|

市場調查報告書

商品編碼

2061660

工業冷卻系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Industrial Refrigeration System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

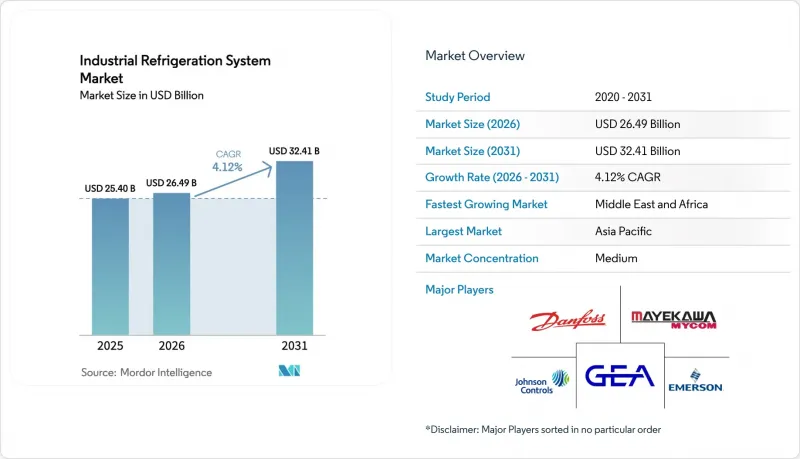

據 Mordor Intelligence 稱,2025 年工業冷卻系統市場價值為 254 億美元,預計到 2031 年將達到 324.1 億美元,而 2026 年為 264.9 億美元,預測期(2026-2031 年)的複合年成長率為 4.12%。

本報告依設備(壓縮機、冷凝器、蒸發器等)、冷媒(氨、二氧化碳等)、應用領域(食品飲料加工、冷凍物流等)、系統容量(小於100kW等)、系統類型(單級、雙級等)及地區分類。市場預測以美元計價。

全球工業冷卻系統市場趨勢與洞察

自動化低溫運輸倉庫的激增

自動化低溫運輸倉庫推動了對2兆瓦及以上氨製冷系統的需求,因為它們將處理量集中在少數幾個高容量樞紐,這些樞紐全天候在零下溫度下運作。主要廠商宣布的投資計畫也印證了這一趨勢,大規模冷凍食品設施需要更嚴格的溫度控制(±0.5°C),推動了多級壓縮和級聯系統的應用。亞洲食品電商的蓬勃發展進一步加速了現有設施的維修,物流業者紛紛採用變速螺桿壓縮機和物聯網賦能的蒸發器風扇。自動化倉庫起重機製造商也透過協調機械搬運和冷凍控制來設定更嚴格的溫度容差,以防止機器人表面出現冷凝水。因此,工業冷卻系統市場正經歷著專案價值的提升、長期服務合約的增加以及售後市場收入的成長。

對遵守氟化氣體法規和《基加利協定》的期限要求更加嚴格。

監管淘汰計劃正在縮短新型氫氟碳化合物(HFC)設備的使用壽命,從而推動向天然冷媒的轉型。歐盟目前強制要求到2030年將HFC的使用量減少95%,而美國將從2025年1月起禁止在新工業冷凍設備中使用HFC。洩漏追蹤的文件規定增加了管理成本,交付工廠預先充填且密封的氨和二氧化碳冷媒架更具吸引力。日本每噸二氧化碳當量3000日圓的碳價提高了HFC洩漏的直接成本,而罰款和處罰進一步增加了違規風險。這些政策的組合正在加速設備更換週期,從而推動工業冷卻系統市場的成長,儘管成熟經濟體的總裝置容量保持穩定。

天然冷媒產業面臨高額資本投入和技術純熟勞工短缺的問題。

由於採用不銹鋼熱交換器、增強型通風系統和冗餘安全聯鎖裝置等特性,天然冷媒冷凍設備的成本比同等規格的氫氟碳化合物(HFC)冷凍設備高成本%。此外,認證氨冷卻技術人員的供不應求,尤其是在北美地區,進一步加劇了預算壓力。北美地區的退休人數遠遠超出培訓學員人數。認證機構要求兩年以上的在職經驗,這導致人員招募速度放緩,計畫工期延長。美國主要大都會地區的人事費用已高達每小時150美元,這一額外成本延長了投資回收期,並減緩了中小企業的工業製冷系統的市場推廣。設備供應商正在推出工廠預製、撬裝式模組以減少現場施工,但人手不足在可預見的未來仍可能繼續阻礙專案進展。

細分市場分析

控制設備已成為工業冷卻系統市場中成長最快的細分領域。雖然壓縮機仍將保持其核心地位,預計到2025年將佔據36.18%的銷售佔有率,但可程式邏輯控制器(PLC)、變頻器和雲端控制面板預計到2031年將以4.93%的複合年成長率成長。這一成長反映了加州第24號修正案等法規的影響,該修正案強制要求在超過100千瓦的系統中整合需量反應。先進的驅動裝置可將壓縮機能耗降低高達50%,使設施業主能夠在18個月內收回投資。這種節能效果也將使一些延期項目得以實現,從而擴大工業冷卻系統市場的整體規模。冷凝器和蒸發器的發展落後於市場平均水平,因為其設計改進側重於傳熱效率的漸進式提升,而非效率的大幅提高。由於級聯式和跨臨界式系統設計中需要中間熱交換,接收器和熱交換器的需求量很大,導致每個裝置的物料清單 (BOM) 價值增加。控制設備供應商也將分析服務訂閱捆綁銷售,從而產生持續收入,穩定整個宏觀經濟週期中的收益。

數位化維修正日益成為現有工廠(棕地)的重點。成熟經濟體的營運商透過將新的驅動裝置和感測器套件與現有壓縮機結合,既能利用現有的硬體投資,又能從公用事業公司獲得能源補貼。這種組合提高了傳統資產的利用率,並使那些在商品價格波動中面臨融資困境的加工商受益。市場調查顯示,北美地區超過15年的老舊壓縮機中,預計有30%將在未來三年內需要進行控制系統升級,顯示售後市場具有巨大的成長潛力。硬體供應商正與IT平台合作,以確保網路安全合規性,並消除買家對勒索軟體的擔憂,這些擔憂先前阻礙了技術的普及。總而言之,隨著用戶對數據驅動效率的重視,控制和自動化領域的成長速度將持續超過整個工業冷卻系統市場。

氨冷媒憑藉其零全球暖化潛值 (GWP) 特性和在大型工廠中優異的動態性能,在 2025 年佔據了 42.41% 的裝機量。然而,超臨界二氧化碳 (CO2) 冷媒的設計正以 4.51% 的複合年成長率 (CAGR) 持續成長,直至 2031 年。歐洲已樹立了行業標桿,在超級市場和物流中心部署了數千個低填充量 CO2 冷媒架。隨著 2028 年監管合規期限的臨近,這種設計正逐步擴展到北美的物流中心。氫氟碳化合物 (HFC) 仍然用於需要超低溫環境且維修預算有限的地區,但監管障礙限制了新的 HFC 項目數量。碳氫化合物(主要是丙烷)在 50 千瓦以下的小規模系統中找到了市場,因為這些系統的可燃性風險可控。設備製造商透過提供雙冷媒平台來分散風險,使終端用戶能夠根據當地法規的變化更換冷媒。

受封裝標準化的推動,二氧化碳 (CO2) 工業冷卻系統市場規模正在擴大。供應商提供預製機架,其中包含氣體冷卻器和熱回收模組,無需現場特定設計,從而加快了試運行。案例研究表明,一家海鮮加工廠在從 R-507A 製冷系統切換到 CO2 增壓機架後,總能耗降低了 35%,這充分證明了 CO2 的價值。在氣候溫暖的地區,並聯壓縮和絕熱氣體冷卻器可以緩解 CO2 效率的下降,從而擴大其應用範圍。保險公司更傾向於為面向顧客的零售場所提供 CO2 冷凍系統的保險,而不是氨冷卻系統,這促使超級市場的規格清單轉向跨臨界設計。這些趨勢正在穩步推動 CO2 在更廣泛的工業冷卻系統市場中的應用。

區域分析

預計到2025年,亞太地區將佔工業冷卻系統市場銷售額的41.22%,主要得益於政府對低溫運輸改良和乳製品加工廠升級的補貼。中國500億元人民幣的農村低溫運輸計畫正在加速內陸省份氨庫的建設。印度的合作乳製品生產商提高了冷藏牛奶的產能,這些牛奶需要在兩小時內冷卻至4度C以下,而只有高效螺桿壓縮機才能實現這一目標。日本正著力於2025年HCFC禁令生效前對其R-22系統維修,而澳洲和紐西蘭則正以跨臨界CO2系統維修超級市場,以期在新店中徹底消除HFC的使用。東南亞水產品出口商正在增加其速凍生產線,預計2024年對越南和泰國的壓縮機出貨量將增加18%。這些項目共同推動該地區工業冷卻系統市場的擴張,其成長速度與人口成長帶來的食品需求成長速度相符。

預計中東和非洲地區的複合年成長率將達到5.23%,位居全球之首。糧食安全挑戰正推動連接港口與內陸樞紐的冷鏈物流走廊的發展。杜拜已累計5億美元在傑貝阿里附近新建10棟倉庫,每座倉庫都將配備適用於攝氏45度環境溫度的二氧化碳冷卻器。杜拜環球港務集團(DP World)投資2,900萬美元在埃及開設設施,以支持符合歐盟藥品良好分銷規範(GDP)的藥品進口,進而增強人們對該地區物流服務的信心。沙烏地阿拉伯的NEOM工業區正在投資建造一條氨低溫運輸,以支持垂直農業計畫;同時,馬士基及其當地合作夥伴正在利雅德建造一座10萬平方公尺的冷凍設施。自2025年1月起實施的洩漏報告要求正在加速天然冷媒的採用,刺激控制系統的升級,並推動海灣地區工業冷卻系統市場的發展。

北美和歐洲仍是科技潮流的領導者,相關法規加速了更新換代的進程。美國的《技術過渡規則》正在推動酪農產區的氫氟碳化合物(HFC)向氨的維修,而公共產業的補貼計劃則使變速驅動更具成本效益。歐洲修訂後的氟化氣體計畫意味著,62%的冷庫業主已將維修累計2027年的預算。儘管成長速度落後於新興地區,但高昂的單價仍使這些地區成為重要的收入來源。在南美洲,需求依然強勁,這得益於巴西在肉類出口領域的主導地位。 JBS運作85座氨廠,還有更多工廠正在興建中。非洲市場規模仍然小規模,但南非葡萄酒產業鏈和肯亞園藝產業中利基冷藏物流的需求表明,未來成長潛力巨大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 自動化低溫運輸倉庫的激增

- 對遵守氟化氣體法規和《基加利協定》的期限要求更加嚴格。

- 超低填充量氨氣(NH3)和二氧化碳(CO2)系統的快速普及

- 利用人工智慧進行預測性維護,降低生命週期成本

- 綠色氫氣工廠需要大規模冷卻

- 浸沒式冷卻資料中心對餘熱回收冷卻器的需求

- 市場限制因素

- 天然冷媒產業面臨高額資本投入和熟練勞動力短缺的問題。

- 鋼鐵和銅價的波動推高了設備成本。

- 物聯網連接冷凍系統的網路保險費

- 變頻壓縮機中稀土元素磁體的供應風險

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過裝置

- 壓縮機

- 冷凝器

- 蒸發器

- 熱交換器和熱接收器

- 控制與自動化

- 其他設備

- 透過冷媒

- 氨(R-717)

- 二氧化碳(R-744)

- 氫氟碳化合物(HFC/HFO)

- 碳氫化合物(丙烷、異丁烷)

- 透過使用

- 食品/飲料加工

- 冷凍與物流

- 化學品和製藥

- 石油和天然氣/液化天然氣

- 資料中心和電子產品

- 按容量分類的系統容量

- 小於100千瓦(小型)

- 100至1000千瓦(中等規模)

- 超過 1 兆瓦(大型)

- 依系統類型

- 單級壓縮

- 兩級壓縮

- 級聯和跨臨界

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Johnson Controls International plc

- Emerson Electric Co.

- GEA Group AG

- Danfoss A/S

- Mayekawa Mfg. Co., Ltd.

- Ingersoll Rand plc

- Carrier Global Corp.

- Daikin Industries Ltd.

- BITZER Kuhlmaschinenbau GmbH

- Star Refrigeration Ltd.

- Dover Corporation

- LU-VE Group

- Guntner GmbH and Co. KG

- EVAPCO, Inc.

- Alfa Laval AB

- Mitsubishi Heavy Industries Thermal Systems

- Baltimore Aircoil Company

- Industrial Frigo Srl

- Tecumseh Products Company

- Kirloskar Pneumatic Co. Ltd.

- SANDEN Holdings Corp.

- Bock GmbH

- Howden Group

- Frascold SpA

- Carnot Refrigeration

- Hillphoenix, Inc.

- Trane Technologies plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the industrial refrigeration system market size was valued at USD 25.40 billion in 2025 and is estimated to grow from USD 26.49 billion in 2026 to reach USD 32.41 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

This report is Segmented by Equipment (Compressors, Condensers, Evaporators, and More), Refrigerant (Ammonia, Carbon Dioxide, and More), Application (Food and Beverage Processing, Cold-Storage and Logistics, and More), System Capacity (Less Than 100 KW, and More), System Type (Single-Stage, Two-Stage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Refrigeration System Market Trends and Insights

Surge in Automated Cold-Chain Warehouses

Automated cold warehouses concentrate throughput in fewer, high-capacity hubs that operate around the clock at sub-zero temperatures, driving demand for ammonia systems sized above 2 megawatts. Investment announcements from major operators confirm the trend, with large frozen-food sites requiring tighter +-0.5 °C control that favours multi-stage compression and cascade architectures. Asian grocery e-commerce growth further accelerates retrofits, prompting logistics providers to add variable-speed screw compressors and IoT-ready evaporator fans. Manufacturers of automated storage and retrieval cranes also set stricter thermal tolerances, aligning mechanical handling with refrigeration controls to prevent condensation on robotics. As a result, the industrial refrigeration system market sees higher average project values and longer-term service contracts, lifting aftermarket revenue streams.

Tightening F-Gas and Kigali Compliance Deadlines

Regulatory phase-down schedules shorten the viable window for new HFC equipment, prompting a surge in natural-refrigerant conversions. The European Union now mandates a 95% cut in HFC use by 2030, while the United States bars HFCs from new industrial process refrigeration from January 2025. Documentation rules on leak tracking add administrative cost, favouring factory-packaged ammonia and CO2 racks that arrive pre-charged and hermetically tested. Financial penalties compound non-compliance risk, as Japan's carbon price of JPY 3,000 per ton of CO2-equivalent raises the direct cost of HFC leaks. This policy mix accelerates a replacement cycle that sustains industrial refrigeration system market growth even as total installed capacity stabilizes in mature economies.

High Capex and Skilled-Labor Scarcity for Natural Refrigerants

Natural-refrigerant plants cost 20%-40% more than HFC equivalents because of stainless-steel heat exchangers, enhanced ventilation, and redundant safety interlocks. Budget pressures are compounded by a shrinking pool of certified ammonia technicians, especially in North America where retirements outpace training enrolment. Certification bodies require two years of supervised field experience, delaying workforce replenishment and extending project schedules. Labor premiums reach USD 150 per hour in major U.S. metro areas, a surcharge that elongates payback periods and slows industrial refrigeration system market adoption in smaller enterprises. Equipment vendors respond with factory-built, skid-mounted modules that reduce on-site work, but labour scarcity will remain a near-term drag on project velocity.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Ultra-Low-Charge NH3 and CO2 Systems

- AI-Enabled Predictive Maintenance Lowering Lifecycle Cost

- Volatile Steel and Copper Prices Inflating Equipment Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Controls already represent the fastest-growing slice of the industrial refrigeration system market. Compressors retained a 36.18% revenue share in 2025, underscoring their central function, yet programmable logic controllers, variable-frequency drives, and cloud dashboards are climbing at a 4.93% CAGR to 2031. This expansion mirrors mandates such as California's Title 24 update that requires demand-response integration in systems capacity above 100 kilowatts. Advanced drives trim compressor energy by up to 50%, allowing site owners to recover investment within 18 months, and the energy savings improve the overall industrial refrigeration system market size by unlocking deferred projects. Condensers and evaporators trail the market average as their design advances focus on incremental heat-transfer gains rather than radical efficiency jumps. Receivers and heat exchangers gain traction because cascade and transcritical designs need intermediate heat exchange, adding bill-of-materials value per installation. Controls vendors also bundle analytics subscriptions, producing annuity revenue that stabilizes earnings across macro cycles.

Digital retrofits increasingly target brownfield plants. Operators in mature economies pair existing compressors with new drives and sensor kits, leveraging sunk hardware cost while capturing energy rebates from utilities. The pairing boosts legacy asset utilization, a benefit for cash-constrained processors navigating commodity price swings. Market surveys show 30% of installed compressors above 15 years old in North America are now candidates for control upgrades within three years, suggesting a sizable aftermarket runway. Hardware suppliers form alliances with IT platforms to ensure cybersecurity compliance, addressing buyer concerns over ransomware that previously stalled adoption. In aggregate, controls and automation will continue to outpace aggregate industrial refrigeration system market growth as users prioritize data-driven efficiency.

Ammonia held 42.41% of 2025 installations, buoyed by zero-GWP credentials and superior thermodynamic performance in large plants. Nevertheless, transcritical carbon dioxide designs are advancing at a 4.51% CAGR through 2031. Europe sets the standard, deploying thousands of low-charge CO2 racks in supermarkets and distribution hubs, yet uptake now spreads to North American distribution centers ahead of 2028 compliance deadlines. Hydrofluorocarbons linger in pockets that demand ultra-low temperatures or have limited retrofit budgets, but legislative barriers render new HFC projects marginal. Hydrocarbons, chiefly propane, capture niche demand in small systems capacity below 50 kilowatts where flammability risk is manageable. Equipment makers hedge bets by offering dual-refrigerant platforms, allowing end-users to switch refrigerants as local codes evolve.

The industrial refrigeration system market size attached to carbon dioxide expands on the back of packaging standardization. Vendors supply pre-engineered racks complete with gas coolers and heat reclaim modules, removing site-specific engineering and accelerating commissioning. Case studies record 35% total energy savings in seafood processing plants after switching from R-507A to CO2 booster racks, an outcome that bolsters the value narrative. In warmer climates, parallel compression and adiabatic gas coolers mitigate CO2 efficiency penalties, broadening feasible operating zones. Insurance carriers are more comfortable covering CO2 than ammonia in customer-facing retail spaces, a factor that tips supermarket specification lists toward transcritical designs. These dynamics ensure a widening footprint for carbon dioxide within the broader industrial refrigeration system market.

Geography Analysis

Asia Pacific accounted for 41.22% of 2025 revenue in the industrial refrigeration system market, reflecting government subsidies for cold-chain buildouts and dairy-processing upgrades. China's CNY 50 billion rural cold-chain scheme spurs ammonia warehouse construction in interior provinces. India's cooperative dairies added chilled-milk capacity requiring sub-4 °C cooling within two hours, a spec achievable only with high-efficiency screw compressors. Japan focuses on retrofitting R-22 systems ahead of its 2025 HCFC ban, while Australia and New Zealand roll out transcritical CO2 supermarket upgrades to fully remove HFCs from new stores. Southeast Asian seafood exporters boost blast-freezing lines, and compressor shipments to Vietnam and Thailand rose 18% in 2024. These projects combine to expand the regional industrial refrigeration system market size at a pace that matches population-driven food demand.

The Middle East and Africa have the highest forecast CAGR at 5.23%. Food security agendas fuel cold-storage corridors linking ports to inland hubs. Dubai earmarked USD 500 million for ten new warehouses near Jebel Ali, each designed with CO2 chillers suitable for 45 °C ambient conditions. DP World opened a USD 29 million facility in Egypt to serve pharmaceutical imports under EU Good Distribution Practice, adding credibility to regional logistics offerings. Saudi Arabia's NEOM zone invests in ammonia cold chain to back vertical farming schemes, while Maersk and local partners build a 100,000-square-meter refrigerated site in Riyadh. Leak-reporting mandates starting January 2025 accelerate natural-refrigerant adoption and pull in controls upgrades, reinforcing industrial refrigeration system market momentum across the Gulf.

North America and Europe remain technology trendsetters, with regulations sparking replacement cycles. The United States Technology Transitions Rule propels HFC-to-ammonia retrofits in dairy states, and utility rebates sweeten the payback for variable-speed drives. Europe's revised F-Gas plan has 62% of cold-store owners budgeting retrofits by 2027. While growth rates trail emerging regions, high unit values keep these continents significant revenue contributors. South America shows steady demand anchored in Brazil's meat-export dominance, and JBS runs 85 ammonia plants with more in build stage. Africa remains modest yet pockets in South Africa's wine chain and Kenya's floriculture add niche refrigerated logistics, pointing to future upside.

- Johnson Controls International plc

- Emerson Electric Co.

- GEA Group AG

- Danfoss A/S

- Mayekawa Mfg. Co., Ltd.

- Ingersoll Rand plc

- Carrier Global Corp.

- Daikin Industries Ltd.

- BITZER Kuhlmaschinenbau GmbH

- Star Refrigeration Ltd.

- Dover Corporation

- LU-VE Group

- Guntner GmbH and Co. KG

- EVAPCO, Inc.

- Alfa Laval AB

- Mitsubishi Heavy Industries Thermal Systems

- Baltimore Aircoil Company

- Industrial Frigo S.r.l.

- Tecumseh Products Company

- Kirloskar Pneumatic Co. Ltd.

- SANDEN Holdings Corp.

- Bock GmbH

- Howden Group

- Frascold S.p.A.

- Carnot Refrigeration

- Hillphoenix, Inc.

- Trane Technologies plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Automated Cold-Chain Warehouses

- 4.2.2 Tightening F-Gas and Kigali Compliance Deadlines

- 4.2.3 Rapid Adoption of Ultra-Low-Charge NH3 and CO2 Systems

- 4.2.4 AI-Enabled Predictive Maintenance Lowering Lifecycle Cost

- 4.2.5 Green-Hydrogen Plants Requiring Large-Scale Chilling

- 4.2.6 Demand from Immersion-Cooled Data Centres for Heat-Reuse Chillers

- 4.3 Market Restraints

- 4.3.1 High Capex and Skilled-Labour Scarcity for Natural Refrigerants

- 4.3.2 Volatile Steel and Copper Prices Inflating Equipment Costs

- 4.3.3 Cyber-Insurance Premiums for IoT-Linked Refrigeration Systems

- 4.3.4 Rare-Earth Magnet Supply Risk for VSD Compressors

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Equipment

- 5.1.1 Compressors

- 5.1.2 Condensers

- 5.1.3 Evaporators

- 5.1.4 Heat-Exchangers and Receivers

- 5.1.5 Controls and Automation

- 5.1.6 Others, Equipment

- 5.2 By Refrigerant

- 5.2.1 Ammonia (R-717)

- 5.2.2 Carbon Dioxide (R-744)

- 5.2.3 Hydro-Fluorocarbons (HFC/HFO)

- 5.2.4 Hydro-Carbons (Propane, Isobutane)

- 5.3 By Application

- 5.3.1 Food and Beverage Processing

- 5.3.2 Cold-Storage and Logistics

- 5.3.3 Chemicals and Pharmaceuticals

- 5.3.4 Oil and Gas / LNG

- 5.3.5 Data Centres and Electronics

- 5.4 By System Capacity

- 5.4.1 Less Than 100 kW (Small)

- 5.4.2 100 - 1,000 kW (Medium)

- 5.4.3 Greater Than 1 MW (Large)

- 5.5 By System Type

- 5.5.1 Single-Stage Compression

- 5.5.2 Two-Stage Compression

- 5.5.3 Cascade & Transcritical

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Johnson Controls International plc

- 6.4.2 Emerson Electric Co.

- 6.4.3 GEA Group AG

- 6.4.4 Danfoss A/S

- 6.4.5 Mayekawa Mfg. Co., Ltd.

- 6.4.6 Ingersoll Rand plc

- 6.4.7 Carrier Global Corp.

- 6.4.8 Daikin Industries Ltd.

- 6.4.9 BITZER Kuhlmaschinenbau GmbH

- 6.4.10 Star Refrigeration Ltd.

- 6.4.11 Dover Corporation

- 6.4.12 LU-VE Group

- 6.4.13 Guntner GmbH and Co. KG

- 6.4.14 EVAPCO, Inc.

- 6.4.15 Alfa Laval AB

- 6.4.16 Mitsubishi Heavy Industries Thermal Systems

- 6.4.17 Baltimore Aircoil Company

- 6.4.18 Industrial Frigo S.r.l.

- 6.4.19 Tecumseh Products Company

- 6.4.20 Kirloskar Pneumatic Co. Ltd.

- 6.4.21 SANDEN Holdings Corp.

- 6.4.22 Bock GmbH

- 6.4.23 Howden Group

- 6.4.24 Frascold S.p.A.

- 6.4.25 Carnot Refrigeration

- 6.4.26 Hillphoenix, Inc.

- 6.4.27 Trane Technologies plc

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工業製冷市場:2026-2032年全球市場預測(依組件、溫度範圍、容量、冷媒、終端用戶產業、銷售管道和安裝類型分類)

工業製冷市場:2026-2032年全球市場預測(依組件、溫度範圍、容量、冷媒、終端用戶產業、銷售管道和安裝類型分類) 工業製冷系統市場報告:按組件、冷媒類型、應用和地區分類(2026-2034 年)

工業製冷系統市場報告:按組件、冷媒類型、應用和地區分類(2026-2034 年) 工業冷凍市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝配置、設備

工業冷凍市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝配置、設備 全球集中式冷凍系統市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球集中式冷凍系統市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球工業冷凍系統市場報告2026年全球工業冷凍設備市場報告

2026年全球工業冷凍系統市場報告2026年全球工業冷凍設備市場報告 玻璃門冷藏櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年工業製冷系統市場-全球產業規模、佔有率、趨勢、機會及預測(依冷媒類型、設備類型、最終用戶產業、地區及競爭格局分類,2021-2031年預測)

玻璃門冷藏櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年工業製冷系統市場-全球產業規模、佔有率、趨勢、機會及預測(依冷媒類型、設備類型、最終用戶產業、地區及競爭格局分類,2021-2031年預測) 工業製冷市場規模、佔有率及成長分析(按組件、冷媒類型、應用及地區分類)-2026-2033年產業預測

工業製冷市場規模、佔有率及成長分析(按組件、冷媒類型、應用及地區分類)-2026-2033年產業預測 工業製冷系統市場規模、佔有率和成長分析(按組件、冷媒類型、應用、類型、銷售通路和地區分類)-2026-2033年產業預測

工業製冷系統市場規模、佔有率和成長分析(按組件、冷媒類型、應用、類型、銷售通路和地區分類)-2026-2033年產業預測