要求。現有市場參與者擁有廣泛的合作夥伴生態系統,從而推動了託管式特權存取管理消費模式的快速擴張。

預計到2031年,亞太地區將以23.60%的複合年成長率成長,成為全球成長最快的地區。新加坡金融管理局的指導方針強制要求在銀行基礎設施中實施特權存取控制,這項標準正在東協成員國中推廣。日本成熟的網路安全文化正在推動平台更新周期。 Zoho Japan憑藉其Password Manager Pro在2023年佔據了46.2%的市場佔有率,而NTT TechnoCross則因其在國內特權存取管理(PAM)領域的領先地位而連續獲得行業獎項。中國和印度的成長得益於智慧製造專案和資料本地化立法,這些立法要求對管理員操作進行嚴格的審計追蹤。

在歐洲,由於《一般資料保護規範》(GDPR) 和歐盟《網路與資訊安全指令》(NISD) 對特權帳戶保護不足的行為施加了處罰,特權會話控制技術正穩步普及。德國和英國在該地區引領相關支出,因為汽車、金融和通訊業者在國家安全法中都面臨關於特權存取的明確規定。英國的《通訊安全法》強制要求通訊業者在2024年網路升級前實施特權會話控制,這進一步提升了相關解決方案的優先順序。在南歐和北歐,由於政府的數位轉型(DX)資金以及醫療保健系統面臨的勒索軟體攻擊風險日益增加,相關需求也日益凸顯。

在中東和非洲,儘管仍處於起步階段,但對特權存取管理 (PAM) 的需求正在迅速成長,這主要得益於石油和天然氣行業運營技術 (OT) 的現代化、主權雲的採用以及國家層面的網路安全戰略。波灣合作理事會(GCC) 成員國的銀行和公共產業在競標文件中擴大要求 PAM 認證,這迫使國際供應商建立本地資料中心並提供阿拉伯語支援。在撒哈拉以南非洲,隨著行動支付生態系統的擴展,身份驗證濫用的風險日益增加,南非和肯亞在 PAM 的應用方面處於領先地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 機器 ID 的快速成長和金鑰管理的日益複雜化。

- 利用零信任架構加速特權會話的隔離

- DevSecOps 工具鏈的整合推動了對雲端原生 PAM 的需求。

- AI 驅動的攻擊面辨識正在加速 PAM 在 OT 和 IoT 領域的應用。

- 網路保險的嚴格承保要求

- 向後量子密碼學過渡將給憑證儲存帶來壓力。

- 市場限制因素

- 缺乏PAM實施和生命週期管治的技能

- 混合遺留環境中棕地整合的複雜性

- 影子IT的氾濫阻礙了政策的實施。

- 訂閱服務的普及正在推高中小型企業的總擁有成本(TCO)。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 現場

- 雲

- 混合

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- BFSI

- 資訊科技/通訊

- 政府/公共部門

- 衛生保健

- 零售與電子商務

- 製造業

- 能源公用事業

- 其他終端用戶產業

- 按類型進行存取控制

- 共用/特權帳戶管理

- 跨應用程式密碼管理 (AAPM)

- 端點特權管理 (EPM)

- 雲端和SaaS權限管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CyberArk Software Ltd.

- BeyondTrust Corporation

- Delinea Inc.

- One Identity LLC

- IBM Corporation

- Broadcom Inc.

- ARCON TechSolutions Pvt. Ltd.

- WALLIX Group SA

- Micro Focus International plc

- ManageEngine-Zoho Corporation Pvt. Ltd.

- Hitachi ID Systems Inc.

- Senhasegura-MT4 Tecnologia Ltda.

- Keeper Security Inc.

- Thales Group(Gemalto NV)

- Fudo Security Sp. z oo

- Ekran System Inc.

- Saviynt Inc.

- Ericom Software Ltd.

- Quest Software Inc.

- Bravura Security Inc.

第7章 市場機會與未來趨勢

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the privileged access management market size is expected to increase from USD 4.25 billion in 2025 to USD 5.17 billion in 2026 and reach USD 13.83 billion by 2031, growing at a CAGR of 21.72% over 2026-2031.

This report is Segmented by Component (Solutions & Services), Deployment Mode (On-Premises and More), Organization Size (Large Enterprises and Small & Medium Enterprises), End-User Industry (BFSI & More), Type of Access Control (Shared/Privileged Account Management, Application To Application Password Management, & More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Privileged Access Management Market Trends and Insights

Rapid Proliferation of Machine Identities and Secrets Management Complexity

Organisations running microservices, containers, and event-driven architectures now generate thousands of short-lived service accounts every day, creating a credential-sprawl problem that legacy vaults cannot absorb. CyberArk observes ratios of 40 machine identities for every human identity, and 87% of enterprises admit to storing secrets in multiple, unmanaged locations. Vendor roadmaps respond with automated discovery, rotation, and behavioural analytics tuned to non-human accounts, a capability highlighted by Saviynt's research that calls for machine-identity-specific lifecycle policies.

Zero-Trust Architectures Accelerating Privileged Session Isolation

Government frameworks such as the United States Department of Defense Zero Trust Execution Roadmap require privileged access management controls by FY 2027, confirming that just-in-time provisioning and continuous session validation are mandatory inside zero-trust blueprints. Enterprises in finance and healthcare mirror these mandates, causing PAM vendors to integrate with identity federations, micro-segmentation gateways, and behavioural risk engines that revoke privileges when contextual risk rises.

Skills Scarcity for PAM Deployment and Lifecycle Governance

Identity-security programmes demand expertise across cryptography, directory services, and API integration-skills in chronic short supply worldwide. Enterprises often discover that staff versed in traditional identity governance struggle to operate cloud-native analytics modules that rely on machine-learning models. Large banks and healthcare networks offset the gap through long-term managed service contracts, while many SMEs postpone projects until external consultants become available. Vendor response includes low-code policy builders and prescriptive deployment templates that reduce configuration time but cannot fully eliminate the need for skilled practitioners.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native PAM Demand from DevSecOps Tool-Chain Integration

- AI-Driven Attack-Surface Discovery Boosting PAM Adoption in OT and IoT

- Brownfield Integration Complexity Across Hybrid Legacy Estates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The solutions category dominated the privileged access management market, accounting for 64.10% revenue share in 2025, while the services category is projected to grow at 24.40% CAGR through 2031. Platform consolidation remains the primary buying criterion as enterprises favour unified vaulting, session isolation, and entitlement analytics delivered within a single console. The privileged access management market size for solutions reached USD 2.72 billion in 2025 and is forecast to exceed USD 8.2 billion by 2031, whereas services will climb from USD 1.53 billion to USD 5.65 billion during the same horizon. CyberArk's USD 1.54 billion acquisition of Venafi illustrates a vendor playbook that merges machine-identity management with human-privilege workflows. Buyers cite lower integration costs and faster audit readiness as decisive factors when selecting all-in-one platforms over point products.

Services growth is propelled by three factors: a chronic shortage of identity-security experts, rising complexity in hybrid estates, and the shift toward outcome-based managed services that bundle tool licensing with 24X7 monitoring. Managed service providers advertise predictable subscription pricing that aligns with OpEx-oriented security budgets, particularly among SMEs. Continuous advisory services also help enterprises keep pace with quarterly compliance updates and emerging post-quantum cryptography guidelines, allowing service partners to maintain double-digit expansion throughout the decade.

Cloud deployments captured 57.05% of privileged access management market share in 2025, reflecting buyer preference for SaaS-delivered vaults and policy engines that avoid on-premises hardware. The privileged access management market size for cloud deployments reached USD 2.42 billion in 2025, with a projected USD 7.75 billion valuation by 2031. Hybrid implementations, however, post the fastest 24.10% CAGR as enterprises bridge on-premises mainframes and air-gapped OT networks with cloud control planes. SSH Communications Security's PrivX offers side-by-side password vaulting and certificate-based brokerage, enabling phased migration without downtime.

Persistent regulatory requirements in defence, utilities, and payment processing keep on-premises deployments relevant, especially where data sovereignty statutes forbid external key stores. Vendors mitigate migration risk through containerised vault appliances that run inside private clouds yet replicate metadata to SaaS analytics clusters, offering a compromise between local control and cloud-scale insights. Over the forecast period, hybrid adoption will outpace pure cloud in verticals with significant legacy footprints, while green-field digital natives will remain fully SaaS.

Geography Analysis

North America retained 38.10% privileged access management market share in 2025, reflecting regulatory impetus from federal zero-trust mandates and high breach-cost awareness. The United States Treasury's crackdown on ransomware-facilitated money laundering compels banks and insurers to treat privileged access as a control of first resort. Canada follows similar patterns through updated PIPEDA guidelines, while Mexico's financial authorities impose vaulting requirements on cross-border payment service providers. Market incumbents maintain extensive partner ecosystems, enabling rapid scaling of managed PAM consumption models.

Asia-Pacific will rise at a 23.60% CAGR through 2031, the fastest worldwide trajectory. Singapore's Monetary Authority guidelines require privileged access controls across banking infrastructures, setting a benchmark that ripples across ASEAN member states. Japan's mature cyber-security culture drives platform refresh cycles; Zoho Japan secured 46.2% shipment share in 2023 via its Password Manager Pro offering, while NTT TechnoCross captured consecutive industry awards for domestic PAM leadership. Growth in China and India stems from smart-manufacturing programmes and data-localisation statutes that require strong audit trails for administrator actions.

Europe notes steady adoption due to GDPR and the EU Network and Information Security Directive that penalise inadequate privileged-account protection. Germany and the United Kingdom head regional spending because automotive, financial, and telecom operators face explicit privileged-access clauses within national security legislation. The UK Telecommunications Security Act obliges carriers to implement privileged session controls before 2024 network upgrades, reinforcing the solution priority. Southern Europe and the Nordics exhibit emerging demand, spurred by government digital-transformation funds and heightened ransomware exposure in healthcare systems.

Middle East and Africa display nascent yet accelerating demand, driven by oil-and-gas OT modernisation, sovereign cloud rollouts, and national-level cyber-security strategies. Gulf Cooperation Council banks and utilities increasingly require PAM certification in tender documents, pushing international vendors to establish local data centres and Arabic language support. South Africa and Kenya lead sub-Saharan adoption because of mobile-money ecosystem growth that raises credential-abuse risks.

- CyberArk Software Ltd.

- BeyondTrust Corporation

- Delinea Inc.

- One Identity LLC

- IBM Corporation

- Broadcom Inc.

- ARCON TechSolutions Pvt. Ltd.

- WALLIX Group SA

- Micro Focus International plc

- ManageEngine - Zoho Corporation Pvt. Ltd.

- Hitachi ID Systems Inc.

- Senhasegura - MT4 Tecnologia Ltda.

- Keeper Security Inc.

- Thales Group (Gemalto NV)

- Fudo Security Sp. z o.o.

- Ekran System Inc.

- Saviynt Inc.

- Ericom Software Ltd.

- Quest Software Inc.

- Bravura Security Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid proliferation of machine identities and secrets management complexity

- 4.2.2 Zero-trust architectures accelerating privileged session isolation

- 4.2.3 Cloud-native PAM demand from DevSecOps tool-chain integration

- 4.2.4 AI-driven attack surface discovery boosting PAM adoption in OT and IoT

- 4.2.5 Stringent cyber-insurance underwriting requirements

- 4.2.6 Post-quantum crypto transition pressure on credential vaulting

- 4.3 Market Restraints

- 4.3.1 Skills scarcity for PAM deployment and lifecycle governance

- 4.3.2 Brownfield integration complexity across hybrid legacy estates

- 4.3.3 Shadow-IT proliferation undermining policy enforcement

- 4.3.4 High TCO for SMEs amid subscription sprawl

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Energy and Utilities

- 5.4.8 Other End-user Industries

- 5.5 By Type of Access Control

- 5.5.1 Shared/Privileged Account Management

- 5.5.2 Application to Application Password Management (AAPM)

- 5.5.3 Endpoint Privilege Management (EPM)

- 5.5.4 Cloud and SaaS Privilege Management

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CyberArk Software Ltd.

- 6.4.2 BeyondTrust Corporation

- 6.4.3 Delinea Inc.

- 6.4.4 One Identity LLC

- 6.4.5 IBM Corporation

- 6.4.6 Broadcom Inc.

- 6.4.7 ARCON TechSolutions Pvt. Ltd.

- 6.4.8 WALLIX Group SA

- 6.4.9 Micro Focus International plc

- 6.4.10 ManageEngine - Zoho Corporation Pvt. Ltd.

- 6.4.11 Hitachi ID Systems Inc.

- 6.4.12 Senhasegura - MT4 Tecnologia Ltda.

- 6.4.13 Keeper Security Inc.

- 6.4.14 Thales Group (Gemalto NV)

- 6.4.15 Fudo Security Sp. z o.o.

- 6.4.16 Ekran System Inc.

- 6.4.17 Saviynt Inc.

- 6.4.18 Ericom Software Ltd.

- 6.4.19 Quest Software Inc.

- 6.4.20 Bravura Security Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

Frost Radar™:特權存取管理,2026 年全球特權存取管理,2025-2030 年

Frost Radar™:特權存取管理,2026 年全球特權存取管理,2025-2030 年 特權存取管理市場:2026-2032年全球市場預測(按組件、憑證類型、身分驗證方法、部署模式、組織規模和最終用戶產業分類)

特權存取管理市場:2026-2032年全球市場預測(按組件、憑證類型、身分驗證方法、部署模式、組織規模和最終用戶產業分類) 2026年全球特權存取管理解決方案市場報告全球特權存取管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球特權存取管理解決方案市場報告全球特權存取管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 特權存取管理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、部署模式、企業規模、產業垂直領域、地區和競爭格局分類,2021-2031 年)

特權存取管理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、部署模式、企業規模、產業垂直領域、地區和競爭格局分類,2021-2031 年) 特權存取管理市場報告:2031 年趨勢、預測與競爭分析

特權存取管理市場報告:2031 年趨勢、預測與競爭分析 特權存取管理解決方案市場(全球,2025-2029)

特權存取管理解決方案市場(全球,2025-2029) 特權存取管理解決方案市場規模、佔有率和成長分析(按組件、部署模式、組織規模、應用、垂直和地區)- 產業預測 2025-2032

特權存取管理解決方案市場規模、佔有率和成長分析(按組件、部署模式、組織規模、應用、垂直和地區)- 產業預測 2025-2032 特權存取管理市場機會、成長促進因素、產業趨勢分析與預測 2025 - 2034 年

特權存取管理市場機會、成長促進因素、產業趨勢分析與預測 2025 - 2034 年