|

市場調查報告書

商品編碼

2061725

高粱脂肪酸油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Tall Oil Fatty Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

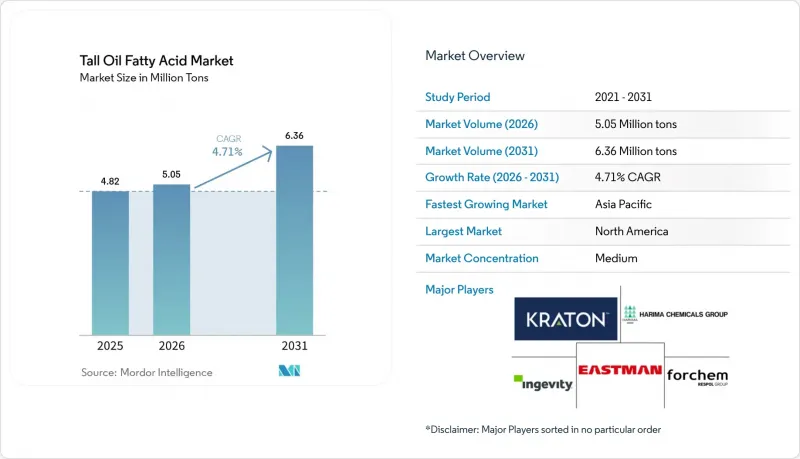

根據 Mordor Intelligence 預測,妥爾油脂肪酸的市場規模預計將在 2025 年達到 482 萬噸,2026 年達到 505 萬噸,到 2031 年達到 636 萬噸,2026 年至 2031 年的複合年成長率為 4.71%。

本報告按產品類型(油酸、亞麻油酸、亞麻油酸、棕櫚酸及其他產品類型)、應用領域(醇酸樹脂、二聚體酸、脂肪酸酯及其他應用)、終端用戶行業(肥皂和清潔劑、油漆和塗料及其他)以及地區(亞太地區、北美地區、歐洲及其他地區)進行細分。市場預測以銷售量(噸)為單位。

全球妥爾油脂肪酸市場趨勢及洞察

對生物基潤滑劑的需求日益成長

汽車和工業設備原始設備製造商 (OEM) 正在轉向符合嚴格生態標籤標準的生物基潤滑油。妥爾油脂肪酸 (TOFA) 市場的參與企業正將 TOFA 酯定位為一種可直接替代基料,具有高潤滑性、快速生物分解性和可靠的低溫流動性。 2023 年,CTO 價格飆升迫使潤滑油生產商暫時轉而使用植物脂肪酸,但此後通過多年供應契約,價格已趨於穩定。新的需求領域包括電動車的傳熱流體和風力發電機的齒輪箱油,這兩者都需要高純度的氫化 TOFA。生產商正在升級其氫化和分餾設備,以滿足氧化穩定性目標。隨著 OEM 的永續發展目標日益嚴格,歐洲和美國對經過認證和可追溯的 TOFA 的訂單正在不斷成長。

建築塗料中醇酸樹脂消費量的成長

建築塗料產業正在推動醇酸樹脂的消費,利用其黏合劑實現流平性、保光性和經濟高效的固態含量。 LEED 和 BREEAM 等認證體系鼓勵使用含有可再生碳的塗料,尤其是以妥爾油脂肪酸 (TOFA) 為基礎的醇酸樹脂,其生物基碳含量尤為突出。受印度和中國城市住宅建設的推動,亞太地區的塗料市場正在蓬勃發展。雖然丙烯酸和聚氨酯分散體在高檔外牆塗料領域備受關注,但醇酸-丙烯酸混合體係正在迅速縮小性能差距。與塗料製造商合作開發這些混合產品的生產商有望獲得盈利的長期供應合約。因此,妥爾油脂肪酸市場正將其重心從傳統的通用酯類轉向這些高附加價值黏合劑應用領域。

對針葉木牛皮紙漿生產能力的依賴

全球軟木牛皮紙漿產量限制了妥爾油脂肪酸(TOFA)的供應。自2020年以來,數位媒體和包裝產業轉向使用硬木纖維,導致北美多家造紙廠關閉。同時,隨著可再生柴油業務的擴張,預計CTO的需求佔有率將增加,化學品製造商和燃料用戶之間的競爭也日益激烈。 TOFA市場在確保永續原料方面面臨挑戰,尤其是在南美洲和東南亞,這些地區尚未新建軟木紙漿廠。

細分市場分析

截至2025年,油酸將佔據妥爾油脂肪酸市場42.74%的最大佔有率,而亞麻油酸預計到2031年將以5.92%的複合年成長率成長。油酸的C18:1結構使其成為金屬加工液、界面活性劑和醇酸樹脂的基礎原料。經滅菌處理的油酸與甘油和多元醇混合使用,可增強個人保健產品和農藥配方中的乳化劑性能,即使在原料價格波動的情況下也能穩定市場需求。富含三不飽和鍵的亞麻油酸因其能夠促進快速氧化交聯,在高性能塗料和黏合劑聚醯胺中具有重要價值。此類黏合劑在汽車輕量化和風力發電機葉片製造中發揮重要作用,從而推動了該領域的成長。

亞麻油酸的成長也反映出精煉商正轉向高利潤的特種產品。對氮基儲存和抗氧化包裝的投資降低了其氧化敏感性,從而支持更長的供應鏈。棕櫚酸和其他飽和脂肪酸佔據了肥皂、橡膠和香料等細分市場,但缺乏滿足激增需求的反應能力。 SunPine公司向α-蒎烯的多元化發展以及Kraton公司對產量最佳化的關注表明,妥爾油脂肪酸市場的參與企業企業正在完善其產品線,以抵消大宗商品價格波動的影響。

區域分析

到2025年,北美將佔全球總產量的35.38%,這主要得益於美國東南部牛皮紙漿廠為綜合煉油廠供應原料。可再生柴油燃料的實施加劇了CTO的競標競爭,導致2022年至2023年間價格大幅上漲。儘管Ingevity出售北查爾斯頓煉油廠降低了綜合產能,但Kraton的塔器升級旨在重新奪回區域市場佔有率。加拿大向美國煉油廠出口CTO,而墨西哥的需求主要集中在清潔劑產業。

預計到2031年,亞太地區將維持7.51%的複合年成長率,這主要得益於中國的生物材料發展藍圖和印度蓬勃發展的建築業,後者使油漆需求加倍。俄羅斯對中國木材出口的限制推高了中國TOFA買家的成本,導致他們轉向北歐和美國的鋸木廠採購。日本和韓國正透過汽車潤滑油來穩定區域需求,而印尼和越南則在提高牛皮紙產能(儘管其中大部分源自硬木)。

歐洲正受益於瑞典和芬蘭的綜合煉油廠,這些煉油廠向化學和生質燃料工廠供應妥爾油 (CTO)。儘管 RED III 法規下的雙重累計導致 SunPine 的銷量下滑,煉油廠的訂單依然存在,但 UPM 的 Leuna 專案凸顯了後向整合的資本密集特徵。法國逐步取消妥爾油摻混上限以及德國的雙重累計正在創造跨境套利機會,鼓勵妥爾油脂肪酸市場的參與企業將其貨物運往更有利的司法管轄區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對生物基潤滑劑的需求日益成長

- 建築塗料中醇酸樹脂的消耗量不斷成長

- TOFA基二聚體酸在黏合劑和油田化學品的應用日益廣泛

- 政府對低碳原料的獎勵

- 該地區CTO煉油廠的關閉推高了價格溢價,並推動了新產能的擴張。

- 市場限制因素

- 對針葉木牛皮紙漿生產能力的依賴

- 加強有關伐木的森林法規

- 與低成本植物油衍生脂肪酸的競爭

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 油酸

- 亞麻油酸

- 亞麻油酸

- 棕櫚酸

- 其他產品類型(例如硬脂酸)

- 透過使用

- 醇酸樹脂

- 二聚酸

- 脂肪酸酯

- 其他用途(例如,潤滑油添加劑)

- 按最終用戶行業分類

- 肥皂和清潔劑

- 油漆和塗料

- 車

- 金屬加工潤滑劑

- 石油和天然氣

- 其他終端用戶產業(黏合劑、密封劑等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Ataman Kimya

- Eastman Chemical Company

- Fintoil Hamina Oy

- Forchem Oyj

- Foreverest Resources Ltd.

- Georgia-Pacific Chemicals

- Harima Chemicals Group, Inc.

- Ilim Group

- Imperial Industrial Minerals Company

- Ingevity

- Kraton Corporation

- Lascaray SA

- Pasand Speciality Chemicals

- Pine Chemical Group

- Segezha Group

- SunPine AB

- Univar SolutionsLLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the tall oil fatty acid market size is projected to be 4.82 Million tons in 2025, 5.05 Million tons in 2026, and reach 6.36 Million tons by 2031, growing at a CAGR of 4.71% from 2026 to 2031.

This report is Segmented by Product Type (Oleic Acid, Linoleic Acid, Linolenic Acid, Palmitic Acid, and Other Product Types), Application (Alkyd Resins, Dimer Acids, Fatty Acid Esters, and Other Applications), End-User Industry (Soaps and Detergents, Paints and Coatings, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Tall Oil Fatty Acid Market Trends and Insights

Escalating Demand for Bio-based Lubricants

Original equipment manufacturers in automotive and industrial equipment are switching to bio-based lubricants that satisfy stringent eco-label criteria. Tall Oil Fatty Acid market participants position TOFA esters as drop-in basestocks that offer high lubricity, rapid biodegradation, and reliable low-temperature flow. Elevated CTO costs temporarily prompted formulators to revert to vegetable fatty acids in 2023, but multi-year supply contracts have since stabilized pricing. New demand pockets include electric-vehicle thermal fluids and wind-turbine gearbox oils, both of which need high-purity, hydrogenated grades. Producers are upgrading hydrotreating and fractionation units to meet oxidative-stability targets. As OEM sustainability targets tighten, volume commitments for certified, traceable TOFA are growing across Europe and the United States.

Expanding Alkyd-Resin Consumption in Architectural Coatings

Architectural coatings dominate the consumption of alkyd resins, leveraging their binders for enhanced leveling, gloss retention, and a cost-effective solids content. Certification schemes like LEED and BREEAM incentivize paints with renewable carbon content, and notably, TOFA-based alkyds boast a bio-based carbon content. The Asia-Pacific region, propelled by urban housing initiatives in India and China, witnesses growth in its coatings segment. While acrylic and polyurethane dispersions are gaining traction in premium exterior coatings, hybrid alkyd-acrylic systems are rapidly bridging the performance divide. Producers collaborating with coating companies to co-develop these hybrids stand to secure lucrative long-term offtake agreements. As a result, the Tall Oil Fatty Acid market is shifting focus towards these value-added binder applications, moving away from its traditional commodity esters.

Dependence on Softwood Kraft-Pulping Capacity

Global output of softwood kraft pulp limits the availability of Tall Oil Fatty Acid (TOFA). Since 2020, a shift in digital media and packaging towards hardwood fibers has resulted in the closure of several mills across North America. Meanwhile, as renewable diesel expansions eye a larger share of CTO, competition intensifies between chemical producers and fuel customers. The TOFA market faces a persistent feedstock challenge, especially in the absence of new softwood mills emerging in South America or Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use of TOFA-based Dimer Acids in Adhesives and Oil-field Chemicals

- Government Incentives for Low-Carbon Feedstocks

- Stricter Forestry Regulations on Logging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oleic Acid held 42.74% of volume in 2025, the largest slice of Tall Oil Fatty Acid market share, while Linolenic Acid is projected to register the fastest 5.92% CAGR through 2031. Oleic Acid's C18:1 profile underpins metalworking fluids, surfactants, and alkyd resins. Its esters with glycerol and polyols fortify emulsifiers across personal-care and agrochemical formulations, keeping demand stable even amid feedstock fluctuations. Linolenic Acid, rich in triple unsaturation, enables rapid oxidative crosslinking, making it valuable in high-performance coatings and adhesive polyamides. Automotive lightweighting and wind-turbine blade production require such adhesives for fatigue resistance, explaining the segment's momentum.

Growth in Linolenic Acid also reflects refiners' move toward high-margin specialties. Investments in nitrogen-blanketed storage and antioxidant packages mitigate its oxidation sensitivity, supporting longer supply chains. Palmitic and other saturated acids fulfill soap, rubber, and fragrance niches but lack the reactivity to capture dynamic demand. SunPine's diversification into a-Pinene and Kraton's focus on yield optimization illustrate how Tall Oil Fatty Acid market participants are upgrading product slates to offset commodity price volatility.

Geography Analysis

North America contributed 35.38% of the 2025 volume, led by Southeastern United States kraft-pulp mills that supply integrated refineries. Renewable diesel mandates have escalated CTO bidding wars, lifting prices substantially between 2022 and 2023. Ingevity's divestment of its North Charleston refinery removed integrated capacity, while Kraton's tower upgrade aims to claw back regional share. Canada exports CTO to U.S. refiners, and Mexico's demand sits mostly in detergents.

Asia-Pacific is forecast to post a 7.51% CAGR through 2031, bolstered by China's bio-materials roadmap and India's construction boom, which multiplies coatings demand. Russia-to-China timber curbs raised costs for Chinese TOFA buyers, redirecting procurement to Nordic and U.S. mills. Japan and South Korea stabilize regional demand through automotive lubricants, whereas Indonesia and Vietnam add kraft capacity, albeit mostly hardwood.

Europe benefits from Sweden and Finland's integrated kraft complexes that feed CTO to both chemical and biofuel plants. RED III double-counting sustains refinery order books even after SunPine's revenue dip, while UPM's Leuna project highlights the capital intensity of backward integration. France's CTO blend cap and Germany's phase-out of double counting introduce cross-border arbitrage, nudging Tall Oil Fatty Acid market participants to route cargoes toward more favorable jurisdictions.

- Ataman Kimya

- Eastman Chemical Company

- Fintoil Hamina Oy

- Forchem Oyj

- Foreverest Resources Ltd.

- Georgia-Pacific Chemicals

- Harima Chemicals Group, Inc.

- Ilim Group

- Imperial Industrial Minerals Company

- Ingevity

- Kraton Corporation

- Lascaray S.A.

- Pasand Speciality Chemicals

- Pine Chemical Group

- Segezha Group

- SunPine AB

- Univar SolutionsLLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating demand for bio-based lubricants

- 4.2.2 Expanding alkyd-resin consumption in architectural coatings

- 4.2.3 Rising use of TOFA-based dimer acids in adhesives and oil-field chemicals

- 4.2.4 Government incentives for low-carbon feedstocks

- 4.2.5 Regional CTO-refinery closures driving price premiums and new capacity

- 4.3 Market Restraints

- 4.3.1 Dependence on softwood kraft-pulping capacity

- 4.3.2 Stricter forestry regulations on logging

- 4.3.3 Competition from lower-cost vegetable-oil fatty acids

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Oleic Acid

- 5.1.2 Linoleic Acid

- 5.1.3 Linolenic Acid

- 5.1.4 Palmitic Acid

- 5.1.5 Other Product Types (Stearic Acid, etc.)

- 5.2 By Application

- 5.2.1 Alkyd Resins

- 5.2.2 Dimer Acids

- 5.2.3 Fatty Acid Esters

- 5.2.4 Other Applications (Lubricant Additives, etc.)

- 5.3 By End-user Industry

- 5.3.1 Soaps and Detergents

- 5.3.2 Paints and Coatings

- 5.3.3 Automotive

- 5.3.4 Metalworking Fluids

- 5.3.5 Oil and Gas

- 5.3.6 Other End User Industries (Adhesives and Sealants, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Ataman Kimya

- 6.4.2 Eastman Chemical Company

- 6.4.3 Fintoil Hamina Oy

- 6.4.4 Forchem Oyj

- 6.4.5 Foreverest Resources Ltd.

- 6.4.6 Georgia-Pacific Chemicals

- 6.4.7 Harima Chemicals Group, Inc.

- 6.4.8 Ilim Group

- 6.4.9 Imperial Industrial Minerals Company

- 6.4.10 Ingevity

- 6.4.11 Kraton Corporation

- 6.4.12 Lascaray S.A.

- 6.4.13 Pasand Speciality Chemicals

- 6.4.14 Pine Chemical Group

- 6.4.15 Segezha Group

- 6.4.16 SunPine AB

- 6.4.17 Univar SolutionsLLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

原油焦油衍生產品市場報告:按成分、應用、最終用戶和地區分類(2026-2034 年)

原油焦油衍生產品市場報告:按成分、應用、最終用戶和地區分類(2026-2034 年) 原油及高品位原油市場-全球產業規模、佔有率、趨勢、機會及預測:依產品、應用、最終用戶、地區及競爭格局分類,2021-2031年

原油及高品位原油市場-全球產業規模、佔有率、趨勢、機會及預測:依產品、應用、最終用戶、地區及競爭格局分類,2021-2031年 蒸餾妥爾油市場:按產品類型、製造流程、應用和分銷管道分類的全球市場預測,2026-2032年

蒸餾妥爾油市場:按產品類型、製造流程、應用和分銷管道分類的全球市場預測,2026-2032年 粗妥爾油市場:按蒸餾製程、應用、最終用戶和地區分類粗妥爾油衍生物市場:依衍生物類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測妥爾油脂肪酸市場:2026-2032年全球市場預測(依產品類型、等級、應用、終端用戶產業及通路分類)妥爾油市場:依產品類型、原料、應用和終端用戶產業分類-2026-2032年全球預測

粗妥爾油市場:按蒸餾製程、應用、最終用戶和地區分類粗妥爾油衍生物市場:依衍生物類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測妥爾油脂肪酸市場:2026-2032年全球市場預測(依產品類型、等級、應用、終端用戶產業及通路分類)妥爾油市場:依產品類型、原料、應用和終端用戶產業分類-2026-2032年全球預測 全球粗妥爾油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球粗妥爾油市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球妥爾油脂肪酸市場報告

2026年全球妥爾油脂肪酸市場報告 妥爾油脂肪酸市場規模、佔有率及成長分析(按產品、應用、最終用戶和地區分類)-2026-2033年產業預測

妥爾油脂肪酸市場規模、佔有率及成長分析(按產品、應用、最終用戶和地區分類)-2026-2033年產業預測