|

市場調查報告書

商品編碼

2044206

汽車吸音材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Acoustic Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

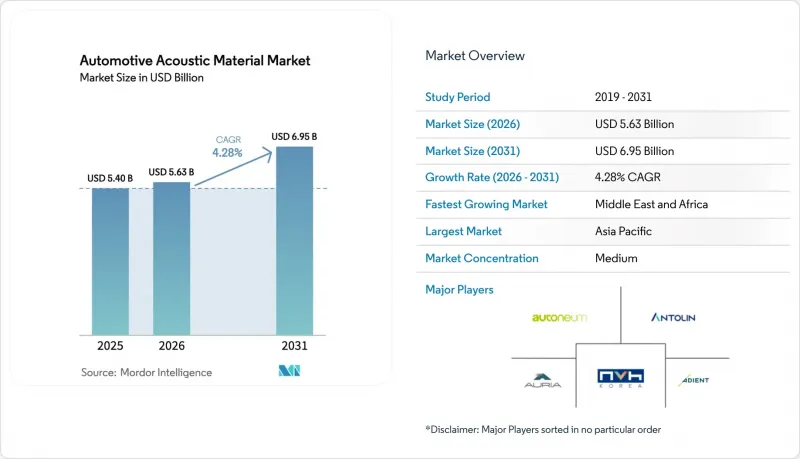

汽車吸音材料市場預計將從 2025 年的 54 億美元成長到 2026 年的 56.3 億美元,到 2031 年達到 69.5 億美元,預測期(2026 年至 2031 年)的複合年成長率為 4.28%。

這一穩步成長主要得益於電動車 (EV) 產量的增加、日益嚴格的車內噪音法規以及對輕質多功能複合材料日益成長的需求。原始設備製造商 (OEM) 正致力於將隔熱和隔音功能整合到單層封裝中,以滿足嚴格的車內噪音標準,同時為滑板式電動車平台預留空間。聚氨酯憑藉其久經考驗的減振性能仍保持主導,但由於更嚴格的回收法規,聚丙烯的需求也在不斷成長。區域成長主要集中在亞太地區,隨著新的組裝廠投產,中東和非洲的成長率超過了全球平均水準。材料科學的進步以及旨在擴大區域業務基礎和豐富產品系列的策略性收購,加劇了市場競爭。

全球汽車聲學材料市場趨勢及洞察

全球對電動車和混合動力車的車內噪音制定更嚴格的法規

電動車 (EV) 和混合動力汽車(HEV) 目前面臨滿足歐盟法規 540/2014 和中國 GB 1495-2024 標準規定的車廂噪音上限的挑戰,這導致對高密度泡棉、多層複合材料和精密調校頻率吸收器的需求激增。原始設備製造商 (OEM) 必須在兩年內獲得認證材料,這使得已獲得認證的供應商擁有顯著的價格優勢。在產品選擇方面,既能阻隔逆變器雜訊又不影響腿部空間的薄壁聚氨酯複合材料正受到越來越多的關注。這些法規現在正蔓延到售後市場,要求替換零件滿足與原廠設備相同的聲學規格,這進一步擴大了潛在的整體需求。能夠使其研發計劃與認證時間表相符的供應商可以設定溢價並獲得多年合約。

透過 OEM 生產,轉向輕質、多功能隔音隔熱複合材料。

製造商正將NVH阻尼器和隔熱材料整合到單一面板中,與傳統的多層結構相比,顯著減輕了重量。富含聚丙烯的基體材料備受青睞,因為它們符合歐洲「循環經濟行動計畫」中規定的可回收性標準。這種轉變正在加速化學製造商與擁有先進黏合生產線的一級加工商之間的策略合作。雖然這些複合材料的每平方公尺成本顯著更高,但原始設備製造商(OEM)可以透過減少緊固件數量、縮短生產週期和提高電動車續航里程來收回成本。整合混煉和貼合加工設備的供應商透過在單次生產過程中實現嚴格的尺寸公差和雙重特性目標,獲得了競爭優勢。

發泡體石化原料供應鏈的波動

受中東地區地緣政治緊張局勢影響,聚氨酯關鍵前體甲苯二異氰酸酯的價格在2025年大幅波動。缺乏避險機制的中小型加工商的利潤率急劇下降。原始設備製造商(OEM)採取了雙重採購和成本轉嫁條款談判等應對措施,但這增加了採購的複雜性。雖然生物基原料路線有望帶來穩定性,但它們仍然會增加成本,且產能有限。擁有後向整合化學品部門或長期合約的供應商正在採取措施應對短期衝擊,並維持其作為首選供應商的地位。

細分市場分析

聚氨酯憑藉其可靠的阻尼性能、成熟的供應鏈以及眾多原始設備製造商(OEM)的積極評價,仍然是市場的基石,預計到2025年將保持40.25%的市場佔有率。汽車吸音材料市場受益於聚氨酯可調性的多樣性,這種特性使其能夠建構針對特定頻寬的獨特孔結構。然而,對可回收性和降低密度的需求推動聚丙烯以6.55%的複合年成長率成長,使其成為突出的成長動力。供應商正在轉向高聚丙烯(PP)共混物,以在滿足阻燃標準的同時顯著減輕重量。生物基原料也正在興起,但目前仍處於試點階段,因為需要擴大規模才能滿足大規模合約的需求。

聚氨酯生產商正積極應對這一趨勢,推出符合歐盟REACH法規標準的可再生多元醇等級產品和低VOC配方。聚氨酯汽車隔音材料的市場規模預計將進一步擴大,反映出其在漸進式創新方面擁有堅實的基礎。聚丙烯的崛起正在推動亞洲地區產能的成長,該地區的綜合石化企業正在降低樹脂成本。玻璃纖維和特殊纖維分別在商用車和豪華車的內裝中發揮獨特的作用,兼顧了成本、重量和美觀。

到2025年,內裝解決方案將佔銷售額的53.18%,這得益於多年來對駕乘舒適性和法規遵從性的重視。車門面板、地毯和儀表板隔熱材料已形成穩定的大量生產體系,為供應商的現金流量提供了保障。汽車隔音市場不斷創新,透過複合氈等材料提升內裝品質,這些材料不僅兼具設計元素的功能,也簡化了組裝,增強了品質感。然而,受電動車空氣動力學性能和風噪降低法規的推動,外飾市場正以7.58%的複合年成長率快速成長。

底盤護板、輪拱襯板和A柱飾板採用聚丙烯和熱成型PET混合材料,可降低寬頻雜訊並承受石塊衝擊。預計到2031年,汽車外部零件的吸音材料市場將顯著成長。整合式空氣動力學和吸音模組有助於汽車製造商在單一組件中實現續航里程和車廂靜謐性目標,其原理是透過降低阻力並抑制渦流噪音。供應商正在開發耐候複合材料,這些材料能夠承受熱循環和道路鹽分的侵蝕,確保長期耐久性,且不會劣化聲學性能。

區域分析

預計到2025年,亞太地區將佔全球銷量的38.16%,這主要得益於中國1,240萬輛的電動車產量以及印度不斷擴大的組裝。為了實現準時交貨並根據當地氣候條件調整配方,當地聲學元件供應商正在上海、浦那和蔚山等地的汽車整車廠附近建立基地。中國汽車聲學材料市場也受到在地採購限制的影響,迫使外國公司透過合資企業擴大產能。日本在混合技術領域的專長正在推動對雙模隔振板的需求,而以出口為導向的韓國整車廠則正在為北美和歐洲市場指定符合全球標準的解決方案。

中東和非洲地區正經歷最快的成長,複合年成長率達5.75%,這主要得益於阿拉伯聯合大公國的工業發展以及沙烏地阿拉伯在其「2030願景」中納入的製造業扶持措施。埃及和摩洛哥新建的CKD(全組裝套件)工廠正在創造對耐高溫儀表板隔熱材料和車門密封條的當地需求。南非正利用其成熟的出口管道對歐洲市場進行出口,歐洲市場對符合歐盟噪音法規和回收指令的認證材料需求旺盛。儘管基礎設施仍然面臨挑戰,但豐富的石化原料為該地區的泡沫材料生產提供了支撐,並降低了當地加工商因原料價格波動而面臨的風險。

歐洲高階品牌持續引領該地區在聲學技術領域的前沿地位。德國汽車製造商正在尋求既符合NVH(噪音、振動和聲振粗糙度)標準又符合永續性標準的超輕層壓材料,供應商則致力於開發支援閉合迴路回收的單材料薄膜。法國和義大利優先考慮符合循環經濟目標的再生纖維氈,而英國則支持致力於氣凝膠混合吸音材料的新創公司。北美地區電動皮卡的普及增加了對輪拱和底盤減震的需求,以降低輪胎噪音,從而為美國工廠帶來了新的生產需求。在各個地區,汽車聲學材料市場都在調整配方,以適應不同的法規距離要求,從而降低氮氧化物和噪音排放。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球對電動車和混合動力車的車內噪音制定更嚴格的法規

- 原始設備製造商向輕質、多功能聲學和熱學複合材料轉型

- 快速的都市化正在推動亞洲新興國家對車內舒適度的需求不斷成長。

- 共乘和無人駕駛計程車數量的不斷增加,將優先考慮耐用的 NVH(噪音、振動和不平順性)內裝。

- 符合ESG要求的生物基發泡體和再生纖維的興起

- 整合式聲學組件可實現車載音響系統的微型化

- 市場限制因素

- 用於發泡體的石化原料供應鏈波動

- 滑板式電動車平台的空間限制了隔熱材料的厚度。

- 對廢舊產品的回收義務更加嚴格,材料也越來越複雜。

- 主動降噪技術的日益普及導致被動式降噪材料的需求下降。

- 價值/供應鏈分析

- 技術展望

- 監理情勢

- 波特五力模型

- 新進入者的威脅

- 替代品的威脅

- 買方的議價能力

- 供應商的議價能力

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值單位:美元)

- 依材料類型

- 聚氨酯

- 聚丙烯

- 聚氯乙烯(PVC)

- 玻璃纖維

- 纖維

- 橡皮

- 發泡體

- 其他

- 按應用程式字段

- 內部的

- 外部的

- 車輛類型

- 搭乘用車

- 輕型商用車(LCV)

- 中型和重型商用車輛(MHCV)

- 巴士和長途汽車

- 按銷售管道

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Autoneum Holding AG

- Grupo Antolin

- Auria Solutions

- 3M Company

- BASF SE

- Continental AG

- Henkel AG & Co. KGaA

- NVH Korea Inc.

- Adient plc

- Compagnie de Saint-Gobain SA

- Toray Industries Inc.

- Sumitomo Riko Co. Ltd.

- Lear Corporation

- Forvia SE(Faurecia SE)

- Owens Corning

- Johns Manville Corporation

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- LyondellBasell Industries NV

第7章 市場機會與未來展望

The automotive acoustic material market size is expected to increase from USD 5.40 billion in 2025 to USD 5.63 billion in 2026 and reach USD 6.95 billion by 2031, reflecting a 4.28% CAGR during the forecast period (2026 to 2031). Increasing electric vehicle production, intensifying interior noise regulations, and the push for lightweight multifunctional composites underpin this steady advance. OEMs focus on integrating thermal and acoustic functions into single-layer packages to free up space in skateboard EV platforms while meeting stringent cabin-noise limits. Polyurethane retains its lead because of proven damping performance, yet polypropylene gains traction as recycling mandates tighten. Geographic growth remains anchored in Asia-Pacific, but the Middle East and Africa outpace global averages as new assembly plants start production. Competitive intensity is shaped by material science breakthroughs and strategic acquisitions that expand regional footprints and diversify product portfolios.

Global Automotive Acoustic Material Market Trends and Insights

Stringent Global Interior Noise Regulations for EVs and HEVs

Electric and hybrid models now face cabin-noise caps under Regulation (EU) 540/2014 and China's GB 1495-2024 standards, driving an immediate spike in demand for high-density foams, multilayer laminates, and precision-tuned frequency absorbers . OEMs must secure certified materials within a two-year window, creating pricing leverage for suppliers already validated. Product selection increasingly revolves around low-thickness polyurethane composites that block inverter whine without sacrificing foot-well space. Regulations now spill into the aftermarket, compelling replacement parts to match original acoustic specifications, thereby enlarging total addressable demand. Suppliers that align R&D pipelines with certification schedules can command premiums and lock in multiyear contracts.

OEM Shift Toward Lightweight, Multifunctional Acoustic-Thermal Composites

Manufacturers are merging NVH dampers with thermal barriers into single panels that deliver notable mass savings over legacy multilayer stacks. Polypropylene-rich matrices are preferred because they meet recyclability thresholds emerging in Europe's Circular Economy Action Plan. The shift accelerates strategic partnerships between chemical companies and Tier 1 converters that control advanced bonding lines. Although such composites cost significantly more per square meter, OEMs recoup expenses through reduced fastener counts, faster takt times, and improved range in EVs. Suppliers with integrated compounding and laminating assets gain a competitive edge by hitting tight dimensional tolerances and dual-property targets in one production pass.

Supply-Chain Volatility in Petrochemical Feedstocks for Foams

Prices for toluene diisocyanate, a key polyurethane precursor, swung significantly during 2025 because of geopolitical tensions affecting Middle Eastern production. Margins for smaller converters without hedging mechanisms experienced a significant contraction. OEMs responded by dual-sourcing and negotiating pass-through clauses, raising procurement complexity. While bio-feedstock routes promise stability, they remain cost-additive and limited in capacity. Suppliers with backward-integrated chemical lines or long-term contracts insulate themselves from near-term shocks and retain preferred-vendor status.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization Spurring Demand for In-Cabin Comfort in Emerging Asia

- Growing Ride-Sharing and Robo-Taxi Fleets Prioritizing Durable NVH Interiors

- Space Constraints in Skateboard EV Platforms Limiting Insulation Thickness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane remained the anchor at 40.25% share in 2025 because of reliable damping, established supply chains, and broad OEM validation. The automotive acoustic material market benefits from polyurethane's tuning versatility, enabling bespoke cell structures for specific frequency bands. Yet recyclability pressures and the search for lower density drive polypropylene's 6.55% CAGR, positioning it as the standout growth vector. Suppliers pivot to PP-rich blends that trim significant mass while meeting flammability codes. Bio-sourced feedstocks emerge but require scaling to match volume contracts, keeping them in pilot phases for now.

Polyurethane producers respond with renewable polyol grades and low-VOC formulations that align with EU REACH thresholds. The automotive acoustic material market size for polyurethane is set for further expansion, reflecting a solid base for incremental innovation. Polypropylene's rise invites capacity expansions in Asia, where integrated petrochemical complexes cut resin costs. Fiberglass and specialty textiles hold niche roles in commercial and premium interiors, respectively, balancing cost, weight, and aesthetics.

Interior solutions delivered 53.18% revenue in 2025, a testament to long-standing focus on occupant comfort and regulatory compliance. Door panels, floor carpets, and dash insulators form stable, high-volume programs that anchor supplier cash flows. The automotive acoustic material market continues to innovate in interior trims through composite felts that double as design surfaces, easing assembly and enhancing perceived quality. However, the exterior segment grows faster at 7.58% CAGR, propelled by EV aerodynamics and wind-noise management mandates.

Underbody shields, wheel-arch liners, and A-pillar trims leverage polypropylene and thermoformed PET blends that resist stone impact while dampening broadband noise. The automotive acoustic material market size assigned to exterior components is forecast to grow significantly by 2031. Integrated aero-acoustic modules lower drag and suppress vortex-induced noise, feeding OEM range and cabin-quietness targets in one assembly. Suppliers refine weather-stable composites able to survive thermal cycling and road-salt exposure without acoustic drift, locking in long-term durability claims.

The Automotive Acoustic Material Market Report is Segmented by Material Type (Polyurethane, Polypropylene, Polyvinyl Chloride, Fiberglass, and More), Application Area (Interior and Exterior), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), and More), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 38.16% of global revenue in 2025, anchored by China's 12.4 million electric car production count and India's expanding assembly clusters . Local acoustic suppliers co-locate near OEM plants in Shanghai, Pune, and Ulsan to meet just-in-time targets and adapt formulations to regional climate conditions. The automotive acoustic material market in China also absorbs local content rules, pushing foreign firms toward joint ventures for capacity scaling. Japan's hybrid expertise sustains demand for dual-mode barrier-absorber panels, while South Korea's export-focused OEMs specify global-compliant solutions to serve North American and European destinations.

The Middle East and Africa post the fastest expansion at 5.75% CAGR, led by the industrial development in the United Arab Emirates and Saudi Arabian manufacturing incentives embedded in Vision 2030. New CKD plants in Egypt and Morocco create localized demand for dash insulators and door seals tuned for high ambient temperatures. South Africa leverages established export channels to Europe, requiring materials certified to EU noise and recycling directives. Although infrastructure limitations persist, abundant petrochemical feedstocks underpin regional foam production, cushioning feedstock volatility on local converters.

Europe's premium brands keep the region at the forefront of acoustic technology. Germany's OEMs demand ultralight laminates that meet both NVH and sustainability thresholds, spurring suppliers to develop mono-material films compatible with closed-loop recycling. France and Italy prioritize felts made from recycled textile fibers, fitting circular-economy goals, while the United Kingdom nurtures start-ups exploring aerogel-hybrid absorbers. North America's transition toward electric pickup trucks intensifies the need for wheel-arch and underbody damping to manage tire roar, injecting fresh volume into plants in the United States. Across geographies, the automotive acoustic material market adapts formulations to match varying regulatory distances to curb NOx and noise emissions.

List of Companies Covered in this Report:

- Autoneum Holding AG

- Grupo Antolin

- Auria Solutions

- 3M Company

- BASF SE

- Continental AG

- Henkel AG & Co. KGaA

- NVH Korea Inc.

- Adient plc

- Compagnie de Saint-Gobain S.A.

- Toray Industries Inc.

- Sumitomo Riko Co. Ltd.

- Lear Corporation

- Forvia SE (Faurecia SE)

- Owens Corning

- Johns Manville Corporation

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- LyondellBasell Industries N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Interior Noise Regulations for EVs and HEVs

- 4.2.2 OEM Shift Toward Lightweight, Multifunctional Acoustic-Thermal Composites

- 4.2.3 Rapid Urbanization Spurring Demand for In-Cabin Comfort in Emerging Asia

- 4.2.4 Growing Ride-Sharing and Robo-Taxi Fleets Prioritizing Durable NVH Interiors

- 4.2.5 Emergence of Bio-Based Foams and Recycled Textiles Aligned With ESG Mandates

- 4.2.6 Integrated Acoustic Packages Enabling Vehicle Audio-System Downsizing

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Volatility in Petrochemical Feedstocks for Foams

- 4.3.2 Space Constraints in Skateboard EV Platforms Limiting Insulation Thickness

- 4.3.3 Escalating End-of-Life Recycling Mandates Increasing Material Complexity

- 4.3.4 Rising Popularity of Active Noise Cancellation Cutting Passive-Material Demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Material Type

- 5.1.1 Polyurethane

- 5.1.2 Polypropylene

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Fiberglass

- 5.1.5 Textiles

- 5.1.6 Rubber

- 5.1.7 Foam

- 5.1.8 Others

- 5.2 By Application Area

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCVs)

- 5.3.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.3.4 Buses and Coaches

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Autoneum Holding AG

- 6.4.2 Grupo Antolin

- 6.4.3 Auria Solutions

- 6.4.4 3M Company

- 6.4.5 BASF SE

- 6.4.6 Continental AG

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 NVH Korea Inc.

- 6.4.9 Adient plc

- 6.4.10 Compagnie de Saint-Gobain S.A.

- 6.4.11 Toray Industries Inc.

- 6.4.12 Sumitomo Riko Co. Ltd.

- 6.4.13 Lear Corporation

- 6.4.14 Forvia SE (Faurecia SE)

- 6.4.15 Owens Corning

- 6.4.16 Johns Manville Corporation

- 6.4.17 Covestro AG

- 6.4.18 Dow Inc.

- 6.4.19 Huntsman Corporation

- 6.4.20 LyondellBasell Industries N.V.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

聲學材料市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、最終用戶、地區和競爭格局分類,2021-2031年

聲學材料市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、最終用戶、地區和競爭格局分類,2021-2031年 汽車聲學材料市場:2026-2032年全球市場預測(按應用、材料、車輛類型、最終用戶和分銷管道分類)

汽車聲學材料市場:2026-2032年全球市場預測(按應用、材料、車輛類型、最終用戶和分銷管道分類) 2026年全球降噪音通風口市場報告聲學材料市場:依產品類型、材料、應用、最終用戶、通路分類,全球預測(2026-2032年)2026年全球汽車聲學材料市場報告車輛隔音材料市場:依材料類型、技術、車輛類型、應用領域和最終使用者管道分類,全球預測(2026-2032年)

2026年全球降噪音通風口市場報告聲學材料市場:依產品類型、材料、應用、最終用戶、通路分類,全球預測(2026-2032年)2026年全球汽車聲學材料市場報告車輛隔音材料市場:依材料類型、技術、車輛類型、應用領域和最終使用者管道分類,全球預測(2026-2032年) 全球汽車聲學材料市場規模:依類型、零件、應用、車輛、區域範圍和預測

全球汽車聲學材料市場規模:依類型、零件、應用、車輛、區域範圍和預測