|

市場調查報告書

商品編碼

2061741

運動控制:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Motion Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

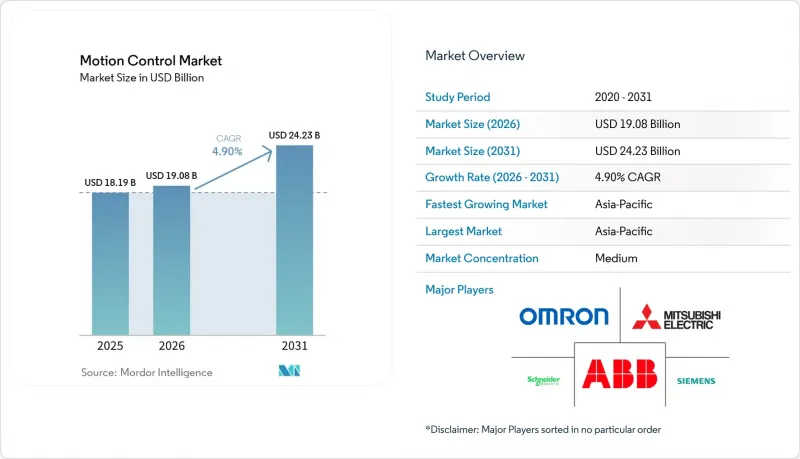

根據 Mordor Intelligence 預測,運動控制市場規模將從 2025 年的 181.9 億美元成長到 2026 年的 190.8 億美元,到 2031 年達到 242.3 億美元,2026 年至 2031 年的複合年成長率為 4.90%。

本報告按產品類型(馬達、驅動器等)、技術(電子機械、液壓、氣動)、系統類型(開放回路、閉合迴路)、軸類型(單軸、多軸)、應用(物料輸送、包裝等)、終端用戶行業(電子半導體、石油天然氣等)和地區進行細分。市場預測以美元計價。

全球運動控制市場趨勢及洞察

對智慧交通和機器整合機器人的需求正在激增。

製造商正在引入自主機器人和人工智慧驅動的輸送機,以提高加工能力並解決人手不足。預計全球機器人支出將從2025年的717.8億美元增加到2030年的1508.4億美元,這將推動對能夠管理多軸路徑規劃和避障的控制器的需求。 83%的製造商計劃將生成式人工智慧整合到其工廠車間,因此運動控制韌體現在整合了用於安排維護、平衡負載和自動調整伺服增益的預測演算法。這些功能使智慧機器人成為運動控制市場的主要驅動力。

快速過渡到分散式伺服驅動

透過將智慧功能從控制面板轉移到馬達側,佈線量可減少高達 86%,從而提高運動控制市場的電磁相容性。先進的驅動器現在整合了安全 PLC、資料登錄和邊緣運算功能,從而減少了控制面板空間並提高了生產線的柔軟性。 SEW-EURODRIVE 的 MOVIMOT 系列(額定功率 0.37 至 7.5 kW)憑藉其數位馬達介面和內建的安全轉矩關閉功能,體現了這項變革。

稀土元素磁鐵供應波動導致價格飆升

釹和鏑的價格波動導致伺服馬達成本上漲高達25%,對高扭力運動平台的利潤率造成壓力。儘管供應商多元化計畫和鐵氧體馬達的研發工作正在進行中,但實用化預計將會晚於預期的時間。

細分市場分析

到2025年,馬達將佔運動控制市場20.78%的佔有率,鞏固其作為通用執行器的地位。推動這一成長的主要動力來自用於機器人的緊湊型伺服馬達、用於半導體步進馬達的高扭矩馬達以及用於醫療設備的無框馬達。驅動器作為電源和位置控制之間的智慧層,是成長最快的細分市場,複合年成長率達6.65%,並正朝著邊緣運算方向發展,即時分析振動、溫度和負載。硬體和軟體的整合正在推動業務收益的成長,因為供應商正以訂閱模式銷售預測演算法。

對於在核磁共振成像儀孔內導航的醫療機器人而言,小型化至關重要;而像三菱電機1500A HVIGBT這樣的高功率模組則能提高鋼鐵廠和風力發電機中逆變器的效率。隨著原始設備製造商(OEM)維修現有生產線以適應更高的伺服頻寬和安全合規的驅動器,對控制器和機械系統的需求仍然強勁。

到2025年,電子機械平台將主導運動控制市場,佔據60.55%的市場佔有率,其優勢在於運作清潔、精度可擴展以及易於與數位雙胞胎整合。向淨零排放流程的轉型和能源成本的降低正在加速伺服電動壓力機作為液壓壓力機的替代方案的普及。配備壓力感測器和IO-Link閥的氣動解決方案正以6.85%的複合年成長率快速成長,因為它們能夠滿足低負載取放操作的需求,在這些操作中,速度比精度更為重要。

混合式設計趨勢將電動致動器與比例液壓系統結合,以實現高功率和高能源效率運作。預計電動線性致動器的銷售額將從2022年的205億美元成長到2032年的343億美元,反映出汽車沖壓加工和食品包裝領域對永續性的需求日益成長。

區域分析

預計到2025年,亞太地區將佔全球銷售額的37.65%,這主要得益於中國從低成本組裝向高度自動化生產的轉型,以及韓國半導體投資的創紀錄成長。印度的生產連結獎勵計畫計畫(PLI)正在加速電子園區的建設,這些園區指定伺服電動貼片機用於SMT生產線。區域政策支援、低成本的工程人才以及不斷上漲的工資水平,共同促成了許多工廠能夠在兩年內收回自動化投資成本。

在北美,企業正利用回流生產相關的激勵措施和稅額扣抵,對現有棕地工廠進行升級改造,採用節能驅動裝置。美國原始設備製造商(OEM)正優先考慮網路安全架構,以應對針對營運技術(OT)網路的高調勒索軟體攻擊。 ABB在威斯康辛州投資1億美元建設的園區就是一個典型的例子,該園區旨在縮短供應鏈並實現快速客製化。

綠色製造是歐洲的優先事項,德國汽車製造商正在對伺服壓力機進行改造,加裝能量再生模組,以滿足範圍 1 的目標。 NIS2 指令對運動網路引入了嚴格的加密措施,雖然這延緩了一些專案的進展,但最終促成了穩健架構的建構。協作機器人正被日益廣泛地採用,尤其是在義大利和西班牙,這兩個國家人口老化導致技術純熟勞工短缺。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對智慧交通系統和機器整合機器人的需求正在激增。

- 快速過渡到分散式伺服驅動

- 韓國和台灣半導體製造廠的擴張

- 移動式液壓系統的電氣化和運動控制器的進步

- 根據 FDA 附件 1 的修訂,對藥品填充和包裝生產線進行現代化改造。

- 在PLI的支持下,印度的電子產業叢集正在加速伺服的需求。

- 市場限制因素

- 稀土元素磁鐵供應波動導致價格飆升

- 歐洲OT網路安全認證延遲

- IGBT 和 MCU 的供不應求限制了驅動器的出貨量。

- 南美洲缺乏統一的程式設計標準

- 價值供應鏈分析

- 監理展望

- 技術進步

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 引擎

- 駕駛

- 控制器

- 執行器和機械系統

- 感測器和回饋裝置

- 軟體和服務

- 透過技術

- 電子機械

- 油壓

- 氣壓

- 依系統類型

- 開放回路

- 閉合迴路

- 按軸類型

- 單軸

- 多軸

- 透過使用

- 物料輸送

- 包裝

- 組裝和拆卸

- 檢驗和測試

- 機器人技術

- 3D列印/積層製造

- 按最終用戶行業分類

- 電子和半導體

- 製藥/生命科學/醫療設備

- 石油和天然氣

- 金屬和採礦

- 食品/飲料

- 車

- 航太/國防

- 物流和倉儲

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- Siemens AG

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Yaskawa Electric Corporation

- Schneider Electric SE

- Omron Corporation

- Parker Hannifin Corp

- Fanuc Corporation

- Bosch Rexroth AG

- Delta Electronics, Inc.

- Emerson Electric Co.

- Kollmorgen Corporation

- Inovance Technology

- Nidec Corporation

- Novanta Inc.

- Danfoss A/S

- Altra Industrial Motion

- Moog Inc.

- Beckhoff Automation GmbH & Co. KG

- Lenze SE

- Aerotech Inc.

- Allied Motion Technologies Inc.

- NSK Ltd.

- Hiwin Technologies Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the motion control market size is expected to increase from USD 18.19 billion in 2025 to USD 19.08 billion in 2026 and reach USD 24.23 billion by 2031, growing at a CAGR of 4.90% over 2026-2031.

This report is Segmented by Product Type (Motors, Drives, and More), Technology (Electromechanical, Hydraulic, Pneumatic), System Type (Open Loop, Closed Loop), Axis Type (Single Axis, Multi-Axis), Application (Material Handling, Packaging, and More), End-User Industry (Electronics and Semiconductor, Oil and Gas, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Motion Control Market Trends and Insights

Surge in Demand for Smart Conveyance and Machine-Integrated Robotics

Manufacturers are deploying autonomous mobile robots and AI-driven conveyors to raise throughput and offset labor shortages. Global robotics spending is projected to climb from USD 71.78 billion in 2025 to USD 150.84 billion by 2030, intensifying the need for controllers that manage multi-axis path planning and collision avoidance. With 83% of producers planning to embed generative AI on the plant floor, motion-control firmware now incorporates predictive algorithms that schedule maintenance, balance loads, and self-tune servo gains. These capabilities position smart robotics as a primary catalyst for the motion control market.

Rapid Transition to Decentralised Servo Drives

Moving intelligence from the cabinet to the motor slashes cabling by up to 86% and improves electromagnetic compatibility in the motion control market. Advanced drives now integrate safety PLC, data logging, and edge computing, cutting panel space and boosting line flexibility. SEW-EURODRIVE's MOVIMOT range, rated 0.37-7.5 kW, illustrates this shift with digital motor interfaces and built-in safe torque off functions.

Price Spikes from Rare-Earth Magnet Supply Volatility

Neodymium and dysprosium price swings have inflated servo motor costs by up to 25%, squeezing margins for high-torque motion platforms. Supplier diversification programs and ferrite-based motor R&D are under way, but commercial roll-out will trail the forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor Fab Expansions in South Korea and Taiwan

- Electrification of Mobile Hydraulics Upgrading Motion Controllers

- OT-Network Cyber-Security Certification Delays in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Motors held 20.78% of the motion control market in 2025, underscoring their status as universal actuators. Growth stems from compact servomotors for robotics, large torque motors for semiconductor steppers, and frameless motors for medical devices. Drives, the intelligence layer between power and position, are the fastest risers at 6.65% CAGR, evolving into edge computers that analyze vibration, temperature, and load in real time. This hardware-software fusion enlarges service revenues as vendors sell predictive algorithms on subscription.

Miniaturization is critical in medical robots that navigate inside MRI bores, while high-power modules like Mitsubishi Electric's 1,500 A HVIGBT raise inverter efficiency for steel mills and wind turbines. Controllers and mechanical systems enjoy steady demand as OEMs retrofit legacy lines to accommodate higher servo bandwidths and safety-rated drives.

Electromechanical platforms dominated the motion control market with a 60.55% share in 2025, favored for clean operation, scalable precision, and straightforward integration with digital twins. The shift toward net-zero processes and lower utility bills accelerates adoption of servo-electric presses, replacing hydraulic counterparts. Pneumatic solutions, now equipped with pressure sensors and IO-Link valves, are expanding at 6.85% CAGR by satisfying low-force pick-and-place tasks where speed trumps accuracy.

The hybridization trend marries electric actuators with proportional hydraulics, allowing force-dense yet energy-efficient motion. Electric linear actuator revenues are projected to climb from USD 20.5 billion in 2022 to USD 34.3 billion by 2032, mirroring sustainability mandates in automotive stamping and food packaging.

Geography Analysis

Asia Pacific held 37.65% of global revenue in 2025, propelled by China's shift from low-cost assembly to high-automation production and South Korea's record semiconductor outlays. India's Production Linked Incentive program is catalyzing electronics parks that specify servo-electric pick-and-place units in SMT lines. Regional policy support, low-cost engineering talent, and rising wages converge to make automation pay back in under two years for many factories.

North America leverages reshoring incentives and tax credits to upgrade brownfield plants with energy-efficient drives. U.S. OEMs emphasize cyber-secure architectures, a response to high-profile ransomware attacks on OT networks. ABB's USD 100 million Wisconsin campus exemplifies investment aimed at shortening supply chains and supporting quick-turn customization.

Europe prioritizes green manufacturing; German automakers retrofit servo presses with energy-recuperation modules to meet Scope 1 targets. The NIS2 directive introduces strict encryption for motion networks, slowing some projects but ultimately fostering resilient architectures. Collaborative robot adoption is high as demographic aging creates skilled-labor gaps, particularly in Italy and Spain.

- ABB Ltd.

- Siemens AG

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Yaskawa Electric Corporation

- Schneider Electric SE

- Omron Corporation

- Parker Hannifin Corp

- Fanuc Corporation

- Bosch Rexroth AG

- Delta Electronics, Inc.

- Emerson Electric Co.

- Kollmorgen Corporation

- Inovance Technology

- Nidec Corporation

- Novanta Inc.

- Danfoss A/S

- Altra Industrial Motion

- Moog Inc.

- Beckhoff Automation GmbH & Co. KG

- Lenze SE

- Aerotech Inc.

- Allied Motion Technologies Inc.

- NSK Ltd.

- Hiwin Technologies Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for smart conveyance and machine-integrated robotics

- 4.2.2 Rapid transition to decentralised servo drives

- 4.2.3 Semiconductor fab expansions in South Korea and Taiwan

- 4.2.4 Electrification of mobile hydraulics upgrading motion controllers

- 4.2.5 Post-FDA Annex 1 modernisation of pharma fill-finish lines

- 4.2.6 India's PLI-backed electronics clusters accelerating servo demand

- 4.3 Market Restraints

- 4.3.1 Price spikes from rare-earth magnet supply volatility

- 4.3.2 OT-network cyber-security certification delays in Europe

- 4.3.3 IGBT and MCU shortages constraining drive shipments

- 4.3.4 Lack of unified programming standards in South America

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Advancements

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Motors

- 5.1.2 Drives

- 5.1.3 Controllers

- 5.1.4 Actuators and Mechanical Systems

- 5.1.5 Sensors and Feedback Devices

- 5.1.6 Software and Services

- 5.2 By Technology

- 5.2.1 Electromechanical

- 5.2.2 Hydraulic

- 5.2.3 Pneumatic

- 5.3 By System Type

- 5.3.1 Open Loop

- 5.3.2 Closed Loop

- 5.4 By Axis Type

- 5.4.1 Single Axis

- 5.4.2 Multi-Axis

- 5.5 By Application

- 5.5.1 Material Handling

- 5.5.2 Packaging

- 5.5.3 Assembly and Disassembly

- 5.5.4 Inspection and Testing

- 5.5.5 Robotics

- 5.5.6 3D Printing / Additive Manufacturing

- 5.6 By End-user Industry

- 5.6.1 Electronics and Semiconductor

- 5.6.2 Pharmaceutical / Life Sciences / Medical Devices

- 5.6.3 Oil and Gas

- 5.6.4 Metal and Mining

- 5.6.5 Food and Beverage

- 5.6.6 Automotive

- 5.6.7 Aerospace and Defense

- 5.6.8 Logistics and Warehousing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 Israel

- 5.7.4.1.2 Saudi Arabia

- 5.7.4.1.3 United Arab Emirates

- 5.7.4.1.4 Turkey

- 5.7.4.1.5 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Egypt

- 5.7.4.2.3 Rest of Africa

- 5.7.4.1 Middle East

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Mitsubishi Electric Corporation

- 6.4.4 Rockwell Automation, Inc.

- 6.4.5 Yaskawa Electric Corporation

- 6.4.6 Schneider Electric SE

- 6.4.7 Omron Corporation

- 6.4.8 Parker Hannifin Corp

- 6.4.9 Fanuc Corporation

- 6.4.10 Bosch Rexroth AG

- 6.4.11 Delta Electronics, Inc.

- 6.4.12 Emerson Electric Co.

- 6.4.13 Kollmorgen Corporation

- 6.4.14 Inovance Technology

- 6.4.15 Nidec Corporation

- 6.4.16 Novanta Inc.

- 6.4.17 Danfoss A/S

- 6.4.18 Altra Industrial Motion

- 6.4.19 Moog Inc.

- 6.4.20 Beckhoff Automation GmbH & Co. KG

- 6.4.21 Lenze SE

- 6.4.22 Aerotech Inc.

- 6.4.23 Allied Motion Technologies Inc.

- 6.4.24 NSK Ltd.

- 6.4.25 Hiwin Technologies Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

高精度運動平台:2026-2032 年全球市場佔有率和排名、總收入和需求預測。

高精度運動平台:2026-2032 年全球市場佔有率和排名、總收入和需求預測。 運動和位置感測器市場報告:趨勢、預測和競爭分析(至2035年)

運動和位置感測器市場報告:趨勢、預測和競爭分析(至2035年) 定位平台市場預測至2034年-按類型、驅動系統、驅動機構、最終用戶和地區分類的全球分析

定位平台市場預測至2034年-按類型、驅動系統、驅動機構、最終用戶和地區分類的全球分析 電腦數值控制(CNC) 市場:按型號、組件、軸數、控制方法和最終用戶分類-2026-2032 年全球市場預測運動控制市場:2026-2032年全球市場預測(按交付方式、運動技術、軸配置、控制架構、輸出範圍、應用和產業分類)

電腦數值控制(CNC) 市場:按型號、組件、軸數、控制方法和最終用戶分類-2026-2032 年全球市場預測運動控制市場:2026-2032年全球市場預測(按交付方式、運動技術、軸配置、控制架構、輸出範圍、應用和產業分類) 全球運動控制市場規模、佔有率、趨勢和成長分析報告(2026-2034)運動定位平台市場:依運動類型、軸類型、軸承類型、驅動機構、負載能力、最終用戶和銷售管道分類-2026-2032年全球市場預測

全球運動控制市場規模、佔有率、趨勢和成長分析報告(2026-2034)運動定位平台市場:依運動類型、軸類型、軸承類型、驅動機構、負載能力、最終用戶和銷售管道分類-2026-2032年全球市場預測 2026年全球機器人運動控制軟體市場報告無槽無刷直流伺服馬達市場:按控制類型、連續轉矩範圍、額定電壓、終端用戶產業和應用分類-全球預測,2026-2032年單軸定位平台市場:按驅動系統、驅動技術、應用和終端用戶產業分類,全球預測(2026-2032年)

2026年全球機器人運動控制軟體市場報告無槽無刷直流伺服馬達市場:按控制類型、連續轉矩範圍、額定電壓、終端用戶產業和應用分類-全球預測,2026-2032年單軸定位平台市場:按驅動系統、驅動技術、應用和終端用戶產業分類,全球預測(2026-2032年)