|

市場調查報告書

商品編碼

2044232

歐洲彈性辦公空間:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Flexible Office - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

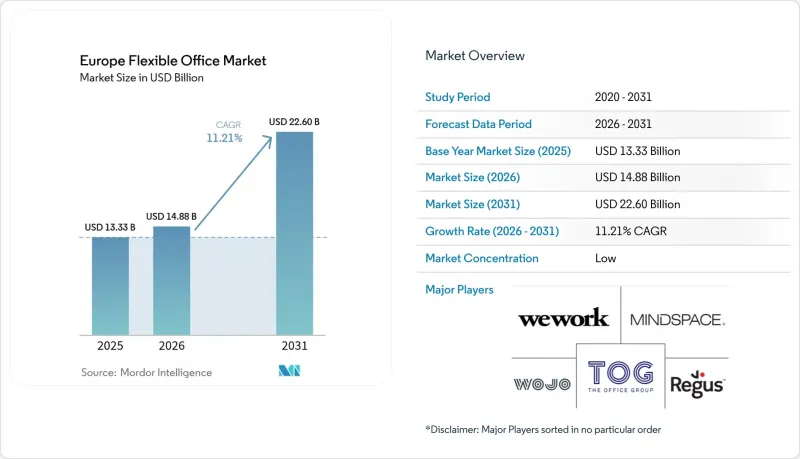

歐洲彈性辦公市場預計到 2025 年將達到 133.3 億美元,到 2026 年將達到 148.8 億美元,到 2031 年將達到 226 億美元,2026 年至 2031 年的複合年成長率為 11.21%。

基準年的重新評估導致基準年從2025年大幅調整至2026年,此前未納入統計的服務式辦公室庫存和整合到企業總部的靈活辦公桌現已累計,從而使歐洲的報告標準與北美IFRS 16租賃會計準則保持一致。每週3-4天到辦公室辦公的混合辦公政策,以及對A級ESG認證建築日益成長的需求,為租戶將靈活辦公空間視為其投資組合不可或缺的一部分而非臨時補充,奠定了穩健的基礎。人工智慧驅動的運轉率分析和專用5G連接正在提高每個工作站的收入,並降低獨立營運商的進入門檻。同時,與永續發展掛鉤的融資正在推動資本流入維修項目,擴大優質物業的供應,並從根本上維持高階資產的低空置率。

歐洲彈性辦公市場趨勢與洞察

享受“高品質假期”,入住符合A級標準和ESG規範的彈性辦公空間。

租戶正轉向那些擁有檢驗環保性能的建築,預計到2025年,獲得認證的辦公空間租金溢價將比二次性辦公空間高出15-20%。歐盟的《企業永續發展報告指令》(CSRD)強制要求揭露租賃物業的範圍3排放,這使得未經認證的辦公空間對公司聲譽構成風險。 IWG和The Office Group等業者會公佈詳細的碳排放強度指標,並致力於在其所有物業組合中實現淨零排放。相較之下,業主更傾向於與Flex品牌建立收益分成夥伴關係,以降低擱淺資產的風險。這種「追求品質」的趨勢使得優質Flex辦公空間的租金保持堅挺,儘管低等級建築的獎勵不斷增加。

每週強製到辦公室三到四天的做法,推動了對混合型、彈性辦公空間的需求。

歐洲主要公司已將臨時混合辦公安排轉為永久性政策。沃達豐規定員工每月至少有八天在辦公室辦公,歐洲中央銀行已將混合辦公框架延長至2027年,微軟則對區域員工維持每週三天在辦公室辦公的規定。由於每日出勤率仍難以預測,各公司透過簽訂多年期合約來保障辦公空間的剩餘容量,從而確保營運商穩定的運轉率,以此對沖風險。諸如Stellantis公司2024年恢復全職辦公的政策調整凸顯了市場的波動性,並強化了彈性辦公空間作為因應政策變化保障的重要性。儘管IT行業持續裁員,但每位員工的辦公桌數量卻在增加,支撐了收入成長。這種結構性變化解釋了為何即使在週期性裁員的情況下,歐洲彈性辦公市場仍能持續擴張。

高昂的室內裝修和設備成本正在給企業的利潤率帶來壓力。

預計2024年至2025年間,建築成本將以每年8%至12%的速度上漲,高階室內裝修成本將增加至每平方公尺870至1,305美元。先進的暖通空調系統、LED照明和智慧建築感測器(必須符合歐盟分類標準)將使預算再增加15%至20%。由於新店通常需要18至24個月才能達到收支平衡,融資有限的業者將面臨長期資金消耗的風險。沒有批量採購合約或內部工程部門的小規模品牌最為脆弱,它們將被擠出企業契約,被迫進入盈利較低的自由職業者主導的細分市場。

細分市場分析

至2025年,共享辦公空間將佔歐洲彈性辦公市場收入的51.22%,凸顯其對注重協作的自由工作者和創新機構的吸引力。同時,預計到2031年,服務式辦公室和行政套房的複合年成長率將達到12.1%,超過歐洲彈性辦公室市場的整體擴張速度,因為銀行和顧問公司將資料安全放在首位。服務式辦公室領域的崛起伴隨著遵守NIS2標準的壓力,配備專用空調、可上鎖門禁和共用伺服器機架的私人辦公室價格溢價高達30-40%[3]。為了應對這項挑戰,供應商推出了將私人辦公室與共享休息室相結合的混合產品,以平衡隱私和社區氛圍。

「追求品質生活」的趨勢持續推動服務式辦公空間的需求。例如,IWG與安聯房地產合作,在德國、法國和西班牙預租了25萬平方公尺獲得ESG認證的全新辦公空間,租期至2025年。同時,模組化室內系統將施工週期縮短至八週,加快了資本週轉速度,並降低了擴張帶來的風險。雖然共享辦公空間仍佔據相當大的市場佔有率,但隨著企業租戶轉向更注重隱私的辦公模式,其佔有率正在逐漸下降,重塑歐洲靈活辦公市場格局。

《歐洲彈性辦公市場報告》按類型(共享辦公空間、服務式辦公室/行政套房等)、產業(資訊科技(IT 和 ITES)等)、最終用戶(企業、自由工作者、新創公司及其他)和國家(英國、德國、法國、西班牙、義大利及其他歐洲國家)進行細分。本報告提供上述所有細分市場的市場規模和預測(以美元以金額為準)。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 享受“高品質假期”,入住符合A級標準和ESG規範的彈性辦公空間。

- 每週強製到辦公室工作 3-4 天的規定,維持了對混合型、彈性辦公空間的需求。

- 企業脫碳努力和歐盟分類法正在加速靈活樞紐的維修。

- GreenLink Loans 可將不良資產再融資為靈活空間。

- 人工智慧驅動的運轉率分析可提高每個工作站的收入。

- 部署私人 5G 中立主機將降低衛星式彈性辦公室採用 IT 的門檻。

- 市場限制因素

- 高昂的室內設計和機電費用正在給企業的利潤率帶來壓力。

- 由於獎勵,二次性辦公空間租金低於彈性辦公空間。

- NIS2 和 GDPR 下的隱私審查正在減緩大型企業對小規模品牌的採用速度。

- 跨境增值稅(VAT) 差異正在推高在多個國家開展業務的租戶的總擁有成本 (TCO)。

- 價值/供應鏈分析

- 概述

- 房地產開發商和業主—關鍵見解

- 工作空間設計與技術顧問 - 主要見解

- 模組化家具和智慧辦公室解決方案供應商—關鍵洞察

- 業界的政府法規和舉措

- 彈性辦公房地產市場的技術創新

- 辦公室房地產關鍵指標(供應量、租金、價格、運轉率/空置率)

- 遠距辦公對空間需求的影響

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值單位:美元)

- 按類型

- 共同工作空間

- 服務式辦公室/行政套房

- 其他(混合辦公、虛擬辦公)

- 按行業

- 資訊科技(IT 和 ITES)

- 銀行、金融服務、保險業 (BFSI)

- 商業諮詢和專業服務

- 其他服務(零售、生命科學、能源、法律)

- 按最終用途

- 自由工作者

- 公司

- 新創企業及其他

- 國家

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 公司簡介

- Regus Group Companies

- WeWork

- The Office Group

- Mindspace

- Wojo

- Knotel

- Talent Garden

- Huckletree

- Selina

- Bisley Flexible Offices

- Impact Hub

- Techspace

- Labs(LabTech)

- CBRE Hana(now-The Office Partners)

- Deskopolitan

- Spacesworks

- Utopicus(Banco Santander)

- Station F

- Ordnungs ApS

- Matrikel 1

第7章 市場機會與未來展望

The Europe flexible office market size is projected to be USD 13.33 billion in 2025, USD 14.88 billion in 2026, and reach USD 22.60 billion by 2031, growing at a CAGR of 11.21% from 2026 to 2031.

Base-year revaluation, which now captures previously untracked serviced-office inventory as well as embedded flex desks inside corporate headquarters, produced the sharp 2025-2026 step-change, aligning European reporting with North American IFRS 16 lease-accounting standards. Hybrid work policies that require three to four days in the office each week, together with rising demand for Grade-A, ESG-certified buildings, have created a resilient baseline for occupiers that view flex space as an essential portfolio component rather than surge capacity. AI-enabled occupancy analytics and private 5G connectivity are lifting revenue per workstation and lowering entry barriers for independent operators. Meanwhile, sustainability-linked loans are channeling capital into retrofit projects, expanding high-quality supply and keeping vacancy for premium assets structurally tight.

Europe Flexible Office Market Trends and Insights

Flight-to-Quality Toward Grade-A, ESG-Compliant Flex Offices

Occupiers are trading up to buildings that deliver verifiable environmental performance, widening the rent premium for certified space to 15-20% over secondary stock in 2025. EU Corporate Sustainability Reporting Directive rules compel disclosure of Scope 3 emissions from leased real estate, making uncertified space a reputational liability. Operators such as IWG and The Office Group publish granular carbon-intensity metrics and have portfolio-wide net-zero commitments. In turn, landlords favor revenue-share partnerships with flex brands that help de-risk stranded assets. This quality flight anchors price resilience for prime flex hubs even while incentives proliferate in lower-grade buildings.

Mandatory 3-to-4-Day Office Policies Sustain Hybrid Flex-Space Demand

Europe's largest employers have converted temporary hybrid schedules into permanent policy. Vodafone requires eight office days per month, the European Central Bank has extended its hybrid framework through 2027, and Microsoft keeps a three-day rule for regional staff. Because daily attendance remains unpredictable, enterprises hedge by locking multi-year memberships that guarantee overflow capacity, ensuring stable occupancy for operators. Policy reversals such as Stellantis's 2024 full-time return order underscore volatility, reinforcing flex space as insurance against mandate changes. Even with tech head-count reductions, desk-per-employee ratios are rising, supporting revenue growth. This structural shift explains why the Europe flexible office market continues expanding despite cyclical layoffs.

High Fit-Out & M&E Costs Erode Operator Margins

Construction-cost inflation ran 8-12% annually in 2024-2025, lifting premium fit-out spend to USD 870-1,305 per m2. Advanced HVAC controls, LED lighting, and smart-building sensors demanded by EU Taxonomy compliance add another 15-20% to budgets. Because new sites often take 18-24 months to reach break-even, capital-constrained operators risk prolonged cash burn. Smaller brands lacking bulk-purchase agreements or in-house engineering are most exposed, pushing them toward lower-value freelancer niches and away from enterprise contracts.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Decarbonization & EU Taxonomy Accelerate Retrofit Flex Hubs

- Green-Linked Loans Unlock Refinancing of Distressed Assets Into Flex Space

- Vacant Secondary Offices Undercut Flex Rents With Incentives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Co-working spaces captured 51.22% of Europe flexible office market revenue in 2025, underscoring their appeal to freelancers and creative agencies that prize collaboration. Serviced offices and executive suites, however, are forecast to grow at a 12.1% CAGR to 2031, outpacing overall Europe flexible office market size expansion as banks and consulting firms prioritize data security. The serviced segment's rise mirrors NIS2 compliance pressure; enclosed layouts with dedicated HVAC, lockable access, and private server racks command 30-40% pricing premiums[3]. Operators respond with hybrid products that combine private suites and shared lounges, balancing confidentiality with community.

Continued flight-to-quality strengthens serviced-suite demand. IWG, for example, pre-leased 250,000 m2 of new ESG-certified space across Germany, France, and Spain under a 2025 alliance with Allianz Real Estate. Meanwhile, modular fit-out systems cut build times to eight weeks, reducing capital cycles and de-risking expansion. Co-working's share remains large but is edging lower as enterprise occupiers reshape the Europe flexible office market share mix in favor of privacy-first formats.

The Europe Flexible Office Market Report is Segmented by Type (Co-Working Spaces, Serviced Offices / Executive Suites, and More) by Sector (Information Technology (IT and ITES), and More), by End Use (Enterprises, Freelancers and Start Ups & Others), and by Country (UK, Germany, France, Spain, Italy and Rest of Europe). The Report Provides Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- Regus Group Companies

- WeWork

- The Office Group

- Mindspace

- Wojo

- Knotel

- Talent Garden

- Huckletree

- Selina

- Bisley Flexible Offices

- Impact Hub

- Techspace

- Labs (LabTech)

- CBRE Hana (now - The Office Partners)

- Deskopolitan

- Spacesworks

- Utopicus (Banco Santander)

- Station F

- Ordnungs ApS

- Matrikel 1

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Flight-to-quality toward Grade-A, ESG-compliant flex offices

- 4.2.2 Mandatory 3-to-4-day office policies sustain hybrid flex-space demand

- 4.2.3 Corporate decarbonisation & EU Taxonomy accelerate retrofit flex hubs

- 4.2.4 Green-linked loans unlock refinancing of distressed assets into flex space

- 4.2.5 AI-driven occupancy analytics lift revenue per workstation

- 4.2.6 Private 5G neutral-host roll-out lowers IT barriers for satellite flex offices

- 4.3 Market Restraints

- 4.3.1 High fit-out & M&E costs erode operator margins

- 4.3.2 Vacant secondary offices under-cut flex rents with incentives

- 4.3.3 NIS2 and GDPR privacy scrutiny delays large-enterprise uptake of small brands

- 4.3.4 Cross-border VAT gaps inflate TCO for multi-country occupiers

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers & Asset Owners - Key Insights

- 4.4.3 Workspace Design & Technology Consultants - Key Insights

- 4.4.4 Modular Furniture & Smart Office Solutions Providers - Key Insights

- 4.5 Government Regulations & Initiatives in the Industry

- 4.6 Technological Innovations in the Flexible Office Real Estate Market

- 4.7 Key Office Real-Estate Metrics (Supply, Rentals, Prices, Occupancy/Vacancy %)

- 4.8 Impact of Remote Working on Space Demand

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Type

- 5.1.1 Co-Working Space

- 5.1.2 Serviced Offices / Executive Suites

- 5.1.3 Others (Hybrid, Virtual Office)

- 5.2 By Sector

- 5.2.1 Information Technology (IT & ITES)

- 5.2.2 BFSI (Banking, Financial Services & Insurance)

- 5.2.3 Business Consulting & Professional Services

- 5.2.4 Other Services (Retail, Life-Sciences, Energy, Legal)

- 5.3 By End Use

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start-Ups & Others

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 UK

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Regus Group Companies

- 6.3.2 WeWork

- 6.3.3 The Office Group

- 6.3.4 Mindspace

- 6.3.5 Wojo

- 6.3.6 Knotel

- 6.3.7 Talent Garden

- 6.3.8 Huckletree

- 6.3.9 Selina

- 6.3.10 Bisley Flexible Offices

- 6.3.11 Impact Hub

- 6.3.12 Techspace

- 6.3.13 Labs (LabTech)

- 6.3.14 CBRE Hana (now - The Office Partners)

- 6.3.15 Deskopolitan

- 6.3.16 Spacesworks

- 6.3.17 Utopicus (Banco Santander)

- 6.3.18 Station F

- 6.3.19 Ordnungs ApS

- 6.3.20 Matrikel 1

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment