|

市場調查報告書

商品編碼

2061941

供應鏈和物流中的智慧體人工智慧:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Agentic AI In The Supply Chain And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

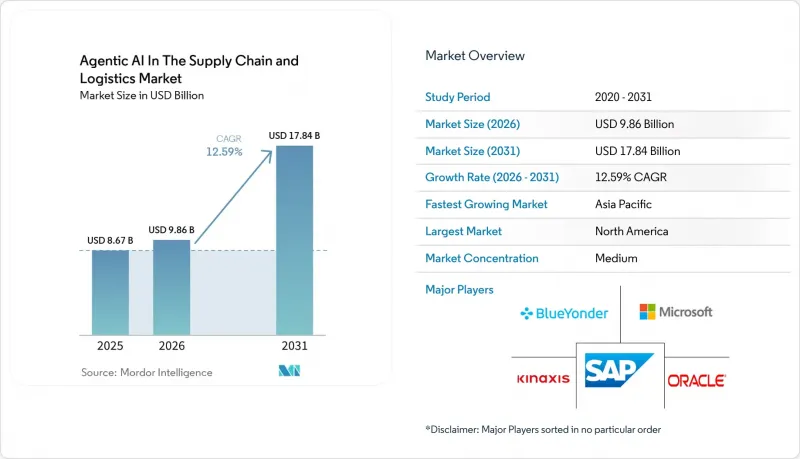

預計到 2026 年,供應鏈和物流領域的智慧人工智慧市場規模將達到 98.6 億美元,到 2031 年將達到 178.4 億美元,同期複合年成長率為 12.59%。

本報告按組件(軟體平台等)、應用(需求預測與規劃、倉儲與履約最佳化等)、產業(零售與電商、製造業、食品飲料等)、部署模式(雲端、本地部署、混合部署)和地區細分。市場預測以美元計價。

全球基於代理的人工智慧市場趨勢及供應鏈和物流的洞察

融合人工智慧代理的雲端原生供應鏈管理平台迅速普及。

雲端超大規模資料中心業者商現在將多代理工具作為其供應鏈套件的一部分,消除了整合障礙,並將決策延遲從數小時縮短到數秒。亞馬遜雲端服務 (AWS) 於 2025 年 5 月推出了“Connect Decisions”,隨後 Oracle 和 SAP 也相繼推出類似服務,提供用於需求預測、貨運預訂和海關文件創建的嵌入式代理。沒有內部人工智慧人才的中型企業可以透過訂閱計畫利用這些功能,但決策歷史在自身雲端環境中的累積會增加平台鎖定風險。

人手不足正在加速倉庫自動化領域的投資。

低失業率和高離職率正迫使物流公司採用由多智慧體框架控制的自主移動機器人和人形系統。 UPS計畫在2025年投資1.2億美元用於人工智慧驅動的卸貨設施,而GXO物流公司在多個地點試點部署了Dexterity和Agility機器人後,生產效率提高了22%。房地產設計標準正朝著機器人友善佈局轉變,無法適應自動化工作流程的老舊設施正被淘汰。

與傳統ERP和TMS系統整合成本高昂

許多中型企業仍然依賴採用批量更新的單體資料庫,這限制了它們採用事件驅動流等先進技術來建立多智慧體人工智慧系統的能力。遷移到這些系統成本高昂,每個物流網路的成本在 500 萬美元到 2,000 萬美元之間,而且實施過程可能需要長達三年。此外,每個智慧體平台都採用其獨特的本體,需要開發客製化的中間件解決方案。這項要求進一步增加了實施過程的複雜性,加劇了擁有資源有效管理這些轉型的大型企業與往往難以跟上步伐的中小型企業之間的生產力差距。

細分市場分析

在供應鏈和物流領域的基於代理的人工智慧市場中,人工智慧驅動的軟體在2025年將佔總收入的57.81%。隨著邊緣推理和機器人技術的融合,供應鏈和物流領域的基於代理的人工智慧硬體市場預計將以13.19%的更快速度成長。半導體價格的下降和預先整合感知堆疊的普及縮短了投資回收期,使得本地承運商更容易獲得自動堆高機和視覺引導揀選等技術。隨著整合商對舊有系統維修、最佳化垂直代理以及培訓主管人員,業務收益也在不斷成長。軟體套件繼續受益於付費使用制和現有的雲端合作關係,使其成為許多新進入者的切入點。

企業只有在對其平台內建的編配邏輯充滿信心後才會部署硬體。基於 Jetson 的機器人和 Gaudi 的輸送機都捆綁了參考代理,可以整合到主流的雲端供應鏈管理 (SCM) 套件中,從而降低整合工作量。這使得超大規模資料中心業者可以透過訂閱式軟體和認證設備生態系統來獲利,而機器人供應商則可以透過專業的機械手臂設計、感測器融合和安全認證來脫穎而出。

需求預測佔2025年預算分配的35.83%,因為許多零售商和製造商已經收集了時間序列和因果模型所需的資料。然而,由於人口密集的城市、當日達的預期以及勞動力短缺,預計「最後一公里編配」將以13.79%的複合年成長率成長。聯邦快遞的先導計畫透過將RFID和路線規劃代理人與車輛和步行機器人連接起來,成功降低了15%的配送成本。倉庫最佳化仍然是核心領域,因為美國倉庫的年周轉率超過43%,預計到2025年將出現40萬個倉庫空缺。

隨著基準資料集規範供應商績效,採購代理的使用日益增加。同時,注重碳排放的車輛路線規劃納入了即時排放數據,以滿足永續性法規的要求。逆向物流和越庫作業目前仍屬於小眾領域,但隨著電子商務退貨和循環經濟規則的興起,它們正在逐步發展壯大。每個細分領域都利用不同的資料模式,但為了消除人工瓶頸,需要進行全面的多方協調。

區域分析

北美擁有成熟的雲端基礎設施,且亞馬遜、UPS 和 FedEx 等公司已率先採用,預計到 2025 年將佔全球收入的 41.83%。公共部門對國內半導體製造業的獎勵也推動了邊緣硬體生態系統的擴張。歐洲的成長速度較慢,主要是由於歐盟人工智慧法規增加了文件編制負擔。不過,對低碳環保路線的補貼在一定程度上抵銷了合規成本。

預計亞太地區將呈現最高成長率,到2031年複合年成長率將達到13.59%。中國、印度和日本已投入超過500億美元的國家人工智慧資金,用於國內硬體和大規模語言模式的研發。中國國務院已將供應鏈應用列為優先發展領域,各省紛紛為智慧港口和保稅區物流提供津貼。印度的新創公司正在為中小型製造商提供自主採購工具,而在日本,勞動力老化正在推動物流中心採用機器人技術。

在南美洲,電子商務用戶已超過巴西人口的一半,聖保羅和里約熱內盧對自動配送的需求日益成長。在阿根廷,儘管宏觀經濟波動,人工智慧驅動的貨物匹配仍在推廣,但由於該地區部分地區寬頻存取有限,雲端技術的採用速度緩慢。中東和非洲仍處於起步階段,但阿拉伯聯合大公國和沙烏地阿拉伯正根據其多元化策略,將自主人工智慧融入國家物流走廊。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 融合人工智慧代理的雲端原生供應鏈管理平台迅速普及。

- 人手不足正在加速倉庫自動化領域的投資。

- 更低的感測器和運算成本使得價格更親民的人工智慧硬體成為可能。

- 歐盟人工智慧法案實施後,對可解釋的代理管治框架的需求激增。

- 擴大即時排放資料在碳排放導向路線獎勵的應用

- 自主多智慧體基準資料集的出現,用於標準化採購KPI。

- 市場限制因素

- 與傳統ERP和TMS系統整合成本高昂

- 有關資料隱私和主權的法規增加了合規的負擔。

- 缺乏特定領域的模擬沙箱限制了強化學習智慧體的訓練。

- 由於多主體工作流程的徹底改革,企業變革管理出現疲勞

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體平台

- 人工智慧硬體系統

- 服務(整合和諮詢)

- 透過使用

- 需求預測與規劃

- 最佳化倉庫和履約

- 交通路線規劃與車輛管理

- 採購與尋源自動化

- 最後一公里配送編配

- 其他用途

- 按行業分類

- 零售與電子商務

- 製造業

- 食品/飲料

- 醫療和藥品

- 車

- 其他工業部門

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Amazon.com Inc.

- IBM Corporation

- NVIDIA Corporation

- Blue Yonder Group Inc.

- Manhattan Associates Inc.

- Kinaxis Inc.

- Coupa Software Inc.

- GXO Logistics Inc.

- Locus Robotics Corp.

- Raft Technologies Ltd.

- OneTrack AI Inc.

- AgentChain Inc.

- Beamup AI Inc.

- Glacis Inc.

- Experidium Inc.

- AGENSTRUM Labs BV

- JASCI Software Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the agentic AI market in the supply chain and logistics market is expected to grow from USD 9.86 billion in 2026 to USD 17.84 billion by 2031, expanding at a CAGR of 12.59% over the same period.

This report is Segmented by Component (Software Platforms, and More), Application (Demand Forecasting and Planning, Warehouse and Fulfillment Optimization, and More), Industry Vertical (Retail and E-Commerce, Manufacturing, Food and Beverage, and More), Deployment Model (Cloud-Based, On-Premise, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In The Supply Chain And Logistics Market Trends and Insights

Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents

Cloud hyperscalers now ship multi-agent tools as part of their supply-chain suites, removing integration friction and cutting decision latency from hours to seconds. Amazon Web Services introduced Connect Decisions in May 2025, while Oracle and SAP followed with embedded agents for demand sensing, freight booking, and customs documentation. Mid-market enterprises lacking in-house AI talent can activate these capabilities through subscription tiers, though platform lock-in risk increases once decision histories accumulate inside proprietary clouds.

Labor Shortages Accelerating Warehouse Automation Investments

Low unemployment and high worker turnover push logistics operators to deploy autonomous mobile robots and humanoid systems controlled by multi-agent frameworks. UPS directed USD 120 million toward AI-driven unloading equipment in 2025, and GXO Logistics reported 22% productivity gains after rolling out Dexterity and Agility Robotics pilots across several sites. Real estate design norms are shifting toward robot-friendly layouts, marginalizing legacy facilities that cannot accommodate automated workflows.

High Integration Costs With Legacy ERP and TMS Systems

Most mid-market operators continue to rely on monolithic databases that use batch updates, which limits their ability to adopt advanced technologies such as event-driven streams for multi-agent AI systems. Transitioning to such systems involves high costs, ranging from USD 5 million to USD 20 million per distribution network, and the implementation process can take up to 3 years. Additionally, each agent platform employs its own proprietary ontologies, necessitating the development of custom middleware solutions. This requirement further complicates the adoption process and exacerbates the productivity disparities between large enterprises, which have the resources to manage such transitions effectively, and smaller enterprises, which often struggle to keep pace.

Other drivers and restraints analyzed in the detailed report include:

- Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware

- Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act

- Data Privacy and Sovereignty Regulations Increasing Compliance Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AI-driven software captured 57.81% of the total 2025 revenue in the agentic AI market for supply chain and logistics. The agentic AI in the supply chain and logistics market size for hardware is on course to grow faster at 13.19% as edge inference converges with robotics. Falling chip prices and pre-integrated perception stacks shorten payback periods, bringing autonomous forklifts and vision-guided picking within reach of regional carriers. Services revenue scales as integrators retrofit legacy systems, tune vertical agents, and train supervisors. Software suites continue to benefit from consumption pricing and pre-existing cloud relationships, so they remain the entry point for most newcomers.

Enterprises adopt hardware once they trust the orchestration logic resident in their platforms. Jetson-powered robots and Gaudi-based conveyors are bundled with reference agents that slot into leading cloud SCM suites, shrinking integration effort. Hyperscalers thus monetize both subscription software and certified device ecosystems, while robotics vendors differentiate on specialized gripper design, sensor fusion, and safety certifications.

Demand forecasting led 2025 allocation at 35.83% because most retailers and manufacturers already collect the data needed for time-series and causal models. Last-mile orchestration, however, will log the fastest 13.79% CAGR as dense cities, same-day expectations, and labor shortages collide. FedEx pilots achieve 15% reductions in delivery costs when RFID and route-planning agents coordinate vehicles and sidewalk robots. Warehouse optimization remains a core area, as annual U.S. warehouse turnover exceeded 43% and 400,000 vacancies in 2025.

Procurement agents gain traction as benchmark datasets standardize supplier performance, while carbon-aware fleet routing embeds real-time emissions data to satisfy sustainability mandates. Reverse logistics and cross-docking remain niche but rise gradually with e-commerce returns and circular-economy rules. Each sub-segment taps different data modalities, yet all require multi-agent coordination to eliminate manual bottlenecks.

Geography Analysis

North America accounted for 41.83% of 2025 revenue, thanks to mature cloud infrastructure and early adoption by Amazon, UPS, and FedEx. Public-sector incentives for domestic semiconductor fabrication also support the expansion of the edge hardware ecosystem. Europe grows more slowly because the EU AI Act adds documentation overhead, though carbon-aware routing subsidies partially offset compliance costs.

Asia-Pacific is forecast to post the fastest 13.59% CAGR through 2031 as China, India, and Japan channel more than USD 50 billion in sovereign AI funding into domestic hardware and large language models. China's State Council earmarked supply-chain applications, prompting provincial grants for smart ports and bonded-zone logistics. India's startup scene brings agentic procurement tools to small manufacturers, and Japan's aging workforce propels robot adoption in distribution centers.

South America advances as Brazilian e-commerce surpasses half the population, spurring demand for autonomous delivery in Sao Paulo and Rio de Janeiro. Argentina pursues AI-guided freight matching despite macro volatility, while limited broadband in parts of the region slows cloud uptake. The Middle East and Africa remain early-stage, yet the United Arab Emirates and Saudi Arabia fold agentic AI into national logistics corridors aligned with diversification strategies.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Amazon.com Inc.

- IBM Corporation

- NVIDIA Corporation

- Blue Yonder Group Inc.

- Manhattan Associates Inc.

- Kinaxis Inc.

- Coupa Software Inc.

- GXO Logistics Inc.

- Locus Robotics Corp.

- Raft Technologies Ltd.

- OneTrack AI Inc.

- AgentChain Inc.

- Beamup AI Inc.

- Glacis Inc.

- Experidium Inc.

- AGENSTRUM Labs B.V.

- JASCI Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents

- 4.2.2 Labor Shortages Accelerating Warehouse Automation Investments

- 4.2.3 Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware

- 4.2.4 Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act

- 4.2.5 Rising Usage of Real-Time Emissions Data for Carbon-Aware Routing Incentives

- 4.2.6 Emergence of Autonomous Multi-Agent Benchmark Datasets Standardizing Procurement KPIs

- 4.3 Market Restraints

- 4.3.1 High Integration Costs With Legacy ERP and TMS Systems

- 4.3.2 Data Privacy and Sovereignty Regulations Increasing Compliance Burdens

- 4.3.3 Scarcity of Domain-Specific Simulation Sandboxes Limiting RL Agent Training

- 4.3.4 Enterprise Change-Management Fatigue From Multi-Agent Workflow Overhauls

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 AI-Enabled Hardware Systems

- 5.1.3 Services (Integration and Consulting)

- 5.2 By Application

- 5.2.1 Demand Forecasting and Planning

- 5.2.2 Warehouse and Fulfillment Optimization

- 5.2.3 Transportation Routing and Fleet Management

- 5.2.4 Procurement and Sourcing Automation

- 5.2.5 Last-Mile Delivery Orchestration

- 5.2.6 Other Applications

- 5.3 By Industry Vertical

- 5.3.1 Retail and E-Commerce

- 5.3.2 Manufacturing

- 5.3.3 Food and Beverage

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Automotive

- 5.3.6 Other Industry Verticals

- 5.4 By Deployment Model

- 5.4.1 Cloud-Based

- 5.4.2 On-Premise

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Amazon.com Inc.

- 6.4.5 IBM Corporation

- 6.4.6 NVIDIA Corporation

- 6.4.7 Blue Yonder Group Inc.

- 6.4.8 Manhattan Associates Inc.

- 6.4.9 Kinaxis Inc.

- 6.4.10 Coupa Software Inc.

- 6.4.11 GXO Logistics Inc.

- 6.4.12 Locus Robotics Corp.

- 6.4.13 Raft Technologies Ltd.

- 6.4.14 OneTrack AI Inc.

- 6.4.15 AgentChain Inc.

- 6.4.16 Beamup AI Inc.

- 6.4.17 Glacis Inc.

- 6.4.18 Experidium Inc.

- 6.4.19 AGENSTRUM Labs B.V.

- 6.4.20 JASCI Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

供應鏈分析市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測

供應鏈分析市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測 2026年全球供應鏈分析市場報告

2026年全球供應鏈分析市場報告 2026-2030年全球逆向物流人工智慧市場

2026-2030年全球逆向物流人工智慧市場 供應鏈分析市場:按解決方案類型、部署方式、應用和區域分類

供應鏈分析市場:按解決方案類型、部署方式、應用和區域分類 全球供應鏈和物流領域基於代理的人工智慧市場:市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球供應鏈和物流領域基於代理的人工智慧市場:市場規模、佔有率、趨勢和成長分析報告(2026-2034) 供應鏈分析市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、行業和地區分類,2026-2034 年

供應鏈分析市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、行業和地區分類,2026-2034 年 供應鏈分析市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能全球供應鏈分析市場規模、佔有率、趨勢和成長分析報告(2026-2034)

供應鏈分析市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能全球供應鏈分析市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2025-2029年全球供應鏈最佳化人工智慧市場

2025-2029年全球供應鏈最佳化人工智慧市場 2025-2029年全球供應鏈管理人工智慧市場

2025-2029年全球供應鏈管理人工智慧市場