|

市場調查報告書

商品編碼

2044263

中國無機碘化物市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China Inorganic Iodide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

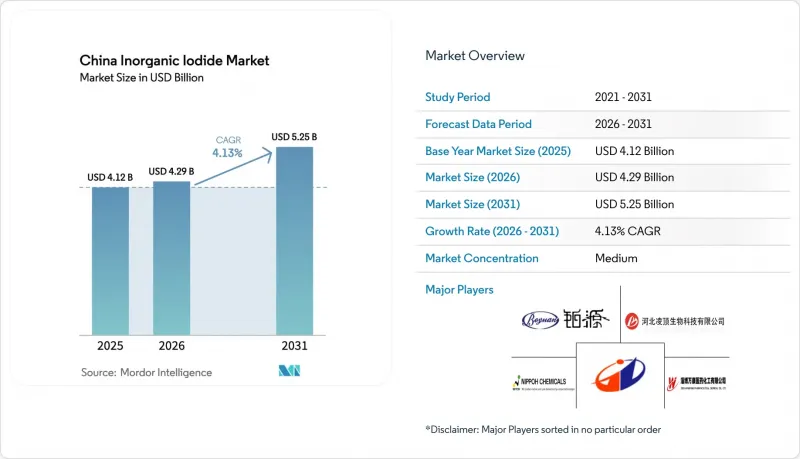

中國無機碘化物市場預計將從 2025 年的 41.2 億美元和 2026 年的 42.9 億美元成長到 2031 年的 52.5 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.13%。

此次擴張主要受醫藥產業對碘化鉀的需求、支持光學級碘化物的顯示面板獎勵的轉變以及政府補充核災應急藥品等因素驅動。國內加工企業控制全球20%的原料藥產量和約80%的上游工程關鍵原料,因此能夠有效應對原料價格波動,同時維持渤海灣地區和長三角化工園區的運轉率。結構性不利因素包括碘採購嚴重依賴智利、液晶顯示器向有機Delta二極體顯示器的轉變以及更嚴格的環保標準迫使小規模工廠搬遷或關閉。目前,國內現貨價格受庫存週期的影響大於原物料價格波動,凸顯了完善的營運資金管理和長期供應合約的重要性。

中國無機碘化物市場趨勢與洞察

原料藥產量激增,帶動了中國醫藥產業叢集對碘化物的需求。

位於山東和江蘇兩省化工園區的加工企業受益於完善的公用設施和中國現行的監管優勢,中國擁有18%的歐洲藥典(EP)認證。這確保了碘化鉀和氫碘酸的價格與原料藥藥(API)的成長掛鉤,而非與GDP掛鉤。儘管由於2024年取消了部分發酵原料的退稅政策,成本有所上升,但由於造影劑和甲狀腺藥物能夠吸收價格波動,利潤率依然穩健。因此,即使通用碘化物的需求下降,高純度碘化物受需求波動的影響也較小。

工業飼料廠的擴張促進了碘強化飼料預混合料的使用。

動物營養領域約佔全球碘消耗量的7%,隨著食鹽減量宣傳活動導致膳食碘攝取量下降,比例正在擴大。在農業部殘留物標準的推動下,山東和河南兩省的飼料廠正從使用粗添加劑轉向使用藥用級碘化鉀,該標準優先考慮通過ISO 9001認證的供應商。儘管由於預混合料合約續約緩慢,銷售量的成長需要幾個季度才能實現,但畜牧場的整合正在推動中國無機碘化物市場持續繁榮發展。

與健康相關的副作用導致最大劑量限制收緊。

世界衛生組織更新的禁忌症強調了老年人甲狀腺健康的風險,促使中國監管機構對消費品中的碘含量進行調查,並可能將某些碘化物列為重點管制物質。江蘇省的污染物控制計畫包括審計和逐步淘汰環節,這將增加中小加工企業的合規成本。擁有全面毒理學數據和ISO 9001認證的企業能夠維持市場准入,而不符合標準的工廠則面臨被淘汰的風險,這可能會略微減緩中國無機碘化物市場的複合年成長率。

細分市場分析

截至2025年,碘化鉀將佔中國無機碘化物市場38.76%的佔有率,主要受甲狀腺治療、飼料強化和民防錠劑等需求的推動。氫碘酸預計到2031年將以5.18%的複合年成長率成長,主要受乙酸羰基化催化劑和石墨烯還原技術的推動,可望進一步提升其在中國無機碘化物市場的佔有率。碘化鈉、碘酸鉀、碘化鋰和碘化銀則主要應用於閃爍晶體和人工降雨劑等細分領域。純度是決定性因素。超高純度產品的價格是標準產品的3到5倍,即使大宗價格下跌也能保障利潤。

第二代催化還原和電滲析純化技術可降低環境影響,滿足江蘇省污染物排放法規要求,使合規加工商能夠在不超標排放標準的情況下提高產量。這些技術還能減少含硫廢棄物和重金屬殘留,提升跨國製藥買家所要求的ESG(環境、社會和治理)指標,並促進中國無機碘化物進口市場的發展。

中國無機碘化物市場按產品(碘化鉀、碘化鈉、碘酸鉀、氫碘酸等)和應用(動物飼料和營養補充劑、藥品和醫療產品、光學偏光片、工業化學品等)進行細分。本報告提供上述所有細分市場中國無機碘化物市場的市場規模和預測(以金額為準)。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 原料藥產量的激增正在推動中國醫藥產業叢集對碘化物的需求。

- 工業飼料廠的擴張增加了對碘強化飼料預混合料的需求。

- 儲備碘化鉀片以應對核能緊急情況。

- KI熱穩定劑在中國尼龍和工程塑膠產業的應用日益廣泛

- 政府對液晶顯示器製造廠的獎勵促進了碘化物在偏光片。

- 市場限制因素

- 由於可能存在健康方面的副作用,使用上限已收緊。

- 進口碘價格的波動給生產商的利潤率帶來了壓力。

- 從液晶顯示器 (LCD) 向有機發光二極體 (OLED) 的轉變導致顯示器產業對碘化物的需求下降。

- 價值鏈分析

- 監管分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品

- 碘化鉀

- 碘化鈉

- 氫碘化物

- 碘酸鉀

- 其他產品

- 透過使用

- 飼料和營養保健品

- 藥品和醫療保健

- 光學偏光片

- 工業化學品

- 其他用途

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AJAY SQM

- Deep Water Chemicals

- Godo Shigen Co., Ltd

- Hebei Lingding Biotechnology Co., Ltd

- Hebei Yime New Material Technology Co., Ltd

- Independent Iodine China Ltd

- Jiangsu Kaihuida New Material Technology Co., Ltd

- Jiangxi Shengdian S&T Co., Ltd

- Merck KGaA

- Nanjing Taiye Chemical Industry Co., Ltd.

- Nippoh Chemicals Co., Ltd

- Qingdao Gimhae Iodide Chemical Co., Ltd

- Shandong Boyuan Pharmaceutical & Chemical Co., Ltd

- Sqm SA

- Tai'an Havay Group Co., Ltd.

- Toho Earthtech, Inc.

- Zibo Anquan Chemical Co., Ltd.

- Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

第7章 市場機會與未來展望

The China Inorganic Iodide Market size is projected to expand from USD 4.12 billion in 2025 and USD 4.29 billion in 2026 to USD 5.25 billion by 2031, registering a CAGR of 4.13% between 2026 and 2031.

Expansion is paced by pharmaceutical demand for potassium iodide, the migration of display-panel incentives that support optical-grade iodides, and government restocking of nuclear-preparedness tablets. Upstream control of 20% of global API output and about 80% of key starting materials keeps domestic converters well placed to absorb feedstock volatility while maintaining capacity utilization at chemical parks along the Bohai Rim and the Yangtze River Delta. Structural headwinds stem from Chile-centric iodine sourcing, LCD-to-OLED substitution, and tighter environmental standards that pressure smaller plants to relocate or shut down. Inventory cycles rather than feedstock swings currently drive domestic spot prices, underscoring the importance of working-capital discipline and long-term supply contracts.

China Inorganic Iodide Market Trends and Insights

Surging API Output Fueling Iodide Demand in China's Pharma Clusters

Converters anchored in Shandong and Jiangsu chemical parks benefit from integrated utilities and regulatory moats created by China's 18% share of European Pharmacopoeia certificates, ensuring that potassium iodide and hydroiodic acid track API growth rather than GDP. The removal of tax rebates on certain fermentation feedstocks in 2024 raised costs, yet margin resilience persists because contrast media and thyroid drugs absorb price swings. High-purity iodides therefore enjoy demand insulation when commodity grades soften.

Expansion of Industrial Feed Mills Boosting Iodide-Fortified Feed Premixes

Animal nutrition accounts for roughly 7% of global iodine use and gains ground as salt-reduction campaigns lower dietary iodine intake. Consolidating feed mills in Shandong and Henan are shifting from crude additives to pharmaceutical-grade potassium iodide, backed by Ministry of Agriculture residue limits that favor ISO 9001-certified suppliers. Because premix contracts turn over slowly, volume growth materializes over multiple seasons, yet intensified livestock farming locks in a durable vibration for the China Inorganic Iodide market.

Health-Related Side-Effects Triggering Tighter Use-Level Caps

WHO's updated contraindications highlight thyroid risks among the elderly, prompting Chinese regulators to examine consumer-goods iodine content and possibly list certain iodides as priority-control substances. Jiangsu's draft pollutant plan outlines audits and potential phase-outs, raising compliance costs for smaller converters. Firms holding comprehensive toxicology files and ISO 9001 certification are positioned to retain access, while non-compliant plants risk exit, shaving a fraction from the China Inorganic Iodide market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Re-stocking of KI Tablets for Nuclear-Emergency Preparedness

- Rising Adoption of KI Heat Stabilizers in China's Nylon and Engineering Plastics

- Volatile Imported Iodine Prices Squeezing Producer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Potassium iodide held 38.76% China Inorganic Iodide market share in 2025, capturing demand from thyroid treatments, feed fortification, and civil-defense tablets. Hydroiodic acid is projected to rise at a 5.18% CAGR through 2031 on the back of acetic-acid carbonylation catalysts and graphene reduction, pushing its slice of the China inorganic iodide market size upward. Sodium iodide, potassium iodate, lithium iodide, and silver iodide together fill niche segments such as scintillator crystals and cloud-seeding agents. The decisive factor is purity: ultra-high-grade lots command 3-5 times commodity pricing, shielding earnings when bulk prices weaken.

Second-generation catalytic reduction and electrodialysis purification lower environmental overhead and match Jiangsu pollutant-governance demands, allowing compliant converters to raise output without breaching discharge limits. Because these technologies cut sulfur waste and heavy-metal residues, they also improve ESG profiles sought by multinational pharma buyers, reinforcing the stickiness of imports from the China Inorganic Iodide market.

The China Inorganic Iodide Market is Segmented by Product (Potassium Iodide, Sodium Iodide, Potassium Iodate, Hydroiodic Acid, and Other Products) and by Application (Animal Feed and Nutraceuticals, Pharmaceuticals and Medical, Optical Polarizing Films, Industrial Chemicals, and Other Applications). The Report Offers Market Size and Forecasts for the China Inorganic Iodide Market in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- AJAY SQM

- Deep Water Chemicals

- Godo Shigen Co., Ltd

- Hebei Lingding Biotechnology Co., Ltd

- Hebei Yime New Material Technology Co., Ltd

- Independent Iodine China Ltd

- Jiangsu Kaihuida New Material Technology Co., Ltd

- Jiangxi Shengdian S&T Co., Ltd

- Merck KGaA

- Nanjing Taiye Chemical Industry Co., Ltd.

- Nippoh Chemicals Co., Ltd

- Qingdao Gimhae Iodide Chemical Co., Ltd

- Shandong Boyuan Pharmaceutical & Chemical Co., Ltd

- Sqm S.A.

- Tai'an Havay Group Co., Ltd.

- Toho Earthtech, Inc.

- Zibo Anquan Chemical Co., Ltd.

- Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging API output fuelling iodide demand in China's pharma clusters

- 4.2.2 Expansion of industrial feed mills boosting iodide-fortified feed premixes

- 4.2.3 Re-stocking of KI tablets for nuclear-emergency preparedness

- 4.2.4 Rising adoption of KI heat stabilisers in China's nylon and engineering plastics

- 4.2.5 Government incentives for LCD fabs sustaining polarising-film iodide consumption

- 4.3 Market Restraints

- 4.3.1 Health-related side-effects triggering tighter use-level caps

- 4.3.2 Volatile imported iodine prices squeezing producer margins

- 4.3.3 LCD-to-OLED migration eroding iodide demand from display sector

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Potassium Iodide

- 5.1.2 Sodium Iodide

- 5.1.3 Hydroiodic Acid

- 5.1.4 Potassium Iodate

- 5.1.5 Other Products

- 5.2 By Application

- 5.2.1 Animal Feed and Nutraceuticals

- 5.2.2 Pharmaceuticals and Medical

- 5.2.3 Optical Polarizing Films

- 5.2.4 Industrial Chemicals

- 5.2.5 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AJAY SQM

- 6.4.2 Deep Water Chemicals

- 6.4.3 Godo Shigen Co., Ltd

- 6.4.4 Hebei Lingding Biotechnology Co., Ltd

- 6.4.5 Hebei Yime New Material Technology Co., Ltd

- 6.4.6 Independent Iodine China Ltd

- 6.4.7 Jiangsu Kaihuida New Material Technology Co., Ltd

- 6.4.8 Jiangxi Shengdian S&T Co., Ltd

- 6.4.9 Merck KGaA

- 6.4.10 Nanjing Taiye Chemical Industry Co., Ltd.

- 6.4.11 Nippoh Chemicals Co., Ltd

- 6.4.12 Qingdao Gimhae Iodide Chemical Co., Ltd

- 6.4.13 Shandong Boyuan Pharmaceutical & Chemical Co., Ltd

- 6.4.14 Sqm S.A.

- 6.4.15 Tai'an Havay Group Co., Ltd.

- 6.4.16 Toho Earthtech, Inc.

- 6.4.17 Zibo Anquan Chemical Co., Ltd.

- 6.4.18 Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment