|

市場調查報告書

商品編碼

2044239

閘流體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thyristor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

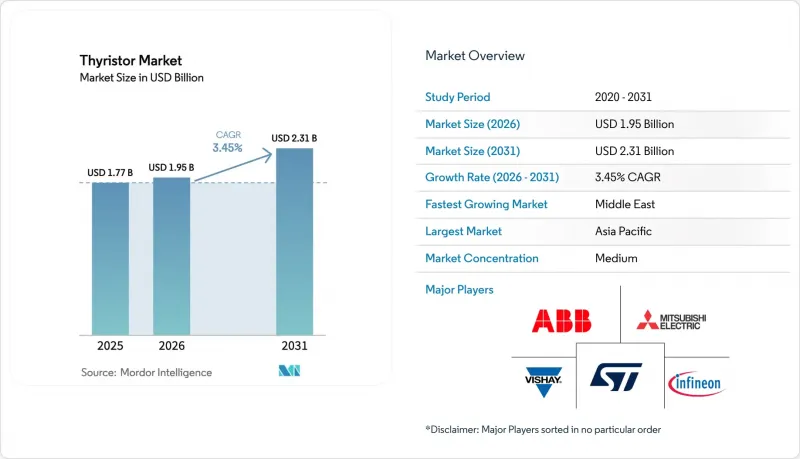

2025 年閘流體市場價值為 17.7 億美元,預計到 2031 年將達到 23.1 億美元,而 2026 年為 19.5 億美元,預測期(2026-2031 年)複合年成長率為 3.45%。

儘管碳化矽金屬氧化物半導體場場效電晶體(SiC MOSFET)在汽車和高頻工業驅動市場中市場佔有率不斷成長,但由於電力公司在吉瓦級高壓直流(HVDC)電路中仍然偏愛線路整流閥,因此市場需求仍然強勁。採購週期主要受大規模電網專案驅動,這些專案能夠確保未來數年的訂單,但模組整合商正在向整合閘極驅動器和感測器的智慧功率模組領域拓展業務。隨著中國領先的分立元件供應商提供的封裝式和柱狀封裝裝置的平均售價比歐洲競爭對手低20-30%,低功率和中功率產品的價格競爭日益激烈。同時,假冒仿冒品的風險和認證延遲也凸顯了可追溯性和垂直整合製造的重要性。

全球閘流體市場趨勢與洞察

擴大高壓直流輸電線路以整合亞洲離岸風力發電

在中國、韓國和澳大利亞,大規模離岸風電走廊持續構成新建±800千伏輸電線路的基礎,每條走廊每吉瓦容量需要200-300個壓裝式晶閘管。光是在中國,哈密重慶-寧夏-湖南輸電線路就新增了16吉瓦的換流容量,其中包括用於線路整流階段的閘流體閥。韓國的「西海岸能源高速公路」計畫已於2024年核准,預計到2028年將需要1,600個高功率閥。澳洲的馬裡努斯連接線採用了混合閥設計,為閘流體提供了獨立的高壓位置[hitachienergy.com]。因此,即使電壓源換流器(VSC)的選擇越來越多,閘流體市場預計仍將保持強勁,專案訂單將持續到2030年代初。

歐盟電力運營商電網規範強制要求動態無功功率補償

歐洲輸電系統運營商協會 (ENTSO-E) 更新後的指導方針要求配電運營商在尖峰時段和非高峰時段將功率因數維持在 ±0.95 以內。德國聯邦網路管理局已強制要求所有裝置容量超過 10 兆瓦的發電廠在 2026 年 1 月前安裝動態支援系統,這推動了閘流體訂單電容器組和靜態無功功率補償器 (SVC) 的訂單成長。在西班牙,一台配備 48 脈衝閥組件的 1800 兆乏靜態同步補償器已經安裝完畢。義大利已訂購 900 兆乏軟性交流輸電系統 (FACTS) 設備,用於緩解可再生能源發電量削減的影響,預計將於 2024 年投入使用。由於合規期限延長至 2028 年,一波分階段的維修正在進行中,這將支撐歐洲和北美地區的閘流體市場。

在電動車逆變器中以SiC MOSFET取代現有產品

各大汽車製造商正在向碳化矽(SiC)裝置過渡,該裝置可將逆變器體積減少約三分之一,並將車輛續航里程延長約6%,取代400V和800V系統中傳統的基於閘流體的輔助設備。大規模生產的增加已將SiC的價格溢價降低至絕緣柵雙極電晶體(IGBT)價格的三倍以下,從而促進了中端車型的轉型。閘流體供應商缺乏與之匹敵的高頻開關能力,因此到2025年,許多品牌的單車安裝成本將低於6美元。汽車領域的銷售額曾經是成長的支柱,但如今卻在下滑,這限制了閘流體市場在移動出行領域的成長潛力。

細分市場分析

2025年,閘流體將佔市場需求的65.71%,成為電化學加工中低頻相控整流器、馬達軟啟動器和汽車交流發電機調節器的基礎元件。這些裝置具有6000-8000V的擊穿電壓和超過其突波電流10倍的突波抗擾度,並且批量採購價格低於15美元,這使得閘流體市場在對價格敏感的工業細分市場中持續廣泛應用。預計到2031年,閘極關斷型閘閘流體(GTO)的複合年成長率將達到3.82%,因為其自整流特性正被用於簡化模組化多級變換器和城市軌道交通升級改造中的保護電路。這一領域的成長在中國高鐵路車輛車隊中尤其明顯,因為新型變換器仍依賴GTO來實現故障隔離,同時也要承受振動和溫度波動的影響。雖然三端雙向可控矽、反導式和非對稱式可控矽能夠滿足住宅調光和斬波器驅動等小規模領域的應用,但它們都無法滿足核心可控矽的需求。

設計方案的選擇體現了開關速度和每安培經濟性之間的權衡。雖然工業級可控矽整流器(SCR)閘流體的市場規模保持穩定,但GTO晶閘管在需要更快關斷以實現更高功率密度和耐受能力的領域正日益受到青睞。雙向三端雙向可控矽開關元件(TRIAC)的銷售量持平,因為智慧家庭中心正在用固態繼電器取代傳統的繼電器。反向導通型TRIAC在斬波器應用中發展勢頭強勁,透過將二極體和閘流體整合到單一晶片上來降低電感。另一方面,非對稱TRIAC適用於反向應力極小的高壓直流(HVDC)輸電線路。涵蓋這五大類裝置的供應商正受益於交叉銷售,這導致了銷售的適度集中。

到2025年,500兆瓦以下的應用將佔45.83%的市場佔有率,涵蓋中壓驅動器、區域靜態無功補償器(SVC)和配電級換流器。額定值的標準化簡化了設計,並且在現有設備的升級改造中更受歡迎,因為在這些情況下,安裝空間限制比最終電流密度更為重要。隨著數十億美元的高壓直流輸電線路將離岸風力發電連接到跨境輸電網,預計1,000兆瓦以上的設備將以3.97%的複合年成長率成長。韓國西海岸8吉瓦的主幹線路將採用約1600層堆疊的高功率裝置,每層都串聯連接多個壓接組件[home.kepco.co.kr]。 500-1000兆瓦的中型項目,例如沙烏地阿拉伯的750兆瓦鋁整流器項目,具有均衡的資本效率和可控的諧波。

對於高功率訂單,首選能夠承受單件3-4kW散熱的膠囊式封裝,這需要直接液冷。 IEC 60747-9認證需要18個月,因此擁有內部測試設備的現有製造商享有一定的進入門檻。同時,三菱電機的下一代8500V壓裝IGBT模組雖然面積更小,但成本卻高出40-50%,限制了其在空間受限的變電站中的應用。因此,隨著吉瓦級電網的不斷擴展,兆瓦級閘流體的市場佔有率穩步成長,而寬能隙裝置則在中端市場逐漸佔據一席之地。

區域分析

到2025年,亞太地區將以45.48%的市場佔有率主導閘流體市場,這主要得益於中國12吉瓦高壓直流輸電容量的擴建以及印度6400公里鐵路的電氣化改造。日本正透過模組化多級混合換能器加強島際互聯,這些換能器仍需高壓閘極關斷堆疊結構。韓國8吉瓦的旗艦項目則支撐著數年的訂單積壓。澳洲的馬裡努斯連接線計畫預計將持續建造至2030年代初,該計畫將引入電壓源換能器(VSC)技術以減少每兆瓦的裝置數量。該地區還擁有全球最大的離散半導體製造群,預計到2025年,中國晶圓廠將出貨4.2億顆用於驅動、消費性電子和牽引領域的裝置。

預計中東地區將呈現最高的成長率,2026年至2031年間的複合年成長率將達到4.08%。這主要歸功於沙烏地阿拉伯的NEOM大型企劃,該項目為4吉瓦的電解槽訂購了整流器,每吉瓦需要800至1000個大電流模組[neom.com]。蘇代爾和達夫拉等太陽能發電廠整合了閘流體開關電容器組和靜態無功補償器(SVC),可提供超過900兆瓦時的綜合無功補償容量。巴林和卡達的鋁冶煉廠維修消耗了數千個大電流裝置,到2028年,沿岸地區至少規劃了三個電解槽計畫。因此,該地區的需求與依賴油氣收入的能源多元化預算密切相關。

在北美和歐洲,晶閘管市場正逐步擴張。德國正在進行設備維修,以應對2026年起強制實施的動態無功功率支援;西班牙部署的1,800兆乏靜止同步補償器(STATCOM)已展現出對電網的即時影響。然而,美國電力公司對門極關閉裝置的認證週期可能超過18個月,這可能會延遲收入確認。在南美,巴西東北部風電併網的600兆乏軟性交流輸電系統(FACTS)合約是主要驅動力。同時,非洲的計畫儲備以南非的串聯電容器走廊為主導,但資金限制預計將運作推遲到2027年或更晚。整體而言,全球趨勢凸顯了區域性政策和專案資金籌措利率如何影響閘流體市場。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟電力運營商電網規範強制要求動態無功功率補償

- 擴大高壓直流輸電線路以整合亞洲離岸風力發電

- 中國和印度的摩托車電動車快速充電基礎設施採用SCR電堆

- 海灣合作理事會(GCC)國家鋁冶煉廠整流器現代化改造

- 印度和德國對鐵路機車用固態斷路器的需求激增

- 航空電子設備中採用抗輻射光觸發閘流體

- 市場限制因素

- 電動車逆變器中SiC MOSFET的損耗

- 東南亞地區假冒SCR模組導致OEM廠商召回產品。

- 美國電力公司GTO認證週期過長

- 多晶矽價格的波動推高了分立式閘流體的成本。

- 產業價值鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 依設備類型

- 矽控整流器(SCR)

- 門極關斷閘流體(GTO)

- 雙向三端雙向可控矽

- 反向導通閘閘流體

- 非對稱閘流體(ASCR)

- 按類型分類的額定輸出

- 500兆瓦或以下

- 500~1,000MW

- 超過1000兆瓦

- 安裝方法和包裝

- 螺柱類型

- 膠囊/光碟

- SMD貼片和夾式安裝

- 模組(智慧功率模組、混合動力模組)

- 觸發方法

- 電動門操作

- 光觸發(LTT)

- 由脈衝變壓器觸發

- 按最終用途行業分類

- 工業驅動和電機控制

- 高壓直流輸電和FACTS(SVC、STATCOM)

- 可再生能源轉換(太陽能、風能)

- 運輸(鐵路、船舶)

- 汽車(汽車充電器、電動車動力傳動系統)

- 家用電器/家用電器

- 航太/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Infineon Technologies AG

- Mitsubishi Electric Corp.

- ABB Ltd.

- STMicroelectronics NV

- Vishay Intertechnology Inc.

- Littelfuse Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Dynex Semiconductor Ltd.

- IXYS Corp.(Littelfuse)

- WeEn Semiconductors Co. Ltd.

- Shindengen Electric Mfg. Co. Ltd.

- Dongguan Yangjie Electronic Co.

- Jiangsu JieJie Microelectronics

- Sensata Technologies Inc.

- CRRC Zhuzhou Institute(CRRC CSI)

- Diodes Inc.

- Central Semiconductor Corp.

- GeneSiC Semiconductor(Navitas)

- Powerex Inc.

- Semikron Danfoss A/S

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corp.

第7章 市場機會與未來展望

The Thyristor market size was valued at USD 1.77 billion in 2025 and is estimated to grow from USD 1.95 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 3.45% during the forecast period (2026-2031).

Demand is steady because utilities still favor line-commutated valves for multi-gigawatt high-voltage direct current (HVDC) corridors, even as silicon-carbide metal-oxide-semiconductor field-effect transistors (SiC MOSFETs) win share in automotive and high-frequency industrial drives. Procurement cycles are shaped by large grid projects that lock in orders years ahead, while module integrators diversify toward intelligent power modules that embed gate drivers and sensors. Price competition is intensifying in low-and mid-power ratings as Chinese discrete suppliers offer stud and capsule devices at 20-30% lower average selling prices than European peers. At the same time, counterfeit risk and certification delays are raising the importance of traceability and vertically integrated manufacturing.

Global Thyristor Market Trends and Insights

Expansion of HVDC Links Integrating Offshore Wind in Asia

Mega-scale offshore wind corridors continue to anchor new +-800 kV lines across China, South Korea, and Australia, each requiring between 200-300 press-pack devices per gigawatt of capacity. China's Hami-Chongqing and Ningxia-Hunan lines alone add 16 GW of converter capacity that specifies thyristor valves for line-commutated stages. Korea's West Coast Energy Expressway, approved in 2024, locks in 1,600 high-power devices through 2028 . Australia's Marinus Link adopts a mixed valve approach that still reserves discrete high-voltage positions for thyristors [hitachienergy.com]. Project backlogs therefore extend into the early 2030s, sustaining the Thyristor market even as voltage-source converter (VSC) choices rise.

Grid-Code-Mandated Dynamic Reactive-Power Compensation in EU Utilities

Updated ENTSO-E guidance now obliges distribution operators to maintain power factor within +-0.95 during peak and off-peak windows. Germany's Federal Network Agency sets a January 2026 deadline for plants above 10 MW to install dynamic support, stimulating orders for thyristor-switched capacitor banks and static var compensators. Spain has already deployed 1,800 MVAr of static synchronous compensators equipped with 48-pulse valve assemblies. Italy awarded 900 MVAr of flexible alternating current transmission systems (FACTS) gear in 2024 to reduce renewable curtailment. Compliance windows to 2028 underpin a rolling retrofit wave that supports the Thyristor market across Europe and North America.

SiC MOSFET Cannibalization in EV Inverters

Leading automakers have migrated to SiC devices that shrink inverter volume by nearly one-third and raise vehicle range by about 6%, displacing legacy thyristor-based auxiliaries in 400-V and 800-V systems. Mass-production scale has reduced the SiC premium to less than triple insulated-gate bipolar transistor (IGBT) pricing, encouraging mid-tier models to switch. Thyristor vendors lack comparable high-frequency switching capability, so content per vehicle fell below USD 6 in 2025 for many brands. Automotive revenue, formerly a growth pillar, is now retreating, limiting the Thyristor market's upside in mobility segments.

Other drivers and restraints analyzed in the detailed report include:

- Modernization of Aluminum-Smelter Rectifiers in Gulf Cooperation Council Countries

- Fast-Charging Infrastructure for Two-Wheeler EVs in China and India Using SCR Stacks

- Counterfeit SCR Modules Causing OEM Recalls in Southeast Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicon-controlled rectifiers secured 65.71% of demand in 2025, anchoring low-frequency phase-controlled rectifiers across electro-chemical processing, motor soft-starters, and automotive alternator regulators. These devices combine 6,000-8,000 V blocking strength with surge tolerance above 10X rated current, while selling for under USD 15 in volume, which keeps the Thyristor market pervasive in price-sensitive industrial niches. Gate turn-off thyristors are forecast to log a 3.82% CAGR to 2031 as modular multilevel converters and urban rail upgrades adopt their self-commutating capability for simplified protection. The segment's growth is evident in China's high-speed train fleet, where new converters withstand vibration and temperature swings yet still rely on GTOs for fault isolation. Triacs, reverse-conducting, and asymmetric variants each address smaller pockets such as residential dimming or chopper drives, but none rival the scale of core SCR demand.

Design-in decisions reflect a trade-off between switching speed and per-ampere economics. The Thyristor market size for SCRs in industrial service remains stable, whereas GTO penetration rises where power density and ride-through dictate faster turn-off. Bidirectional triac sales stay flat because smart-home hubs replace legacy dimmers with solid-state relays. Reverse-conducting types gain in traction choppers, collapsing diode and thyristor into one die to cut inductance, while asymmetric parts meet HVDC poles that rarely see reverse stress. Suppliers that span all five device families capture cross-sell benefits, contributing to moderate revenue concentration.

Applications under 500 MW held 45.83% share in 2025, covering medium-voltage drives, regional static var compensators, and distribution-level converters. Standardized ratings streamline engineering, favorite for brownfield upgrades where footprint constraints override ultimate current density. Above 1,000 MW installations are forecast to grow at a 3.97% CAGR because multibillion-dollar HVDC corridors link offshore wind farms and cross-border grids. South Korea's 8 GW West Coast backbone will use about 1,600 stacked levels of high-power devices, each level series-connecting multiple press packs [home.kepco.co.kr]. Mid-tier 500-1,000 MW projects such as Saudi Arabia's 750 MW aluminum rectifier complex demonstrate balanced capital efficiency and manageable harmonics.

High-power orders favor capsule packages that tolerate 3-4 kW heat dissipation per device, necessitating direct liquid cooling. Certification under IEC 60747-9 can take 18 months, so incumbents with in-house test bays enjoy an access moat. Meanwhile, next-generation 8,500 V press-pack IGBT modules from Mitsubishi Electric offer smaller footprints, but their 40-50% cost premium limits adoption to space-constrained substations. The Thyristor market share in mega-watt segments therefore expands steadily as gigawatt-scale links multiply, even though wide-bandgap devices nibble at the mid-range.

The Thyristor Market Report is Segmented by Device Type (Silicon-Controlled Rectifier (SCR), and More), Power Rating (Below 500 MW, 500-1000 MW, and Above 1000 MW), Mounting and Package (Stud-Type, Capsule/Disc, and Module), Triggering Method (Electrical, Light, Pulse Transformer, and More), End-Use Industry (Industrial Drives and Motor Control, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the Thyristor market with 45.48% share in 2025, lifted by China's addition of 12 GW HVDC capacity and India's electrification of 6,400 route-kilometers of railway track. Japan is reinforcing inter-island links with modular multilevel converter hybrids that still need high-voltage gate turn-off stacks, and South Korea's 8 GW backbone project sustains a multiyear order book. Australia's Marinus Link introduces VSC technology, trimming devices per megawatt yet extending construction through the early 2030s. The region also houses the world's largest discrete manufacturing clusters, with Chinese fabs shipping 420 million units in 2025 for drives, appliances, and traction.

The Middle East is projected to post the fastest 4.08% CAGR during 2026-2031 as Saudi Arabia's NEOM mega-project orders rectifiers for 4 GW of electrolyzers, each gigawatt requiring 800-1,000 high-current capsules [neom.com]. Solar plants such as Sudair and Al Dhafra integrate thyristor-switched capacitor banks and static var compensators that together exceed 900 MVAr of reactive support. Aluminum smelter upgrades in Bahrain and Qatar consume thousands of high-current devices, and at least three Gulf potline projects are queued through 2028. Regional demand therefore ties closely to energy-diversification budgets linked to hydrocarbon revenue.

North America and Europe exhibit moderate expansion. Germany's mandate for dynamic reactive support effective 2026 is triggering retrofits, and Spain's 1,800 MVAr STATCOM rollout showcases immediate grid benefits. Certification cycles for gate turn-off stacks in U.S. utilities, however, may exceed 18 months, delaying revenue recognition. South America centers on Brazil's 600 MVAr FACTS contracts that integrate Northeastern wind, while Africa's pipeline is led by South Africa's series capacitor corridor, yet fiscal constraints push commissioning beyond 2027. Collectively, the global footprint underscores how region-specific policies and project financing rates govern the Thyristor market trajectory.

- Infineon Technologies AG

- Mitsubishi Electric Corp.

- ABB Ltd.

- STMicroelectronics N.V.

- Vishay Intertechnology Inc.

- Littelfuse Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Dynex Semiconductor Ltd.

- IXYS Corp. (Littelfuse)

- WeEn Semiconductors Co. Ltd.

- Shindengen Electric Mfg. Co. Ltd.

- Dongguan Yangjie Electronic Co.

- Jiangsu JieJie Microelectronics

- Sensata Technologies Inc.

- CRRC Zhuzhou Institute (CRRC CSI)

- Diodes Inc.

- Central Semiconductor Corp.

- GeneSiC Semiconductor (Navitas)

- Powerex Inc.

- Semikron Danfoss A/S

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-code-mandated Dynamic Reactive-Power Compensation in EU Utilities

- 4.2.2 Expansion of HVDC Links Integrating Offshore Wind in Asia

- 4.2.3 Fast-charging Infrastructure for 2-wheeler EVs in China and India using SCR Stacks

- 4.2.4 Modernization of Aluminum-smelter Rectifiers in Gulf Cooperation Council Countries

- 4.2.5 Surge in Solid-state Circuit Breakers for Rail Locomotives in India and Germany

- 4.2.6 Adoption of Radiation-hard Optically Triggered Thyristors in Avionics

- 4.3 Market Restraints

- 4.3.1 SiC MOSFET Cannibalization in EV Inverters

- 4.3.2 Counterfeit SCR Modules Causing OEM Recalls in Southeast Asia

- 4.3.3 Lengthy Certification Cycles for GTOs in United States Utilities

- 4.3.4 Volatile Polysilicon Pricing Inflating Discrete Thyristor Cost

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Device Type

- 5.1.1 Silicon-Controlled Rectifier (SCR)

- 5.1.2 Gate Turn-Off Thyristor (GTO)

- 5.1.3 Bidirectional Triac

- 5.1.4 Reverse Conducting Thyristor

- 5.1.5 Asymmetric Thyristor (ASCR)

- 5.2 By Power Rating

- 5.2.1 Less than 500 MW

- 5.2.2 500 - 1 000 MW

- 5.2.3 Above 1 000 MW

- 5.3 By Mounting and Package

- 5.3.1 Stud-Type

- 5.3.2 Capsule / Disc

- 5.3.3 SMD and Clip-mount

- 5.3.4 Module (Intelligent Power Module, Hybrid)

- 5.4 By Triggering Method

- 5.4.1 Electrical Gate Triggered

- 5.4.2 Light Triggered (LTT)

- 5.4.3 Pulse Transformer Triggered

- 5.5 By End-use Industry

- 5.5.1 Industrial Drives and Motor Control

- 5.5.2 HVDC and FACTS (SVC, STATCOM)

- 5.5.3 Renewable Power Conversion (Solar, Wind)

- 5.5.4 Transportation (Rail Traction, Marine)

- 5.5.5 Automotive (On-board Chargers, EV Powertrain)

- 5.5.6 Consumer Electronics and Appliances

- 5.5.7 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 ABB Ltd.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Vishay Intertechnology Inc.

- 6.4.6 Littelfuse Inc.

- 6.4.7 ON Semiconductor Corp.

- 6.4.8 Renesas Electronics Corp.

- 6.4.9 Dynex Semiconductor Ltd.

- 6.4.10 IXYS Corp. (Littelfuse)

- 6.4.11 WeEn Semiconductors Co. Ltd.

- 6.4.12 Shindengen Electric Mfg. Co. Ltd.

- 6.4.13 Dongguan Yangjie Electronic Co.

- 6.4.14 Jiangsu JieJie Microelectronics

- 6.4.15 Sensata Technologies Inc.

- 6.4.16 CRRC Zhuzhou Institute (CRRC CSI)

- 6.4.17 Diodes Inc.

- 6.4.18 Central Semiconductor Corp.

- 6.4.19 GeneSiC Semiconductor (Navitas)

- 6.4.20 Powerex Inc.

- 6.4.21 Semikron Danfoss A/S

- 6.4.22 Fuji Electric Co., Ltd.

- 6.4.23 Toshiba Electronic Devices & Storage Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球閘流體市場報告

2026年全球閘流體市場報告 閘流體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

閘流體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 整合式閘極整流閘流體市場:2026-2032年全球市場預測(依產品類型、電壓等級、電流等級、銷售管道、應用及最終用戶分類)

整合式閘極整流閘流體市場:2026-2032年全球市場預測(依產品類型、電壓等級、電流等級、銷售管道、應用及最終用戶分類) IGCT市場分析及至2035年預測:依類型、產品、服務、技術、組件、應用、最終用戶、功能及安裝類型分類

IGCT市場分析及至2035年預測:依類型、產品、服務、技術、組件、應用、最終用戶、功能及安裝類型分類 閘流體市場規模、佔有率和成長分析(按功率等級、裝置類型、安裝/封裝、觸發方式、最終用戶和地區分類)-2026-2033年產業預測

閘流體市場規模、佔有率和成長分析(按功率等級、裝置類型、安裝/封裝、觸發方式、最終用戶和地區分類)-2026-2033年產業預測 IGCT 市場預測(至 2032 年):按類型、額定功率、冷卻方式、封裝設計、應用、最終用戶和地區進行的全球分析全球閘流體市場:未來預測(2025-2030)

IGCT 市場預測(至 2032 年):按類型、額定功率、冷卻方式、封裝設計、應用、最終用戶和地區進行的全球分析全球閘流體市場:未來預測(2025-2030) 門極可關斷閘流體管的全球市場全球光觸發閘流體市場

門極可關斷閘流體管的全球市場全球光觸發閘流體市場 IGCT(整合式門極換向閘流體)市場報告:趨勢、預測與競爭分析(至 2031 年)

IGCT(整合式門極換向閘流體)市場報告:趨勢、預測與競爭分析(至 2031 年)