|

市場調查報告書

商品編碼

2061905

印刷薄膜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Printed Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

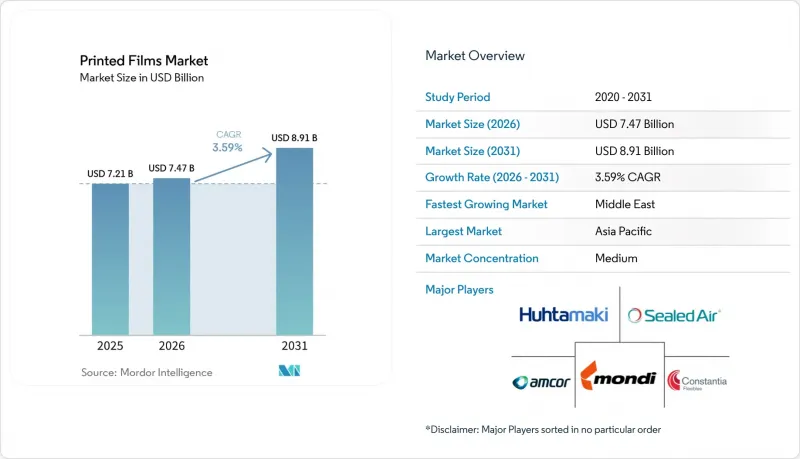

根據 Mordor Intelligence 預測,印刷薄膜市場規模將從 2025 年的 72.1 億美元和 2026 年的 74.7 億美元成長到 2031 年的 89.1 億美元,在預測期(2026 年至 2031 年)內實現 3.59% 的複合年成長率。

本報告按薄膜材料(聚乙烯薄膜、聚丙烯薄膜等)、印刷技術(柔版印刷等)、印刷油墨類型(溶劑型油墨、水性油墨等)、終端用戶行業(食品飲料、個人護理及化妝品等)、薄膜厚度(25毫米及以下等)和地區進行細分。市場預測以美元計價。

全球印刷薄膜市場趨勢與洞察

對永續包裝解決方案的需求日益成長

目前,品牌採購合約中包含循環經濟條款,要求加工商證明其產品具有生物基含量和可回收性。 CARBIOS 的酵素法回收聚乳酸薄膜於 2025 年在美國獲得食品接觸適用性認證,實現了閉合迴路回收,無需降級回收。 Metalvuoto 的生物基 PLA 基材阻隔塗層可將氧氣透過率降低至 5 cc/m²/天以下,從而將農產品的保存期限延長 40%。歐盟將於 2026 年生效的包裝和包裝廢棄物法規將對不合規的軟包裝處以罰款,這將加速基材的再合成,並促進永續印刷薄膜的採用。

電子商務的成長正在推動對保護性印刷膜的需求。

預計到2025年,全球小包裹量將達到1,500億件,每個小包裹通常需要1.8層薄膜包裹。為了應對這項挑戰,加工商開發了高強度聚乙烯郵寄袋,這種郵寄袋能夠承受超過400克/平方米的穿刺測試,同時還能相容於水性柔版印刷油墨。自動化履約中心傾向於使用摩擦係數為0.18的共擠滑動層,這使得它們能夠在分類傳送帶上每小時處理8000個小包裹。能夠在10分鐘內更換圖案的數位印刷機,能夠滿足小批量促銷的需求,實現當日送達,並有助於提升印刷薄膜在物流包裝領域的市場佔有率。

印刷油墨和薄膜原料價格的波動

2025年,中東地區的供應中斷以及中國裂解裝置的關閉導致聚乙烯價格從每噸950美元飆升至每噸1,320美元,嚴重影響了加工商的利潤率。 2026年初,二氧化鈦價格年增18%至每噸3,200美元,推高了白色油墨的成本。雖然像Uflex這樣擁有自有樹脂和顏料生產設施的加工商可以享受200-250個基點的利潤率,但許多獨立公司被迫每季調整價格,這限制了印刷薄膜市場的可預測投資。

細分市場分析

2025年,聚乙烯的銷售額佔比為37.22%,但聚酯預計將以3.61%的複合年成長率成長,超過印刷薄膜市場。這主要得益於醫藥和阻隔性食品應用領域對氧氣透過率低於3 cc/m²/天。東麗的氧化鋁塗層PET在保持透明度的同時,實現了12µm厚度下0.8 cc/m²/天的氧氣滲透率,而低密度聚乙烯若不採用複雜的多層結構則無法達到這一規格。聚丙烯在熱封強度超過2.5 N/15 mm的應用中仍然不可或缺,但鄰苯二甲酸酯的禁用持續下降PVC在食品接觸應用中的佔有率。目前估值處於個位數中段的新興生物聚合物,正在循環經濟試點計畫中發揮試驗平台的作用,並使印刷薄膜市場對永續性的討論保持活躍。

經濟高效的減薄策略正在推動聚酯材料的應用。 Innovia 的奈米多孔雙向拉伸聚丙烯 (BOPP) 無需雷射穿孔即可確保生菜和漿果的透氣性,而 Cosmo First 的防霧聚對苯二甲酸乙二醇酯 (PET) 則可使冷藏包裝袋保持長達三週的透明狀態。由於歐盟監管機構將總遷移量限制在 10 mg/dm² 以內,市場對具有完全可追溯性的食品級樹脂的需求日益成長,這使得特種 PET 成為印刷薄膜行業中現有聚烯的強勁挑戰者。

預計到2025年,柔版印刷將佔銷售額的41.82%,但噴墨印刷3.75%的複合年成長率預示著一個轉折點。數位印刷機無需製版即可完成,即使是500米的單次印刷也能盈利,因此非常適合本地化推廣和增加產品種類。 Windmoeller & Helscher的混合型印刷機整合了用於靜態品牌標識的柔版印刷單元和用於序列化QR碼的噴墨列印頭,從而降低了各種產品系列的千張印刷成本。凹版印刷對於超過百萬公尺的零食和香菸包裝膜仍然至關重要,因為這類包裝膜的滾筒成本必須有效攤銷,且色差必須控制在±1ΔE以內。

持續創新是柔版印刷保持競爭力的關鍵。博斯特的M6生產線可自動對齊印版,減少40%的製版廢料,縮小與數位印刷的廢棄物差距。同時,採用網版印刷和移印技術的印刷薄膜市場仍處於小眾階段,主要集中在導電線和專用防篡改密封件上。在所有印刷平台上,加工商都在權衡資本投資與生產批量柔軟性之間的關係,而這種權衡將影響整個印刷薄膜產業未來的設備採購。

區域分析

亞太地區佔印刷薄膜市場佔有率的34.17%,這主要得益於Cosmo First在印度投產的年產81,200噸的生產線以及Jindal Poly Films投資700千卡(約合8400萬美元)的擴建項目。這些項目鞏固了該地區在雙向拉伸聚丙烯(BOPP)和雙向拉伸聚酯薄膜(BOPET)供應領域的主導地位。在中國,儘管樹脂短缺,但國內對電子商務信封的需求仍以中等個位數的速度成長。同時,日本加工商專注於出口導向型醫藥應用,這些應用需要嚴格的過渡控制。在東南亞國家,對特種複合薄膜的額外投資進一步深化了全部區域的印刷薄膜市場。

受低遷移和可回收薄膜售價上漲的推動,北美和歐洲合計佔據了全球近一半的市場佔有率。安姆科與貝瑞全球合併後,銷售額達到240億美元,凸顯了產業重組的趨勢;而蒙迪12億歐元(約13.4億美元)的資本投資計畫正在擴大單材料立式袋的產量。 2026年生效的歐盟包裝法規正加速向可回收結構轉型,這項要求也是維持成熟經濟體印刷薄膜市場規模的重要因素。

預計中東地區將呈現最高成長率,到2031年複合年成長率將達到3.96%。這主要得益於沙烏地阿拉伯憑藉GulfPack公司年產13.5萬噸雙向拉伸聚丙烯(BOPP)生產線,成為向非洲和南亞轉口的樞紐。南美洲潛力巨大,但外匯波動限制了其資本支出。另一方面,非洲仍然高度依賴進口,南非和埃及作為區域樞紐,滿足了對基礎軟包裝的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對永續包裝解決方案的需求日益成長

- 電子商務的成長正在推動對保護性印刷膜的需求。

- 高解析度數位印刷技術的進步

- 智慧互動包裝的廣泛應用

- 利用軟式電路板的印刷電子產品快速發展

- 嚴格的法規正在促進可生物分解印刷薄膜的使用。

- 市場限制因素

- 印刷油墨和薄膜原料價格的波動

- 關於塑膠廢棄物管理的環境問題

- 先進印刷機的初始投資成本很高

- 影響特種基板的供應鏈中斷

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 透過電影材料

- 聚乙烯(PE)薄膜

- 聚丙烯(PP)薄膜

- 聚酯(PET)薄膜

- 聚氯乙烯(PVC)薄膜

- 其他膠片材料

- 透過印刷技術

- 柔版印刷

- 凹版印刷

- 數位噴墨列印

- 其他印刷技術

- 按印刷油墨類型

- 溶劑型油墨

- 水性油墨

- UV/EB固化油墨

- 其他類型的印刷油墨

- 按最終用戶行業分類

- 食品/飲料

- 個人護理化妝品

- 製藥

- 居家護理和清潔

- 其他終端用戶產業

- 按膠片類型

- 25微米或更小

- 25~50µm

- 50~100µm

- 100微米或以上

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sealed Air Corporation

- Amcor plc

- Huhtamaki Oyj

- Mondi plc

- Constantia Flexibles Group GmbH

- CCL Industries Inc.

- Sonoco Products Company

- Avery Dennison Corporation

- Uflex Limited

- Cosmo First Limited

- Klockner Pentaplast GmbH & Co. KG

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- Taghleef Industries LLC

- POLIFILM GmbH

- FlexFilms Limited

- Jindal Poly Films Limited

- Innovia Films Limited

- Toray Industries, Inc.

- Bemis Company, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the printed films market size is projected to expand from USD 7.21 billion in 2025 and USD 7.47 billion in 2026 to USD 8.91 billion by 2031, registering a CAGR of 3.59% during the forecast period (2026 to 2031).

This report is Segmented by Film Material (Polyethylene Films, Polypropylene Films, and More), Printing Technology (Flexographic Printing, and More), Printing Ink Type (Solvent-Based Inks, Water-Based Inks, and More), End-User Industry (Food and Beverage, Personal Care and Cosmetics, and More), Film Thickness (Up To 25 Mm, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Printed Films Market Trends and Insights

Rising Demand for Sustainable Packaging Solutions

Brand procurement contracts now embed circularity clauses that oblige converters to certify bio-based content and recyclability. CARBIOS secured US food-contact clearance in 2025 for enzymatically recycled polylactic-acid films, enabling closed-loop recovery without downcycling. Metalvuoto's bio-based barrier coating on PLA substrates delivers oxygen transmission below 5 cc/m2/day and extends produce shelf life by 40%. The EU Packaging and Packaging Waste Regulation, effective in 2026, introduces monetary penalties for non-compliant flexibles, prompting rapid substrate reformulation and boosting the adoption of sustainable printed films.

Growth of E-Commerce Boosting Protective Printed Films

Global parcel volumes reached 150 billion in 2025, each typically wrapped in 1.8 layers of film. Converters answered with high-impact polyethylene mailers that withstand >400 g-force puncture tests yet accept water-based flexo inks. Automated fulfillment centers favor coextruded slip layers with a 0.18 coefficient of friction to enable sortation belts to move 8,000 parcels per hour. Digital presses that swap graphics within 10 minutes support small promotional batches, aligning with same-day-delivery demands and sustaining market penetration of printed films in logistics packaging.

Volatility in Raw Material Prices for Printing Inks and Films

Polyethylene swung from USD 950/t to USD 1,320/t in 2025 on Middle East outages and China cracker shutdowns, slashing converter margins. Titanium dioxide climbed 18% YoY to USD 3,200/t in early 2026, inflating white-ink costs. Converters with captive resin or pigment facilities, such as Uflex, enjoy a 200-250 bp margin cushion, yet many independents are forced into quarterly repricing, limiting predictable investment in the printed films market.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in High-Resolution Digital Printing Technologies

- Increasing Adoption of Smart and Interactive Packaging

- Environmental Concerns Regarding Plastic Waste Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene accounted for 37.22% of 2025 revenue, yet polyester is on track to outpace the printed films market at a 3.61% CAGR, buoyed by pharmaceutical and high-barrier food formats that demand oxygen levels below 3 cc/m2/day. Toray's aluminum-oxide-coated PET delivers 0.8 cc/m2/day at 12 µm yet remains transparent, a specification low-density polyethylene cannot match without multilayer complexity. Polypropylene remains essential wherever heat-seal strength above 2.5 N/15 mm is required, while PVC's share continues to erode in food-contact applications due to phthalate bans. Emerging biopolymers currently have only mid-single-digit value but serve as a testbed for circularity pilots and keep the printed films market narrative around sustainability alive.

Cost-effective downgauging strategies are reinforcing polyester uptake. Innovia's nano-porous BOPP allows lettuce and berries to breathe without laser perforation, and Cosmo First's anti-fog PET keeps refrigerated pouches clear for a three-week shelf life. With regulators capping overall migration at 10 mg/dm2 in the EU, demand for food-grade resins with full traceability is increasing, positioning specialty PET grades as credible challengers to incumbent polyolefins within the printed films industry.

Flexo accounted for 41.82% share of 2025 revenue, but inkjet's 3.75% CAGR signals an inflection. Digital presses eliminate plate-mount downtime and run 500-meter jobs profitably, making them perfect for regional promotions and SKU proliferation. Windmoeller and Hoelscher's hybrid unit integrates flexo stations for static branding and inkjet heads for serialized QR codes, reducing cost per thousand impressions across mixed portfolios. Rotogravure remains relevant for snack and tobacco films exceeding 1 million meters, where cylinder costs amortize efficiently, and color variation must remain within +-1 ΔE.

Ongoing innovation keeps flexo competitive. Bobst's M6 line automatically registers plates and curtails setup scrap by 40%, narrowing waste differentials versus digital. Meanwhile, the printed films market for screen and pad technologies remains niche, focusing on conductive tracks and specialized tamper seals. Across print platforms, converters are weighing capital outlay against run-length flexibility, a trade-off that shapes future equipment purchases throughout the printed films industry.

Geography Analysis

Asia-Pacific accounted for 34.17% of the printed films market, anchored by India's 81,200 tpa line from Cosmo First and Jindal Poly Films' INR 700 crore (USD 84 million) expansion, which together reinforce regional leadership in BOPP and BOPET supply. China's domestic demand for e-commerce mailers grew at mid-single-digit rates despite resin shortages, while Japan's converters focused on export-oriented pharmaceutical applications that require stringent migration controls. Southeast Asian nations captured follow-on investment in specialty laminates, adding to the depth of the printed films market across the region.

North America and Europe jointly captured nearly one-half of global value, driven by higher selling prices for low-migration and recyclability-compliant films. Amcor's USD 24 billion revenue base after merging with Berry Global accentuates consolidation, and Mondi's EUR 1.2 billion (USD 1.34 billion) capex program increases mono-material stand-up pouch output. The EU Packaging Regulation, taking effect in 2026, spurs redesigns toward recyclable structures, an imperative that sustains the printed films market size in mature economies.

The Middle East is expected to post the fastest CAGR of 3.96% through 2031, as GulfPack's 135,000 tpa BOPP line positions Saudi Arabia as a re-export platform to Africa and South Asia. South America holds high potential but faces currency volatility that tempers capital spending, while Africa remains largely import-dependent, with South Africa and Egypt hosting regional hubs that serve basic flexible packaging needs.

- Sealed Air Corporation

- Amcor plc

- Huhtamaki Oyj

- Mondi plc

- Constantia Flexibles Group GmbH

- CCL Industries Inc.

- Sonoco Products Company

- Avery Dennison Corporation

- Uflex Limited

- Cosmo First Limited

- Klockner Pentaplast GmbH & Co. KG

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- Taghleef Industries LLC

- POLIFILM GmbH

- FlexFilms Limited

- Jindal Poly Films Limited

- Innovia Films Limited

- Toray Industries, Inc.

- Bemis Company, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Sustainable Packaging Solutions

- 4.2.2 Growth of E-Commerce Boosting Protective Printed Films

- 4.2.3 Advancements in High-Resolution Digital Printing Technologies

- 4.2.4 Increasing Adoption of Smart and Interactive Packaging

- 4.2.5 Rapid Expansion of Printed Electronics on Flexible Substrates

- 4.2.6 Stringent Regulations Driving Biodegradable Printed Film Usage

- 4.3 Market Restraints

- 4.3.1 Volatility in Raw Material Prices for Printing Inks and Films

- 4.3.2 Environmental Concerns Regarding Plastic Waste Management

- 4.3.3 High Initial Capital Investment in Advanced Printing Presses

- 4.3.4 Supply Chain Disruptions Affecting Specialty Substrates

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Material

- 5.1.1 Polyethylene (PE) Films

- 5.1.2 Polypropylene (PP) Films

- 5.1.3 Polyester (PET) Films

- 5.1.4 Polyvinyl Chloride (PVC) Films

- 5.1.5 Other Film Materials

- 5.2 By Printing Technology

- 5.2.1 Flexographic Printing

- 5.2.2 Rotogravure Printing

- 5.2.3 Digital Inkjet Printing

- 5.2.4 Other Printing Technologies

- 5.3 By Printing Ink Type

- 5.3.1 Solvent-based Inks

- 5.3.2 Water-based Inks

- 5.3.3 UV/EB-curable Inks

- 5.3.4 Other Printing Ink Types

- 5.4 By End-user Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Pharmaceuticals

- 5.4.4 Homecare and Cleaning

- 5.4.5 Other End-user Industries

- 5.5 By Film Thickness

- 5.5.1 Up to 25 µm

- 5.5.2 25 - 50 µm

- 5.5.3 50 -100 µm

- 5.5.4 Above 100 µm

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sealed Air Corporation

- 6.4.2 Amcor plc

- 6.4.3 Huhtamaki Oyj

- 6.4.4 Mondi plc

- 6.4.5 Constantia Flexibles Group GmbH

- 6.4.6 CCL Industries Inc.

- 6.4.7 Sonoco Products Company

- 6.4.8 Avery Dennison Corporation

- 6.4.9 Uflex Limited

- 6.4.10 Cosmo First Limited

- 6.4.11 Klockner Pentaplast GmbH & Co. KG

- 6.4.12 Toppan Inc.

- 6.4.13 Dai Nippon Printing Co., Ltd.

- 6.4.14 Taghleef Industries LLC

- 6.4.15 POLIFILM GmbH

- 6.4.16 FlexFilms Limited

- 6.4.17 Jindal Poly Films Limited

- 6.4.18 Innovia Films Limited

- 6.4.19 Toray Industries, Inc.

- 6.4.20 Bemis Company, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

阻隔包裝市場預測至2034年-按產品類型、材料、阻隔類型、技術、應用、最終用戶和地區分類的全球分析

阻隔包裝市場預測至2034年-按產品類型、材料、阻隔類型、技術、應用、最終用戶和地區分類的全球分析 全球阻隔膜市場:市場規模、佔有率、成長和行業分析:按材料類型、產品類型、最終用途和地區預測(至2034年)

全球阻隔膜市場:市場規模、佔有率、成長和行業分析:按材料類型、產品類型、最終用途和地區預測(至2034年) 阻隔膜市場:按類型、材料、包裝、最終用戶和分銷管道分類-2026-2032年全球市場預測增亮膜市場:2026-2032 年全球市場以產品類型、材料、設備類型、通路和厚度預測。可再生阻隔膜市場預測至2034年-全球材料類型、薄膜結構、回收製程、阻隔類型、應用、最終用戶及地區分析

阻隔膜市場:按類型、材料、包裝、最終用戶和分銷管道分類-2026-2032年全球市場預測增亮膜市場:2026-2032 年全球市場以產品類型、材料、設備類型、通路和厚度預測。可再生阻隔膜市場預測至2034年-全球材料類型、薄膜結構、回收製程、阻隔類型、應用、最終用戶及地區分析 全球阻隔膜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球醫用和電子包裝用SiOx阻隔膜市場:按塗層技術、基材、薄膜厚度和應用分類的預測(2026-2032年)食品飲料包裝用SiOx阻隔膜:按包裝類型、技術、阻隔等級、應用和最終用戶分類的全球預測(2026-2032年)

全球阻隔膜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球醫用和電子包裝用SiOx阻隔膜市場:按塗層技術、基材、薄膜厚度和應用分類的預測(2026-2032年)食品飲料包裝用SiOx阻隔膜:按包裝類型、技術、阻隔等級、應用和最終用戶分類的全球預測(2026-2032年) 食品包裝用高阻隔薄膜市場:依材料種類(PE、BOPP/BOPET、CPP、EVOH、尼龍)、技術、應用(肉類和魚類、乳製品、休閒食品、糖果、烘焙產品、寵物食品)、最終用戶和地區劃分-全球預測至2036年

食品包裝用高阻隔薄膜市場:依材料種類(PE、BOPP/BOPET、CPP、EVOH、尼龍)、技術、應用(肉類和魚類、乳製品、休閒食品、糖果、烘焙產品、寵物食品)、最終用戶和地區劃分-全球預測至2036年 日本阻隔膜市場規模、佔有率、趨勢和預測:按類型、材料、應用和地區分類,2026-2034年

日本阻隔膜市場規模、佔有率、趨勢和預測:按類型、材料、應用和地區分類,2026-2034年