|

市場調查報告書

商品編碼

2061532

亞太地區智慧鑰匙市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Smart Key - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

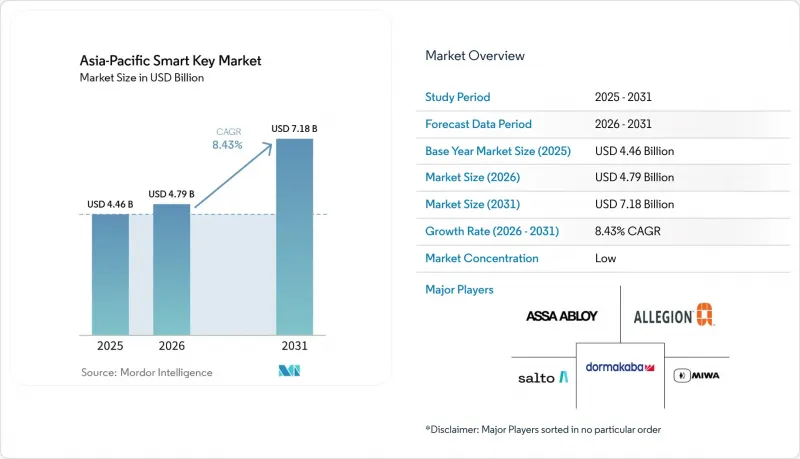

預計亞太地區智慧鑰匙市場規模將從 2025 年的 44.6 億美元成長到 2026 年的 47.9 億美元,到 2031 年將達到 71.8 億美元,2026 年至 2031 年的複合年成長率為 8.43%。

本報告按產品類型(智慧型汽車鑰匙、智慧門鑰匙及鎖具聯動認證、行動端鑰匙和虛擬鑰匙等)、技術(RFID、藍牙和BLE、NFC、Wi-Fi等)、認證方式(基於智慧型手機的存取等)、終端用戶產業(汽車、住宅、飯店等)和地區進行細分。市場預測以美元(USD)為單位。

亞太地區智慧鑰匙市場趨勢及洞察。

亞太地區都市區家庭對智慧家庭的接受度不斷提高。

在人口密集的都市區,智慧家庭的日益普及正在擴大整個全部區域住宅門禁系統的潛在市場。在開發人員、房東和物業經理能夠將門禁系統整合到更廣泛的數位化家居服務中,而非將其作為獨立設備銷售的領域,市場需求最為強勁。這加快了豪華公寓和專業管理物業的更新週期,同時也允許在新房屋建設過程中直接安裝。此外,能夠將門鎖、憑證、使用者權限和居住者支援整合到單一服務層級的品牌,其價值也隨之提升,而非僅依靠硬體價格競爭。在亞太地區智慧鑰匙市場,住宅需求正日益受到開發商和物業經理等機構投資者的影響,導致部署時間縮短,定價權轉移到平台主導供應商。這種轉變也有利於那些能夠在整個租賃期內提供持續憑證管理、遠端配置、訪客訪問和生命週期服務的供應商。

酒店業向非接觸式賓客訪問和移動鑰匙的轉型

該地區的飯店服務商正轉向非接觸式門禁,以減少對前台的依賴,並簡化客人抵達時的繁瑣流程。 2026年3月,三井不動產在其所有三井花園酒店和系列酒店品牌中推出了兼容Apple Wallet的房卡,該房卡採用Vingcard的雲端門禁管理系統「Vostio」和MIFARE 2GO認證資訊。這一發展表明,酒店不再孤立地評估門鎖,而是將認證資訊的分發、雲端編配以及與設施系統的兼容性納入考慮。基於錢包的門禁方式日益重要的另一個原因是,它降低了用戶下載專用應用程式和建立帳戶的門檻,從而消除了降低客人參與度的因素。在亞太智慧鑰匙市場,飯店的實施清楚地展現了行動認證的有效性,並有助於智慧型手機門禁在服務式公寓和企業設施等其他環境中普及。因此,能夠整合門禁硬體、身分驗證資訊發布和飯店工作流程軟體的供應商,在抓住酒店業下一波需求方面,具有更大的優勢。

高昂的初始維修和整合成本

高昂的維修和整合成本持續限制著智慧門鎖的廣泛應用,尤其是在老舊建築和小規模的物業組合中,這些場所往往沒有明確的智慧門禁預算。挑戰通常不僅限於門鎖本身,實施過程中可能還需要升級門禁系統、電力、網路、身分驗證流程以及本地服務基礎設施。在二、三線城市,這個問題尤其突出,因為這些地區的建築類型更加多樣化,承包商可能需要在實施前進行更多現場改造。持續的軟體成本也是一個關鍵因素,因為物業經理不僅要評估初始實施成本,還要評估管理多個地點眾多門禁系統的每月費用。因此,智慧門鎖的實施初期往往集中在新建築、豪華飯店、企業園區以及開發商主導的專案上,因為這些專案能夠容納整套軟體和服務。在亞太地區的智慧鑰匙市場,儘管用戶興趣日益濃厚且技術準備就緒,但這種成本結構限制了實際維修的範圍。

細分市場分析

預計到2025年,智慧汽車鑰匙將佔據亞太地區智慧鑰匙市場48.33%的佔有率,使汽車產業成為最大的產品細分市場,遙遙領先。這一領先地位反映了汽車製造商在遠端進入、防盜系統以及日益普及的智慧型手機數位存取工具方面的長期投資。到2025年底,CCC認證涵蓋了16家汽車製造商的產品,其中亞太地區的品牌佔據了穩固的地位。如此規模使得汽車產業獲得了最廣泛的應用記錄,並在供應商銷售量、檢驗參與度和生態系統知名度方面保持著核心地位。同時,其成熟度也自然限制了其超越其他認證類別的速度,因為汽車產業的成長仍然依賴車輛上市週期、供應商驗證週期和生產計畫。

預計到2031年,行動虛擬鑰匙的複合年成長率將達到9.03%,這表明在該大類產品中,軟體和錢包將成為主導其成長的主要動力。 Allegion宣布,到2026年,Aliro 1.0將建立一個標準化模型,用於在Apple、Google和Samsung錢包環境中實現行動憑證與讀卡機之間的通訊。智慧門鑰匙和鎖具整合認證方法仍然十分重要,因為住宅和商業建築是除汽車領域外應用最廣泛的領域。同時,智慧鑰匙圈、卡片和穿戴式裝置非常適合共用或臨時存取較為常見的機構工作流程。在亞太地區智慧鑰匙市場,這種構成比表明硬體出貨量將繼續保持廣泛,但商業性重點正在轉向軟體控制、認證的可移植性和持續的服務價值。因此,亞太地區智慧鑰匙產業的變革並非源自於新型鎖具形式的出現,而是源自於誰控制設備之上的認證層。

到2025年,RFID將在亞太地區智慧鑰匙市場佔據34.87%的佔有率,這反映了其在飯店門鎖、辦公門禁卡以及與交通運輸整合的身份驗證環境中長期存在的穩固地位。 RFID的強勢地位得以維持,原因在於營運商了解其工作流程,員工熟悉身份驗證資訊的發放方式,以及許多設施已部署讀卡器,導致快速更換成本高昂。從實際角度來看,這使得RFID在中型飯店、企業設施、公共設施和綜合用途建築中佔據了穩固的地位,因為在這些場所,可靠性比新穎性更為重要。在卡片式存取已十分普遍且更新周期較長的成熟環境中,已部署的基礎設施尤為重要。簡而言之,目前的技術轉型大多是透過混合配置實現的,而不是從現有的RFID基礎設施進行突然遷移。

預計到2031年,低功耗藍牙(BLE)將以9.43%的複合年成長率成長,並逐漸成為基於近距離感應和錢包主導的訪問體驗的首選技術層。汽車連線聯盟(CCC)已將數位鑰匙認證擴展到包括BLE和超寬頻(UWB),從而支援更流暢的免持使用和設備間互動場景。近場通訊(NFC)仍然是一個強大的輔助工具,因為基於輕觸的存取方式仍然熟悉且可靠。另一方面,Wi-Fi在遠端管理、配置和韌體更新方面仍然發揮著重要作用,但不再是主要的認證通道。在亞太地區智慧鑰匙市場,技術競爭正從單純的連接性聲明轉向更具可操作性的檢驗,重點關注互通性、讀卡器相容性、憑證傳輸以及整體用戶體驗品質。因此,亞太智慧鑰匙產業正朝著多重通訊協定架構發展,成功的供應商更有可能是那些能夠簡化營運商複雜性的供應商,而不是那些推廣單一無線標準的供應商。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區都市區家庭智慧家庭普及率不斷提高

- 酒店業向非接觸式賓客門禁和移動鑰匙過渡

- 企業對現有系統升級為基於雲端的存取控制的需求。

- 汽車製造商持續採用數位鑰匙進行聯網汽車技術

- 擴大共享居住、短期租賃和無人空間模式

- 推廣可審計的訪問日誌,以滿足保險和合規性要求。

- 市場限制因素

- 高昂的初始維修和整合成本

- 網路安全和憑證欺騙風險

- 房地產、電子錢包和汽車生態系統之間互通性的碎片化

- 一線城市以外地區的安裝公司和售後服務體係有差異

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 智慧汽車鑰匙

- 智慧門鑰匙和鎖整合認證訊息

- 移動和虛擬鑰匙

- 智慧鑰匙圈、卡片、穿戴設備

- 透過技術

- RFID

- 藍牙和低功耗藍牙

- NFC

- Wi-Fi

- 生物識別

- 身份驗證方法

- 透過智慧型手機存取

- 鑰匙圈門禁

- 使用鑰匙卡進入

- 小鍵盤和密碼訪問

- 透過生物識別進行訪問

- 按最終用戶行業分類

- 車

- 住宅

- 飯店業

- 企業及商業建築

- 工業和公共基礎設施

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ASSA ABLOY AB

- Allegion plc

- dormakaba Holding AG

- SALTO Systems, SL

- MIWA Lock Co., Ltd.

- ZKTeco Co., Ltd.

- igloohome Pte Ltd.

- U-tec Group Inc.

- OpenKey, Inc.

- Blockchain Lock Inc.

- KEYU Intelligence Co., Ltd.

- Nuki Home Solutions GmbH

- LOQED BV

- Latch, Inc.

- Kisi, Inc.

- Shenzhen Kaadas Intelligent Technology Co., Ltd.

- Guangdong Be-Tech Security Systems Co., Ltd.

- SimonsVoss Technologies GmbH

- Gantner Electronic GmbH

- Onity, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific smart key market size is expected to grow from USD 4.46 billion in 2025 to USD 4.79 billion in 2026 and is forecast to reach USD 7.18 billion by 2031 at 8.43% CAGR over 2026-2031.

This report is Segmented by Product Type (Smart Car Keys, Smart Door Keys and Lock-Linked Credentials, Mobile-Based and Virtual Keys, and More), Technology (RFID, Bluetooth and BLE, NFC, Wi-Fi, and More), Authentication Method (Smartphone-Based Access, and More), End-User Industry (Automotive, Residential, Hospitality, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Smart Key Market Trends and Insights

Rising Smart Home Penetration In Urban Asia-Pacific Households

Rising smart home adoption in dense urban areas is expanding the addressable market for residential access systems across the region. The strongest demand is emerging where developers, landlords, and managed rental operators can bundle access into the broader digital home offer rather than sell it as a standalone device purchase. This speeds up replacement cycles in premium apartments and professionally managed properties, while new construction enables more direct installation during construction. It also raises the value of brands that can tie locks, credentials, user permissions, and resident support into a single service layer, rather than competing solely on hardware price. In the Asia-Pacific smart key market, residential demand is increasingly shaped by institutional buyers such as developers and property managers, shortening rollout timelines and shifting pricing power toward platform-led vendors. That change also favors suppliers that can support recurring credential management, remote provisioning, visitor access, and lifecycle service over the full occupancy period.

Hospitality Shift Toward Contactless Guest Access And Mobile Keys

Hospitality operators across the region are moving toward contactless access because it reduces reliance on the front desk and removes friction at guest arrival. Mitsui Fudosan introduced Room Key in Apple Wallet across its Mitsui Garden Hotels and sequence hotel brands in March 2026 using Vingcard's Vostio cloud-based access management system and MIFARE 2GO credentials. This kind of rollout shows that hotels are no longer evaluating locks in isolation, because the real decision now includes credential delivery, cloud orchestration, and property system compatibility. Wallet-based entry also matters because it lowers the user barrier that comes with proprietary app downloads and account setup, which can slow guest participation. In the Asia-Pacific smart key market, hotel adoption has become a visible proof point for mobile credentials and is helping normalize phone-based access across other settings such as serviced apartments and enterprise spaces. Vendors that can link door hardware, credential issuance, and hotel workflow software are therefore better placed to capture the next phase of hospitality spending.

High Upfront Retrofit And Integration Costs

High retrofit and integration costs continue to limit broader deployment, especially in older buildings and smaller property portfolios that lack a clear budget for connected access. The challenge is usually broader than the lock itself, because deployment may also require upgrades to doors, power, networking, credential-issuance workflows, and local service capabilities. This is a larger problem in tier-2 and tier-3 cities, where building stock is more varied, and installers may need to make more site-level modifications before a rollout can begin. Recurring software fees also matter, because portfolio operators have to evaluate not only the first installation cost but also the monthly expense of managing many doors across several sites. As a result, adoption tends to concentrate first in new construction, premium hospitality, enterprise campuses, and developer-led projects that can absorb the full software and service stack. In the Asia-Pacific smart key market, this cost profile narrows the practical retrofit base, even as user interest and technology readiness both improve.

Other drivers and restraints analyzed in the detailed report include:

- Continued OEM Adoption of Connected Vehicle Digital Keys

- Enterprise Retrofit Demand For Cloud-Based Access Control

- Cybersecurity And Credential Spoofing Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart Car Keys held 48.33% of the Asia-Pacific smart key market share in 2025, which made automotive the largest product segment by a clear margin. That lead reflects the long history of OEM investment in remote entry, immobilizer-linked systems, and increasingly phone-based digital access tools. By the end of 2025, CCC certification covered products from 16 automakers, and APAC brands were firmly represented in that base. This scale gave the automotive segment the deepest installed footprint and kept it central to supplier volume, standards participation, and ecosystem visibility. At the same time, automotive growth remains tied to vehicle launch cycles, supplier validation windows, and production schedules, so its maturity imposes natural limits on how quickly it can outpace other credential categories.

Mobile-Based and Virtual Keys are forecast to grow at a 9.03% CAGR through 2031, pointing to a stronger software- and wallet-led growth path within the broader category. Allegion stated in 2026 that Aliro 1.0 creates a standardized model for mobile credentials and reader communication across Apple, Google, and Samsung wallet environments. Smart Door Keys and lock-linked credentials remain important because residential and commercial buildings provide the widest non-automotive installed base, while Smart Key Fobs, Cards, and Wearables still fit institutional workflows where shared or temporary access is common. In the Asia-Pacific smart key market, this mix suggests that hardware volume will remain broad, but the commercial center of gravity is moving toward software control, credential portability, and recurring service value. The Asia-Pacific smart key industry is therefore being reshaped less by the presence of a new lock format and more by who controls the credential layer that sits above the device.

RFID accounted for 34.87% of the Asia-Pacific smart key market in 2025, reflecting its long-established role in hospitality locks, office access cards, and transit-linked credential environments. Its position remains strong because operators understand the workflow, staff know how to issue credentials, and many sites already have readers that are expensive to replace quickly. In practical terms, this gives RFID a durable role across mid-market hotels, corporate facilities, institutional sites, and mixed-use buildings where reliability matters more than feature novelty. The installed base is especially relevant in mature environments where card-centric access has become routine, and replacement cycles are long. That means a large part of the current technology transition is happening through hybrid stacks rather than through abrupt migration away from existing RFID-supported infrastructure.

Bluetooth Low Energy is forecast to grow at 9.43% CAGR through 2031 and is becoming the preferred layer for proximity-based and wallet-driven access experiences. The Car Connectivity Consortium expanded Digital Key certification to include BLE and UWB, which supports more seamless hands-free and cross-device use cases. NFC still plays a strong supporting role because tap-based access remains familiar and dependable, while Wi-Fi continues to matter for remote management, provisioning, and firmware updates rather than as the main credential channel. In the Asia-Pacific smart key market, technology competition is shifting from basic connectivity claims to a more practical test that centers on interoperability, reader compatibility, credential handoff, and the overall quality of the user journey. The Asia-Pacific smart key industry is therefore moving toward multi-protocol architectures in which the most successful vendors are likely to be those that simplify complexity for operators rather than those that promote a single wireless standard.

List of Companies Covered in this Report:

- ASSA ABLOY AB

- Allegion plc

- dormakaba Holding AG

- SALTO Systems, S.L.

- MIWA Lock Co., Ltd.

- ZKTeco Co., Ltd.

- igloohome Pte Ltd.

- U-tec Group Inc.

- OpenKey, Inc.

- Blockchain Lock Inc.

- KEYU Intelligence Co., Ltd.

- Nuki Home Solutions GmbH

- LOQED B.V.

- Latch, Inc.

- Kisi, Inc.

- Shenzhen Kaadas Intelligent Technology Co., Ltd.

- Guangdong Be-Tech Security Systems Co., Ltd.

- SimonsVoss Technologies GmbH

- Gantner Electronic GmbH

- Onity, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Smart Home Penetration in Urban Asia-Pacific Households

- 4.2.2 Hospitality Shift Toward Contactless Guest Access and Mobile Keys

- 4.2.3 Enterprise Retrofit Demand for Cloud-Based Access Control

- 4.2.4 Continued OEM Adoption of Connected Vehicle Digital Keys

- 4.2.5 Expansion of Co-Living, Short-Stay Rentals, and Unmanned Space Formats

- 4.2.6 Insurance and Compliance Push for Audit-Ready Access Logs

- 4.3 Market Restraints

- 4.3.1 High Upfront Retrofit and Integration Costs

- 4.3.2 Cybersecurity and Credential Spoofing Risks

- 4.3.3 Fragmented Interoperability Across Property, Wallet, and Vehicle Ecosystems

- 4.3.4 Installer and After-Sales Capability Gaps Outside Tier-1 Cities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Smart Car Keys

- 5.1.2 Smart Door Keys and Lock-Linked Credentials

- 5.1.3 Mobile-Based and Virtual Keys

- 5.1.4 Smart Key Fobs, Cards, and Wearables

- 5.2 By Technology

- 5.2.1 RFID

- 5.2.2 Bluetooth and BLE

- 5.2.3 NFC

- 5.2.4 Wi-Fi

- 5.2.5 Biometric Authentication

- 5.3 By Authentication Method

- 5.3.1 Smartphone-Based Access

- 5.3.2 Key Fob-Based Access

- 5.3.3 Card Key-Based Access

- 5.3.4 Keypad and PIN-Based Access

- 5.3.5 Biometric-Based Access

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Residential

- 5.4.3 Hospitality

- 5.4.4 Enterprise and Commercial Buildings

- 5.4.5 Industrial and Public Infrastructure

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASSA ABLOY AB

- 6.4.2 Allegion plc

- 6.4.3 dormakaba Holding AG

- 6.4.4 SALTO Systems, S.L.

- 6.4.5 MIWA Lock Co., Ltd.

- 6.4.6 ZKTeco Co., Ltd.

- 6.4.7 igloohome Pte Ltd.

- 6.4.8 U-tec Group Inc.

- 6.4.9 OpenKey, Inc.

- 6.4.10 Blockchain Lock Inc.

- 6.4.11 KEYU Intelligence Co., Ltd.

- 6.4.12 Nuki Home Solutions GmbH

- 6.4.13 LOQED B.V.

- 6.4.14 Latch, Inc.

- 6.4.15 Kisi, Inc.

- 6.4.16 Shenzhen Kaadas Intelligent Technology Co., Ltd.

- 6.4.17 Guangdong Be-Tech Security Systems Co., Ltd.

- 6.4.18 SimonsVoss Technologies GmbH

- 6.4.19 Gantner Electronic GmbH

- 6.4.20 Onity, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment