|

市場調查報告書

商品編碼

2061986

Kairomon:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Kairomones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

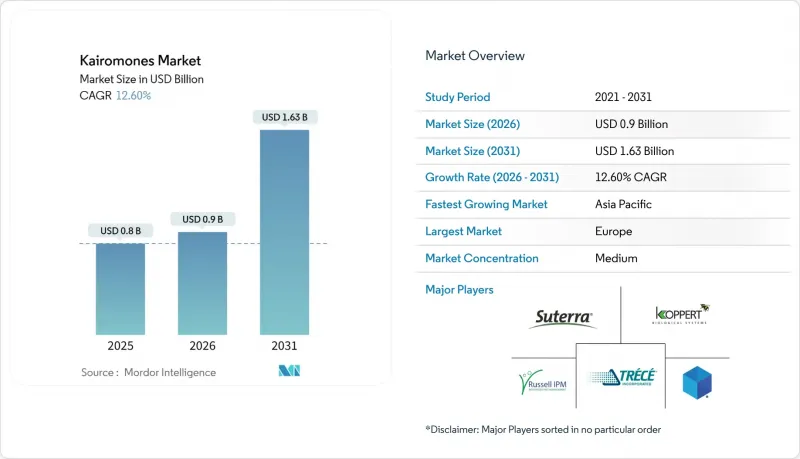

根據 Mordor Intelligence 預測,信息素市場規模將從 2025 年的 8 億美元成長到 2026 年的 9 億美元,到 2031 年達到 16.3 億美元,2026 年至 2031 年的複合年成長率為 12.6%。

本報告按功能(大規模捕獲、檢測和監測、交配抑制及其他功能)、作物類型(田間作物、園藝作物、種植作物、花卉及其他作物類型)和地區(北美、南美、歐洲、亞太地區以及中東和非洲)進行分類。市場預測以美元計價。

全球 Kairomon 市場趨勢與洞察

採取措施規範廣譜殺蟲劑的替代品

世界各國政府正收緊農藥殘留標準,迫使生產商採用風險較低的替代方案。這一轉變促進了在綜合蟲害管理(IPM)框架下使用信息素引誘劑。歐盟於2022年提案的《永續使用條例》(SUR)旨在鼓勵使用非化學替代方案,並透過2030年將風險降低50%來促進IPM的實施。在加拿大,加拿大衛生署的農藥再評估計畫持續審查訊息化合物,以確保持續的法律規範。這些監管趨勢正在促進農藥使用量的減少,並幫助生產商達到全球良好農業規範(GlobalG.AP)和雨林聯盟等認證標準。

生物發酵訊息化合物的單位價格降低

生物發酵訊息化合物成本的下降促使基於信息素的解決方案在作物保護領域得到更廣泛的應用。代謝工程和發酵製程的改進提高了生產效率,實現了複雜揮發性化合物的規模化和成本效益型生產。例如,2021年發表在《生物工程與生物技術》(Bioengineering and Biotechnology)雜誌上的一項研究表明,基因改造的解脂耶氏酵母(Yarrowia lipolytica)可以作為高效的微生物平台,用於生產昆蟲信息素及相關訊息化合物。與傳統微生物系統相比,代謝工程的進步顯著提高了生產效率。

報名費用高昂

在歐盟,建立每種活性成分的身份、純度、功效和環境動力學方面的文件成本高昂,核准過程可能需要數年時間。日本和澳洲也面臨類似的監管挑戰,這使得像Suterra LLC這樣資金雄厚的公司擁有競爭優勢,但小規模、具有創新精神的公司通常選擇獲得配方許可,而不是獨立註冊。根據經合組織生物農藥經濟合作暨發展組織小組的說法,目前正在努力建立一個相互認可的框架,但進展仍然緩慢。

細分市場分析

檢測和監測領域仍佔據信息素市場最大佔有率,預計到2025年將佔41%的市場佔有率。然而,在歐洲和北美等地區,該領域正日趨成熟,基於引誘劑的調查方法已被廣泛應用。交配抑制市場預計將呈現最高的成長率,從2026年到2031年將以18%的複合年成長率成長,超過12.6%的整體市場成長率。這一成長主要得益於生產成本的降低以及大規模作物保護策略中應用的增加。同時,在肯亞和巴西等地區,大規模誘捕方法持續獲得穩定發展,這得益於配方技術的進步,即使在惡劣的環境條件下也能提高田間性能。

2022年,全球永續資訊素害蟲防治解決方案供應商Suterra LLC宣布,其四款成熟產品已獲得有機材料審查組織(OMRI)的註冊,可用於有機農業生產。此外,在肯亞園藝領域,Russell IPM Ltd的AI驅動誘捕系統結合交配抑制方案,能夠實現基於數據的害蟲防治決策。這些進展反映了近期行業發展趨勢:從「以檢測為中心的解決方案」轉向「抑制策略」。而這項轉變的驅動力在於數位化農業工具的整合應用。

區域分析

在費洛蒙市場,預計到2025年,歐洲將佔據29%的市場佔有率,繼續保持最大的區域市場地位。這一主導地位歸功於法國、德國和荷蘭等國健全的法規結構,以及綜合蟲害管理(IPM)實踐的廣泛應用。該地區正受益於政策主導的永續農業轉型、生物基半化學品本地產量的增加以及積極參與區域創新項目。此外,在以永續性為導向的農業舉措的支持下,基於信息素的解決方案正在東歐市場逐步獲得認可。

亞太市場預計將呈現最高成長率,2026年至2031年的複合年成長率預計為15.8%。這一成長主要得益於中國和印度等國家生物農藥的日益普及、政府的利好政策以及國內生產能力的提升。此外,將數位化農業工具與半化學農藥的應用相結合,尤其是在高價值作物系統中,也呈現日益成長的趨勢。然而,農村地區的基礎設施和實施方面的挑戰導致全部區域市場擴張不平衡。

北美作為信息素市場的監管和創新中心,繼續發揮至關重要的作用。不斷變化的政策正在推動生產者採用訊息化合物化學解決方案。在南美,合作社主導的分銷模式以及商業農業中永續病蟲害管理實踐的廣泛應用,使得市場佔有率不斷成長。在非洲和中東,信息素解決方案正逐漸獲得認可,尤其是在人工林和出口作物領域。監測技術的進步和人們對無殘留農業實踐認知的提高,都為這一成長提供了支持。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 採取措施規範廣譜殺蟲劑的替代品

- 降低生物發酵訊息化合物的單位成本

- 將智慧 Kairomon 誘餌引進精密農業

- 適用於高溫脅迫地區的氣候適應型殺蟲劑組合

- 利用 CRISPR 技術建構的微生物底盤,用於合成叢集化合物

- 利用數位雙胞胎模型最佳化Kyromon發布

- 市場限制因素

- 跨多個司法管轄區的高額註冊費

- 炎熱潮濕氣候下的磁場不穩定性

- 發展中農業經濟體最後一公里物流的不足

- 低成本合成費洛蒙引發的品牌內競爭

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按功能

- 大規模陷阱

- 檢測和監測

- 交配抑制

- 其他功能

- 按作物類型

- 田間作物

- 園藝作物

- 種植作物

- 花卉栽培

- 其他作物類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 俄羅斯

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Suterra LLC

- Russell IPM Ltd

- Synergy Semiochemicals Corp.

- Koppert Biological Systems BV

- Trece, Inc.

- Bioglobal Holdings Limited

- Chemtica Internacional, SA

- Rincon-Vitova Insectaries, Inc.

- Harmony Ecotech Private Limited

- SANIDAD AGRICOLA ECONEX, SL

- SOSPALM

- Colkim Srl

- Novagrica Hellas SA

- Provivi, Inc.

- ISCA Technologies, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the kairomones market size is projected to grow from USD 0.80 billion in 2025 to USD 0.90 billion in 2026, reaching USD 1.63 billion by 2031, with a CAGR of 12.6% during the 2026-2031 period.

This report is Segmented by Function (Mass Trapping, Detection and Monitoring, Mating Disruption, and Other Functions), by Crop Type (Field Crops, Horticulture Crops, Plantation Crops, Floriculture, and Other Crop Types), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Kairomones Market Trends and Insights

Regulatory Push to Replace Broad-Spectrum Insecticides

Governments are increasingly implementing stricter residue limits, prompting growers to adopt low-risk alternatives. This shift is encouraging the use of kairomone lures within integrated pest management (IPM) frameworks. The Sustainable Use Regulation (SUR), proposed by the European Union in 2022, seeks to enhance the adoption of integrated pest management (IPM) by encouraging the use of non-chemical alternatives and reducing the risk by 50% by 2030. In Canada, Health Canada's pesticide re-evaluation programs continue to review semiochemical substances, demonstrating ongoing regulatory oversight. These regulatory developments promote reduced insecticide usage and assist growers in meeting certification standards such as GlobalG.A.P. and Rainforest Alliance.

Falling Unit-Cost of Bio-Fermented Semiochemicals

Declining unit costs of bio-fermented semiochemicals are driving increased adoption of kairomone-based solutions in crop protection. Improvements in metabolic engineering and fermentation processes have enhanced production efficiency, enabling scalable and cost-effective manufacturing of complex volatile compounds. For instance, a study published in Bioengineering and Biotechnology in 2021 indicates that engineered Yarrowia lipolytica serves as an effective microbial platform for producing insect pheromones and related semiochemicals. Advances in metabolic engineering have notably enhanced production efficiency compared to previous microbial systems.

High Multi-Jurisdictional Registration Fees

The preparation of identity, purity, efficacy, and environmental fate dossiers incurs high costs per active substance in the European Union, with approval processes taking several years. Comparable regulatory challenges in Japan and Australia provide a competitive edge to well-funded companies like Suterra LLC, while smaller innovators often opt to license formulations instead of pursuing independent registrations. According to the Organisation for Economic Co-operation and Development Biopesticide Steering Group, efforts are being made to establish mutual recognition frameworks, though progress remains slow.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Ag Adoption of Smart Kairomone Lures

- Climate-Smart Repellent Portfolios for Heat-Stressed Regions

- Field Instability in Hot and Humid Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The detection and monitoring segment remains the largest in the kairomones market, accounting for 41% of the market share in 2025. However, this segment is maturing in regions such as Europe and North America, where lure-based scouting methods are already widely adopted. The mating disruption market size is projected to grow at the fastest rate, with a CAGR of 18% from 2026 to 2031, surpassing the overall market growth rate of 12.6%. This growth is driven by declining production costs and increasing adoption in large-scale crop protection strategies. Meanwhile, mass trapping continues to gain steady traction in regions like Kenya and Brazil, supported by advancements in formulation technologies that improve field performance under challenging environmental conditions.

In 2022, Suterra LLC, a global provider of sustainable pheromone pest control solutions, announced that four of its established products are now listed with the Organic Materials Review Institute (OMRI) for use in organic agricultural production. Further, Russell IPM Ltd's artificial intelligence (AI)-enabled trapping systems in Kenya's floriculture sector, facilitating data-driven pest control decisions in alignment with mating disruption programs. These developments reflect a broader industry trend observed in recent years, transitioning from detection-focused solutions to disruption strategies. This shift is influenced by the integration of digital agriculture tools.

Geography Analysis

Europe remained the largest regional segment in the kairomones market, holding a 29% market share in 2025. This dominance is attributed to robust regulatory frameworks and the widespread adoption of integrated pest management practices in countries such as France, Germany, and the Netherlands. The region benefits from policy-driven transitions toward sustainable agriculture, increased local production of bio-based semiochemicals, and active participation in regional innovation programs. Additionally, Eastern European markets are gradually adopting kairomone-based solutions, supported by sustainability-focused agricultural initiatives.

The Asia-Pacific market size is projected to grow at the fastest rate, with a projected CAGR of 15.8% from 2026 to 2031. Growth in this region is driven by increasing biopesticide adoption, favorable government policies, and rising domestic production capabilities in countries like China and India. The integration of digital agriculture tools with semiochemical applications, particularly in high-value crop systems, is also gaining traction. However, infrastructure and adoption challenges in rural areas create a varied pace of market expansion across the region.

North America continues to play a pivotal role as a regulatory and innovation hub for the kairomones market. Evolving policies are encouraging broader adoption of semiochemical-based solutions among growers. South America is enhancing its market presence through cooperative-led distribution models and the increasing use of sustainable pest management practices in commercial agriculture. The Middle East and Africa are witnessing a gradual uptake of kairomone-based solutions, particularly in plantation and export-oriented crops. This growth is supported by advancements in monitoring technologies and a growing awareness of residue-free agricultural practices.

- Suterra LLC

- Russell IPM Ltd

- Synergy Semiochemicals Corp.

- Koppert Biological Systems B.V.

- Trece, Inc.

- Bioglobal Holdings Limited

- Chemtica Internacional, S.A.

- Rincon-Vitova Insectaries, Inc.

- Harmony Ecotech Private Limited

- SANIDAD AGRICOLA ECONEX, S.L.

- SOSPALM

- Colkim S.r.l.

- Novagrica Hellas S.A.

- Provivi, Inc.

- ISCA Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push to replace broad-spectrum insecticides

- 4.2.2 Falling unit-cost of bio-fermented semiochemicals

- 4.2.3 Precision-ag adoption of smart kairomone lures

- 4.2.4 Climate-smart repellent portfolios for heat-stressed regions

- 4.2.5 Clustered Regularly Interspaced Short Palindromic (CRISPR)-engineered microbial chassis for volatile synthesis

- 4.2.6 Digital-twin modeling that optimizes kairomone release

- 4.3 Market Restraints

- 4.3.1 High multi-jurisdictional registration fees

- 4.3.2 Field instability in hot and humid climates

- 4.3.3 Patchy last-mile distribution in developing agri-economies

- 4.3.4 Brand cannibalization from low-priced synthetic pheromones

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Mass Trapping

- 5.1.2 Detection and Monitoring

- 5.1.3 Mating Disruption

- 5.1.4 Other Functions

- 5.2 By Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticulture Crops

- 5.2.3 Plantation Crops

- 5.2.4 Floriculture

- 5.2.5 Other Crop Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Russia

- 5.3.3.4 United Kingdom

- 5.3.3.5 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Kenya

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Suterra LLC

- 6.4.2 Russell IPM Ltd

- 6.4.3 Synergy Semiochemicals Corp.

- 6.4.4 Koppert Biological Systems B.V.

- 6.4.5 Trece, Inc.

- 6.4.6 Bioglobal Holdings Limited

- 6.4.7 Chemtica Internacional, S.A.

- 6.4.8 Rincon-Vitova Insectaries, Inc.

- 6.4.9 Harmony Ecotech Private Limited

- 6.4.10 SANIDAD AGRICOLA ECONEX, S.L.

- 6.4.11 SOSPALM

- 6.4.12 Colkim S.r.l.

- 6.4.13 Novagrica Hellas S.A.

- 6.4.14 Provivi, Inc.

- 6.4.15 ISCA Technologies, Inc.

7 Market Opportunities and Future Outlook

信息素市場規模、佔有率和成長分析:按產品類型、形態、應用、目標害蟲、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

信息素市場規模、佔有率和成長分析:按產品類型、形態、應用、目標害蟲、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 信息素市場預測至2034年:按類型、作物、功能和地區分類的全球分析

信息素市場預測至2034年:按類型、作物、功能和地區分類的全球分析 綜合蟲害管理(IPM)信息素市場報告:按產品、功能、應用方法、用途和地區分類(2026-2034 年)

綜合蟲害管理(IPM)信息素市場報告:按產品、功能、應用方法、用途和地區分類(2026-2034 年) 綜合蟲害防治費洛蒙市場:依產品類型、作用機轉、應用及地區分類

綜合蟲害防治費洛蒙市場:依產品類型、作用機轉、應用及地區分類 Kairomon全球市場報告2026

Kairomon全球市場報告2026 全球綜合蟲害管理(IPM)信息素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資訊素市場規模、佔有率、成長及全球市場分析:按類型、應用和地區分類,並預測至2026-2034年訊息化合物市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測2026年全球半化學品市場報告

全球綜合蟲害管理(IPM)信息素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資訊素市場規模、佔有率、成長及全球市場分析:按類型、應用和地區分類,並預測至2026-2034年訊息化合物市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測2026年全球半化學品市場報告 資訊素市場:按類型、來源、劑型、應用和最終用戶分類,全球預測,2026-2032年

資訊素市場:按類型、來源、劑型、應用和最終用戶分類,全球預測,2026-2032年