|

市場調查報告書

商品編碼

2061900

覆銅層壓板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Copper Clad Laminate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

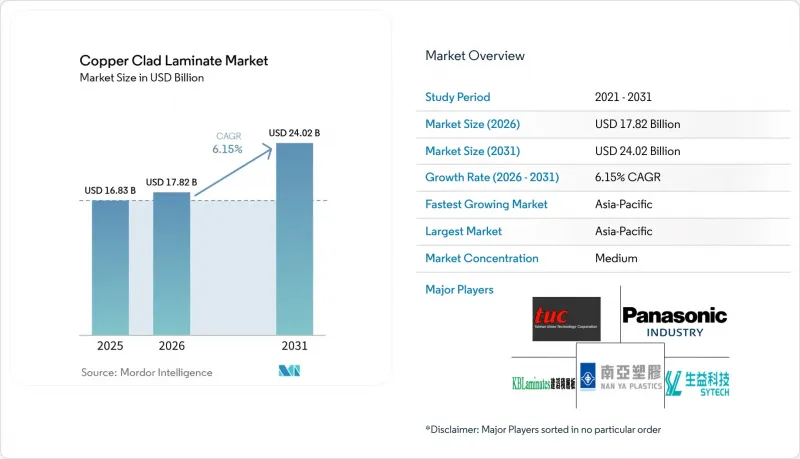

據 Mordor Intelligence 稱,2025 年覆銅層壓板市場價值為 168.3 億美元,預計到 2031 年將達到 240.2 億美元,而 2026 年為 178.2 億美元,預測期(2026-2031 年)的複合年成長率為 6.15%。

本報告按樹脂類型(環氧樹脂、酚醛樹脂、聚醯亞胺樹脂等)、形態(剛性和軟性)、增強材料(玻璃纖維布、紙基等)、應用領域(消費性電子、通訊系統等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球覆銅層壓板市場趨勢及洞察

電子產品和印刷電路板的強勁需求正在推動根本性成長。

印度電子產品產值預計將從2015會計年度的19兆盧比(296億美元)成長至2024會計年度的95.2兆盧比(1,130億美元),這將提振國內PCB需求,並推動覆銅板市場的發展。根據“電子元件製造計劃”,2026年1月獲批的22個項目將為國內覆銅板和PCB工廠帶來4186.3兆印度盧比(44.38億美元)的投資。儘管低成本的FR-4材料面臨價格壓力,但採用多層HDI(高密度基板)基板的供應商卻獲得了更高的利潤率。

5G 網路基礎設施部署的加速推動了高頻 CCL 的採用。

5G基地台的建設需要介電損耗小於0.005的層壓基板,頻寬為24–77 GHz,RO3003和RO4830 Plus系列正好滿足此細分市場需求。台灣聯科科技在無鹵素和碳中和材料方面的研發,清楚地表明通訊業者對性能和永續性都有雙重要求。早期6G研究已經開發出工作在亞太赫茲頻段的聚醯亞胺薄膜原型,但其實用化水準仍處於技術成熟度3–6級。

銅價和石油基樹脂價格的波動給利潤率帶來了壓力。

2024年,倫敦金屬交易所(LME)的銅價一度飆升至近13,842美元/噸,之後趨於穩定。同時,受油價波動和亞太地區供應鏈中斷的影響,環氧樹脂原料成本在2025年之前以每年7%至10%的速度上漲。儘管Resonaq Holdings已於2026年3月起實施了30%的漲價,Kingboard Laminates和Nanya Plastics也在2025年進行了多次價格調整,但這些措施比原物料成本的飆升滯後了3至6個月,在此期間擠壓了毛利率。那些未實現銅箔和樹脂生產垂直整合的中小型複合板(CCL)製造商面臨嚴重的脆弱性。它們缺乏規模優勢來談判固定價格契約,也無法在不將成本轉嫁給下游的情況下自行承擔不斷上漲的成本,這可能導致市場佔有率被能夠提供價格穩定的大型競爭對手蠶食。

細分市場分析

到2025年,環氧樹脂將佔總產量的65.66%,主要用於消費性電子產品的通用電路基板。然而,由於航空航太和軟性電子產品產業對耐高溫(高達250 度C)性能的需求,聚醯亞胺預計將以7.12%的複合年成長率快速成長至2031年。特種氟聚合物雖然規模較小,但由於滿足毫米波和雷達應用的要求,其價格是環氧樹脂的3到5倍。像盛益這樣的供應商正在整合其聚四氟乙烯(PTFE)生產能力,以確保獲得帶有嵌入式電容器的伺服器訂單,這凸顯了樹脂的選擇如何決定利潤率。

目前,高效能混合物將環氧樹脂和聚偏苯二甲酸乙二醇酯(PPO)結合,以減少熱膨脹係數(CTE)的差異,並用於多層伺服器基板。隨著單面應用的減少,酚醛樹脂和紙基產品也隨之減少。諸如Arlon的85N和Panasonic的HIPER系列等複合樹脂的推出,已在航太和電動汽車逆變器等細分市場佔據一席之地,幫助供應商在原料價格波動時保持定價權。

儘管2025年硬質產品銷售額佔比仍高達78.21%,但受折疊式智慧型手機和穿戴式裝置普及的推動,軟性層壓板市場預計到2031年將以7.34%的複合年成長率成長。斗山公司的軟性複合層壓板(FCCL)展現出超過百萬次折疊的耐久性,而泰福仕在泰國投資3500萬美元的工廠將滿足汽車內裝和顯示模組的需求。

剛柔混合材料產品正拓展至醫療設備和機器人領域,其價格溢價高達2-3倍。掌握超薄銅箔加工和黏合劑層壓技術的供應商能夠確保產品在設計採用後的穩定性。同時,主要的剛性基板製造商透過自主生產玻璃纖維和銅箔來維持規模經濟,並透過對通用FR-4基板採取激進的定價策略來捍衛其市場佔有率。

區域分析

預計到2025年,亞太地區將佔全球銷售額的35.38%,並在2031年之前以7.78%的複合年成長率持續成長。僅在泰國和印度,政府就已宣布了獎勵性投資計劃,這將推動當地對層壓板的需求。儘管中國仍是最大的消費市場,但地緣政治格局的變化正促使台灣和中國當地的企業進軍東南亞市場,預計到2026年,泰國在全球整體印刷電路板(PCB)市場的佔有率將超過5%。

北美和歐洲合計約佔全球銷售額的一半,主要得益於航太、國防和超大規模資料中心的需求。 AGC Multi Material America 透過 Tritek 拓展了其分銷網路,以增強其在美國的供應穩定性。歐盟的碳政策提高了合規門檻,這使得能夠投資於無鹵化和可再生能源轉型的大型成熟企業更具優勢。

截至2025年,南美洲、中東和非洲的市佔率將最低。儘管巴西汽車市場的復甦以及海灣國家電信項目的開展為尚未開發的地區提供了成長機遇,但基礎設施的不平衡和上游原料的短缺限制了短期市場滲透。隨著區域製造業生態系統的成熟,那些提供本地技術支援的領先有望贏得客戶的忠誠。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子產品和印刷電路板需求強勁

- 加速5G網路基礎架構的部署

- 汽車電氣化和高級駕駛輔助系統的普及

- AI 伺服器板需要超薄嵌入式電容 CCL。

- GaN/SiC功率模組的興起需要高導熱係數的CCL

- 市場限制因素

- 銅和石油基樹脂的價格波動

- 加強全球環境、健康與安全以及碳足跡法規

- 新一代印刷機和等離子生產線的資本投資成本不斷上升。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧樹脂

- 酚醛樹脂

- 聚醯亞胺

- 聚酯纖維

- 氟樹脂/聚四氟乙烯

- 聚亞苯醚(PPE)

- 聚亞苯醚(PPO)

- 其他

- 按形狀

- 死板的

- 靈活的

- 按類型分類的加固材料

- 玻璃纖維布

- 紙張類型

- 複合材料/芳香聚醯胺/液晶聚合物

- 其他材料

- 透過使用

- 通訊系統

- 家用電子產品

- 汽車電子產品和電動車動力傳動系統

- 工業和電力電子

- 資料中心和人工智慧伺服器

- 航太/國防

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- AGC Inc.

- Chang Chun Group

- Doosan Corporation Electro-Materials

- Elite Material Co., Ltd.

- Goldenmax International Technology Ltd.

- Grace Electron

- Guangdong Chaohua Technology Co., Ltd.

- Isola Group

- ITEQ CORPORATION

- Kingboard Laminates Holdings Ltd.

- NAN YA PLASTICS CORPORATION

- Panasonic Industry Co., Ltd.

- Resonac Holdings Corporation

- Rogers Corporation

- Shandong Jinbao Electronics Co., Ltd.

- SHENGYI TECHNOLOGY CO., LTD.

- Sumitomo Bakelite Co., Ltd.

- Sytech Technology Co., Ltd.

- TACONIC

- Taiwan Union Technology Corporation

- Ventec International Group

- ZHEJIANG WAZAM NEW MATERIALS CO., LTD.

第7章 市場機會與未來展望

According to Mordor Intelligence, the copper clad laminate market size was valued at USD 16.83 billion in 2025 and is estimated to grow from USD 17.82 billion in 2026 to reach USD 24.02 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Epoxy, Phenolic, Polyimide, and More), Form Type (Rigid and Flexible), Reinforcement Material (Fiberglass Fabric, Paper-Based, and More), Application (Consumer Electronics, Communication Systems, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Copper Clad Laminate Market Trends and Insights

Robust Demand for Electronics and PCB Drives Baseline Growth

India's electronics output climbed from INR 1.90 lakh crore (USD 29.6 billion) in FY 2015 to INR 9.52 lakh crore (USD 113 billion) in FY 2024, raising local PCB requirements and boosting the Copper Clad Laminate market. Twenty-two projects cleared under the Electronics Component Manufacturing Scheme in January 2026 unlocked INR 41,863 crore (USD 4.438 billion) of investment aimed at domestic laminate and PCB (Printed Circuit Board) plants. Suppliers integrating into high-layer HDI (High-Density Interconnect) boards capture stronger margins even as low-cost FR-4 faces price pressure.

Acceleration of 5G Network Infrastructure Rollout Fuels High-Frequency CCL Adoption

5G base-station builds require laminates with dielectric loss below 0.005 across 24-77 GHz, a niche addressed by RO3003 and RO4830 Plus families. Taiwan Union Technology's R&D for halogen-free, carbon-neutral materials underscores how carriers seek both performance and sustainability. Early 6G research is already prompting prototypes of polyimide films operating in the sub-THz band, though readiness sits at TRL 3-6.

Copper and Petroleum-Based Resin Price Volatility Compresses Margins

Copper prices on the London Metal Exchange peaked near USD 13,842 per tonne in 2024 before moderating, and epoxy resin feedstock costs rose 7-10% annually through 2025, driven by petroleum price swings and supply-chain disruptions in Asia-Pacific. Resonac Holdings implemented a 30% price increase effective March 2026, and Kingboard Laminates and Nan Ya Plastics executed multiple price adjustments in 2025, yet these actions lag raw-material cost spikes by 3-6 months, compressing gross margins during the interim. Smaller CCL manufacturers without vertical integration into copper foil or resin production face acute vulnerability: they lack the scale to negotiate fixed-price contracts and cannot absorb cost inflation without passing it downstream, which risks losing share to larger competitors who can offer price stability.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Electrification and ADAS Penetration Reshape Material Specifications

- AI-Server Boards Demand Ultra-Thin Embedded-Capacitance CCL

- Stricter Global EHS and Carbon-Footprint Regulations Elevate Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy held 65.66% of 2025 volume, anchoring commodity boards for consumer devices, yet polyimide captured faster growth with a 7.12% CAGR through 2031 as aerospace and flexible electronics seek durability to 250°C. Specialty fluoropolymer grades, though small, earn 3-5 times epoxy prices by meeting mmWave and radar requirements. Suppliers such as Shengyi integrate PTFE capability to secure embedded-capacitance server wins, highlighting how resin choice determines margin bands.

High-performance blends now pair epoxy with PPO to reduce CTE mismatch, supporting multi-layer server boards. Phenolic and paper-based products are declining as single-sided applications fade. Composite resin launches, including Arlon's 85N and Panasonic's HIPER series, capture aerospace and EV inverter niches and help suppliers defend pricing power during raw-material swings.

Rigid products contributed 78.21% of 2025 revenue, yet flexible laminates are pacing at a 7.34% CAGR to 2031, owing to foldable phones and wearables. Doosan's FCCL demonstrates durability over 1 million folds, while Taiflex's USD 35 million Thailand plant will support automotive interiors and display modules.

Rigid-flex hybrids are spreading into medical devices and robotics, commanding a 2-3 times cost premium. Suppliers that master ultra-thin copper handling and adhesive-less lamination secure design-win stickiness. Meanwhile, large rigid producers defend scale economies through in-house glass fabric and copper foil, allowing aggressive pricing in commodity FR-4 to protect share.

Geography Analysis

Asia-Pacific generated 35.38% of 2025 revenue and is projected to rise at a 7.78% CAGR through 2031. Thailand and India alone have announced incentive-led investments, catalyzing local laminate demand. China maintains the largest consumption base, yet geopolitical shifts are steering Taiwanese and mainland firms to Southeast Asia, with Thailand's PCB share expected to top 5% globally in 2026.

North America and Europe together accounted for about half of global revenue, owing to aerospace, defense, and hyperscale data centers. AGC Multi Material America expanded distribution through Tritek to fortify UnitedStates supply security. EU carbon policies elevate compliance hurdles, favoring large incumbents that can fund halogen-free and renewable power upgrades.

South America and the Middle East & Africa held the lowest share in 2025. Brazil's vehicle rebound and Gulf-state telecom projects offer white-space growth, but infrastructure gaps and limited upstream feedstocks temper near-term penetration. Early movers that provide local technical support may capture loyalty as regional manufacturing ecosystems mature.

- AGC Inc.

- Chang Chun Group

- Doosan Corporation Electro-Materials

- Elite Material Co., Ltd.

- Goldenmax International Technology Ltd.

- Grace Electron

- Guangdong Chaohua Technology Co., Ltd.

- Isola Group

- ITEQ CORPORATION

- Kingboard Laminates Holdings Ltd.

- NAN YA PLASTICS CORPORATION

- Panasonic Industry Co., Ltd.

- Resonac Holdings Corporation

- Rogers Corporation

- Shandong Jinbao Electronics Co., Ltd.

- SHENGYI TECHNOLOGY CO., LTD.

- Sumitomo Bakelite Co., Ltd.

- Sytech Technology Co., Ltd.

- TACONIC

- Taiwan Union Technology Corporation

- Ventec International Group

- ZHEJIANG WAZAM NEW MATERIALS CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust demand for electronics and PCB

- 4.2.2 Acceleration of 5G network infrastructure rollout

- 4.2.3 Automotive electrification and ADAS penetration

- 4.2.4 AI-server boards need ultra-thin embedded-capacitance CCL

- 4.2.5 Rise of GaN/SiC power modules needing high-thermal CCL

- 4.3 Market Restraints

- 4.3.1 Copper and petroleum-based resin price volatility

- 4.3.2 Stricter global EHS and carbon-footprint regulations

- 4.3.3 CAPEX inflation for next-gen press and plasma lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Phenolic

- 5.1.3 Polyimide

- 5.1.4 Polyester

- 5.1.5 Fluoropolymer / PTFE

- 5.1.6 Polyphenylene Ether (PPE)

- 5.1.7 Polyphenylene Oxide (PPO)

- 5.1.8 Others

- 5.2 By Form Type

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 By Reinforcement Material

- 5.3.1 Fiberglass Fabric

- 5.3.2 Paper-based

- 5.3.3 Composite / Aramid / LCP

- 5.3.4 Other Materials

- 5.4 By Application

- 5.4.1 Communication Systems

- 5.4.2 Consumer Electronics

- 5.4.3 Automotive Electronics and EV Powertrain

- 5.4.4 Industrial and Power Electronics

- 5.4.5 Data-centre and AI Servers

- 5.4.6 Aerospace and Defense

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Chang Chun Group

- 6.4.3 Doosan Corporation Electro-Materials

- 6.4.4 Elite Material Co., Ltd.

- 6.4.5 Goldenmax International Technology Ltd.

- 6.4.6 Grace Electron

- 6.4.7 Guangdong Chaohua Technology Co., Ltd.

- 6.4.8 Isola Group

- 6.4.9 ITEQ CORPORATION

- 6.4.10 Kingboard Laminates Holdings Ltd.

- 6.4.11 NAN YA PLASTICS CORPORATION

- 6.4.12 Panasonic Industry Co., Ltd.

- 6.4.13 Resonac Holdings Corporation

- 6.4.14 Rogers Corporation

- 6.4.15 Shandong Jinbao Electronics Co., Ltd.

- 6.4.16 SHENGYI TECHNOLOGY CO., LTD.

- 6.4.17 Sumitomo Bakelite Co., Ltd.

- 6.4.18 Sytech Technology Co., Ltd.

- 6.4.19 TACONIC

- 6.4.20 Taiwan Union Technology Corporation

- 6.4.21 Ventec International Group

- 6.4.22 ZHEJIANG WAZAM NEW MATERIALS CO., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 High-frequency (mmWave), 5G and Automotive Growth Nodes

- 7.3 Capacity Expansion in Emerging Manufacturing Hubs

覆銅層壓板(CCL)市場-全球預測,2026-2032年

覆銅層壓板(CCL)市場-全球預測,2026-2032年 2026 年至 2035 年高頻高速覆銅板市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年高頻高速覆銅板市場的商業機會、成長要素、產業趨勢分析與預測。 全球聚四氟乙烯覆銅層壓板市場:按類型、性能等級、增強材料、應用和地區分類-預測至2031年

全球聚四氟乙烯覆銅層壓板市場:按類型、性能等級、增強材料、應用和地區分類-預測至2031年 銅包層壓板市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測。

銅包層壓板市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測。 2026年全球高頻高速覆銅板(CCL)市場報告

2026年全球高頻高速覆銅板(CCL)市場報告 伺服器覆銅層壓板市場報告:趨勢、預測和競爭分析(至2035年)

伺服器覆銅層壓板市場報告:趨勢、預測和競爭分析(至2035年) 人工智慧伺服器用覆銅層壓板 (CCL) – 2026-2032 年全球市場佔有率排名、總銷售額和需求預測。全球覆銅層壓板市場規模、佔有率、趨勢及成長分析報告(2026-2034)2026年全球覆銅板市場報告2026年金屬基覆銅層壓板全球市場報告

人工智慧伺服器用覆銅層壓板 (CCL) – 2026-2032 年全球市場佔有率排名、總銷售額和需求預測。全球覆銅層壓板市場規模、佔有率、趨勢及成長分析報告(2026-2034)2026年全球覆銅板市場報告2026年金屬基覆銅層壓板全球市場報告