|

市場調查報告書

商品編碼

2061984

汽車護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Car Care Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

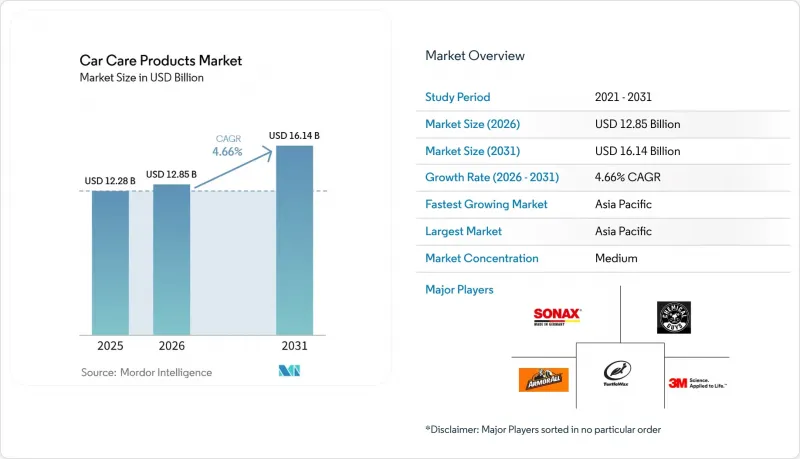

根據 Mordor Intelligence 預測,汽車護理產品市場規模預計將在 2025 年達到 122.8 億美元,2026 年達到 128.5 億美元,到 2031 年達到 161.4 億美元,2026 年至 2031 年的複合年成長率為 4.66%。

本報告按產品類型(清潔/洗車、拋光/打蠟、內裝護理等)、分銷管道(線上、線下)、劑型(液體等)、應用領域(外部、內部)、終端用戶行業(DIY、專業)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球汽車護理產品市場趨勢及洞察

汽車銷售成長與售後市場擴張

預計到2025年,歐洲新車註冊量將達到1,100萬輛,其中電池式電動車(BEV)將佔19%。純電動車註冊量的成長推動了對感測器安全清潔劑和非導電車載消毒劑的需求。同時,預計到2025年,美國汽車售後市場規模將達到1,427.7億美元。這一成長主要受車輛老化(平均使用壽命為12年)的驅動,導致消費者在修復拋光劑和輪胎保養產品上的支出增加。在巴西,全套汽車美容套餐的價格高達2800雷亞爾(約560美元),顯示市場對高階塗層產品有著強烈的購買意願。中國佔全球空氣清新劑產量的70%以上,是全球成長的主要驅動力,但也面臨日益嚴峻的合規風險。特別是,一些不合格的凝膠產品被發現甲醛含量遠超過歐盟基準值兩個數量級以上。

消費者對預防性維護的意識日益增強

2022年,美國家庭平均年行駛里程降至7,937英里。然而,隨著車輛使用年限的延長,消費者越來越重視車輛的耐用性而非外觀。印度中央污染控制委員會已將車內揮發性有機化合物(VOC)濃度限制在500微克/立方公尺。此外,68%的印度車主對現有空氣清新劑的效果不滿意,這為經認證的低排放替代品提供了明顯的市場機會。到了2025年,英國特許經營公司「Revive!」完成27萬次維修,累計2650萬英鎊(3,360萬美元)的銷售額。這印證了外包給專業機構(尤其是使用商用級拋光劑的機構)的趨勢日益成長。

來自不知名品牌的巨大價格壓力

在印度、東南亞和拉丁美洲部分地區,低價無品牌清潔劑的激增迫使全球品牌推出小包裝和更低的促銷價格。這項挑戰在網路市場尤為突出,未經監管的進口產品往往能逃避審查,並以比正品低30%至40%的價格出售。因此,除非品牌能夠透過卓越的性能或永續性來證明其高價的合理性,否則其利潤率將不斷下降。儘管執法進展緩慢,但印尼和墨西哥海關近期查獲的假洗衣液表明,到2026年,監管力度將會加大。為了因應這項挑戰,各大品牌正在實施QR碼溯源,並進行微型網紅行銷主導,以教育消費者了解仿冒品的宣傳活動。

細分市場分析

預計到2025年,汽車護理產品市場中,清潔和洗車產品將佔銷售額的50.26%。內裝護理是成長最快的細分市場,複合年成長率達5.26%,這主要得益於車主擁有車輛的周期延長以及人們對車內空氣質量日益重視,從而帶動了內飾護理劑和除臭劑消費量的成長。雖然外飾洗車液仍然佔據主導地位,但由於陶瓷和石墨烯塗層的興起延長了重新噴漆的間隔時間,其成長速度正在放緩。符合印度新標準BIS IS 17359:2020的特種除臭劑也越來越受歡迎,並因其低VOC(揮發性有機化合物)含量而備受青睞。

拋光和打蠟產品正面臨來自新一代塗層產品的替代壓力,後者承諾可保持數年的耐久性。玻璃清潔劑以及輪圈和輪胎相關產品仍保持著中等個位數的成長,但在一些地區,例如中國《T/CPQS A0042-2025》等法規結構正在推動低排放量車載產品,這些產品的需求仍然穩定。產品系列的兩極化現象十分明顯。商品化的清潔劑在商店價格上競爭,而高科技塗層和車載護理產品則憑藉其卓越的性能宣稱來支撐高價。

到2025年,實體店憑藉其面對面的產品體驗和捆綁銷售策略,將佔據全球銷售額的71.12%,佔據主導地位。同時,由於YouTube教學與AR技術簡化了多步驟塗層工藝,線上銷售也呈現上升趨勢,年複合成長率達6.16%。像SOFT99的「Subs99」這樣的訂閱模式,雖然目前普及率仍低於15%,但正在將一次性購買轉化為穩定且持續的收入來源。

數位化進程並不均衡。北美和西歐處於領先,而亞太地區的本地消費者仍然傾向於選擇本地汽車零件商店。 Valvoline於2025年12月收購了162家Breeze Autocare門市,凸顯了全通路整合的重要性,也顯示了提高門市密度如何能夠促進在換油櫃檯交叉銷售高階潤滑油。

區域分析

預計到2025年,亞太地區將佔汽車護理產品市場37.95%的佔有率,並在2031年之前以5.89%的複合年成長率成長。先前,實驗室檢測顯示,中國生產的標榜「環保」的空氣清新劑凝膠中,有42%的甲醛含量超過歐盟基準值的17倍,此後中國收緊了出口管制。這為國內品牌進入市場打開了大門,前提是它們能夠獲得必要的認證。在印度,BIS IS 17359:2020標準和CPCB規定的500µg/m3的VOC閾值正在推動低排放產品的推廣。此外,市場有明顯的缺口,68%的車主對目前使用的空氣清新劑不滿意。 SOFT99是一家日本公司,將於2024年迎來其成立70週年,它像徵著該地區在耐用蠟和塗料方面的悠久傳統。

北美和歐洲仍然是重要的市場,但這兩個地區的市場都已趨於成熟。配方變化的步伐主要受美國環保署 (EPA) 和加州空氣資源委員會 (CARB) 對揮發性有機化合物 (VOC) 的限制所驅動。展望2026年,更嚴格的生態標示標準將限制二氧化鈦和某些半揮發性物質的使用。這項變更迫使配方開發人員考慮使用生物性界面活性劑,同時也要應對印尼2022年棕櫚油出口禁令導致的棕櫚油供應波動帶來的挑戰。受D2C(直接面對消費者)訂閱模式成功推動,美國的線上消費趨勢發展速度高於全球平均。然而,由於2022年美國家庭平均行駛里程僅為7937英里,車輛外部清潔的頻率受到影響。為了彌補這一下降,車內清潔劑和除臭產品的使用量正在增加。

儘管市佔率可能較小,但拉丁美洲、中東和非洲等地區在特定領域正呈現成長態勢。巴西一家汽車美容店將一套全面的陶瓷塗層套餐定價高達 560 美元,凸顯了市場對高耐久性塗層的購買意願。在阿根廷,燃油零售商 YPF 正在將自動隧道式洗車場改造為多層次的便利服務。與此同時,在巴西,一些行動新創公司正在湧現,它們只需 1200 美元的初始投資即可啟動營運。中東地區強烈的紫外線和多塵環境推動了耐輻射密封劑銷售的成長。此外,沿岸地區的市政當局正日益強制推行水資源循環利用,促使人們傾向於選擇低用水量的化學產品。然而,墨西哥北部和南歐的水資源短缺限制了生物界面活性劑原料的產量,促使供應商考慮採用發酵法。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車銷售成長與售後市場擴張

- 消費者對預防性維護的意識日益增強

- 專業級洗車和汽車美容中心數量增加

- 過渡到無水、環保配方

- 由原始設備製造商 (OEM) 提供的護理耗材訂閱包

- 市場限制因素

- 來自非組織品牌的巨大價格壓力

- 經合組織國家對汽車美容氣霧劑中的揮發性有機化合物(VOC)制定了嚴格的規定。

- 成熟經濟體平均駕駛距離減少

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 清潔和洗衣用品

- 拋光和打蠟產品

- 室內護理產品

- 玻璃清潔劑

- 車輪和輪胎護理產品

- 其他

- 透過分銷管道

- 線上

- 離線

- 按形式

- 液體

- 泡沫和噴霧

- 濕紙巾和毛巾

- 透過使用

- 內部的

- 外部的

- 按最終用戶行業分類

- DIY(Do-It-Yourself)

- 專業/服務中心

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- BP plc

- Chemical Guys

- Energizer Auto. Armor All

- Griot's Garage

- Illinois Tool Works Inc.(ITW)

- LIQUI MOLY GmbH

- Malco Products, Inc.

- Meguiar's

- Mothers

- Shell plc

- Simoniz USA

- SOFT99 Corporation

- Sonax GmbH

- Turtle Wax, Inc.

- Wurth Group

- Zep Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the car care products market size is projected to be USD 12.28 billion in 2025, USD 12.85 billion in 2026, and reach USD 16.14 billion by 2031, growing at a CAGR of 4.66% from 2026 to 2031.

This report is Segmented by Product Type (Cleaning & Washing, Polishing & Waxing, Interior Care, and More), Distribution Channel (Online, Offline), Form (Liquids, and More), Application (Exterior, Interior), End-User Industry (DIY, Professional), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Car Care Products Market Trends and Insights

Growing Automotive Sales and Aftermarket Expansion

In 2025, Europe saw new-vehicle registrations climb to 11 million units, with battery-electric vehicles (BEVs) making up 19% of these deliveries. This increase in BEV registrations has spurred a growing demand for sensor-safe cleaners and non-conductive interior disinfectants. Meanwhile, in the U.S., the automotive aftermarket reached USD 142.77 billion in 2025. This growth is largely attributed to an aging fleet, averaging 12 years, which in turn boosts spending on restorative polishes and tire dressings. In Brazil, full-detail packages costing up to BRL 2,800 (equivalent to USD 560) highlight the market's willingness to pay for premium coatings. China, responsible for over 70% of the world's air freshener production, not only drives global growth but also faces increased compliance risks. Notably, some of its substandard gel products have been found to exceed EU formaldehyde limits by significant double-digit multiples.

Rising Consumer Awareness of Preventive Maintenance

In 2022, the average annual mileage for vehicles per U.S. household dropped to 7,937 miles. However, with extended ownership durations, consumers are now prioritizing longevity over mere aesthetics. India's Central Pollution Control Board set a cap of 500 µg/m3 on interior VOC levels. Additionally, with 68% of Indian car owners expressing dissatisfaction with current air-freshener performance, there's a clear market opportunity for certified low-emission alternatives. In 2025, UK franchise Revive! completed 270,000 repairs, generating revenues of GBP 26.5 million (USD 33.6 million). This underscores a trend of increasing outsourcing to specialists, particularly those utilizing commercial-grade polishes.

Intense Price Pressure from Unorganized Brands

In India, Southeast Asia, and parts of Latin America, a surge of low-priced, unbranded detergents is compelling global brands to introduce smaller pack sizes and reduce promotional prices. This challenge is especially pronounced online, where non-compliant imports slip through scrutiny, undercutting their labeled counterparts by 30 to 40%. As a result, margins for branded players shrink, unless they can justify premiums through performance or sustainability credentials. While enforcement has been slow, recent customs seizures of counterfeit wash liquids in Indonesia and Mexico hint at tighter oversight in 2026. In response, brands are adopting QR-code traceability and launching in-house micro-influencer initiatives to educate consumers about counterfeit risks.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Professional Wash/Detail Centers

- Shift Toward Waterless, Eco-Friendly Formulations

- Stringent VOC Caps on Detailing Aerosols in OECD Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cleaning and washing solutions commanded 50.26% of 2025 revenue in the car care products market. Interior care is the fastest-growing slice at 5.26% CAGR because longer ownership and air-quality vigilance raise consumption of conditioners and odor eliminators. The dominance of exterior shampoos remains, yet their growth is capped by ceramic and graphene coatings that extend repaint intervals. Specialty odor neutralizers also respond to new BIS standard IS 17359:2020 in India, rewarding low-VOC labels.

Polishing and waxing face substitution pressure from next-generation coatings promising multi-year durability. Glass cleaners and wheel-and-tire SKUs remain mid-single-digit contributors but enjoy steady demand where regulatory frameworks, such as China's T/CPQS A0042-2025, push low-emission interior products. Portfolio bifurcation is clear: commoditized washes compete on shelf price, while high-tech coatings and cabin treatments justify premium tickets through performance claims.

In 2025, offline outlets accounted for a dominant 71.12% of the global turnover, capitalizing on tactile merchandising and bundled services. Meanwhile, online revenues are on an upward trajectory, growing at a 6.16% CAGR, as YouTube tutorials and AR overlays simplify multi-step coatings. Subscription models, like SOFT99's Subs99, are shifting one-time purchases into a steady stream of recurring revenue, even as attach rates hover below 15%.

Digital adoption is not uniform: North America and Western Europe are leading, while rural buyers in Asia-Pacific still lean towards local parts stores. The importance of omnichannel integration is highlighted by Valvoline's December 2025 acquisition of 162 Breeze Autocare stores, showing how a denser network can enhance the cross-sale of premium liquids at oil-change counters.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 37.95% of the car care products market revenue and is projected to grow at a CAGR of 5.89% through 2031. After laboratory tests revealed that 42% of "eco-friendly" air-freshener gels produced in China surpassed EU formaldehyde limits by 17 times, the country's export scrutiny has tightened. This has paved the way for domestic brands to step in, provided they secure the necessary certifications. In India, the BIS IS 17359:2020 standard and CPCB's VOC threshold of 500 µg/m3 incentivize low-emission products. Furthermore, with 68% of owners expressing dissatisfaction with current air fresheners, there is a clear gap in the market. Celebrating its 70th anniversary in 2024, Japan's SOFT99 underscores the region's rich legacy in durable waxes and coatings.

While North America and Europe continue to be significant players, they are also witnessing maturity in their markets. The pace of reformulation is largely dictated by EPA and CARB's VOC caps. Looking ahead to 2026, tighter Ecolabel standards will limit the use of titanium dioxide and certain semi-volatiles. This shift is pushing formulators to consider bio-based surfactants, even as they navigate the challenges posed by palm-oil supply fluctuations, a consequence of Indonesia's 2022 export ban. The trend of online adoption in the U.S. is outpacing global averages, bolstered by the success of direct-to-consumer subscriptions. However, with U.S. households averaging just 7,937 miles in 2022, the frequency of exterior washes has been impacted. To offset this decline, there has been an increase in the use of interior conditioners and odor management products.

Regions like Latin America, the Middle East, and Africa, though contributing smaller market shares, are witnessing growth in certain areas. Detailers in Brazil are commanding prices of up to USD 560 for comprehensive ceramic packages, highlighting a market willing to pay for high-durability coatings. In Argentina, fuel retailer YPF is transforming automated tunnel washes into multi-tiered convenience services. Meanwhile, in Brazil, mobile start-ups are making their debut with initial investments as modest as USD 1,200. The Middle East's challenging UV and dust conditions are boosting sales of radiation-resistant sealants. Additionally, municipalities in the Gulf are implementing mandatory water-recycling quotas, favoring products with low-water chemistries. However, water scarcity issues in northern Mexico and southern Europe are limiting feedstock yields for bio-surfactants, prompting suppliers to explore fermentation methods.

- 3M

- BP p.l.c

- Chemical Guys

- Energizer Auto. Armor All

- Griot's Garage

- Illinois Tool Works Inc. (ITW)

- LIQUI MOLY GmbH

- Malco Products, Inc.

- Meguiar's

- Mothers

- Shell plc

- Simoniz USA

- SOFT99 Corporation

- Sonax GmbH

- Turtle Wax, Inc.

- Wurth Group

- Zep Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing automotive sales & expanding aftermarket

- 4.2.2 Rising consumer awareness of preventive maintenance

- 4.2.3 Proliferation of professional wash/detail centers

- 4.2.4 Shift toward waterless, eco-friendly formulations

- 4.2.5 OEM-launched subscription bundles for care consumables

- 4.3 Market Restraints

- 4.3.1 Intense price pressure from unorganized brands

- 4.3.2 Stringent VOC caps on detailing aerosols in OECD nations

- 4.3.3 Declining average vehicle miles in mature economies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Cleaning and Washing Products

- 5.1.2 Polishing and Waxing Products

- 5.1.3 Interior Care Products

- 5.1.4 Glass Cleaners

- 5.1.5 Wheel and Tire Care Products

- 5.1.6 Others

- 5.2 By Distribution Channel

- 5.2.1 Online

- 5.2.2 Offline

- 5.3 By Form

- 5.3.1 Liquids

- 5.3.2 Foams and Sprays

- 5.3.3 Wipes and Towelettes

- 5.4 By Application

- 5.4.1 Interior

- 5.4.2 Exterior

- 5.5 By End-user Industry

- 5.5.1 DIY (Do-It-Yourself)

- 5.5.2 Professional / Service Centers

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 BP p.l.c

- 6.4.3 Chemical Guys

- 6.4.4 Energizer Auto. Armor All

- 6.4.5 Griot's Garage

- 6.4.6 Illinois Tool Works Inc. (ITW)

- 6.4.7 LIQUI MOLY GmbH

- 6.4.8 Malco Products, Inc.

- 6.4.9 Meguiar's

- 6.4.10 Mothers

- 6.4.11 Shell plc

- 6.4.12 Simoniz USA

- 6.4.13 SOFT99 Corporation

- 6.4.14 Sonax GmbH

- 6.4.15 Turtle Wax, Inc.

- 6.4.16 Wurth Group

- 6.4.17 Zep Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

汽車蠟市場-2026-2032年全球市場預測矽油汽車護理產品市場:全球預測,2026-2032年汽車護理產品市場:2026-2032年全球市場預測(依產品類型、形態、應用、最終用戶和通路分類)

汽車蠟市場-2026-2032年全球市場預測矽油汽車護理產品市場:全球預測,2026-2032年汽車護理產品市場:2026-2032年全球市場預測(依產品類型、形態、應用、最終用戶和通路分類) 抗菌汽車護理產品市場分析與預測(至2035年):類型、產品、技術、應用、劑型、最終用戶、功能、應用類型、解決方案汽車護理產品市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、形式、材料類型、最終用戶、功能

抗菌汽車護理產品市場分析與預測(至2035年):類型、產品、技術、應用、劑型、最終用戶、功能、應用類型、解決方案汽車護理產品市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、形式、材料類型、最終用戶、功能 汽車刮痕去除劑市場:按類型、應用和地區分類

汽車刮痕去除劑市場:按類型、應用和地區分類 全球液體汽車護理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球液體汽車護理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球香水夾和木工配件市場報告汽車護理產品市場規模、佔有率、成長及全球產業分析:按產品類型、應用和區域分類,預測2026-2034年全球汽車保養產品市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026年全球香水夾和木工配件市場報告汽車護理產品市場規模、佔有率、成長及全球產業分析:按產品類型、應用和區域分類,預測2026-2034年全球汽車保養產品市場規模、佔有率、趨勢和成長分析報告(2026-2034)