|

市場調查報告書

商品編碼

2061650

防霧添加劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Antifog Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

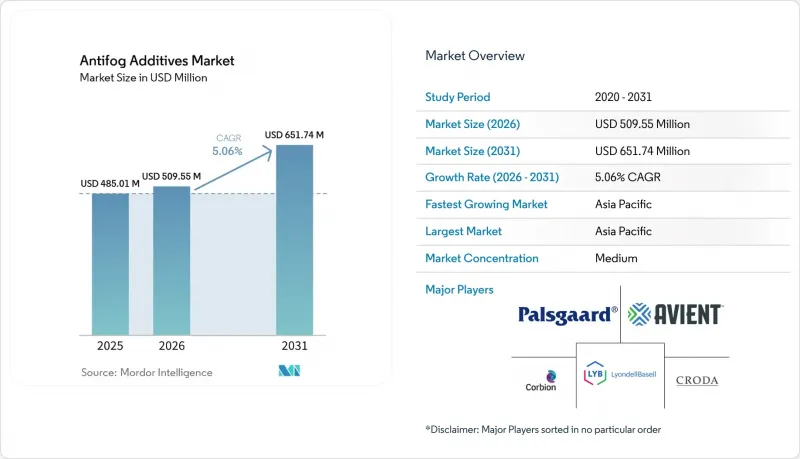

據 Mordor Intelligence 稱,防霧添加劑的市場規模預計在 2026 年達到 5.0955 億美元,高於 2025 年的 4.8501 億美元,預計到 2031 年將達到 6.5174 億美元。

預計 2026 年至 2031 年的複合年成長率為 5.06%。

本報告按類型(甘油酯、聚甘油酯、脂肪酸山梨醇酯及其他)、應用(農業薄膜、包裝薄膜及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球防霧添加劑市場趨勢及洞察

垂直農業向高透明度溫室薄膜過渡。

由於垂直農業依賴光學精度,冷凝控制是決定生產力的直接因素。中國的一項試驗表明,選擇先進的防霧膜可將太陽輻射透過率提高5.33%,從而提高產量和農民利潤。貝瑞世界(Berry World)的「Tufflite Infrared」薄膜就是一個典型的例子,它展示了防滴技術如何延長生長季並使其溢價合理。 [1] 隨著發光量子點薄膜的日益普及,冷凝干擾會阻礙波長調諧,從而形成一個良性循環:對透明度的需求、更高的價格以及對下一代添加劑的性能導向型需求。

單一材料軟性食品包裝需求激增

歐盟包裝和包裝廢棄物法規正推動包裝結構向可回收的單一材料結構轉變,從而淘汰了以往用於阻止添加劑遷移的傳統隔離層。印度塑膠協議下的Huta Maki指南指出,單一材料解決方案佔印度國內塑膠使用量的73%,擴大了符合法規要求的防霧解決方案在防霧添加劑市場的佔有率。 DNP集團的聚乙烯單一材料包裝袋需要使用能夠維持耐氧和耐水蒸氣性能的防霧化學品,同時不能影響分離效果或增加遷移風險。隨著年輕消費者越來越關注環保聲明,品牌越來越被迫選擇擁有永續永續性良好記錄的供應商。

加強 REACH 法規中關於食品接觸膜中酯類遷移的規定

歐盟法規 (EU) 2025/351 引入了新的純度標準和 NIAS 風險評估閾值。現在,對於食品中遷移量超過 0.00015 毫克/公斤的物質,需要提供大量的毒性數據,這導致測試成本增加和研發週期延長。歐洲食品安全局 (EFSA) 的模型顯示,在最壞情況下,聚甘油包裝的遷移量可能高達 50 毫克/公斤食品,這限制了設計的靈活性。不願承擔配方變更成本的供應商可能被迫在 2026 年 9 月的合規截止日期前退出市場,這將重塑防霧劑市場的競爭格局。

細分市場分析

甘油酯類產品已獲得監管機構和加工商數十年的認可,預計到2025年,其在防霧添加劑市場將佔據37.58%的佔有率。美國食品藥物管理局(FDA)的21 CFR 172.854以及世界衛生組織(WHO)可接受攝取量(ADI)(0-25毫克/公斤體重)均強調了其在食品包裝應用中的可靠性。然而,由於聚甘油酯具有優異的熱穩定性和低揮發性(實驗室擠出測試已證實),其市佔率正以5.65%的複合年成長率快速成長。

山梨醇酯被應用於一些對遷移特性有特殊要求的特殊聚合物系統。新興的生物基特種混合物旨在實現緩釋遞送,即使在溫度波動的情況下也能保持防霧性能。 Avient 的 Cesa 平台整合了這些化學技術,展示了智慧載體基質如何使薄膜在多次使用循環中保持透明度。

區域分析

在政府主導的農業現代化進程的支持下,亞太地區預計到2025年將以36.31%的市佔率引領防霧劑市場。中國的補貼政策正在擴大耕地面積,並刺激對添加可控防霧劑的高透明度溫室薄膜的投資。預計到2025年,印度的保護性栽培產量將激增至2.5億噸,這將支撐對防霧劑的長期需求。日本將於2025年6月生效的「正面表列」制度要求國產和進口薄膜在進入市場前必須通過嚴格的過渡性測試,這將消除技術壁壘並推高薄膜單價。

在北美,低溫運輸合規對於保障食品安全至關重要。 《食品安全現代化法案》(FSMA 204)強制要求在整個分銷管道中使用清晰易讀的標籤,而防霧處理並非可選項,而是合規成本。全球低溫運輸聯盟已將透明包裝窗口列為物流品質審核的關鍵績效指標(KPI)。

歐洲的法規環境瞬息萬變。根據歐盟法規 (EU) 2025/351,遵守 REACH 法規需要進行廣泛的 NIAS 評估並提高產品純度。雖然這會帶來短期成本,但也會為那些能夠記錄亞 ppm 級過渡行為的早期採用者帶來回報——這些早期參與企業通常是已經投資於分析能力的全球性跨國公司。預計南美、中東和非洲等新興市場將出現成長機會。秘魯和摩洛哥的溫室計畫正在試驗使用防滴漏膜,但由於監管差異和價格敏感性,推廣速度緩慢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 垂直農業中向高透明溫室薄膜的快速轉變

- 對單一材料軟性食品包裝的需求正在激增。

- 北美強制性低溫運輸標籤法規

- 主要供應商的生物基酯創新產品線

- 亞太地區防霧膜農業補貼計劃

- 市場限制因素

- 加強 REACH 法規中關於食品接觸膜中酯類遷移的規定

- 針對炎熱潮濕的赤道地區使用壽命短的問題,申訴。

- 單甘油和聚甘油原料價格波動

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 甘油酯

- 聚甘油酯

- 山梨醇脂肪酸酯

- 其他類型

- 透過使用

- 農業薄膜

- 包裝膜

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avient Corporation

- Corbion

- Croda International PLC

- Dupont

- Emery Oleochemicals

- Evonik Industries AG

- Guangzhou Cardlo biotechnology Co.,LTD

- High Grade Industries

- Kraton Corporation

- LyondellBasell Industries Holdings BV

- Palsgaard

- PCC Group

- Polyfill Technologies LLP

- Rapidmasterbatches

- Silibase Silicone

- Surya Masterbatches

- Taprath Elastomers LLP

- Tosaf

- ULTRA-PLAS CORPORATION

第7章 市場機會與未來展望

According to Mordor Intelligence, antifog additives market size in 2026 is estimated at USD 509.55 million, growing from 2025 value of USD 485.01 million with 2031 projections showing USD 651.74 million, growing at 5.06% CAGR over 2026-2031.

This report is Segmented by Type (Glycerol Esters, Polyglycerol Esters, Sorbitan Esters of Fatty Acids, Other Types), Application (Agricultural Films, Packaging Films, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Antifog Additives Market Trends and Insights

Shift to high-clarity greenhouse films in vertical farming

Vertical farming relies on optical precision, making condensation control a direct productivity lever. Chinese trials show that selecting advanced antifog films lifts solar radiation penetration by 5.33%, enhancing yields and farmer margins. Berry Global's Tufflite Infrared film illustrates how anti-drip chemistry lengthens growing seasons and justifies premium pricing[1]. As luminescent quantum-dot films gain traction, any fog interference diminishes wavelength tuning, creating a self-reinforcing cycle of clarity requirements, higher prices, and performance-driven demand in the antifog additives market for next-generation additives.

Surge in mono-material flexible food packaging demand

The EU Packaging & Packaging Waste Regulation propels a pivot toward recyclable mono-material structures, removing traditional barrier layers that previously contained additive migration. Huhtamaki guidance under the India Plastics Pact places mono-material solutions at 73% of national plastic use, widening the addressable base for compliant antifog solutions in the antifog additives market. DNP Group's polyethylene-only pouches maintain oxygen and water-vapor resistance, yet require antifog chemistries that neither hinder sorting nor raise migration risk. Younger consumers' scrutiny of environmental claims forces brands to pick suppliers with demonstrable sustainability credentials.

Tightening REACH limits on ester migration in food-contact films

Regulation (EU) 2025/351 introduces new purity standards and NIAS risk-assessment thresholds. Any migration above 0.00015 mg/kg food now demands extensive toxicological data, pushing up testing costs and elongating development timelines. EFSA modeling shows polyglycerol packages could migrate up to 50 mg/kg food under worst-case conditions, limiting design windows. Suppliers unwilling to fund reformulation face potential market exit by the September 2026 compliance deadline, reshaping competition in the antifog additives market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory cold-chain labeling regulations in North America

- Biobased ester innovation pipelines at key suppliers

- Short service-life complaints in hot-humid equatorial zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glycerol esters held 37.58% of antifog additives market share in 2025 owing to decades-long acceptance by regulators and processors. The FDA 21 CFR 172.854 and WHO ADI of 0-25 mg/kg body weight underpin confidence in food packaging use. However, polyglycerol esters are outpacing at 5.65% CAGR thanks to superior thermal stability and lower volatility, properties validated in lab extrusion studies.

Sorbitan esters service niche polymer systems where specific migration properties are needed. An emerging cluster of biobased specialty blends targets controlled-release delivery that sustains antifog performance under temperature swings. Avient's Cesa platform integrates these chemistries, demonstrating how smart carrier matrices can extend film clarity in multi-cycle use.

Geography Analysis

Asia-Pacific leads the antifog additives market with 36.31% share in 2025, underpinned by state-driven agricultural modernization. Chinese subsidy programs increase cropland scale, encouraging investments in high-clarity greenhouse films that feature controlled antifog agents. India's protected cultivation is jumping to 250 million tons output by 2025, sustaining long-term additive demand. Japan's Positive List system, active since June 2025, requires local and imported films to pass stringent migration tests before market entry, thereby lifting technical barriers and unit pricing.

North America relies on cold-chain compliance to maintain food safety. FSMA 204 requires legible labeling during the entire distribution channel, making antifog visibility a compliance cost rather than an optional upgrade. The Global Cold Chain Alliance lists clear pack windows as a KPI for logistics quality audits.

Europe is in regulatory flux. REACH alignment under Regulation (EU) 2025/351 calls for extensive NIAS assessments and purity upgrades. While that creates near-term cost burdens, it also rewards early movers capable of documenting migration behavior at sub-ppm levels-often the global multinationals already invested in analytic capacity. South America and Middle East & Africa provide greenfield growth opportunities. Government greenhouse programs in Peru and Morocco pilot anti-drip films, but fragmented regulations and price sensitivity keep adoption gradual.

- Avient Corporation

- Corbion

- Croda International PLC

- Dupont

- Emery Oleochemicals

- Evonik Industries AG

- Guangzhou Cardlo biotechnology Co.,LTD

- High Grade Industries

- Kraton Corporation

- LyondellBasell Industries Holdings B.V.

- Palsgaard

- PCC Group

- Polyfill Technologies LLP

- Rapidmasterbatches

- Silibase Silicone

- Surya Masterbatches

- Taprath Elastomers LLP

- Tosaf

- ULTRA-PLAS CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to high-clarity greenhouse films in vertical farming

- 4.2.2 Surge in mono-material flexible food packaging demand

- 4.2.3 Mandatory cold-chain labeling regulations in North America

- 4.2.4 Biobased ester innovation pipelines at key suppliers

- 4.2.5 Asia-Pacific agricultural subsidy programs for anti-fog films

- 4.3 Market Restraints

- 4.3.1 Tightening REACH limits on ester migration in food contact films

- 4.3.2 Short service-life complaints in hot-humid equatorial zones

- 4.3.3 Volatile mono- and poly-glycerol feedstock pricing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Glycerol Esters

- 5.1.2 Polyglycerol Esters

- 5.1.3 Sorbitan Esters of Fatty Acids

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Agricultural Films

- 5.2.2 Packaging Films

- 5.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Avient Corporation

- 6.4.2 Corbion

- 6.4.3 Croda International PLC

- 6.4.4 Dupont

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Guangzhou Cardlo biotechnology Co.,LTD

- 6.4.8 High Grade Industries

- 6.4.9 Kraton Corporation

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Palsgaard

- 6.4.12 PCC Group

- 6.4.13 Polyfill Technologies LLP

- 6.4.14 Rapidmasterbatches

- 6.4.15 Silibase Silicone

- 6.4.16 Surya Masterbatches

- 6.4.17 Taprath Elastomers LLP

- 6.4.18 Tosaf

- 6.4.19 ULTRA-PLAS CORPORATION

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

防霧添加劑市場:按類型、形態、製造流程、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測

防霧添加劑市場:按類型、形態、製造流程、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測 防霧添加劑市場規模、佔有率、成長和全球產業分析:按類型和應用、區域的洞察,2026-2034年的預測防霧膜及片材市場:依材料、塗層技術、厚度、終端用戶及通路分類-2026-2032年全球市場預測汽車除霧系統市場:按類型、車輛類型、技術、電源和分銷管道分類-2026-2032年全球預測

防霧添加劑市場規模、佔有率、成長和全球產業分析:按類型和應用、區域的洞察,2026-2034年的預測防霧膜及片材市場:依材料、塗層技術、厚度、終端用戶及通路分類-2026-2032年全球市場預測汽車除霧系統市場:按類型、車輛類型、技術、電源和分銷管道分類-2026-2032年全球預測 汽車除霧系統市場:依類型、組件、銷售管道、技術、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測霧化系統設備市場:按組件、部署方式、組織規模和最終用戶分類,全球預測,2026-2032年全球防霧添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

汽車除霧系統市場:依類型、組件、銷售管道、技術、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測霧化系統設備市場:按組件、部署方式、組織規模和最終用戶分類,全球預測,2026-2032年全球防霧添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球防霧塗料市場報告

2026年全球防霧塗料市場報告 防霧薄膜和片材市場規模、佔有率和成長分析(按材料類型、應用、技術和地區分類)-2026-2033年產業預測

防霧薄膜和片材市場規模、佔有率和成長分析(按材料類型、應用、技術和地區分類)-2026-2033年產業預測 防霧添加劑市場規模、佔有率及成長分析(按類型、應用和地區分類)-產業預測(2026-2033 年)

防霧添加劑市場規模、佔有率及成長分析(按類型、應用和地區分類)-產業預測(2026-2033 年)