|

市場調查報告書

商品編碼

2061689

北美汽車用高強度鋼:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Automotive AHSS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

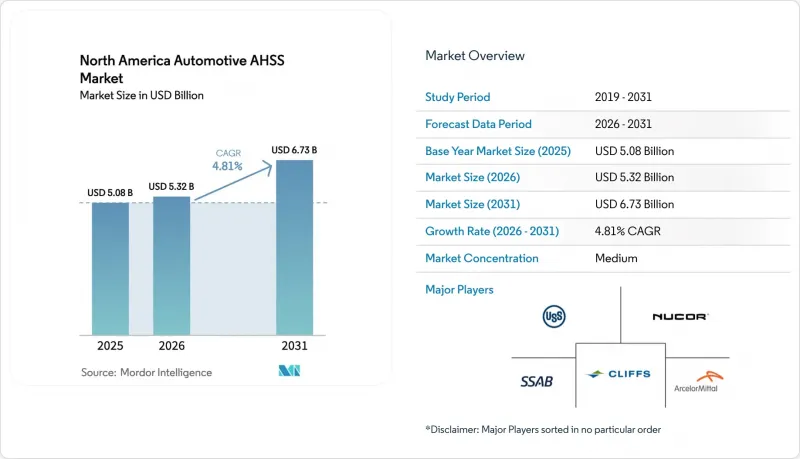

根據 Mordor Intelligence 預測,北美汽車用高抗張強度鋼 (AHSS) 市場將從 2025 年的 50.8 億美元成長到 2026 年的 53.2 億美元,到 2031 年達到 67.3 億美元,在預測期(2026-2031 年成長率為 4.81%。

本報告按產品類型(雙相、TRIP、複雜相、馬氏體及其他)、車輛類型(乘用車及其他)、應用(白車身、底盤、懸吊、車門、擋泥板、艙蓋及其他)、製造程序(軋延、軋延、鍍鋅)、最終用戶(OEM 和售後市場)以及國家/地區進行細分。市場預測以美元(USD)為單位。

北美汽車用高強度鋼市場趨勢與洞察

美國和加拿大嚴格的燃油效率和溫室氣體排放法規正在加速汽車減重。

美國環保署 (EPA) 和國家公路交通安全管理局 (NHTSA) 已最終確定計劃,在 2024-2025 年車型年度內將燃油經濟性提高 8%,到 2026 年逐步提高到 10%,並力爭到 2032 年將平均車輛燃油經濟性提升至相當於 58 英里/加侖(約 4.3 公升/百公里)。車輛總重每減輕一磅(約 0.45 公斤),燃油節省量就會顯著增加。因此,白車身 (BIW) 製造商正從使用普通鋼材轉向使用雙相鋼和複合相鋼。這些尖端材料可以在不影響扭轉剛度的前提下,使用更薄的鈑金。加拿大也採取了類似的措施,實施了零排放車輛的銷售配額制度,旨在全面推廣零排放車輛。此舉強調了結構剛度的重要性,尤其是在電池組增加導致車輛重量增加的情況下。聯準會的一項研究計算了監管合規成本佔車輛價格的百分比。這項發現促使汽車製造商 (OEM) 優先考慮材料改進,而不是成本更高的動力系統改造。蒂森克虜伯的 HCT980XG 雙相鋼與低碳鋼相比,重量顯著減輕,同時維持了降低噪音、振動和不適感 (NVH) 所必需的扭轉剛度。

提高 IIHS 和 NCAP 的碰撞安全評級標準將鼓勵採用更堅固的車身結構。

美國公路安全保險協會 (IIHS) 收緊了側面碰撞標準,對達到「良好」評級所需的 B 柱變形量設定了上限。為了滿足這些標準,製造商擴大在籠式車身結構中使用熱壓硬化馬氏體鋼。這標誌著汽車產業正在改變以往認為足夠安全的零件。未來,美國國家公路交通安全管理局 (NHTSA) 計劃引入正面斜撞和迎面側面碰撞測試,這將要求戶定板和車頂橫桿具有更高的抗張強度。為了獲得「頂級安全之選+」評級,日產汽車增加了高抗張強度鋼 (AHSS) 的使用,並在 Rogue 車型中採用了客製化焊接的立柱。同時,雪佛蘭 Blazer 電動車整合了高強度鋼和超高高抗張強度鋼 (UHSS),清楚地展現了整個產業的立場:即使在主流電動車領域,碰撞安全性也優先於成本。

與傳統鋼材和鋁材相比,成本溢價將持續存在。

強度超過某一水準的先進高強度鋼(AHSS)的價格會比強度較低的等級更高。而馬氏體熱壓硬化鋼的價格溢價可能較高。由於鋁的密度低,製造商可以在非結構性零件(例如蓋子)上實現顯著的減重。這項限制使得AHSS主要用於剛性比重量更重要的結構性部件。雖然關稅降低了進口鋁的成本優勢,但引擎蓋和尾門的製造商仍然傾向於使用複合材料。然而,對於小型、價格敏感的電池式電動車(BEV)而言,天平再次向鋼材傾斜。這是因為AHSS所需的大部分減重可以用更低的單位原料成本來實現。值得注意的是,克利夫蘭克里夫斯公司已經證明,只需對模具進行少量調整,即可在鋁壓機生產線上加工AHSS坯料。這項進步有助於汽車製造商(OEM)進行材料轉型。

細分市場分析

2025年,雙相鋼憑藉其優異的成形性和強度平衡,在北美汽車用高強度鋼(AHSS)市場維持了39.33%的佔有率。 TRIP牌號預計在2026年至2031年間將以7.78%的複合年成長率成長,成為該產品系列中成長率最高的牌號。在碰撞區域,原位硬化和分散變形的能力至關重要。複合相鋼在懸吊連桿中發揮特殊作用,而馬氏體鋼則更受青睞,尤其是在IIHS基準值不允許公差的高強度柱中。孿晶誘導塑性(TIP)鋼和溫成型鋼屬於小眾產品,但它們在研發領域正吸引著大量關注,METAKUS屢獲殊榮的SIBORA鋼便是最好的例證。

某些鋼材兼具高抗張強度和優異的延伸率,從而顯著降低了碰撞測試罐的變形率。調整沖壓間隙已顯示出提高高效成形率 (HER) 的潛力,並可應用於多種模具規格。採用這種鋼材製造液壓成形支柱的特定方案,在滿足最高安全標準的同時,相比熱壓硬化替代方案,實現了成本節約。儘管取得了這些進展,但由於側面碰撞載荷路徑中對耐用部件的持續需求,預計某些高抗張強度鋼材的需求仍將穩步成長。

乘用車仍將佔據最大的市場佔有率,到2025年將佔北美汽車用高強度鋼(AHSS)市場的62.29%,但隨著平台向成本控制更為嚴格的純電動車(BEV)架構轉型,其成長速度正在放緩。同時,由於宅配和服務車輛的電氣化和負載容量的提升,輕型商用車預計將以7.54%的複合年成長率成長。在中型和重型卡車中,高抗張強度鋼(AHSS)被選擇性地用於駕駛室和底盤縱梁,但其用量僅佔車輛總重的一小部分。

通用汽車的BrightDrop Zevo車型採用了更高比例的高強度鋼(AHSS)來平衡沉重的電池組,同時保持寬敞的貨艙空間。福特的新E-Transit也增加了高強度鋼的使用,以便在不降低負載容量下容納更大的電池組。 Rivian的EDV車型則採用熱沖壓車門梁來提高續航里程效率。在乘用車領域,本田思域在其ACE籠式車身結構中大量使用了高強度鋼,而價格更親民的車型則限制了高檔材料的使用,以保持成本競爭力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 美國和加拿大嚴格的燃油效率和溫室氣體排放法規正在加速汽車減重。

- IIHS 和 NCAP 碰撞安全評級標準的提高正在推動更堅固的車身結構的研發。

- 北美電動車產量的激增推高了對電池保護的 AHSS(防熱儲存系統)的需求。

- 國內電弧爐(EAF)的擴建將增加當地高等級鋼材的供應。

- 商業化應用有保證的HER等級,可以消除因邊緣裂紋造成的廢料。

- USMCA原產地規則有利於一級供應商將熱沖壓工序外包到近岸地區。

- 市場限制因素

- 與傳統鋼材和鋁材相比,其成本溢價持續存在。

- 升級資本密集型成型和焊接設備的需求正在減緩中小型二級供應商的採用速度。

- 地緣政治緊張局勢下關鍵合金元素(鎳、鉬)的供應風險

- 由於超高強度鋼鍍鋅生產線產能不足,工程出現延誤。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 雙相(DP)鋼

- 相變誘導塑性(TRIP)鋼

- 複合相(CP)鋼

- 馬氏體鋼

- 其他(包括TWIP和熱成型鋼)

- 按車輛類型

- 搭乘用車

- 輕型商用車(LCV)

- 中型和重型商用車輛(MHCV)

- 透過使用

- 車身結構(BIW)

- 底盤

- 暫停

- 車門、引擎蓋、後車廂蓋

- 保險桿

- 其他規則

- 透過製造程序

- 軋延

- 軋延

- 鍍鋅

- 最終用戶

- 目的地設備製造商 (OEM)

- 售後市場

- 國家

- 美國

- 加拿大

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ArcelorMittal NA

- United States Steel Corporation

- Nucor Corporation

- Cleveland-Cliffs Inc.(AK Steel)

- SSAB AB

- Tata Steel Ltd.

- POSCO

- Thyssenkrupp AG

- Baoshan Iron and Steel Co. Ltd.

- Nippon Steel Corporation

- JFE Steel Corporation

- Hyundai Steel Company

- Kobe Steel Ltd.

- Voestalpine AG

- Steel Dynamics Inc.

- JSW Steel USA

第7章 市場機會與未來展望

According to Mordor Intelligence, the north american automotive AHSS (Advanced High-Strength Steel) market size is projected to grow from USD 5.08 billion in 2025 to USD 5.32 billion in 2026, and is forecast to reach USD 6.73 billion by 2031, growing at a CAGR of 4.81% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dual Phase, TRIP, Complex Phase, Martensitic, and Others), Vehicle Type (Passenger Cars, and More), Application (BIW, Chassis, Suspension, Closures, and More), Manufacturing Process (Cold Rolled, Hot Rolled, and Galvanized), End User (OEMs and Aftermarket), and Country. The Market Forecasts are Provided in Value (USD).

North America Automotive AHSS Market Trends and Insights

Strict U.S./Canada Fuel-Economy and GHG Mandates Accelerate Light Weighting

The Environmental Protection Agency and the National Highway Traffic Safety Administration finalized 8% annual fuel-economy gains for model years 2024-2025 and a 10% step-up for 2026, pushing fleet averages toward 58 mpg-equivalent by 2032 . For every reduction in curb weight, fuel savings increase significantly. As a result, Body-in-White (BIW) manufacturers are transitioning from mild steel to dual-phase or complex-phase grades. These advanced materials enable a reduction in gauge without compromising torsional rigidity. Canada is adopting similar measures, introducing a zero-emission vehicle sales quota that aims to achieve full adoption. This move underscores the need for structural stiffness, especially as battery additions increase vehicle mass. A Federal Reserve study pegged the compliance cost as a percentage of a vehicle's price. This insight has led Original Equipment Manufacturers (OEMs) to prioritize material changes over more expensive propulsion modifications. Thyssenkrupp's HCT980XG dual-phase steel offers significant weight reduction compared to mild steel, all while maintaining a torsional stiffness critical for Noise, Vibration, and Harshness (NVH).

Rising IIHS and NCAP Crash-Rating Targets Spur Stronger Body Structures

The Insurance Institute for Highway Safety tightened side-impact standards, setting a limit on B-pillar intrusion for a "Good" rating. To meet this benchmark, manufacturers often turn to press-hardened martensitic steel in cage structures. This marks a shift from the previously adequate components. Looking ahead, the NHTSA plans to introduce frontal-oblique and far-side tests, necessitating higher tensile targets in rocker and roof rails. In a bid for a Top Safety Pick+ rating, Nissan boosted AHSS content in its Rogue and incorporated tailor-welded pillars. Meanwhile, Chevrolet's Blazer EV, with its AHSS and UHSS integration, underscores the industry's stance: even mainstream EVs prioritize crashworthiness over cost.

Persistent Cost Premium Versus Conventional Steels and Aluminum

AHSS grades above certain strength levels command a price premium over lower-strength grades. Meanwhile, martensitic press-hardened stock can fetch an even heftier premium. Thanks to aluminum's low density, manufacturers can achieve significant weight reduction in non-structural lids. This limitation confines AHSS usage primarily to structures where stiffness is prioritized over weight. While tariffs have diminished the cost advantage of imported aluminum, manufacturers of hoods and liftgates continue to adopt a mixed-material approach. However, for smaller, price-sensitive battery electric vehicles (BEVs), the scales tip back in favor of steel. This is because AHSS provides most of the desired weight reduction at a significantly lower cost per unit of raw material. In a notable move, Cleveland-Cliffs demonstrated that, with only minor adjustments to the dies, AHSS blanks can be processed on aluminum press lines. This development simplifies the transition between materials for original equipment manufacturers (OEMs).

Other drivers and restraints analyzed in the detailed report include:

- Surge in North American EV Output Lifts AHSS Demand for Battery Protection

- Domestic EAF Buildouts Widen Local Supply of Advanced Grades

- Capital-Intensive Forming / Welding Upgrades Slow Adoption at Smaller Tier-2s

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dual-phase steels maintained a 39.33% of the North America automotive AHSS market share in 2025, owing to their formability-versus-strength sweet spot. TRIP grades are forecast to post a 7.78% CAGR over 2026-2031, the fastest among the product slate. In crumple zones, the ability to harden on the fly and distribute deformation is crucial. Complex-phase steels occupy specialized roles in suspension links, while martensitic grades take precedence in high-strength pillars, especially where IIHS thresholds leave no room for error. Although twinning-induced plasticity and warm-formed steels are niche players, they are drawing significant R&D attention, as evidenced by METAKUS's award-winning SIBORA.

A specific type of steel offers high tensile strength and notable elongation, enabling significant draw ratios in crush cans. Adjustments to punching clearance have shown potential to boost HER, impacting die standards across a broad region. A particular concept, utilizing this steel in hydro-formed pillars, achieved cost savings compared to press-hardened alternatives while delivering performance aligned with top safety standards. Despite these advancements, certain high-strength steels are expected to grow steadily, driven by the continued need for durable components in side-impact load paths.

Passenger cars remain the tonnage leader at 62.29% of the North America automotive AHSS market share in 2025, but growth is slow as platforms migrate to cost-conscious BEV architectures. Light commercial vehicles are set for a 7.54% CAGR as parcel and service fleets electrify and increase payload. Medium- and heavy-duty trucks selectively incorporate Advanced High-Strength Steel (AHSS) in their cabs and chassis rails, limiting its use to a small percentage of the vehicle's total mass.

GM's BrightDrop Zevo uses a higher proportion of AHSS to counterbalance a heavy battery, while maintaining a spacious cargo bay. Ford's updated E-Transit increased its AHSS content to accommodate a larger battery pack without reducing payload capacity. Rivian's EDV utilizes hot-stamped door beams to enhance range efficiency. In the passenger car segment, Honda's Civic incorporates a significant amount of AHSS within its ACE cage, while more affordable models limit the use of premium materials to keep costs competitive.

List of Companies Covered in this Report:

- ArcelorMittal NA

- United States Steel Corporation

- Nucor Corporation

- Cleveland-Cliffs Inc. (AK Steel)

- SSAB AB

- Tata Steel Ltd.

- POSCO

- Thyssenkrupp AG

- Baoshan Iron and Steel Co. Ltd.

- Nippon Steel Corporation

- JFE Steel Corporation

- Hyundai Steel Company

- Kobe Steel Ltd.

- Voestalpine AG

- Steel Dynamics Inc.

- JSW Steel USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict U.S./Canada Fuel-Economy and GHG Mandates Accelerate Lightweighting

- 4.2.2 Rising IIHS and NCAP Crash-Rating Targets Spur Stronger Body Structures

- 4.2.3 Surge In North American EV Output Lifts AHSS Demand for Battery Protection

- 4.2.4 Domestic EAF Buildouts Widen Local Supply of Advanced Grades

- 4.2.5 Commercial Roll-Out of Guaranteed HER Grades Eliminates Edge-Crack Scrap

- 4.2.6 USMCA Rules-of-Origin Drive Tier-1 Hot-Stamping Near-Shoring

- 4.3 Market Restraints

- 4.3.1 Persistent Cost Premium Versus Conventional Steels and Aluminum

- 4.3.2 Capital-Intensive Forming/Welding Upgrades Slow Adoption at Smaller Tier-2s

- 4.3.3 Supply Risk for Critical Alloying Elements (Ni, Mo) Amid Geopolitical Tension

- 4.3.4 Limited Galvanizing-Line Capacity for UHSS Coatings Delays Programs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Dual Phase (DP) Steels

- 5.1.2 Transformation-Induced Plasticity (TRIP) Steels

- 5.1.3 Complex Phase (CP) Steels

- 5.1.4 Martensitic Steels

- 5.1.5 Others (including TWIP, Hot-Formed Steels)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCVs)

- 5.2.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.3 By Application

- 5.3.1 Body Structure (BIW)

- 5.3.2 Chassis

- 5.3.3 Suspension

- 5.3.4 Closures (Doors, Hoods, Trunk Lids)

- 5.3.5 Bumpers

- 5.3.6 Other Components

- 5.4 By Manufacturing Process

- 5.4.1 Cold Rolled

- 5.4.2 Hot Rolled

- 5.4.3 Galvanized

- 5.5 By End User

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 ArcelorMittal NA

- 6.4.2 United States Steel Corporation

- 6.4.3 Nucor Corporation

- 6.4.4 Cleveland-Cliffs Inc. (AK Steel)

- 6.4.5 SSAB AB

- 6.4.6 Tata Steel Ltd.

- 6.4.7 POSCO

- 6.4.8 Thyssenkrupp AG

- 6.4.9 Baoshan Iron and Steel Co. Ltd.

- 6.4.10 Nippon Steel Corporation

- 6.4.11 JFE Steel Corporation

- 6.4.12 Hyundai Steel Company

- 6.4.13 Kobe Steel Ltd.

- 6.4.14 Voestalpine AG

- 6.4.15 Steel Dynamics Inc.

- 6.4.16 JSW Steel USA

7 Market Opportunities and Future Outlook

汽車用先進高抗張強度鋼板市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、車輛類型、地區和競爭格局分類,2021-2031年

汽車用先進高抗張強度鋼板市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、車輛類型、地區和競爭格局分類,2021-2031年 汽車用高強度鋼市場:2026-2032年全球市場預測(依產品種類、應用、車輛種類、形狀及加工類型分類)

汽車用高強度鋼市場:2026-2032年全球市場預測(依產品種類、應用、車輛種類、形狀及加工類型分類) 汽車用高抗張強度鋼(AHSS)市場規模、佔有率和成長分析(按產品類型、車輛類型、應用、最終用戶和地區分類)-2026-2033年產業預測

汽車用高抗張強度鋼(AHSS)市場規模、佔有率和成長分析(按產品類型、車輛類型、應用、最終用戶和地區分類)-2026-2033年產業預測 汽車用AHSS的印度市場評估:各種車型,用途類別,鋼類別,各地區,機會,預測(2019年度~2033年度)

汽車用AHSS的印度市場評估:各種車型,用途類別,鋼類別,各地區,機會,預測(2019年度~2033年度) 汽車先進高強度鋼市場,按產品類型、應用、車輛類型、銷售通路、國家及地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測汽車用AHSS的全球市場:各車輛類型,各應用類型,各鋼鐵等級,各地區,機會,預測,2018年~2032年

汽車先進高強度鋼市場,按產品類型、應用、車輛類型、銷售通路、國家及地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測汽車用AHSS的全球市場:各車輛類型,各應用類型,各鋼鐵等級,各地區,機會,預測,2018年~2032年