|

市場調查報告書

商品編碼

2044287

永續電子商務包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Sustainable E-Commerce Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

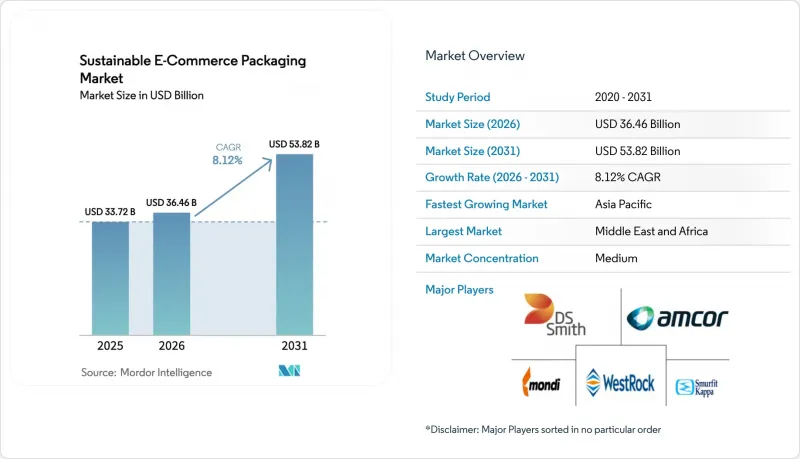

預計到 2025 年,永續電子商務包裝市場規模將達到 337.2 億美元,到 2026 年將達到 364.6 億美元,到 2031 年將達到 538.2 億美元,2026 年至 2031 年的複合年成長率為 8.12%。

針對一次性塑膠製品的監管壓力日益增大、線上訂單激增以及消費者對低碳材料的明顯偏好,正在加速推動末端配送領域對永續解決方案的需求。形態最佳化技術能夠降低體積重量費用,加上循環經濟經營模式的不斷擴展,正推動這些技術在早期採用者之外得到更廣泛的應用。紡織材料領域領導者的整合正在擴大其全球規模和研發預算,而人工智慧驅動的尺寸系統則為品牌所有者帶來了可觀的成本節約,並提高了投資回報率。

全球永續電子商務包裝市場趨勢與洞察

消費者偏好正轉向可回收和環保材料

那些真正致力於環境保護的品牌如今正獲得溢價和更高的客戶忠誠度。一份來自美容和個人護理品牌的報告顯示,61%的消費者會主動尋找具有環保意識的品牌,這推動了向再生材料(PCR)的轉變,與原生樹脂替代品相比,PCR可減少40%以上的碳足跡。因此,採用PCR既增強了收入的穩定性,也提升了品牌聲譽。零售商正在將PCR材料的強制使用範圍擴大到自有品牌產品,可回收性已成為多個線上類別的最低准入要求。各國政府也支持這一趨勢,計劃於2025年在歐盟實施強制性再生材料含量標準,從而提高對相容材料的基本需求。由此產生的連鎖反應正在加速對下一代纖維回收系統的投資,擴大高品質供應來源,並降低成本溢價。隨著轉換率的提高,早期採用者透過簽訂多年PCR材料供應合約來確保利潤率。

電子商務訂單量和最後一公里配送的爆炸性成長

隨著線上消費超越實體零售,各類防護包裝的需求都在增加。 Ranpak公司2024年第三季緩衝包裝銷售成長14.7%,淨銷售額成長11.4%,達9,220萬美元。亞馬遜96.7%可再生紙漿填充信封表明,纖維基解決方案符合跌落測試標準,並可整合到家庭垃圾收集系統中。這促使電商企業加速從塑膠包裝轉向紙質包裝,在成本效益和永續性方面獲益。與加工量相關的規模經濟進一步加劇了高強度、輕質且能在自動化運輸過程中承受穿孔的紙張的價格競爭。這一趨勢推動了對兼容主流回收製程的防潮塗層的需求成長,促進了加工商和化學品供應商之間的合作研發。隨著出貨頻率在高位趨於穩定,即使在大規模生產系統中也能保證品質穩定的包裝供應商正逐漸成為首選供應商。

供應鏈波動以及纖維和聚合物原料成本的波動

自2024年以來,箱板紙價格持續兩位數成長,主要受線上需求激增和能源成本飆升的推動,這給加工商的利潤率帶來了壓力。生物基樹脂的供應日益緊張,農產品價格的波動也波及到PLA和PHA的成本結構中。大規模一體化生產商透過自有林業資產和多年期買方合約來降低風險,而小規模加工商則面臨流動資金需求增加帶來的流動性風險。現貨價格的波動使品牌所有者的期貨定價更加複雜,導致合約續約延遲和新合約形式的開發放緩。因此,在價格不確定性日益加劇的情況下,那些能夠維持避險策略,直到原料短缺問題透過提高產能來緩解的成熟主要企業,暫時處於有利地位。

細分市場分析

由於紙張和紙板具有廣泛的可回收性、成本優勢和穩健的供應鏈,預計到2025年,它們將佔據永續電商包裝市場47.02%的佔有率。隨著甘蔗衍生聚乙烯、樹皮基薄膜和藻類塗層技術的日益成熟,預計到2031年,生質塑膠將以9.78%的最高複合年成長率成長。預計到2031年,生物生質塑膠永續電商包裝市場規模將達到93.2億美元,反映出食品和個人保健產品對更高阻隔性能的需求日益成長。紡織品製造商正試圖透過添加透過再製漿測試的防水分散體來保護其市場佔有率,而石化行業的成熟企業則正在投資化學回收的循環利用,以維持單一材料再生產品的效用。創業投資資金流入蛋白質基薄膜領域,顯示原料選擇範圍正在擴大,預計這將縮小與現有等級產品之間的價格差距。

預計到2025年,牛皮箱紙板和PLA之間的成本差異將縮小至20%以下,這將加速PLA在無需高透明度視窗的郵寄信封中的應用。致力於碳中和的品牌正依靠生命週期分析數據,這些數據表明,經認證的可堆肥薄膜結合工業堆肥的使用,是一種低排放的選擇。因此,企業採購部門正在將採購來源多元化,同時涵蓋傳統纖維材料和新興生物聚合物,以避免技術和監管風險。能夠在單一採購合約中同時提供這兩種基材的供應商將獲得談判優勢,並能確保在整個經濟週期中穩定的供應。

到2025年,瓦楞紙箱仍將維持其主導地位,佔據永續電商包裝市場72.10%的佔有率,這主要得益於其多功能性、承重能力以及成熟的回收系統。同時,郵寄袋和信封的複合年成長率(CAGR)為9.41%,人工智慧驅動的裝盒系統無需使用緩衝材料。隨著零售商採用通過跌落測試的易碎物品紙質緩衝材料,預計到2031年,郵寄袋的永續電商包裝市場規模將達到85.5億美元。更纖薄的包裝形式有利於配送中心,能夠提高輸送機的效率並減少拖車上的空間浪費。

零售商正將包裝多樣化與SKU層級的預測分析結合,以確保在不影響產品保護的前提下,選擇盡可能小的包裝尺寸。訂閱制電商企業更傾向於使用兼具行銷功能的印刷郵件,這加速了能夠經濟高效地處理小批量生產的數位印刷生產線的普及。雖然紙箱仍然是大型家電訂單的核心包裝,但如今的紙箱設計已融入了易撕封口和易撕回扣,以適應逆向物流流程。發泡內襯正在取代模壓紙漿結構,從而減少石油基材料的使用,並提高家庭回收率。

區域分析

到2025年,亞太地區將佔據永續電商包裝市場42.35%的佔有率。這主要得益於中國龐大的小包裹量以及印度電商零售市場持續兩位數的成長。在中國,一些地方政府將退稅與再生材料含量標準掛鉤,提振了出口型經銷商對消費後再生紙板(PCR)的需求。日本加工商率先採用整合近場通訊(NFC)標籤的智慧標籤技術,實現真偽驗證和低溫運輸預警。東南亞的履約中心正採用紙基保溫包裝取代EPS,以回應各國減少廢棄物的藍圖。預計到2031年,亞太地區永續電商包裝市場規模將超過236億美元,反映了當地紡織品和生物塑膠原料的生產。

中東和非洲的複合年成長率最高,達到9.66%,這主要得益於沿岸地區的全通路策略和非洲行動商務的快速成長。沙烏地阿拉伯的消費者調查顯示,消費者願意為環保包裝支付高達12%的附加費,促使當地加工商投資高產能瓦楞紙板生產設備,以取代進口產品。阿拉伯聯合大公國強制要求在2026年實現電子商務外包裝100%回收利用,提高了人們對輕質牛皮紙郵寄袋的需求。南非正利用其相對完善的回收基礎設施,試行推行纖維基隔熱襯墊的上門回收,從而將自身打造成為向撒哈拉以南非洲出口的樞紐。肯亞和盧安達的物流自由區正在吸引對自動化郵寄袋生產線的投資,以支持東非的跨境貿易。

北美和歐洲市場雖已成熟,但其影響力仍然強勁,透過擴大生產者責任制和引入塑膠稅,不斷塑造全球標準。歐盟的《包裝和包裝廢棄物條例》規定,到2030年,所有歐盟包裝材料必須可重複使用或可回收,促使紡織品製造商迅速改進包裝設計。美國品牌所有者預計,到2027年,至少有八個州將在全國範圍內推行生產者延伸責任制(EPR),並將收費系統納入其總成本模型。這些地區正在持續測試和運作高度複雜的解決方案,例如基於紡織品的溫控運輸容器和可向區塊鏈檢驗系統提供資訊的雲端連接追蹤標籤。這些經驗正在快速成長的新興市場中體現,加速全球向成熟的循環經濟框架的整合。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場定義與研究假設

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 消費者偏好正轉向可回收和環保材料

- 電子商務訂單量和最後一公里配送的爆炸性成長

- 全球對一次性塑膠製品的監管、禁令和環境稅

- 透過人工智慧驅動的智慧包裝箱尺寸選擇系統,降低體積重量收費。

- 零售商正擴大採用「包裝即服務 (PaaS)」模式。

- 範圍 3 碳排放報告迫使品牌追求低碳包裝。

- 市場限制因素

- 供應鏈波動以及纖維和聚合物原料成本的波動

- 特定生物基薄膜和塗層的阻隔性能局限性

- 互聯/可追溯包裝資料中的網路安全風險

- 多層軟郵件缺乏回收基礎設施

- 價值/供應鏈分析

- 重要法規結構的評估

- 對關鍵相關人員的影響評估

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 依材料類型

- 塑膠

- 紙張和紙板

- 金屬

- 生質塑膠

- 按包裝類型

- 瓦楞紙箱

- 信封和信封

- 收納袋

- 防護和絕緣解決方案

- 按最終用戶行業分類

- 時尚服飾

- 家用電器

- 飲食

- 製藥

- 個人護理和化妝品

- 永續

- 可回收

- 可堆肥

- 可重複使用的

- 可生物分解

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor PLC

- Smurfit Kappa Group PLC

- WestRock Company

- DS Smith PLC

- Sealed Air Corporation

- Mondi PLC

- International Paper Company

- Packman Packaging Private Limited

- Pinnacle Packing Industries LLC

- HB Fuller Company

- Ranpak Holdings Corporation

- Pregis LLC

- Stora Enso Oyj

- UPM-Kymmene Corporation

- EcoEnclose LLC

- Krones AG

- Sonoco Products Company

- AptarGroup Inc.

- Huhtamaki Oyj

- Veritiv Corporation

第7章 市場機會與未來趨勢

- 評估未開發的領域和未滿足的需求

The Sustainable E-Commerce Packaging Market size is projected to be USD 33.72 billion in 2025, USD 36.46 billion in 2026, and reach USD 53.82 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

Rising regulatory pressure on single-use plastics, surging online order volumes, and clear consumer preference for low-carbon materials are accelerating demand for sustainable solutions across last-mile delivery. Format optimization technologies that reduce dimensional weight fees, alongside expanding circular-economy business models, are broadening adoption beyond early movers. Consolidation among leading fiber-based players is improving global scale and R&D budgets, while AI-enabled right-sizing systems deliver measurable cost savings that reinforce payback arguments for brand owners.

Global Sustainable E-Commerce Packaging Market Trends and Insights

Shift in consumer preference toward recyclable and eco-friendly materials

Brands that prove real environmental commitment now secure price premiums and deeper loyalty. Beauty and personal-care labels report that 61% of shoppers actively seek eco-aligned brands, prompting conversions to post-consumer-recycled (PCR) substrates and achieving carbon-footprint cuts of more than 40% versus virgin resin alternatives. PCR uptake therefore builds both revenue resilience and reputational equity. Retailers are extending PCR mandates to private-label ranges, making recyclability a minimum entry requirement across multiple online categories. Governments reinforce the trend via mandatory recycled-content thresholds that take effect in the European Union in 2025, raising baseline demand for compatible materials. The resulting pull-through effect speeds investment in next-generation fiber recovery systems, widening quality supply and lowering cost premiums. As conversion volumes climb, early adopters protect margin by locking multiyear PCR feedstock agreements.

Explosive growth in e-commerce order volumes and last-mile deliveries

Online spending outpaces store-based retail, lifting protective-packaging requirements across categories. Ranpak logged a 14.7% rise in void-fill volumes in Q3 2024, with net sales up 11.4% to USD 92.2 million . Amazon's 96.7%-repulpable paper-padded mailer proves that fiber-based solutions can meet drop-test criteria and integrate into curbside streams. E-retailers subsequently accelerate plastic-to-paper shifts, capturing both cost efficiencies and sustainability gains. Volume-linked economies of scale widen price competitiveness for high-strength lightweight papers that resist puncture under automated handling. The trend raises demand for moisture-barrier coatings compatible with mainstream recycling processes, stimulating joint R&D between converters and chemical suppliers. As shipment frequency normalizes at a structurally higher base, packaging suppliers that guarantee consistent quality at scale consolidate preferred-supplier status.

Supply-chain volatility and fluctuating fiber / polymer input costs

Containerboard prices have posted double-digit jumps since 2024, propelled by surging online demand and energy-cost spikes, straining converters' margins. Bio-based resin supply is even tighter, with agricultural-commodity price swings feeding through to PLA and PHA cost structures. Large integrated producers mitigate exposure through captive forestry assets or multiyear buy-side contracts, but small converters face liquidity risk as working-capital needs inflate. Spot-price instability complicates forward-pricing for brand owners, delaying contract renewals and slowing new-format rollouts. Heightened price uncertainty therefore temporarily favors established incumbents that can underwrite hedging strategies until capacity additions ease feedstock tension.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven smart-box right-sizing systems reducing dimensional-weight fees

- Reusable packaging-as-a-service models gaining retailer adoption

- Barrier-property limitations of certain bio-based films and coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and paperboard accounted for 47.02% of the sustainable e-commerce packaging market in 2025 thanks to broad recyclability, cost advantages, and robust supply chains. Bioplastics register the fastest 9.78% CAGR to 2031 as sugarcane-derived PE, bark-based films, and algae coatings mature. The sustainable e-commerce packaging market size for bioplastics is projected to reach USD 9.32 billion by 2031, reflecting increased demand for higher barrier performance next to food and personal-care items. Fiber producers safeguard share by adding water-resistant dispersions that pass repulpability tests, while petrochemical incumbents invest in chemical-recycling back-loops to prolong the relevance of mono-material recyclables. Venture funding in protein-based films signals widening raw-material options poised to narrow price gaps with incumbent grades.

Cost differentials between kraft linerboard and PLA narrowed to under 20% in 2025, accelerating substitution in mailers that do not require high-clarity windows. Brands targeting carbon-neutral pledges lean on lifecycle-analysis data that position certified compostable films as a lower-emission choice when paired with industrial-compost access. Industrial procurement teams therefore split volumes across both fibers and emerging biopolymers to hedge technical and regulatory risk. Suppliers that can bundle both substrates within a single sourcing contract gain negotiating leverage and lock in throughput across economic cycles.

Corrugated boxes dominated at 72.10% of the sustainable e-commerce packaging market in 2025 on versatility, stacking strength, and a mature recycling stream. Mailers and envelopes, however, show a 9.41% CAGR on the strength of AI-assisted cartonization systems that eliminate void fill. The sustainable e-commerce packaging market size for mailers is forecast to hit USD 8.55 billion in 2031 as retailers deploy paper padded designs that meet fragile-item drop tests. Slim form factors benefit parcel hubs by lifting conveyor throughput and curbing trailer cube waste.

Retailers pair format diversification with SKU-level predictive analytics, ensuring the smallest feasible exterior is selected without compromising protective performance. Subscription-commerce brands prefer printed mailers that double as marketing real estate, accelerating adoption of digital-print lines that handle shorter runs economically. Boxes stay central for large consumer-electronics orders, yet box designs now integrate peel-and-seal closures and perforated returns strips to fit reverse-logistics workflows. Foam-in-place inserts give way to molded-pulp structures , cutting petroleum inputs and improving curbside recyclability.

The Sustainable E-Commerce Packaging Market Report is Segmented by Material Type (Plastic, Paper and Paperboard, Metal, Bioplastics), Packaging Format (Corrugated Boxes, Mailers and Envelopes, and More), End-User Industry (Fashion and Apparel, Consumer Electronics, and More), Sustainable Attribute (Recyclable, Compostable, Reusable, Biodegradable), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 42.35% of the sustainable e-commerce packaging market in 2025, buoyed by China's giant parcel volumes and India's double-digit e-retail expansion. Several provincial governments in China have tied tax rebates to recycled-content thresholds, boosting demand for PCR linerboard among export-oriented sellers. Japanese converters pioneer smart-label technologies that integrate NFC tags, enabling authenticity checks and cold-chain alerts. Southeast Asian fulfillment hubs adopt paper-based insulated shippers to replace EPS, aligning with national plastic-waste roadmaps. The sustainable e-commerce packaging market size in Asia-Pacific is projected to surpass USD 23.6 billion by 2031, reflecting localized production of both fiber and bio-resin inputs.

Middle East and Africa posts the fastest 9.66% CAGR, lifted by Gulf-region omnichannel initiatives and Africa's mobile-commerce surge. Saudi consumer surveys show willingness to pay up to 12% premiums for eco-friendly packaging, stimulating import substitution by regional converters installing high-throughput corrugators. The United Arab Emirates mandates 100% recyclability for e-commerce outer packs by 2026, propelling interest in lightweight kraft mailers. South Africa leverages comparatively robust collection infrastructure to pilot curbside separation of fiber-based insulated liners, positioning itself as a launchpad for sub-Saharan regional exports. Logistic free-zones in Kenya and Rwanda attract investment in automated mailer production lines that serve East-African cross-border trade.

North America and Europe remain mature but influential markets, shaping global standards through extended producer responsibility rules and plastic-tax rollouts. The European Union's Packaging and Packaging Waste Regulation requires all e-commerce packs to be reusable or recyclable by 2030, spurring rapid design iterations among fiber specialists. United States brand owners anticipate nationwide EPR passage in at least eight additional states by 2027, integrating fee schedules into total-cost models. These regions continue to pilot high-complexity solutions such as fiber-based active-temperature shippers and cloud-connected track-and-trace labels that feed blockchain verification systems. Lessons learned feed into fast-growing emerging markets, accelerating global convergence toward proven circular-economy frameworks.

- Amcor PLC

- Smurfit Kappa Group PLC

- WestRock Company

- DS Smith PLC

- Sealed Air Corporation

- Mondi PLC

- International Paper Company

- Packman Packaging Private Limited

- Pinnacle Packing Industries LLC

- H.B. Fuller Company

- Ranpak Holdings Corporation

- Pregis LLC

- Stora Enso Oyj

- UPM-Kymmene Corporation

- EcoEnclose LLC

- Krones AG

- Sonoco Products Company

- AptarGroup Inc.

- Huhtamaki Oyj

- Veritiv Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift in consumer preference toward recyclable and eco-friendly materials

- 4.2.2 Explosive growth in e-commerce order volumes and last-mile deliveries

- 4.2.3 Global regulatory bans and eco-taxes on single-use plastics

- 4.2.4 AI-driven smart box right-sizing systems reducing dimensional-weight fees

- 4.2.5 Reusable packaging-as-a-service (PaaS) models gaining retailer adoption

- 4.2.6 Scope-3 carbon reporting forcing brands to demand low-carbon packaging

- 4.3 Market Restraints

- 4.3.1 Supply-chain volatility and fluctuating fiber / polymer input costs

- 4.3.2 Barrier-property limitations of certain bio-based films and coatings

- 4.3.3 Cyber-security risks in connected / track-and-trace packaging data

- 4.3.4 Recycling-infrastructure gaps for multi-layer flexible mailers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Bioplastics

- 5.2 By Packaging Format

- 5.2.1 Corrugated Boxes

- 5.2.2 Mailers and Envelopes

- 5.2.3 Pouches and Bags

- 5.2.4 Protective/Insulative Solutions

- 5.3 By End-User Industry

- 5.3.1 Fashion and Apparel

- 5.3.2 Consumer Electronics

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals

- 5.3.5 Personal Care and Cosmetics

- 5.4 By Sustainable Attribute

- 5.4.1 Recyclable

- 5.4.2 Compostable

- 5.4.3 Reusable

- 5.4.4 Biodegradable

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Smurfit Kappa Group PLC

- 6.4.3 WestRock Company

- 6.4.4 DS Smith PLC

- 6.4.5 Sealed Air Corporation

- 6.4.6 Mondi PLC

- 6.4.7 International Paper Company

- 6.4.8 Packman Packaging Private Limited

- 6.4.9 Pinnacle Packing Industries LLC

- 6.4.10 H.B. Fuller Company

- 6.4.11 Ranpak Holdings Corporation

- 6.4.12 Pregis LLC

- 6.4.13 Stora Enso Oyj

- 6.4.14 UPM-Kymmene Corporation

- 6.4.15 EcoEnclose LLC

- 6.4.16 Krones AG

- 6.4.17 Sonoco Products Company

- 6.4.18 AptarGroup Inc.

- 6.4.19 Huhtamaki Oyj

- 6.4.20 Veritiv Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

永續包裝市場:按材料、永續性類型、應用和分銷管道分類-2026-2032年全球市場預測

永續包裝市場:按材料、永續性類型、應用和分銷管道分類-2026-2032年全球市場預測 永續快速消費品包裝市場預測至2034年-按包裝類型、材料類型、永續發展措施、應用和最終用戶分類的全球分析健康永續包裝市場:預測(至2034年)-按材料類型、包裝類型、包裝流程、應用、分銷管道、最終用戶和地區分類的全球分析

永續快速消費品包裝市場預測至2034年-按包裝類型、材料類型、永續發展措施、應用和最終用戶分類的全球分析健康永續包裝市場:預測(至2034年)-按材料類型、包裝類型、包裝流程、應用、分銷管道、最終用戶和地區分類的全球分析 永續產品市場規模、佔有率和成長分析:按產品類型、原料來源、價格範圍、認證類型、分銷管道、最終用戶細分市場和地區分類-2026-2033年產業預測永續包裝材料市場預測至2034年—按材料類型、包裝形式、技術、應用、最終用戶和地區分類的全球分析

永續產品市場規模、佔有率和成長分析:按產品類型、原料來源、價格範圍、認證類型、分銷管道、最終用戶細分市場和地區分類-2026-2033年產業預測永續包裝材料市場預測至2034年—按材料類型、包裝形式、技術、應用、最終用戶和地區分類的全球分析 永續材料市場:按材料類型、應用和地區分類可回收種植袋市場:按材料、應用、最終用戶、分銷管道和層數分類-2026-2032年全球市場預測

永續材料市場:按材料類型、應用和地區分類可回收種植袋市場:按材料、應用、最終用戶、分銷管道和層數分類-2026-2032年全球市場預測 2026年全球永續產品市場報告永續和環保材料市場預測至2034年:按材料類型、產品、技術、應用、最終用戶和地區分類的全球分析永續包裝市場:按材料、製造程序、終端用戶產業和地區分類

2026年全球永續產品市場報告永續和環保材料市場預測至2034年:按材料類型、產品、技術、應用、最終用戶和地區分類的全球分析永續包裝市場:按材料、製造程序、終端用戶產業和地區分類