|

市場調查報告書

商品編碼

2044220

中東和非洲紙漿和造紙行業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Pulp And Paper Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

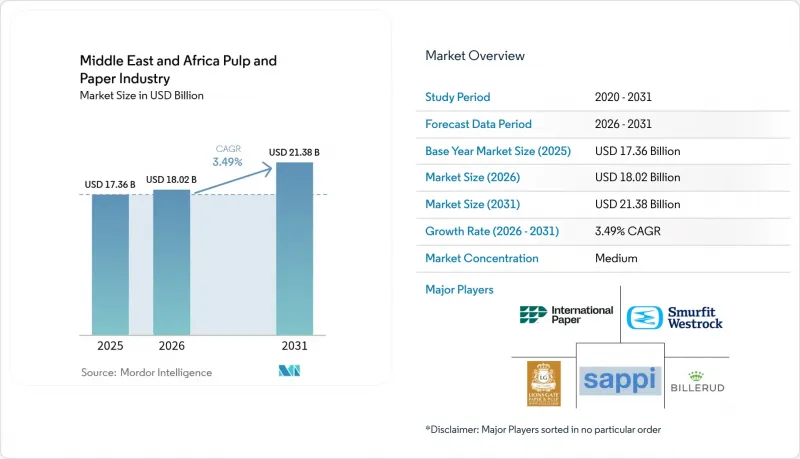

預計中東和非洲的紙漿和造紙市場將從 2025 年的 173.6 億美元和 2026 年的 180.2 億美元成長到 2031 年的 213.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.49%。

儘管結構性纖維短缺導致再生紙進口量居高不下,但海灣合作理事會(GCC)國家的政府支持資金正用於資助綜合造紙廠和替代纖維試點項目,以降低原料風險。南非和波灣合作理事會電子商務小包裹量的成長、肯亞和阿拉伯聯合大公國對一次性塑膠製品的禁令,以及北非和東非人口的持續成長,都支持了瓦楞紙板、紙板和衛生紙的消費。部分非洲市場的貨幣貶值給加工商的利潤率帶來了壓力,但也加速了進口替代投資,因為生產商正尋求在當地採購原料、能源和物流。紅海航線的貨物運輸在地採購提升了區域自給自足的戰略價值,促使主要造紙企業實現運輸路線多元化,並與海灣地區和印度的供應商簽訂長期供應合約。

中東和非洲紙漿和造紙業的趨勢和見解

電子商務包裝需求不斷成長

數位商務的快速發展正在重塑瓦楞紙箱的需求曲線。南非國內的箱板紙產量無法滿足線上訂單量30%的成長,迫使加工業者必須以高昂的運費從東南亞採購箱板紙。海灣合作理事會(GCC)旨在加快清關速度的物流改革預計將使該地區的小包裹量成長兩倍,促使造紙商投資生產更輕、強度更高的紙板,以減輕運輸重量。非洲大陸自由貿易區(AfCFTA)的數位貿易協定進一步加速了內陸國家的最後一公里物流,提高了瓦楞紙板作為零售履約基礎材料的重要性。將廢紙漿採購與自動化瓦楞生產線結合的生產商最有可能最有效地滿足這一不斷成長的需求。

都市區中產階級紙巾產品消費量增加

儘管預計到2024年撒哈拉以南非洲的都市化將超過43%,但家庭用紙巾的使用量仍遠低於全球平均。沙烏地阿拉伯和科威特新運作的紙巾機採用空氣乾燥和結構化輥筒技術,在減少紙漿用量的同時,也實現了更佳的柔軟度。這使得造紙商能夠在保持利潤率的同時,透過提高產品品質來脫穎而出。儘管外匯波動,但強勁的需求支撐著該地區的跨國衛生用品品牌,其銷售額實現了中等個位數的成長。海灣合作理事會(GCC)旅遊中心住宿設施的增加也推動了家庭以外場所對紙巾的需求成長,從而支撐了各種等級紙巾的多樣化產品系列。

中東和北非地區長期缺水限制了造紙廠的許可證發放。

預計到2030年,中東和北非(MENA)地區的淡水資源將低於人均500立方公尺的缺水閾值,監管機構被迫收緊工業污水排放標準。在埃及,一些大型紙漿計畫已被推遲,直到造紙廠能夠證明其具備海水淡化和廢水回用等解決方案。由於化學紙漿生產的用水量約為再生纖維紙漿生產線的三倍,投資者越來越傾向於選擇能夠最大限度減少漂白工序的再生紙漿廠,以及使用椰棗殘渣等非木質原料的紙漿廠。高昂的水處理設備成本,加上不斷上漲的海水淡化成本,給擴張專案的獲利能力帶來了壓力,促使專案轉向節水技術。

細分市場分析

2025年,再生紙漿佔據了最大的銷售佔有率,這反映了阿拉伯聯合大公國長期存在的纖維短缺問題以及生產者延伸責任制(EPR)法規對廢舊產品回收網路的促進作用。多家造紙廠升級了滾筒碎漿機和分類線,以加工從歐洲進口的混合紙包,從而加強了循環經濟並提高了原料品質。在高附加價值領域,溶解用木漿預計將實現最快成長。這主要得益於土耳其和埃及紡織工業叢集中粘膠短纖維的擴張,其目標客戶是尋求永續纖維素原料的歐洲服裝品牌。預計到2031年,中東和非洲紙漿和造紙市場中溶解用木漿的市場規模將以4.43%的複合年成長率成長,這主要得益於位於薩皮的賽科工廠新增11萬噸的產能。一旦商業測試達到一定水平,椰棗樹殘渣等替代纖維有可能取代高達 8% 的進口木片,從而為造紙廠提供抵禦國際木片價格波動的保障。

分級體系仍然傾向於閉合迴路解決方案。在海灣合作理事會(GCC)國家的綜合項目中,牛皮紙生產線和再生紙漿原料相結合,可根據現貨市場紙漿價格的波動靈活調整紙漿等級。同時,在當地林業計畫成熟之前,非洲加工商依賴進口來應對需求波動。阿拉伯聯合大公國政府的研發津貼支持利用溶劑法脫除農業廢棄物中的木素,試點研究表明,與硬木牛皮紙法相比,該方法可使紙漿得率提高50%以上,用水量減少近60%。

預計到2025年,瓦楞紙板紙漿將佔按應用領域分類的銷售額的31.12%,這主要得益於食品出口包裝需求的成長和電子商務的蓬勃發展。中東和非洲的紙漿和造紙市場佔有率預計將繼續保持領先地位,因為海灣合作理事會(GCC)成員國的造紙廠預計到2028年將把測試襯紙和瓦楞紙的年產量提高約90萬噸。克重低於125克/平方米的輕質高耐破強度紙漿正受到小型貨運公司的青睞,這些公司希望降低運輸成本,這也推動了原料配方中再生纖維比例的提高。同時,衛生紙的成長速度最快,複合年成長率(CAGR)達到4.61%。肯亞、奈及利亞和埃及的零售商正在擴大其產品種類,從經濟實惠的單層捲筒紙擴展到高階三層捲筒紙,從而推高了每噸的平均價格。阿拉伯聯合大公國和沙烏地阿拉伯的旅遊業主導需求推動了餐巾紙和毛巾等外帶產品的成長,促使造紙商採用節能的新月形成型機。

儘管印刷和書寫用紙的產量長期呈下降趨勢,但它在非洲各國教育部資助的教科書合約中仍扮演著重要角色。特種紙雖然產量較小,但其利潤率卻是瓦楞紙板的兩到三倍。埃及和南非的加工商正在引進矽塗層和安全線嵌入生產線,以滿足區域標籤和鈔票市場的需求。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務包裝材料需求不斷成長

- 都市區中產階級紙巾產品消費量增加

- 政府對一次性塑膠製品的監管正在將需求轉向紙質替代品。

- 海灣合作理事會對綜合性紙漿和造紙設施的投資正在激增。

- 利用椰棗樹的農業殘渣進行測試可以緩解纖維短缺。

- 航運和自由區循環經濟獎勵

- 市場限制因素

- 木屑進口價格波動很大。

- 中東和北非地區長期缺水,限制了鋸木廠許可證的取得。

- 紅海港口壅塞及額外保全費用

- 非洲主要市場貨幣貶值

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按年級

- 漂白化學紙漿(BCP)

- 用於溶解的木漿(DWP)

- 未漂白牛皮紙漿

- 機械漿

- 再生紙漿

- 透過使用

- 列印/書寫紙

- 報紙紙張

- 組織

- 紙板

- 瓦楞紙板底紙

- 特製紙張

- 按最終用戶行業分類

- 食品和飲料包裝

- 消費品包裝

- 衛生用品

- 出版/教育

- 工業和特殊應用

- 依產品類型

- 繪圖紙

- 包裝紙

- 棉紙

- 特製紙張

- 透過製造技術

- 化學製漿

- 機械製漿

- 再生纖維加工

- 綜合紙漿和造紙廠

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock

- International Paper Company

- Lions Gate Paper & Pulp LLC

- Sappi Limited

- Billerud AB

- Stora Enso Oyj

- Mondi plc

- Oji Holdings Corporation

- Resolute Forest Products Inc.

- Svenska Cellulosa Aktiebolaget SCA

- Nine Dragons Paper(Holdings)Limited

- Asia Pulp & Paper Co., Ltd.

- Kimberly-Clark Corporation

- Pro-Gest SpA

- Metsa Group

- Lee & Man Paper Manufacturing Ltd.

- Mercer International Inc.

- Packaging Corporation of America

第7章 市場機會與未來展望

The Middle East and Africa pulp and paper market size is projected to expand from USD 17.36 billion in 2025 and USD 18.02 billion in 2026 to USD 21.38 billion by 2031, registering a CAGR of 3.49% between 2026 and 2031.

Structural fiber shortages keep recovered-paper imports elevated, while sovereign capital in the Gulf Cooperation Council (GCC) bankrolls integrated mills and alternative-fiber pilots that temper raw-material risk. Rising e-commerce parcel volumes in South Africa and Saudi Arabia, single-use plastic bans in Kenya and the United Arab Emirates (UAE), and steady population growth across North and East Africa underpin boxboard, cartonboard, and tissue consumption. Currency depreciation in several African markets compresses converter margins but also accelerates import-substitution investments as producers seek to localize feedstock, energy, and logistics. Freight disruption on Red Sea lanes has reinforced the strategic premium on regional self-sufficiency, prompting leading mills to diversify shipping routes and sign longer-tenor supply contracts with Gulf and Indian suppliers.

Middle East And Africa Pulp And Paper Industry Trends and Insights

Growing E-Commerce Packaging Demand

Rapid digital-commerce adoption is rewriting corrugated-box demand curves. Domestic containerboard output in South Africa cannot keep pace with the 30% jump in online sales volume, prompting converters to source linerboard from Southeast Asia at elevated freight premiums. GCC logistics reforms that target faster customs clearance are expected to triple intra-regional parcel flows, encouraging mills to invest in light-weight, high-strength grades that trim shipping weight U.AE. The African Continental Free Trade Area (AfCFTA) digital-trade protocol further accelerates last-mile logistics into landlocked economies, reinforcing containerboard as the backbone of retail fulfillment packaging. Producers that couple post-consumer fiber procurement with automated fluting lines are best positioned to capture this incremental tonnage.

Rising Urban Middle-Class Consumption of Tissue Products

Urbanization in sub-Saharan Africa surpassed 43% in 2024, yet household tissue use still trails the global average by a wide margin. New tissue machines in Saudi Arabia and Kuwait deploy through-air-drying and structured-roll technologies that yield premium softness with lower fiber input, enabling mills to differentiate on quality while defending margins. Multinational hygiene brands report mid-single-digit regional sales growth, validating demand resilience even amid currency volatility. With hospitality pipelines expanding across GCC tourism hubs, away-from-home tissue demand is also rising, supporting diversified grade portfolios.

Chronic Water-Stress in MENA Limiting Mill Permitting

Middle East and North Africa (MENA) freshwater availability is forecast to slip below the 500 m3 per-capita scarcity threshold by 2030, forcing regulators to tighten industrial effluent limits. Egypt has already delayed several high-capacity pulp projects until mills can prove desalination or wastewater-reuse solutions. Because chemical pulping consumes roughly three times as much water as recycled-fiber lines, investors increasingly favor recovered-paper plants and non-wood feedstocks such as date-palm residues that require minimal bleaching. The cap-ex premium for water treatment, combined with rising desalinated-water tariffs, weighs on expansion economics and nudges project pipelines toward lower-intensity technologies.

Other drivers and restraints analyzed in the detailed report include:

- Government Bans on Single-Use Plastics Shifting Demand to Paper-Based Substitutes

- Surge in GCC Investment into Integrated Pulp and Paper Capacity

- Port Congestion and Red Sea Security Surcharges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled pulp secured the largest slice of 2025 revenue, reflecting chronic fiber shortages and EPR rules that incentivize post-consumer collection networks U.AE. Multiple mills upgraded drum pulpers and screening lines to handle mixed-paper bales imported from Europe, tightening loop economics and improving furnish quality. On the premium end, dissolving wood pulp is on track for the quickest growth, buoyed by viscose-staple-fiber expansion in Turkish and Egyptian textile clusters that target European apparel brands seeking sustainable cellulose inputs. The Middle East and Africa pulp and paper market size for dissolving wood pulp is projected to expand at a 4.43% CAGR through 2031, supported by a 110,000-tonne capacity addition at Sappi's Saiccor mill. Alternative fibers such as date-palm residues promise to displace up to 8% of imported wood chips once commercial trials reach scale, offering mills a hedge against volatile international chip prices.

The grade mix continues to favor closed-loop solutions. Integrated GCC projects pair Kraft lines with recycled furnish to flex grades in response to spot-pulp swings, while African converters rely on swing imports until local forestry programs mature. Government R&D grants in the UAE support solvent-based delignification of agricultural waste, with pilot runs demonstrating pulp yields above 50% and water savings of nearly 60% versus hardwood kraft U.AE.

Containerboard commanded 31.12% of 2025 application turnover, anchored by food-export packaging and surging e-commerce volumes. The Middle East and Africa pulp and paper market share for this segment is forecast to remain dominant as GCC mills add nearly 900,000 tpa of testliner and fluting by 2028. Lightweight, high-burst grades below 125 gsm are gaining ground among parcel shippers seeking freight savings, nudging furnish recipes toward higher recycled-fiber ratios. Tissue, however, exhibits the fastest trajectory at a 4.61% CAGR. Retail shelves across Kenya, Nigeria, and Egypt are broadening SKU ranges from economy one-ply to premium three-ply rolls, lifting average value per tonne. Tourism-led demand in the UAE and Saudi Arabia is driving growth in away-from-home products such as napkins and towels, prompting mills to commission energy-efficient crescent-former machines.

Printing and writing papers see secular volume erosion but remain relevant in textbook contracts funded by African education ministries. Specialty papers, though low in tonnage, deliver margins two to three times those of containerboard, prompting converters in Egypt and South Africa to install silicone-coating and security-thread embedding lines that serve regional label and banknote markets.

The Middle East and Africa Pulp and Paper Market Report is Segmented by Grade (Mechanical Pulp, Recycled Pulp, and More), Application (Newsprint, Tissue, and More), End-User Industry (Hygiene Products, Publishing and Education, and More), Product Type (Graphic Papers, Packaging Papers, and More), Process Technology (Chemical Pulping, and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Smurfit WestRock

- International Paper Company

- Lions Gate Paper & Pulp LLC

- Sappi Limited

- Billerud AB

- Stora Enso Oyj

- Mondi plc

- Oji Holdings Corporation

- Resolute Forest Products Inc.

- Svenska Cellulosa Aktiebolaget SCA

- Nine Dragons Paper (Holdings) Limited

- Asia Pulp & Paper Co., Ltd.

- Kimberly-Clark Corporation

- Pro-Gest S.p.A.

- Metsa Group

- Lee & Man Paper Manufacturing Ltd.

- Mercer International Inc.

- Packaging Corporation of America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce packaging demand

- 4.2.2 Rising urban middle-class consumption of tissue products

- 4.2.3 Government bans on single-use plastics shifting demand to paper-based substitutes

- 4.2.4 Surge in GCC investment into integrated pulp and paper capacity

- 4.2.5 Date-palm agri-residue trials lowering fibre deficit

- 4.2.6 Maritime Free-Zone circular-economy incentives

- 4.3 Market Restraints

- 4.3.1 Volatile wood-chip import prices

- 4.3.2 Chronic water-stress in MENA limiting mill permitting

- 4.3.3 Port congestion and Red-Sea security surcharges

- 4.3.4 Currency depreciation in key African markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Bleached Chemical Pulp (BCP)

- 5.1.2 Dissolving Wood Pulp (DWP)

- 5.1.3 Unbleached Kraft Pulp

- 5.1.4 Mechanical Pulp

- 5.1.5 Recycled Pulp

- 5.2 By Application

- 5.2.1 Printing and Writing

- 5.2.2 Newsprint

- 5.2.3 Tissue

- 5.2.4 Cartonboard

- 5.2.5 Containerboard

- 5.2.6 Specialty Papers

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage Packaging

- 5.3.2 Consumer Goods Packaging

- 5.3.3 Hygiene Products

- 5.3.4 Publishing and Education

- 5.3.5 Industrial and Specialty Applications

- 5.4 By Product Type

- 5.4.1 Graphic Papers

- 5.4.2 Packaging Papers

- 5.4.3 Tissue Papers

- 5.4.4 Specialty Papers

- 5.5 By Process Technology

- 5.5.1 Chemical Pulping

- 5.5.2 Mechanical Pulping

- 5.5.3 Recycled Fibre Processing

- 5.5.4 Integrated Pulp and Paper Mills

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Saudi Arabia

- 5.6.1.2 United Arab Emirates

- 5.6.1.3 Turkey

- 5.6.1.4 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Kenya

- 5.6.2.3 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock

- 6.4.2 International Paper Company

- 6.4.3 Lions Gate Paper & Pulp LLC

- 6.4.4 Sappi Limited

- 6.4.5 Billerud AB

- 6.4.6 Stora Enso Oyj

- 6.4.7 Mondi plc

- 6.4.8 Oji Holdings Corporation

- 6.4.9 Resolute Forest Products Inc.

- 6.4.10 Svenska Cellulosa Aktiebolaget SCA

- 6.4.11 Nine Dragons Paper (Holdings) Limited

- 6.4.12 Asia Pulp & Paper Co., Ltd.

- 6.4.13 Kimberly-Clark Corporation

- 6.4.14 Pro-Gest S.p.A.

- 6.4.15 Metsa Group

- 6.4.16 Lee & Man Paper Manufacturing Ltd.

- 6.4.17 Mercer International Inc.

- 6.4.18 Packaging Corporation of America

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

加工紙漿市場:按等級、纖維類型、加工方法和應用分類的全球市場預測,2026-2032年高速紙漿洗滌機市場:依原料來源、技術、類型、產能、應用和最終用途產業分類-全球預測,2026-2032年

加工紙漿市場:按等級、纖維類型、加工方法和應用分類的全球市場預測,2026-2032年高速紙漿洗滌機市場:依原料來源、技術、類型、產能、應用和最終用途產業分類-全球預測,2026-2032年 2034年全球紙漿與造紙自動化市場機會與策略

2034年全球紙漿與造紙自動化市場機會與策略 紙漿及造紙市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、安裝類型、設備分類

紙漿及造紙市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、安裝類型、設備分類 紙漿及造紙酶市場機會、成長要素、產業趨勢分析及2026年至2035年預測

紙漿及造紙酶市場機會、成長要素、產業趨勢分析及2026年至2035年預測 全球紙漿和造紙市場:市場規模、份額、成長率、產業分析、類型、應用和區域分析,未來預測(2026-2034)

全球紙漿和造紙市場:市場規模、份額、成長率、產業分析、類型、應用和區域分析,未來預測(2026-2034) 紙漿和造紙市場規模、佔有率和成長分析(按類別、類型、應用、銷售管道和地區分類)-2026-2033年產業預測

紙漿和造紙市場規模、佔有率和成長分析(按類別、類型、應用、銷售管道和地區分類)-2026-2033年產業預測 2032 年紙漿和造紙市場預測:按產品類型、原料、製造流程、應用、最終用戶和地區進行的全球分析

2032 年紙漿和造紙市場預測:按產品類型、原料、製造流程、應用、最終用戶和地區進行的全球分析