|

市場調查報告書

商品編碼

2044241

歐洲停車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe Car Parking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

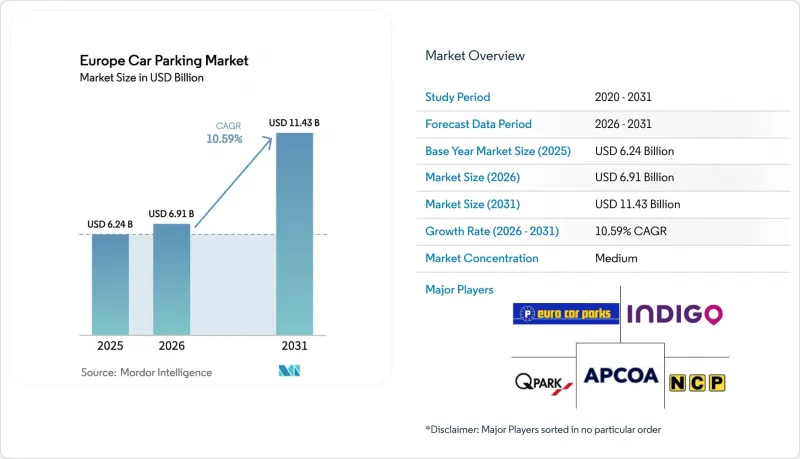

歐洲停車市場預計將從 2025 年的 62.4 億美元和 2026 年的 69.1 億美元成長到 2031 年的 114.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 10.59%。

這種快速擴張反映了空間分配模式從被動式向數據驅動的電氣化資產的轉變,市政當局和私營運營商正將這些資產定位為城市交通戰略的核心要素。自動駕駛和充電基礎設施(AFIR)主導的維修項目、國際觀光恢復到疫情前水平,以及無現金、感測器驅動的路邊停車區域的部署,都增強了運營商的定價能力,並創造了新的收入來源,例如V2G(車輛到電網)聚合。隨著傳統停車場業主尋求透過長期特許經營協議和收購充電網路來維持市場佔有率,競爭日益激烈,而數位化優先的平台則將閒置的住宅和商業空間轉化為可預訂的停車位。能夠將實體容量與預測分析結合的營運商,最能掌握由電子商務微型倉配和電動車普及所帶來的日益成長的需求。

歐洲停車市場趨勢與洞察

擴大停車場強制電動車充電範圍

歐洲停車指令 (AFIR) 規定,所有擁有超過 20 個停車位的歐洲停車場必須至少配備一個充電樁,該規定已於 2024 年生效。各國的具體要求進一步強化了這一影響;例如,德國的 GEIG 法案要求新建的非住宅建築必須預先安裝充電樁線路,且每五個停車位中至少有一個必須預留充電樁線路。這項法規加速了停車場業主與 Allego 和 Fastned 等充電樁專家之間的合作。這種合作模式使營運商能夠分擔資本支出,同時也能獲得能源服務收入。烏得勒支一項包含 500 輛電動車的 V2G(車輛到電網)試點計畫表明,停放的電動車可以在晚高峰時段發電,從而建立了一種停車時間貨幣化的模式。由於實施日期有所延遲——法國將維修期限延長至 2027 年,瑞典則將目標提前至 2025 年——這正在逐步引發採購需求,並將在未來十年內惠及承包商和設備製造商。

城市旅遊業和遊客數量的恢復

2024年,國際旅客數量超過了2019年的水平,歷史中心和交通樞紐再次出現擁擠。馬德里-巴拉哈斯機場等機場開始實施每15分鐘漲價的停車費,預計到2026年第一季,每個停車位的收入將增加12%。零售商試圖透過停車費補貼來維持客流量,但諷刺的是,在巴塞隆納和阿姆斯特丹,儘管需求不斷成長,但由於當地法規減少了路邊停車位,停車位供應卻十分緊張。各地區的復甦速度不盡相同,但整體而言,旅遊路線的停車費都面臨上漲的壓力。

維修電動車相容基礎設施成本高昂

許多2010年以前建造的多層停車場缺乏足夠的變壓器容量來支援多個快速充電樁,這迫使人們進行成本高昂的電網升級,並可能導致工程延長長達18個月。儘管義大利和西班牙的津貼計畫可以覆蓋高達40%的資本支出,但它們也面臨申請量激增和程序繁瑣等挑戰。由於入住率不穩定,區域城市小規模地面停車場的業主難以獲得維修資金。 AFIR要求整合軟體以實現即時價格顯示和非接觸式支付,這給現有的票務系統帶來了額外的負擔。

細分市場分析

P2P平台正在將分散的閒置空間數位化,使業主能夠在夜間和週末將車位變現。到2025年,歐洲停車市場中,傳統停車業者佔據46.23%的市場佔有率,但平台業者正以每年11.26%的速度成長,兩者之間的差距正在縮小。傳統業者依賴市政當局授予的長期營運權,但用戶越來越傾向於使用基於應用程式的預訂方式,這種方式的價格最多可比標價低30%。基礎設施供應商提供的整合API允許現有營運商對其應用程式進行白牌,模糊了不同類別之間的界限。由於監管體系尚不完善,合規性問題依然存在。有些城市將P2P收入歸類為課稅商業活動,而有些城市則將其視為財產的附帶使用。

其次,資產密集型業者正擴大採用動態定價,試圖效法數位競爭對手所享有的需求彈性優勢。 JustPark 預計到 2025 年註冊車位將超過 200 萬個,這表明住宅車道和未充分利用的辦公停車場可以顯著增加都市區停車位供應。基礎設施供應商透過銷售感測器套件、車牌識別 (ANPR) 攝影機和預約軟體,在硬體成本下降的同時縮短投資回收期,從而在這兩個領域獲利豐富。

至2025年,非街道停車設施(地上、多層和地下)將佔歐洲停車市場的63.82%。在限制地上開發的歷史街區,地下停車場的收費較高。然而,隨著感測器網路向市政定價系統提供即時數據,路邊停車位的年複合成長率預計將達到11.48%,高於其他任何類型的停車設施。到2025年,倫敦無現金支付的普及帶來了顯著的可見性提升,使每個行政區都能精確到分鐘地對路邊停車位進行優先排序,包括電動車充電站、自行車道和裝卸貨區。

為了應對這項挑戰,私人停車場業者正透過提供諸如基於應用程式的提前預訂、便捷的入場流程以及捆綁式充電服務等功能來提升用戶體驗,從而為更高的小時收費辯護,以對抗日益便捷的路邊停車位。諸如巴黎計畫在2030年減少6萬個路邊停車位之類的政策,在減少停車位供應的同時,也隨著稀缺性的增加而推高了每個停車位的收入。因此,競爭格局正從單純的停車位容量轉向便利性和附加價值服務的提供。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大停車場強制安裝電動車充電設施的範圍

- 城市旅遊業和遊客數量的恢復

- 地方政府引入動態定價和數位支付

- 微型倉配中心的興起(路邊物流樞紐)

- 將停車數據整合到城市數位雙胞胎中

- 透過V2G(車輛到電網)服務將閒置停車位貨幣化

- 市場限制因素

- 維修電動車相容基礎設施成本高昂

- 出行方式向主動出行和共享出行轉變

- 加強低排放區路邊停車的整治

- 執法部門使用人工智慧時出現的錯誤可能導致訴訟。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按應用程式字段

- 停車場營運商/管理公司

- 基礎設施提供者(硬體和軟體)

- P2P停車應用提供者

- 停車類型

- 路邊停車

- 路外停車位

- 地面停車場

- 多層停車庫

- 地下設施

- 透過技術

- 傳統停車解決方案

- 智慧停車解決方案

- 按最終用戶類型

- 地方政府和地方議會

- 商業設施和零售商店

- 交通樞紐(機場、鐵路、港口)

- 住宅社區

- 醫療設施

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 比利時

- 瑞典

- 波蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- APCOA Parking Holdings GmbH

- Indigo Group SA

- Q-Park NV

- Euro Car Parks Limited

- National Car Parks Limited

- JustPark Limited

- ParkingEye Limited

- EasyPark Group AB

- Parkopedia Limited

- NSL Services Group Limited(part of Marston Holdings Limited)

- Interparking SA

- Saba Infraestructuras, SA

- Parclick SL

- ParkVia Limited

- Flowbird Group SAS(formerly Parkeon)

- Urbiotica SL

- Smart Parking Ltd

- ParkBee BV

- RingGo Limited

- Tazbell Services Group Limited

- Get My Parking Pvt. Ltd.

- ParkMobile, LLC

第7章 市場機會與未來展望

The Europe Car Parking Market size is projected to expand from USD 6.24 billion in 2025 and USD 6.91 billion in 2026 to USD 11.43 billion by 2031, registering a CAGR of 10.59% between 2026 to 2031.

This rapid expansion reflects the shift from passive space allocation to data-driven, electrification-ready assets that city governments and private operators now treat as a core element of urban-mobility strategy. AFIR-driven retrofit programs, the return of international visitors to pre-pandemic levels, and the roll-out of cashless, sensor-enabled curbside zones have combined to raise pricing power and unlock new revenue streams such as vehicle-to-grid (V2G) aggregation. Competition is intensifying as traditional garage owners defend share through long-term concessions and acquisitions of charging networks, while digital-first platforms convert idle residential and commercial capacity into bookable inventory. Operators that can blend physical capacity with predictive analytics are best placed to capture rising demand linked to e-commerce micro-fulfillment and EV adoption.

Europe Car Parking Market Trends and Insights

Expansion Of EV-Charging Mandates In Parking Facilities

AFIR requires every European parking site with more than 20 spaces to install at least one charger, a rule that entered force in 2024. National add-ons magnify the effect, most notably Germany's GEIG law obliging new non-residential buildings to pre-cable one in every five spaces. Compliance is accelerating joint ventures between garage owners and charge-point specialists such as Allego and Fastned, sharing capital outlays while granting operators upside from energy-services revenue. Utrecht's 500-vehicle V2G pilot proved that parked EVs can supply power during evening peaks, creating a template for monetizing dwell time. Staggered enforcement France extended retrofit deadlines to 2027, Sweden pulled its target forward to 2025 creates a rolling procurement wave that benefits contractors and equipment makers across the decade.

Recovery Of Urban Tourism And Footfall

International arrivals exceeded 2019 levels in 2024, restoring congestion in historic centers and transport hubs. Airports such as Madrid-Barajas introduced 15-minute price recalibration, boosting revenue per space by 12% during Q1 2026. Retailers defend in-store traffic by subsidizing parking, while local ordinances shrinking curb capacity in Barcelona and Amsterdam paradoxically tighten supply even as demand climbs. The rebound is uneven, yet the net effect is upward pressure on hourly rates across tourist corridors.

High Retrofit Costs For EV-Ready Infrastructure

Many multi-story garages built before 2010 lack transformer capacity for multiple fast chargers, forcing pricey grid upgrades that can delay projects up to 18 months. Grant schemes in Italy and Spain reimburse up to 40% of capital outlay but suffer from oversubscription and complex paperwork. Smaller surface-lot owners in secondary cities struggle to finance retrofits without proven utilization forecasts. Software integration mandated by AFIR real-time pricing display and contactless payment acceptance adds further burden to legacy ticketing systems.

Other drivers and restraints analyzed in the detailed report include:

- Municipal Adoption Of Dynamic Pricing And Digital Payments

- Emergence Of Curbside Logistics Hubs For Micro-Fulfillment

- Modal Shift To Active And Shared Mobility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peer-to-peer platforms digitize fragmented capacity, letting property owners monetize spaces during evenings and weekends. The Europe car parking market size for parking operators stood at 46.23% in 2025, yet platform players are growing 11.26% annually, narrowing the gap. Traditional operators rely on long-term municipal concessions, but users increasingly favor app-based booking that can undercut posted rates by up to 30%. Integration APIs offered by infrastructure vendors now let incumbents white-label their own apps, blurring lines between categories. Compliance questions persist, as some cities classify P2P income as commercial activity subject to tax, while others treat it as ancillary property use, creating a patchwork regulatory map.

Second-order effects include rising adoption of dynamic pricing among asset-heavy operators keen to emulate the elasticity benefits enjoyed by digital rivals. JustPark surpassed 2 million registered spaces in 2025, proving that residential driveways and under-filled office lots can meaningfully expand urban inventory. Infrastructure suppliers capture upside across both camps, selling sensor kits, ANPR cameras, and reservation software that shorten payback periods even as hardware costs fall.

Off-street facilities surface, multi-story, and underground held 63.82% share of the Europe car parking market in 2025. Underground garages command premium tariffs in heritage districts where above-ground development is restricted. However, on-street inventory is forecast to expand at a 11.48% CAGR, faster than any other site class, as sensor grids feed real-time data into municipal pricing engines. London's cashless expansion in 2025 produced a visibility step-change, enabling boroughs to triage curb space among EV charging, bike lanes, and loading bays with minute-level precision.

Operators of private garages respond by upgrading user experience app pre-booking, frictionless entry, and bundled charging to justify higher hourly fees relative to increasingly convenient curb slots. Policies such as Paris' plan to remove 60,000 on-street spaces by 2030 cut raw supply but push per-space revenue higher as scarcity intensifies. The competitive dynamic thus pivots on delivering convenience and ancillary services rather than pure capacity.

The Europe Car Parking Market Report is Segmented by Application Area (Parking Operators and Management Companies, and More), Parking Site (On-Street Parking, Off-Street Parking and More), Technology (Conventional Parking Solutions, and Smart Parking Solutions), End-User Type (Transportation Hubs, Residential Complexes, and Healthcare Facilities), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APCOA Parking Holdings GmbH

- Indigo Group SA

- Q-Park NV

- Euro Car Parks Limited

- National Car Parks Limited

- JustPark Limited

- ParkingEye Limited

- EasyPark Group AB

- Parkopedia Limited

- NSL Services Group Limited (part of Marston Holdings Limited)

- Interparking SA

- Saba Infraestructuras, S.A.

- Parclick S.L.

- ParkVia Limited

- Flowbird Group SAS (formerly Parkeon)

- Urbiotica S.L.

- Smart Parking Ltd

- ParkBee B.V.

- RingGo Limited

- Tazbell Services Group Limited

- Get My Parking Pvt. Ltd.

- ParkMobile, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of EV-Charging Mandates in Parking Facilities

- 4.2.2 Recovery of Urban Tourism and Footfall

- 4.2.3 Municipal Adoption of Dynamic Pricing and Digital Payments

- 4.2.4 Emergence of Curbside Logistics Hubs for Micro-Fulfilment

- 4.2.5 Integration of Parking Data into City Digital Twins

- 4.2.6 Monetisation of Idle Parking Capacity via Vehicle-to-Grid (V2G) Services

- 4.3 Market Restraints

- 4.3.1 High Retrofit Costs for EV-Ready Infrastructure

- 4.3.2 Modal Shift to Active and Shared Mobility

- 4.3.3 Stricter On-Street Parking Removal in Low-Emission Zones

- 4.3.4 AI-Based Enforcement Errors Triggering Litigation

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application Area

- 5.1.1 Parking Operators / Management Companies

- 5.1.2 Infrastructure Providers (Hardware and Software)

- 5.1.3 P2P Parking Apps Providers

- 5.2 By Parking Site

- 5.2.1 On-Street Parking

- 5.2.2 Off-Street Parking

- 5.2.2.1 Surface Lots

- 5.2.2.2 Multi-Storey Garages

- 5.2.2.3 Underground Facilities

- 5.3 By Technology

- 5.3.1 Conventional Parking Solutions

- 5.3.2 Smart Parking Solutions

- 5.4 By End-User Type

- 5.4.1 Municipalities and Local Councils

- 5.4.2 Commercial Establishments and Retail

- 5.4.3 Transportation Hubs (Airports, Rail, Ports)

- 5.4.4 Residential Complexes

- 5.4.5 Healthcare Facilities

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Belgium

- 5.5.8 Sweden

- 5.5.9 Poland

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 APCOA Parking Holdings GmbH

- 6.4.2 Indigo Group SA

- 6.4.3 Q-Park NV

- 6.4.4 Euro Car Parks Limited

- 6.4.5 National Car Parks Limited

- 6.4.6 JustPark Limited

- 6.4.7 ParkingEye Limited

- 6.4.8 EasyPark Group AB

- 6.4.9 Parkopedia Limited

- 6.4.10 NSL Services Group Limited (part of Marston Holdings Limited)

- 6.4.11 Interparking SA

- 6.4.12 Saba Infraestructuras, S.A.

- 6.4.13 Parclick S.L.

- 6.4.14 ParkVia Limited

- 6.4.15 Flowbird Group SAS (formerly Parkeon)

- 6.4.16 Urbiotica S.L.

- 6.4.17 Smart Parking Ltd

- 6.4.18 ParkBee B.V.

- 6.4.19 RingGo Limited

- 6.4.20 Tazbell Services Group Limited

- 6.4.21 Get My Parking Pvt. Ltd.

- 6.4.22 ParkMobile, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球自動導引運輸車(AGV)與停車機器人市場報告2026年全球停車場和停車庫市場報告2026年全球自動代客泊車人工智慧市場報告

2026年全球自動導引運輸車(AGV)與停車機器人市場報告2026年全球停車場和停車庫市場報告2026年全球自動代客泊車人工智慧市場報告 機器人泊車系統市場:按類型、自動化系統和地區分類

機器人泊車系統市場:按類型、自動化系統和地區分類 全自動多層停車庫市場:依產品類型、技術、停車層數、車輛類型、應用、最終用戶分類,全球預測(2026-2032)多平台車輛停車升降機市場:按類型、系統類型、安裝方式、應用領域和最終用戶分類,全球預測,2026-2032年2026年全球汽車升降平台AGV停車機器人市場報告全球多層停車市場按結構類型、停車系統、最終用戶、應用、支付模式、服務類型和建築材料分類的預測(2026-2032年)多層停車市場按停車類型、營運類型、建築材料和最終用途分類-2026-2032年全球預測多層停車市場按建築類型、所用材料、自動化程度、停車技術和應用分類-全球預測,2026-2032年

全自動多層停車庫市場:依產品類型、技術、停車層數、車輛類型、應用、最終用戶分類,全球預測(2026-2032)多平台車輛停車升降機市場:按類型、系統類型、安裝方式、應用領域和最終用戶分類,全球預測,2026-2032年2026年全球汽車升降平台AGV停車機器人市場報告全球多層停車市場按結構類型、停車系統、最終用戶、應用、支付模式、服務類型和建築材料分類的預測(2026-2032年)多層停車市場按停車類型、營運類型、建築材料和最終用途分類-2026-2032年全球預測多層停車市場按建築類型、所用材料、自動化程度、停車技術和應用分類-全球預測,2026-2032年