|

市場調查報告書

商品編碼

2061887

直接熱敏標籤:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Direct Thermal Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

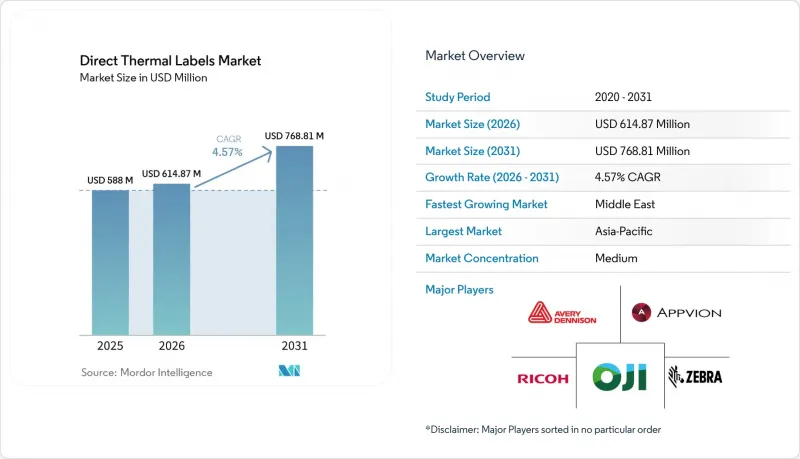

據 Mordor Intelligence 稱,2025 年直接熱轉印標籤市值為 5.88 億美元,預計到 2031 年將達到 7.6881 億美元,而 2026 年為 6.1487 億美元,在預測期(2026-2031 年)內複合年成長率為 4.57%。

本報告按材料類型(紙本和合成材料)、形式(捲筒、折疊式、無底紙)、終端用戶行業(物流運輸、零售和電子商務、食品飲料、醫療保健和製藥、製造和工業以及其他終端用戶行業)和地區進行細分。市場預測以價值(美元)表示。

全球直接熱轉印標籤市場趨勢與洞察

電子商務履約的擴張正在加速按需標籤印刷的發展。

亞太地區的小包裹量預計將從2026年的512.4億美元成長到2035年的1,960.9億美元,複合年成長率(CAGR)為16.08%。這履約中心從批量列印轉向即時列印。直接熱感列印無需更換色帶,減少了停機時間,這在需要當日送達、印表機停機時間不可接受的情況下至關重要。沃爾瑪的試驗計畫採用混合式直接熱敏和RFID標籤,實現了99%的庫存準確率,並展示了條碼和標籤整合帶來的生產力提升。目前,承運商標籤API已整合結帳時的條碼產生功能,使經銷商能夠在幾毫秒內列印正確的運輸標籤。由於熱轉印色帶難以實現這些軟體主導的工作流程,小包裹的成長直接推動了新型直接熱敏印表機的普及,在最繁忙的地點,印表機的更換週期已從18個月縮短至不到12個月。

嚴格的藥品溯源法規

沙烏地阿拉伯食品藥物管理局於2025年發布的一份範本強制要求使用GS1全球貿易項目代碼(GTIN)、阿拉伯語和英語雙語文本以及DataMatrix碼,並要求契約製造以每分鐘超過300個單位的速度進行可變數據列印。阿拉伯聯合大公國衛生署規定最小字元高度為1.6毫米,並包含12個基本資料元素,約旦也制定了類似的雙語標籤規定。熱感式印表機無需預先送入色帶即可立即開始列印,每次批次切換可節省15-20秒。美國FDA分階段過渡到國家藥品代碼(NDC)的計畫將持續到2033年,因此轉換商需要在過渡期間同時支援10位和12位代碼。由於色帶處理限制了處理能力,製藥業正轉向將設備升級為直接熱敏系統,以實現單元級序列化,預計這一趨勢將支撐設備和耗材的銷售量直至2020年代末。

熱敏紙基材價格波動

科勒、多姆特和韓索爾於2026年3月將全球熱感紙價格上調10%,理由是運輸中斷、石化產品價格飆升以及OBD-2染料顯影劑的結構性短缺。全球對OBD-2的需求量約為6000-7000噸,而產能仍低於3000噸,現貨價格超過每噸100萬元人民幣(約14萬美元)。到2025年底,紙漿成本上漲了18%,歐洲造紙廠的能源成本飆升了25-30%,擠壓了加工商的利潤空間。一些中型供應商未能與零售商重新談判固定價格契約,已退出市場。由於亞洲新的塗佈紙生產線要到2027年下半年才能運作,造紙商至少在未來兩年內仍將面臨原料成本波動的問題。

細分市場分析

2025年,紙質面材佔據了熱敏標籤市場61.23%的佔有率。這主要歸功於其價格低廉且與傳統印表機相容。儘管合成面材價格更高,但由於低溫運輸物流和序列化對耐用性的需求不斷成長,預計到2031年,其市場佔有率將以每年4.69%的速度成長。零售商仍在短程小包裹上使用紙質標籤,因為這類標籤的使用壽命僅為30天。但一家歐洲冷凍食品經銷商報告稱,改用合成標籤後,更換成本降低了40%。隨著聚烯薄膜價格差距的縮小,與合成材料相關的熱敏標籤市場規模正在擴大。然而,由於合成材料的彈性模量較高,因此在需要精確壓板壓力且無法調整張力的印表機中,仍使用紙捲。

在製藥、生物技術和戶外物流領域,耐用性而非價格如今已成為基材選擇的決定性因素。合成材料能夠承受-40°C至+80°C的溫度變化,具有極強的防潮性能,並解決了紙質標籤在冷庫和潮濕倉庫中常見的翹曲和剝落問題。艾利丹尼森的RFID套模合成標籤已證明,可重複使用的托特包能夠經受多次洗滌而不剝落。然而,在加工商收回用於處理更厚材料的新型分切和檢測生產線的投資之前,合成材料市場仍處於小眾階段。

區域分析

亞太地區預計在2025年佔全球銷售額的33.15%。這主要得益於電子商務包裝市場的蓬勃發展,該市場預計將從2026年的512.4億美元飆升至2035年的1,960.9億美元。中國仍然是最大的買家,而印度則是成長最快的市場。此外,東南亞的食品平台正在轉向使用合成材料以應對熱帶高溫。 GS1 Sunrise 2027標準和零售商的RFID先導計畫正在推動對直接熱敏列印和編碼技術的需求,尤其是在需要同時進行列印和編碼的履約中心。

預計中東將成為成長最快的次區域,2026年至2031年的複合年成長率將達到5.11%。由於沙烏地阿拉伯的雙語GS1條碼法規、阿拉伯聯合大公國1.6毫米的字體大小要求以及約旦的序列化計劃,對藥品標籤的需求正在不斷成長。 「2030願景」對醫療保健領域的投資以及新建的製藥製造地需要能夠以每分鐘超過300張的速度進行序列化的印表機。儘管紅海運輸中斷和原料價格飆升導致科勒等公司在2026年3月提高了紙張價格,但加工商預計,隨著亞洲新的塗佈生產線在2027年下半年投入運作,這種情況將會緩解。

在歐洲和北美,趨勢呈現出相互矛盾的態勢。沃爾瑪計畫在2026年底前,以數位價格標籤取代美國門市的紙貨架標籤,從而減少門市紙張的使用量。同時,沃爾瑪也在其物流中心強制推廣使用RFID技術,該技術仰賴混合型直接熱轉印標籤。歐盟將於2026年8月生效的法規建議採用無底紙標籤技術,而UPM公司於2026年5月推出的「ProCycle」可水洗黏合劑正是為了滿足這項要求。在南美和非洲,由於缺乏統一的法規以及對價格的敏感性,進展較為緩慢,因此熱轉印標籤技術在長途運輸方面仍然具有吸引力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務履約的擴張正在加速按需標籤印刷的發展。

- 嚴格的藥品溯源法規

- 經濟高效的無色帶列印降低了整體擁有成本。

- 零售業無襯墊產品永續性標準的興起

- 智慧物流中QR碼和RFID功能的整合

- 低溫運輸食品宅配服務的擴展

- 市場限制因素

- 熱敏紙價格波動

- 惡劣環境下影像衰減和穩定性的局限性

- 數位標籤和RFID標籤的廣泛應用

- 對無襯裡加工設備的資本投資

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 紙面材料

- 合成面材

- 按外形規格

- 卷

- 折疊

- 無襯墊

- 按最終用戶行業分類

- 物流/運輸

- 零售與電子商務

- 食品/飲料

- 醫療和藥品

- 製造業和工業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- Appvion Operations Inc.

- Zebra Technologies Corporation

- Oji Holdings Corporation

- Ricoh Company Ltd.

- CCL Industries Inc.

- Honeywell International Inc.

- 3M Company

- SATO Holdings Corporation

- UPM-Kymmene Oyj(UPM Raflatac)

- Brady Corporation

- Brother Industries, Ltd.

- Seiko Epson Corporation

- Fuji Seal International, Inc.

- Multi-Color Corporation

- WS Packaging Group, Inc.

- Resource Label Group, LLC

- LINTEC Corporation

- DNP Imagingcomm Co., Ltd.

- TSC Auto ID Technology Co., Ltd.

- BIXOLON Co., Ltd.

- Label Technology, Inc.

- RR Donnelley & Sons Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the direct thermal labels market was valued at USD 588 million in 2025 and is estimated to grow from USD 614.87 million in 2026 to reach USD 768.81 million by 2031, growing at a CAGR of 4.57% during the forecast period (2026-2031).

This report is Segmented by Material Type (Paper Facestock, and Synthetic Facestock), Form Factor (Rolls, Fan-Fold, and Linerless), End-User Industry (Logistics and Transportation, Retail and E-Commerce, Food and Beverage, Healthcare and Pharmaceuticals, Manufacturing and Industrial, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Direct Thermal Labels Market Trends and Insights

E-Commerce Fulfilment Growth Accelerates On-Demand Label Printing

Parcel volume in Asia-Pacific is projected to climb from USD 51.24 billion in 2026 to USD 196.09 billion by 2035, a 16.08% compound annual growth rate that forces fulfillment centers to switch from bulk batches to real-time printing. Direct thermal eliminates ribbon changes and reduces downtime, which is critical when same-day delivery commitments leave no tolerance for printer stoppages. Walmart's use of hybrid direct thermal and RFID labels achieved 99% inventory accuracy in a pilot program, validating the productivity upside of integrated barcoding and tagging. Carrier-label APIs now embed barcode generation at checkout, letting merchants print the correct service label in milliseconds. These software-driven workflows are unlikely with thermal-transfer ribbons, so parcel growth is directly translating into new direct thermal printer installations, trimming replacement cycles from 18 months to under 12 months in the busiest nodes.

Stringent Pharmaceutical Traceability Mandates

The Saudi Food and Drug Authority template, issued in 2025, requires GS1 GTINs, bilingual Arabic-English text, and DataMatrix codes, pushing contract manufacturers to adopt variable-data printing at rates above 300 units per minute. The UAE Ministry of Health requires a minimum text height of 1.6 mm and 12 mandatory data elements, while Jordan enforces similar bilingual rules. Direct thermal printers start instantly without ribbon pre-feed, saving 15-20 seconds on every batch changeover. The United States FDA's phased National Drug Code migration extends through 2033, so converters must handle both 10-digit and 12-digit codes during transition. Because ribbon handling limits throughput, pharmaceutical lines are retooling around direct thermal for unit-level serialization, a trend likely to support equipment sales and consumables volume through the end of the decade.

Volatility in Thermal-Paper Base Prices

Koehler, Domtar, and Hansol raised global thermal paper prices by 10% in March 2026, blaming shipping disruptions, petrochemical inflation, and a structural shortage of OBD-2 leuco-dye developer. Global demand for OBD-2 stands near 6,000-7,000 tons while capacity remains below 3,000 tons, sending spot prices above RMB 1,000,000 (USD 0.14 million) per ton. Pulp costs climbed 18% in late 2025, and European mills faced 25-30% higher energy bills, squeezing converter margins. Some mid-tier suppliers exited the market after failing to renegotiate fixed-price contracts with retailers. New Asian coating lines will not arrive until late 2027, so converters must cope with unstable input costs for at least two more years.

Other drivers and restraints analyzed in the detailed report include:

- Integration of QR and RFID Features for Smart Logistics

- Cost-Efficient No-Ribbon Printing Lowers Total Ownership

- Fading and Image-Stability Limitations in Harsh Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper facestock accounted for 61.23% of the direct thermal label market share in 2025, driven by its low price and compatibility with legacy printers. Synthetic facestock, although more expensive, is forecast to grow at 4.69% through 2031 as cold-chain logistics and serialization raise durability requirements. Retailers continue to use paper for short-haul parcels, where labels last only 30 days, but frozen-food distributors in Europe reported a 40% reduction in replacement costs after shifting to synthetic labels. The direct thermal labels market size tied to synthetics is enlarging as polyolefin films narrow the price gap. However, synthetic's higher modulus demands precise platen pressure, so printers unable to adjust tension still default to paper rolls.

Durability rather than price now dictates substrate choice in pharmaceuticals, biotech, and outdoor logistics. Synthetic stock resists -40 °C to +80 °C swings and defies moisture, solving the curl and peel seen with paper in cold rooms or humid depots. Avery Dennison's RFID-enabled in-mold synthetic labels demonstrate that reusable totes can withstand multiple wash cycles without delamination. Even so, synthetic media remains niche until converters amortize the new slitting and inspection lines required to handle thicker calipers.

Geography Analysis

Asia-Pacific accounted for 33.15% of 2025 global revenue, supported by e-commerce packaging, which is projected to jump from USD 51.24 billion in 2026 to USD 196.09 billion by 2035. China remains the largest buyer, India the fastest grower, and Southeast Asian grocery platforms are shifting to synthetic stock to withstand tropical heat. GS1 Sunrise 2027 and retailers' RFID pilots are driving demand for direct thermal printing and encoding in fulfillment hubs that require simultaneous printing and encoding capability.

The Middle East is forecast to be the fastest-growing sub-region, with a 5.11% CAGR over 2026-2031. Saudi Arabia's bilingual GS1 barcode rule, the UAE's 1.6 mm text requirement, and Jordan's serialization program are expanding pharmaceutical label volume. Vision 2030 healthcare investment and new drug-manufacturing sites require serialization-ready printers at line speeds exceeding 300 units per minute. Shipping disruptions in the Red Sea, combined with raw-material inflation, explain why Koehler and peers raised paper prices in March 2026, but converters expect relief only after new Asian coating lines start in late 2027.

Europe and North America face mixed trends. Walmart will replace paper shelf tags with digital price labels across all US stores by end-2026, trimming in-store paper volume, yet the same retailer is expanding RFID mandates that rely on hybrid direct thermal labels at distribution centers. The EU regulation, effective in August 2026, favors the adoption of linerless, and UPM's ProCycle wash-off adhesive, launched in May 2026, targets that requirement. South America and Africa trail in uptake because fragmented rules and price sensitivity keep thermal transfer attractive for longer-life shipments.

- Avery Dennison Corporation

- Appvion Operations Inc.

- Zebra Technologies Corporation

- Oji Holdings Corporation

- Ricoh Company Ltd.

- CCL Industries Inc.

- Honeywell International Inc.

- 3M Company

- SATO Holdings Corporation

- UPM-Kymmene Oyj (UPM Raflatac)

- Brady Corporation

- Brother Industries, Ltd.

- Seiko Epson Corporation

- Fuji Seal International, Inc.

- Multi-Color Corporation

- WS Packaging Group, Inc.

- Resource Label Group, LLC

- LINTEC Corporation

- DNP Imagingcomm Co., Ltd.

- TSC Auto ID Technology Co., Ltd.

- BIXOLON Co., Ltd.

- Label Technology, Inc.

- R. R. Donnelley & Sons Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Growth Accelerates On-Demand Label Printing

- 4.2.2 Stringent Pharmaceutical Traceability Mandates

- 4.2.3 Cost-Efficient No-Ribbon Printing Lowers Total Ownership

- 4.2.4 Rise of Linerless Sustainability Standards in Retail

- 4.2.5 Integration of QR and RFID Features for Smart Logistics

- 4.2.6 Expansion of Cold-Chain Food Delivery Services

- 4.3 Market Restraints

- 4.3.1 Volatility in Thermal Paper Base Prices

- 4.3.2 Fading and Image Stability Limitations in Harsh Environments

- 4.3.3 Growing Adoption of Digital Labeling and RFID Tags

- 4.3.4 Capital Expense for Linerless Conversion Equipment

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Paper Facestock

- 5.1.2 Synthetic Facestock

- 5.2 By Form Factor

- 5.2.1 Rolls

- 5.2.2 Fan-fold

- 5.2.3 Linerless

- 5.3 By End-user Industry

- 5.3.1 Logistics and Transportation

- 5.3.2 Retail and E-commerce

- 5.3.3 Food and Beverage

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Manufacturing and Industrial

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Turkey

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 Appvion Operations Inc.

- 6.4.3 Zebra Technologies Corporation

- 6.4.4 Oji Holdings Corporation

- 6.4.5 Ricoh Company Ltd.

- 6.4.6 CCL Industries Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 3M Company

- 6.4.9 SATO Holdings Corporation

- 6.4.10 UPM-Kymmene Oyj (UPM Raflatac)

- 6.4.11 Brady Corporation

- 6.4.12 Brother Industries, Ltd.

- 6.4.13 Seiko Epson Corporation

- 6.4.14 Fuji Seal International, Inc.

- 6.4.15 Multi-Color Corporation

- 6.4.16 WS Packaging Group, Inc.

- 6.4.17 Resource Label Group, LLC

- 6.4.18 LINTEC Corporation

- 6.4.19 DNP Imagingcomm Co., Ltd.

- 6.4.20 TSC Auto ID Technology Co., Ltd.

- 6.4.21 BIXOLON Co., Ltd.

- 6.4.22 Label Technology, Inc.

- 6.4.23 R. R. Donnelley & Sons Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment