|

市場調查報告書

商品編碼

2061962

多智慧體系統(MAS)平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Multi-Agent System (MAS) Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

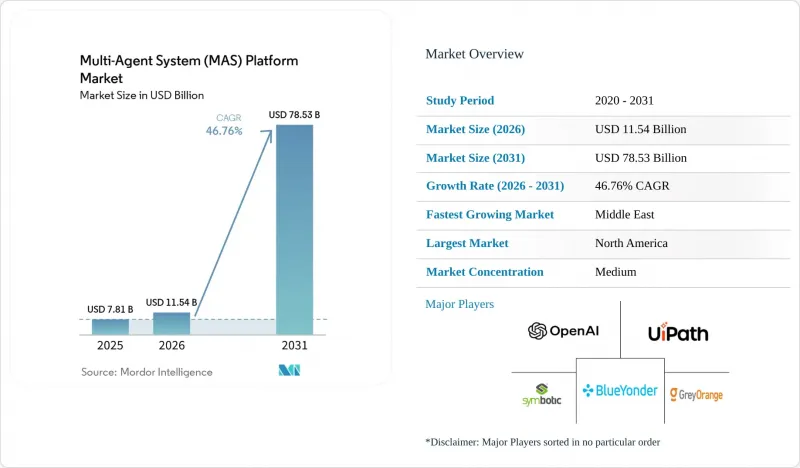

根據 Mordor Intelligence 預測,多智慧體系統平台的市場規模將從 2025 年的 78.1 億美元和 2026 年的 115.4 億美元成長到 2031 年的 785.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 46.76%。

本報告按平台類型(代理開發框架、編配平台、模擬數位雙胞胎套件等)、部署模式(雲端、本地/邊緣等)、最終用戶產業(製造業、供應鏈和物流等)、應用(工作流程和流程協作等)以及地區進行細分。市場預測以美元(USD)為單位。

全球多智慧體系統(MAS)平台市場趨勢與洞察

雲端原生多智慧體系統的應用蓬勃發展

Kubernetes 相容的編配平台使開發人員無需重寫基礎架構即可將代理程式數量從數十個擴展到數千個。微軟的 AutoGen 和 LangGraph Cloud 於 2025 年發布,引入了聲明式模板,可將 YAML說明轉換為可運行的叢集。彈性運算和託管網路縮短了概念驗證(PoC) 週期,而超大規模資料中心業者透過捆綁折扣推理加速器來鎖定客戶,使其留在自己的生態系統中。金融機構和物流公司表示,叢集管理負擔減輕,價值實現時間縮短,進一步強化了推動多代理系統平台市場發展的良性循環。

倉庫自動化中對多機器人編配的需求

如今,履約中心不再只專注於單一機器人的能力,而是著力最佳化整個機器人群聚的生產力。 Locus Robotics公司正在協調300個倉庫中超過6000台自主移動機器人,與人工揀貨相比,訂單處理時間縮短了25%。 Symbotic公司在2024會計年度從沃爾瑪的42個物流中心獲得了5.933億美元的收入,這表明,當編配能夠帶來兩位數的吞吐量提升時,企業願意進行投資。邊緣代理避免了雲端延遲,而基於模擬的預訓練則加速了部署,因此,倉庫自動化被視為推動持續成長的關鍵因素。

缺乏能夠處理多智慧體系統的人員和標準

根據領英發布的《2025年人工智慧人才缺口報告》,68%的公司在招募精通智慧體間通訊和分散式強化學習的工程師方面面臨挑戰,平均招募時間超過90天。缺乏標準化導致供應商需要支援多種本體,增加了新員工入職的難度。此外,全球人才培育體系無法滿足市場需求。人才短缺推高了薪資水平,延長了採用週期,減緩了人工智慧的普及速度。

細分市場分析

預計從2026年到2031年,基於自主代理的SaaS(軟體即服務)交付量將成長47.37%。這一顯著成長反映出買家越來越傾向於選擇能夠簡化分散式系統複雜性的承包訂閱模式。隨著企業尋求可擴展且高效的解決方案,這些模式正推動SaaS領域多代理系統平台的市場規模遠超歷史平均水準。編配平台在2025年仍保持34.63%的收入佔有率,這表明,在提供可靠性、持久性和「僅一次」執行能力的供應商中,成熟的公司已穩固佔據一席之地。

純框架憑藉其柔軟性和可自訂性,持續吸引以工程師主導的組織。然而,由於共識機制和故障檢測的學習曲線陡峭,其普及程度受到限制。 NVIDIA Omniverse 等模擬套件預計到 2025 會計年度將達到 10 億美元的年收入,凸顯了在實際部署前對策略進行虛擬檢驗的日益成長的需求。這一趨勢強調了模擬在降低風險和最佳化實際應用效能方面的重要性。現有企業軟體公司將代理功能整合到 CRM 和 ERP 套件中,由此帶來的競爭壓力預計將擠壓獨立平台的利潤空間。儘管如此,垂直行業專業化和客製化解決方案將有助於緩解商品化的影響,並幫助供應商保持競爭優勢。

預計到2025年,雲端運算將佔據72.58%的市場。這主要歸功於雲端運算的彈性可擴展性和簡化的操作。這項優勢凸顯了多智慧體系統平台市場對基於雲端的解決方案日益成長的偏好。然而,預計到2031年,本地部署和邊緣配置的複合年成長率將高達47.21%。這種快速成長有望縮小雲端運算與其他配置之間的市場佔有率差距。本地部署和邊緣解決方案的日益普及是由對本地資料處理的需求所驅動的,尤其是在製造業和醫院領域。這些機構正努力遵守嚴格的資料保護條例,例如歐盟的《一般資料保護規則》(GDPR),該規範對跨境資料傳輸規定了處罰措施。

技術進步,例如量化模型和低成本推理晶片,使得機器人、POS終端和工業感測器能夠以每百萬令牌不到一美分的成本運行智慧體。這種低成本使得多智慧體系統得以在各行業中普及。此外,將設備端感知迴路與基於雲端的規劃同步相結合的混合拓撲結構,在保持集中管理的同時,顯著降低了延遲。這些混合系統對於需要即時決策和高效運作的應用尤其有利。為了支援此類部署,Microsoft Azure IoT Edge和AWS Greengrass等平台推出了編配增強功能。這些增強功能簡化了分段部署的管理,並確保邊緣設備和雲端基礎架構之間的無縫整合。

區域分析

預計到2025年,北美將佔全球收入的41.38%,這主要得益於超大規模資料中心業者的產品推出以及物流和金融產業的早期應用。 OpenAI與AWS之間價值380億美元的基礎設施夥伴關係凸顯了該地區在擴展混合智慧體工作負載方面的努力。此外,美國一項將自動駕駛汽車與物流鏈相結合的國防計劃,進一步提升了該技術在商業用戶中的合法性,並推動了其在整個行業的更廣泛應用。在歐洲,數據主權和演算法透明度至關重要,領導企業正在試行符合人工智慧標準的基於智慧體的調度系統。 GDPR的限制也推動了對本地部署的需求,因為企業需要遵守嚴格的資料保護條例。政府資助的舉措和大學主導的研究項目持續推動該地區的創新,為多智慧體系統平台市場的整體成長做出了穩步貢獻。

預計中東地區將成為所有地區中複合年成長率最高的地區,2026年至2031年將達到47.11%。沙烏地阿拉伯的NEOM和阿拉伯聯合大公國的杜拜數位雙胞胎等大型專案正在整合能源管理、交通出行和廢棄物管理等功能。該地區的政府資金不僅提供資金支持,還強制要求設定前沿的永續發展目標,為供應商創新和拓展業務創造了有利環境。亞太地區則受惠於中國對智慧城市基礎設施的大量投資、日本成熟的機器人產業以及印度豐富的軟體開發人才。

新加坡的智慧體主導生態社區已成為區域負責人的標桿,展現了智慧體系統在城市發展中的巨大潛力。雖然目前南美和非洲的市場規模較小,但採礦、農業和電信等行業的早期應用正在穩步推進。在這些地區,即使在基礎設施有限的地區,智慧體也被用於最佳化資源配置和提高營運效率,凸顯了其適應性和成長潛力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲原生 MAS 的採用激增

- 倉庫自動化中對多機器人編配的需求

- 融合了基於LLM的智慧體和強化學習框架。

- 邊緣人工智慧成本的降低將使設備內建代理成為可能。

- 代幣獎勵開放式多應用系統協議

- 為那些將安全性放在首位的行業推出代理整合工具包。

- 市場限制因素

- MAS合規人員短缺及標準

- 在代理層級擴大網路安全攻擊面

- GPU和推理晶片供應鏈的波動

- 來自環境、社會及治理(ESG)投資者的壓力,要求提高能源效率

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依平台類型

- 代理開發框架

- 編配平台

- 仿真數位雙胞胎套件

- 自主代理軟體即服務

- 其他平台類型

- 部署模式

- 雲

- 本地部署/邊緣部署

- 產業最終用途

- 製造業

- 供應鍊和物流

- 醫療保健和生命科學

- BFSI

- 智慧城市和基礎設施

- 透過使用

- 工作流程和流程協作

- 多重機器人協作

- 決策支援與規劃

- 仿真數位雙胞胎建模

- 自主交易和財務運營

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 卡達

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OpenAI LLC

- UiPath Inc.

- GreyOrange Inc.

- C3.ai Inc.

- Fetch.ai Foundation Pte Ltd.

- Mindsmiths doo

- CrewAI Inc.

- Swarms AI Inc.

- HASH.ai Ltd.

- Algovera DAO Ltd.

- Emergence AI Inc.

- AgentVerse Technologies Ltd.

- Temporal Technologies Inc.

- Instadeep Ltd.

- Locus Robotics Corp.

- Blue Yonder Group Inc.

- Manus AI

- Onomatic LLC

- Softeon Inc.

- Symbotic Inc.

- Camunda Services GmbH

- Airt Inc.

- Relevance AI Pty Ltd.

- Anthropic PBC

- Cognizant Technology Solutions Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the multi-agent system platform market size is projected to expand from USD 7.81 billion in 2025 and USD 11.54 billion in 2026 to USD 78.53 billion by 2031, registering a CAGR of 46.76% between 2026 and 2031.

This report is Segmented by Platform Type (Agent-Development Frameworks, Orchestration Platforms, Simulation and Digital-Twin Suites, and More), Deployment Mode (Cloud, and On-Premises/Edge), End-Use Industry (Manufacturing, Supply-Chain and Logistics, and More), Application (Workflow and Process Orchestration, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Multi-Agent System (MAS) Platform Market Trends and Insights

Cloud-Native Multi-Agent System Deployment Boom

Kubernetes-compatible orchestration platforms let developers scale from dozens to thousands of agents without rewriting infrastructure. Microsoft's AutoGen and LangGraph Cloud, both launched in 2025, introduced declarative templates that turn YAML descriptions into running clusters. Elastic compute and managed networking shorten proof-of-concept cycles, while hyperscalers bundle discounted inference accelerators that lock customers into their ecosystems. Financial institutions and logistics operators report faster time-to-value once cluster management is offloaded, reinforcing the positive feedback loop that is lifting the multi-agent system platform market.

Warehouse-Automation Demand for Multi-Robot Orchestration

Fulfillment centers now optimize fleet-level productivity rather than individual robot features. Locus Robotics coordinates more than 6,000 autonomous mobile robots across 300 warehouses, cutting order-cycle time by 25% compared with manual picking. Symbotic earned USD 593.3 million from 42 Walmart distribution centers in fiscal 2024, underlining commercial willingness to invest when orchestration delivers double-digit throughput gains. Edge-resident agents avoid cloud latency, and simulation-based pretraining accelerates commissioning, positioning warehouse automation as a durable growth driver.

Scarcity of Multi-Agent-System-Ready Talent and Standards

LinkedIn's 2025 AI Talent Gap Report showed that 68% of enterprises struggle to hire engineers skilled in inter-agent communication and distributed reinforcement learning, stretching median recruitment cycles past 90 days. Fragmented standards complicate onboarding because vendors must support multiple ontologies, while global professional development pipelines lag behind demand. The shortfall inflates salaries and extends implementation timelines, slowing adoption.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of Large-Language-Model-Based Agents and Reinforcement-Learning Frameworks

- Declining Edge-AI Costs Enabling On-Device Agents

- Expanded Cyber-Security Attack Surface at Agent Level

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Autonomous-agent software-as-a-service offerings are forecast to grow at 47.37% between 2026 and 2031. This significant growth reflects the increasing buyer preference for turnkey subscription models that simplify the complexities of distributed systems. These models are driving the multi-agent system platform market size for SaaS well above historical norms, as businesses seek scalable and efficient solutions. Orchestration platforms, which maintained a 34.63% revenue share in 2025, highlight the strong position of incumbents among vendors that provide reliability, durability, and exactly-once execution capabilities.

Pure-play frameworks continue to attract engineering-led organizations due to their flexibility and customization potential. However, the steep learning curve associated with consensus mechanisms and failure detection has limited their broader adoption. Simulation suites, such as NVIDIA Omniverse, achieved a USD 1 billion annual run rate in fiscal 2025, emphasizing the growing demand for virtual validation of policies before physical deployment. This trend underscores the importance of simulation in reducing risks and optimizing performance in real-world applications. Competitive pressure from enterprise-software incumbents bundling agents into CRM and ERP suites is expected to compress standalone platform margins. Nevertheless, vertical specialization and tailored solutions can help mitigate the effects of commoditization, enabling vendors to maintain a competitive edge.

Cloud retained 72.58% of the revenue share in 2025, primarily due to its ability to scale elastically and simplify operations. This dominance highlights the growing preference for cloud-based solutions in the multi-agent system platform market. However, on-premises and edge configurations are projected to achieve a significant compound annual growth rate (CAGR) of 47.21% through 2031. This rapid growth is expected to narrow the market share gap between cloud and other configurations. The increasing adoption of on-premises and edge solutions is driven by the need for localized data processing, particularly among manufacturers and hospitals. These entities aim to comply with stringent data protection regulations, such as the European Union's General Data Protection Regulation (GDPR), which imposes penalties for cross-border data transfers.

Advancements in technology, such as quantized models and cost-effective inference chips, have enabled robots, point-of-sale devices, and industrial sensors to operate agents at a significantly reduced cost-less than one cent per million tokens. This affordability has expanded the accessibility of multi-agent systems across various industries. Additionally, hybrid topologies that combine on-device perception loops with cloud-based planning synchronization offer substantial latency benefits while maintaining centralized oversight. These hybrid systems are particularly advantageous for applications requiring real-time decision-making and operational efficiency. To support such deployments, platforms like Microsoft Azure IoT Edge and AWS Greengrass have introduced orchestration extensions. These enhancements simplify the management of split deployments, ensuring seamless integration between edge devices and cloud infrastructure.

Geography Analysis

North America captured 41.38% of 2025 revenue, driven by hyperscaler product launches and early adoption in logistics and finance. OpenAI and AWS's USD 38 billion infrastructure partnership underscores regional commitment to scaling hybrid-agent workloads. Additionally, the U.S. defense programs that coordinate autonomous vehicles and logistics chains have further legitimized the technology for commercial buyers, encouraging broader adoption across industries. Europe emphasizes data sovereignty and algorithmic transparency, with automotive and industrial automation leaders in Germany piloting agent-based scheduling systems that align with the AI Act. GDPR limitations are also fueling demand for localized deployments, as businesses seek to comply with stringent data protection regulations. Government funding initiatives and university-led research projects continue to drive innovation in the region, ensuring a steady contribution to the overall growth of the multi-agent system platform market.

The Middle East is forecast to record the fastest regional CAGR at 47.11% between 2026 and 2031. Large-scale projects like Saudi Arabia's NEOM and the United Arab Emirates' Dubai Digital Twin are integrating agents for energy management, mobility, and waste management. Sovereign wealth funds in the region are not only supplying capital but also mandating cutting-edge sustainability targets, creating a fertile environment for vendors to innovate and expand. Asia-Pacific benefits from China's significant investments in smart-city infrastructure, Japan's well-established robotics industry, and India's abundant software development talent.

Singapore's agent-driven eco-district serves as a performance benchmark for regional planners, showcasing the potential of agent-based systems in urban development. South America and Africa, while smaller markets today, are demonstrating early adoption in sectors such as mining, agriculture, and telecommunications. In these regions, agents are being used to optimize resource allocation and improve operational efficiency, even in areas with limited infrastructure, highlighting their adaptability and growth potential.

- OpenAI LLC

- UiPath Inc.

- GreyOrange Inc.

- C3.ai Inc.

- Fetch.ai Foundation Pte Ltd.

- Mindsmiths d.o.o.

- CrewAI Inc.

- Swarms AI Inc.

- HASH.ai Ltd.

- Algovera DAO Ltd.

- Emergence AI Inc.

- AgentVerse Technologies Ltd.

- Temporal Technologies Inc.

- Instadeep Ltd.

- Locus Robotics Corp.

- Blue Yonder Group Inc.

- Manus AI

- Onomatic LLC

- Softeon Inc.

- Symbotic Inc.

- Camunda Services GmbH

- Airt Inc.

- Relevance AI Pty Ltd.

- Anthropic P.B.C.

- Cognizant Technology Solutions Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native MAS Deployment Boom

- 4.2.2 Warehouse-Automation Demand for Multi-Robot Orchestration

- 4.2.3 Convergence of LLM-Based Agents and Reinforcement-Learning Frameworks

- 4.2.4 Declining Edge-AI Costs Enabling On-Device Agents

- 4.2.5 Token-Incentivised Open MAS Protocols

- 4.2.6 Emergence of Agent-Alignment Toolkits for Safety-Critical Industries

- 4.3 Market Restraints

- 4.3.1 Scarcity of MAS-Ready Talent and Standards

- 4.3.2 Expanded Cyber-Security Attack Surface at Agent Level

- 4.3.3 GPU and Inference-Chip Supply-Chain Volatility

- 4.3.4 Energy-Efficiency Pressure from ESG Investors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Agent-Development Frameworks

- 5.1.2 Orchestration Platforms

- 5.1.3 Simulation and Digital-Twin Suites

- 5.1.4 Autonomous-Agent SaaS

- 5.1.5 Other Platform Type

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises / Edge

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Supply-Chain and Logistics

- 5.3.3 Healthcare and Life-Sciences

- 5.3.4 BFSI

- 5.3.5 Smart Cities and Infrastructure

- 5.4 By Application

- 5.4.1 Workflow and Process Orchestration

- 5.4.2 Multi-Robot Coordination

- 5.4.3 Decision-Support and Planning

- 5.4.4 Simulation and Digital-Twin Modelling

- 5.4.5 Autonomous Trading and Fin-Ops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Qatar

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI LLC

- 6.4.2 UiPath Inc.

- 6.4.3 GreyOrange Inc.

- 6.4.4 C3.ai Inc.

- 6.4.5 Fetch.ai Foundation Pte Ltd.

- 6.4.6 Mindsmiths d.o.o.

- 6.4.7 CrewAI Inc.

- 6.4.8 Swarms AI Inc.

- 6.4.9 HASH.ai Ltd.

- 6.4.10 Algovera DAO Ltd.

- 6.4.11 Emergence AI Inc.

- 6.4.12 AgentVerse Technologies Ltd.

- 6.4.13 Temporal Technologies Inc.

- 6.4.14 Instadeep Ltd.

- 6.4.15 Locus Robotics Corp.

- 6.4.16 Blue Yonder Group Inc.

- 6.4.17 Manus AI

- 6.4.18 Onomatic LLC

- 6.4.19 Softeon Inc.

- 6.4.20 Symbotic Inc.

- 6.4.21 Camunda Services GmbH

- 6.4.22 Airt Inc.

- 6.4.23 Relevance AI Pty Ltd.

- 6.4.24 Anthropic P.B.C.

- 6.4.25 Cognizant Technology Solutions Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

防撞感測器市場規模、佔有率和成長分析:按感測器機制、運作頻率、應用模式、最終用戶產業和地區分類-2026-2033年產業預測

防撞感測器市場規模、佔有率和成長分析:按感測器機制、運作頻率、應用模式、最終用戶產業和地區分類-2026-2033年產業預測 防撞感測器市場:按車輛類型、感測器類型和應用分類-2026-2032年全球市場預測

防撞感測器市場:按車輛類型、感測器類型和應用分類-2026-2032年全球市場預測 2026-2030年全球多智慧體系統(MAS)平台市場

2026-2030年全球多智慧體系統(MAS)平台市場 全球多智慧體編配平台市場:依產品、容量、部署、編配模式、組織規模及最終用戶產業分類-市場規模、產業動態、機會分析及2026-2035年預測

全球多智慧體編配平台市場:依產品、容量、部署、編配模式、組織規模及最終用戶產業分類-市場規模、產業動態、機會分析及2026-2035年預測 碰撞避免感測器市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析

碰撞避免感測器市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析 2026年全球多智慧體系統市場報告2026年全球防碰撞感測器市場報告

2026年全球多智慧體系統市場報告2026年全球防碰撞感測器市場報告 防撞感測器市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球防撞感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球防撞感測器市場報告

防撞感測器市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球防撞感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球防撞感測器市場報告