|

市場調查報告書

商品編碼

2044190

安全印刷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Security Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

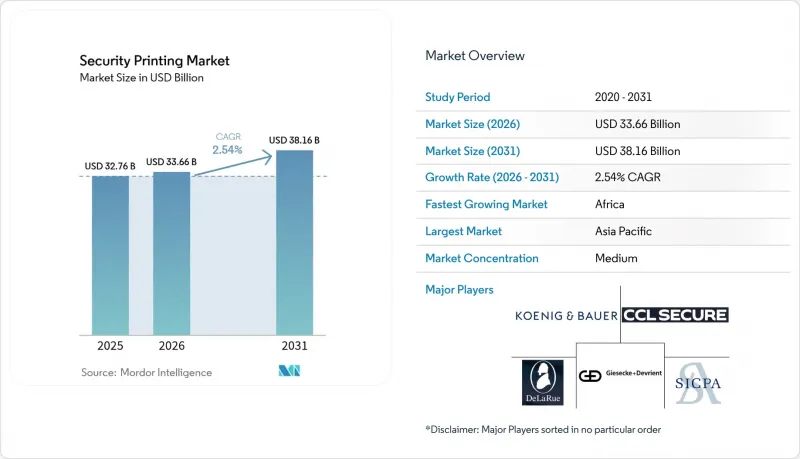

2025 年安全印刷市場價值為 327.6 億美元,預計到 2031 年將達到 381.6 億美元,而 2026 年為 336.6 億美元,預測期(2026-2031 年)複合年成長率為 2.54%。

鈔票、護照和稅票偽造的持續威脅迫使發卡機構採用多層顯性、隱性和法證安全功能。受生物辨識護照的引入和國家生物識別身分計畫的推廣,個人身分證明文件的演變速度超過了現金。聚合物基材因其使用壽命是棉紙的2.5到4倍而日益普及,即使價格高出30%到40%,也能降低生命週期成本。使用RFID和NFC標籤的非接觸式認證如今已成為護照和安全ID卡的主流要求,這催生了對使用線上數位噴墨技術進行個人化客製化的新需求。同時,各國央行的「綠色貨幣」政策鼓勵供應商採用再生棉、低排放油墨和無溶劑清漆,從而在安全印刷市場中開闢了永續發展相關產品的利基市場。

全球安全印刷市場趨勢與洞察

假冒和仿冒事件增多

查獲的假鈔數量不斷增加,加速了光學調製油墨、3D安全帶和微光等防偽技術的應用。歐洲央行在2024年查獲了55.4萬張歐元假鈔,相當於每100萬張真鈔中就有18張是假鈔。德國聯邦銀行查獲的假鈔數量年增了28%,而100美元鈔票仍然是全球最常被偽造的面額。儘管已經引入了符合國際民航組織(ICAO)標準的RFID晶片,護照詐騙依然猖獗,對全像覆膜和雷射雕刻技術的需求持續成長。新興市場大面額鈔票的流通增加了造假者的利潤,也加劇了安全功能的競爭。

政府強制推行安全身分識別和電子護照

政府計畫推動了對安全聚碳酸酯資料頁、雷射雕刻和接觸型智慧卡嵌體的巨大需求。印度將於2025年11月開始發放嵌入生物識別晶片的護照,目標是在2027年實現年產量1,000萬本。歐盟的eIDAS 2.0框架要求成員國實施與安全晶片相連的數位身分錢包,加速了27個機構的設備升級。印尼內政部已選擇IDEMIA作為其大批量NIK卡合約的合作夥伴。同時,在美國,隨著REAL ID實施截止日期臨近(2025年5月),各州駕照部門正在持續進行採購。所需功能因收入階層而異,供應商市場分為兩大板塊:高階生物識別解決方案和成本最佳化的防詐騙解決方案。

無現金支付及向央行數位貨幣的過渡

在高所得市場,數位支付方式的興起正在降低對紙幣的長期需求。國際清算銀行(BIS)的一項調查顯示,94%的受訪央行正在研究央行數位貨幣(CBDC),預計到2024年將推出CBDC,並在六年內向大眾推廣。瑞典的電子克朗試點計畫和歐洲央行的數位歐元計畫表明,到2035年,紙幣發行量將出現兩位數的下降。中國的電子人民幣已擁有2.6億個電子錢包,但農村地區對現金的依賴削弱了其影響力。在非接觸式支付逐漸普及的地區,紙本票據和支票正在消失,印刷商被迫將業務轉向身分證和品牌保護標籤的印刷。

細分市場分析

截至2025年,紙幣仍佔據安全印刷市場最大佔有率,但個人識別卡的需求成長更為迅猛,促使企業重新評估資本投資的優先事項。印度、法國和英國的大規模護照競標確保了晶片嵌入式組裝、雷射雕刻和聚碳酸酯貼合加工等技術未來多年的需求。歐洲的eIDAS 2.0和亞洲更嚴格的KYC(了解你的客戶)要求推動了身分識別卡安全印刷市場規模的成長,促使供應商擴大其區域卡片個性化業務。同時,支票印刷業務正呈現結構性下滑。英國支票簽發量從1990年的39億張下降到2023年的2.19億張。儘管交通票正逐漸轉向支援NFC功能的智慧型手機,但由於監管機構強制要求序列化,菸草和酒精品牌保護標籤的使用量正在增加。歐盟菸草產品指令下的稅票競標表明,即使傳統現金支付方式停滯不前,安全印刷的需求仍然可以成長。

在以現金交易為主的地區,對大面額鈔票的需求使得凹版印刷生產線幾乎滿運作運轉,從而保障了傳統安全印刷設備供應商的市場佔有率。預計到2025年,奈及利亞、印度和西非中央銀行(BEAC)成員國將發行超過2,500億總合鈔票,凸顯了經合組織以外國家鈔票的穩健性。然而,隨著各國央行預期未來將向央行數位貨幣(CBDC)過渡,鈔票的再發行週期正在延長,訂單量也變得更加波動。因此,供應商正在多元化經營至身分證和追蹤溯源標籤領域。這些產品同樣需要具備防偽功能,但每平方公尺基材的利潤率更高。

儘管安全油墨仍佔收入的三分之一以上(按功能分類),但電子元件的價值正在上升。 RFID 和 NFC 標籤的成本為每本護照 2 至 4 美元,目前已成為電子護照組件成本的主要組成表,而全像圖的成本約為 0.30 美元。 2024 年的晶片短缺暴露了價值鏈中的脆弱性,迫使簽發機構採用雙重採購模式,從恩智浦 (NXP)、英飛凌 (Infineon) 以及印度和中國的本土晶圓廠採購晶片。諸如 Surys 的同分異構性等光調製裝置仍然是主要檢驗手段,但隱藏標籤和機器可讀元件目前佔據了大部分收入。 Koenig & Bauer 公司於 2025 年推出的清漆,嵌入了肉眼不可見但在特定波長下可探測到的隱蔽頻譜,無需額外的後表面處理工程即可在印刷過程中應用。這種將可見特徵、隱藏特徵和法醫特徵融合在一起的做法正逐漸成為標準做法,各國央行會為每種面額的鈔票疊加 10-15 種不同的元素,以阻止造假者。

符合GS1和歐盟菸草製品指令標準的序列化系統是成長最快的細分市場。目前,歐盟境內的每個菸草包裝都被分配了一個唯一的標識符,這催生了對能夠以每分鐘120公尺的速度列印600 dpi微縮文字的線上數位列印頭的需求。 Domino和Videojet已率先在這個細分市場佔據了市場佔有率,而Memjet和Xaar則為高階稅封和藥品提案了高解析度的替代解決方案。這些趨勢正在逐步削弱模擬安全油墨的主導地位,未來的成長將轉向混合電子列印技術。

區域分析

亞太地區仍是安全印刷市場的主要收入來源,這主要得益於中國每年發行超過900億張紙幣以及印度流通的1,400億張紙幣。印尼計畫在2030年每年增發3%的紙幣,以及日本於2024年推出的新系列紙幣(預計到2025年中期將有30%投入流通),都將推動該地區的成長。供應商受益於該地區密集的生態系統,組裝基材製造商、凹版印刷機組件製造商和半導體製造廠,這使得他們能夠在該地區採購RFID晶片和光學可變顏料。

預計到2031年,非洲的經濟表現將超越其他所有地區,年複合成長率(CAGR)將達到3.46%。與肯亞Gieseke Devrient公司簽署的五年協議以及與衣索比亞Toppan公司成立的電子護照合資企業,體現了各國致力於在貨幣和身分證生產方面實現自主的承諾。奈及利亞重新設計的紙幣、索馬利亞新版1000先令紙幣以及西非中央銀行(BEAC)的「2020型」紙幣系列,都提高了整個地區的印刷機運轉率。儘管初始資本投資仍然是一個障礙,但多邊金融機構和出口信貸機構正在支持多個承包工程項目的資金籌措,加速向非洲大陸的技術轉移。

歐洲是數位轉型的典型例子。儘管12個國家擁有強大的歐元鈔票印刷基地,但瑞典和挪威的現金使用量已接近個位數,歐洲央行的數位歐元試點計畫可能會在2028年後繼續抑制現金流通。然而,該地區對生物識別護照、符合菸草產品指令的稅票以及帶有序號的藥品標籤的需求依然存在,安全印刷市場也將把重心從現金轉向安全的官方文件。北美也體現了這種雙重性。美國鑄幣局(BEP)每年仍生產76億張鈔票,但對品牌保護標籤和增強型安全駕駛執照的需求成長最為迅速。

在南美洲,貨幣波動使得需求預測變得困難。巴西造幣廠(Casa da Moeda)暫停了部分出口契約,以優先遏制該國的惡性通貨膨脹;而在阿根廷,披索的暴跌擴大了聚合物鈔票試點項目的資金籌措缺口。在中東,各國的印刷廠都在升級設備。阿拉伯聯合大公國生產可回收的500迪拉姆聚合物鈔票,沙烏地阿拉伯擴大產能,旨在減少對歐洲供應商的依賴。因此,每個地區都有其獨特的成長要素和結構性限制因素,也增加了安全印刷市場對多元化產品系列的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 假冒和仿冒事件增多

- 新興市場大面額紙幣的擴張

- 採用聚合物鈔票基材,以提高耐用性和安全性。

- 政府強制推行安全身分識別和電子護照

- 利用人工智慧驅動的線上檢測減少缺陷產品

- 中央銀行「綠色貨幣」永續發展計劃

- 市場限制因素

- 向無現金支付和央行數位貨幣過渡

- 對下一代安全印刷機進行大量資本投資

- 特殊安全油墨和基材供不應求

- 仔細檢視貨幣生產的碳足跡

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 透過使用

- 帳單

- 支付卡

- 查看

- 身分證

- 車票和交通卡

- 郵票和稅票

- 品牌保護和稅務相關問題

- 透過安全功能

- 安全油墨(UV、OVI、光學調製)

- 全像圖和 DOVID

- 浮水印和安全線

- RFID和NFC標籤

- 追蹤、可追溯性和序列化

- 透過印刷技術

- 凹版印刷

- 膠印/平版印刷

- 網版印刷及柔版印刷

- 數位噴墨

- 凹版印刷

- 按基礎材料

- 棉基紙

- 聚合物

- 混合紙和聚合物

- 合成膜和複合膜

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 俄羅斯

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 印尼

- 泰國

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Giesecke+Devrient GmbH

- De La Rue plc

- SICPA Holding SA

- Koenig and Bauer AG

- CCL Secure Pty Ltd

- Oberthur Fiduciaire SAS

- Crane Currency(Crane NXT Co.)

- Toppan Inc.

- IDEMIA Group SAS

- Komori Corporation

- Note Printing Australia Ltd

- Canadian Bank Note Company, Limited

- Landqart AG

- Orell Fussli Holding Ltd(Orell Fussli Security Printing Ltd)

- China Banknote Printing and Minting Corporation

- Security Printing and Minting Corporation of India Ltd(SPMCIL)

- Korea Minting, Security Printing and ID Card Operating Corp.(KOMSCO)

- HID Global Corp.(Citizen Identity Solutions)

第7章 市場機會與未來展望

The security printing market size was valued at USD 32.76 billion in 2025 and estimated to grow from USD 33.66 billion in 2026 to reach USD 38.16 billion by 2031, at a CAGR of 2.54% during the forecast period (2026-2031).

Persistent counterfeiting pressure on banknotes, passports and tax banderoles is compelling issuers to layer multiple overt, covert and forensic features. Personal identification documents are advancing more quickly than cash, helped by biometric-passport rollouts and national digital-ID programs. Polymer substrates are gaining traction because they last 2.5-4 times longer than cotton paper, trimming lifecycle costs even after factoring in their 30-40% price premium. Contactless authentication via RFID and NFC tags is now a mainstream requirement in passports and secure ID cards, creating fresh demand for inline digital-inkjet personalization. Meanwhile, central-bank "green banknote" policies are nudging suppliers toward recycled cotton, lower-emission inks and solvent-free varnishes, opening a sustainability-linked product niche within the security printing market.

Global Security Printing Market Trends and Insights

Rising Incidence of Forgery and Counterfeiting

Counterfeit seizures are climbing, spurring faster adoption of optically variable inks, 3D security ribbons and micro-optic threads. The European Central Bank withdrew 554,000 fake euro notes in 2024, equivalent to 18 counterfeits per million genuine notes.Germany's Bundesbank registered a 28% annual rise in counterfeits, while the U.S. USD 100 note remains the world's most forged series. Passport fraud is also persistent, even after the introduction of ICAO-compliant RFID chips, driving continued demand for holographic overlays and laser engraving. Higher-value notes in emerging markets enlarge the payoff for counterfeiters, reinforcing the security-feature arms race.

Government Mandates for Secure IDs and E-Passports

National programs are boosting volume demand for secure polycarbonate data pages, laser engraving and contactless smart-card inlays. India began issuing biometric chip passports in November 2025 with the goal of producing 10 million units per year by 2027. The European Union's eIDAS 2.0 framework obliges member states to deploy digital-ID wallets tied to secure element chips, catalyzing equipment upgrades across 27 authorities. Indonesia's Home Affairs Ministry selected IDEMIA for a high-volume NIK card contract, while the United States REAL ID deadline of May 2025 kept state driver-license bureaus on a sustained procurement cycle. Mandatory features differ by income tier, splitting the supplier landscape between premium biometric offerings and cost-optimized fraud deterrence.

Shift Toward Cashless Payments and CBDCs

Digital alternatives are eroding long-run demand for physical currency in high-income markets. Ninety-four percent of central banks surveyed by the BIS were researching CBDCs in 2024, with retail launches expected within six years. Sweden's e-krona tests and the European Central Bank's digital euro project foreshadow double-digit contractions in banknote volumes by 2035. China's e-CNY has amassed 260 million wallets, although rural cash reliance tempers the impact. Everywhere that contactless payments take hold, paper tickets and cheques disappear, forcing printers to pivot toward identity documents and brand-protection labels.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Polymer Banknote Substrates for Durability and Security

- Growing Circulation of High-Denomination Banknotes in Emerging Markets

- High Capex for Next-Gen Security Presses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Banknotes generated the largest slice of the security printing market in 2025, yet personal identification documents are growing faster and reshaping capital investment priorities. Large passport tenders in India, France and the United Kingdom locked in multi-year demand for chip-inlay assembly lines, laser engraving and polycarbonate lamination. The security printing market size for ID documents is benefiting from eIDAS 2.0 in Europe and rising KYC requirements in Asia, encouraging suppliers to expand regional card-personalization hubs. Meanwhile, cheque printing is in structural decline after volumes in the United Kingdom dropped from 3.9 billion in 1990 to 219 million in 2023. Transit ticketing is migrating to NFC-enabled smartphones, but brand-protection banderoles for tobacco and alcohol are expanding as regulators impose serialization. Tax-stamp tenders under the EU Tobacco Products Directive illustrate how secure print volumes can grow even as traditional cash instruments stagnate.

In cash-centric regions, high-denomination banknotes keep intaglio press lines running near capacity, preserving the security printing market share of legacy equipment suppliers. Nigeria, India and the BEAC bloc collectively issued more than 250 billion notes in 2025, underlining the resilience of physical currency outside the OECD. However, retender cycles are getting longer and order sizes more variable because central banks anticipate eventual CBDC substitution. Suppliers are therefore diversifying into ID documents and track-and-trace labels, which require similar covert features but carry higher margins per square meter of substrate.

Security inks still anchor more than one-third of feature revenues, but electronic components are climbing the value stack. RFID and NFC tags, each costing USD 2-4 in a passport versus about USD 0.30 for a hologram, now dominate the bill of materials for e-passports. Chip shortages in 2024 exposed supply-chain fragility, pushing issuers to dual-source between NXP, Infineon and domestic fabs in India and China. Optically variable devices such as Surys kinegrams remain critical for first-line verification, yet covert taggants and machine-readable elements drive bulk profitability. Stegano varnish, introduced by Koenig and Bauer in 2025, embeds covert spectra that are invisible to the naked eye but detectable under defined wavelengths, enabling press-side application without an extra finishing step. This convergence of overt, covert and forensic features is standard practice as central banks layer 10-15 distinct elements on each denomination to frustrate counterfeiters.

Serialisation systems meeting GS1 and EU Tobacco Products Directive standards are the fastest-growing micro-segment. Each cigarette pack in the European Union now carries a unique identifier, generating demand for inline digital printheads capable of 600-dpi microtext at 120 meters per minute. Domino and Videojet have captured early share in this niche, while Memjet and Xaar pitch higher-resolution alternatives for premium tax stamps and pharmaceuticals. These trends are gradually eroding the dominance of analog security inks and tilting future growth toward hybrid electronic-print feature sets.

The Security Printing Market Report is Segmented by Application (Banknotes, Payment Cards, Cheques, and More), Security Feature (Security Inks (UV, OVI, Optically Variable), Holograms and DOVIDs, and More), Printing Technology (Intaglio, Offset/Lithography, and More), Substrate (Cotton-Based Paper, Polymer, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the revenue anchor for the security printing market, reflecting China's output above 90 billion banknotes per year and India's 140 billion notes in circulation. Growth is helped by Indonesia's plan to raise banknote volumes 3% annually through 2030 and by Japan's new series introduced in 2024, which were 30% distributed by mid-2025. Suppliers benefit from a dense ecosystem of substrate mills, intaglio press assembly plants and semiconductor fabs, allowing regional sourcing of RFID chips and optically variable pigments.

Africa is predicted to outpace every other region at a 3.46% CAGR to 2031. Kenya's five-year contract with Giesecke+Devrient and Ethiopia's e-passport joint venture with Toppan show a push for sovereign autonomy in currency and ID document manufacture. Nigeria's redesign, Somalia's new 1,000-shilling notes and the BEAC bloc's "type 2020" series bolster regional press utilization rates. Upfront capex remains a hurdle, but multilateral lenders and export-credit agencies are underwriting several turnkey plants, accelerating technology transfer into the continent.

Europe illustrates the digital transition. Despite a robust base of 12 national euro printers, cash usage in Sweden and Norway is near single digits, and the ECB's digital euro pilot may curb circulation after 2028. Nevertheless, the region will sustain demand for biometric passports, tax stamps compliant with the Tobacco Products Directive and serialized pharmaceutical labels, allowing the security printing market to pivot from cash to secure civil documents. North America mirrors this dual track: the United States Bureau of Engraving and Printing still turns out 7.6 billion notes annually, but brand-protection labels and high-security driving licenses are rising fastest.

South America faces currency volatility that complicates forecast volumes. Brazil's Casa da Moeda has halted some export contracts to prioritize domestic hyperinflation mitigation, while Argentina's peso collapse widened tender gaps for polymer note trials. The Middle East is upgrading its own plants; the UAE's recyclable polymer Dh500 note and Saudi Arabia's capacity expansion aim to cut dependence on European suppliers. Each geography thus exhibits a unique mix of growth drivers and structural drag, reinforcing the need for diversified product portfolios within the security printing market.

- Giesecke+Devrient GmbH

- De La Rue plc

- SICPA Holding SA

- Koenig and Bauer AG

- CCL Secure Pty Ltd

- Oberthur Fiduciaire SAS

- Crane Currency (Crane NXT Co.)

- Toppan Inc.

- IDEMIA Group S.A.S.

- Komori Corporation

- Note Printing Australia Ltd

- Canadian Bank Note Company, Limited

- Landqart AG

- Orell Fussli Holding Ltd (Orell Fussli Security Printing Ltd)

- China Banknote Printing and Minting Corporation

- Security Printing and Minting Corporation of India Ltd (SPMCIL)

- Korea Minting, Security Printing and ID Card Operating Corp. (KOMSCO)

- HID Global Corp. (Citizen Identity Solutions)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Forgery and Counterfeiting

- 4.2.2 Growing Circulation of High-Denomination Banknotes in Emerging Markets

- 4.2.3 Adoption of Polymer Banknote Substrates for Durability and Security

- 4.2.4 Government Mandates for Secure IDs and E-Passports

- 4.2.5 AI-Enabled Inline Inspection Reduces Spoilage

- 4.2.6 Central-Bank "Green Banknote" Sustainability Programs

- 4.3 Market Restraints

- 4.3.1 Shift Toward Cashless Payments and CBDCs

- 4.3.2 High Capex for Next-Gen Security Presses

- 4.3.3 Shortages of Specialty Security Inks and Substrates

- 4.3.4 Carbon-Footprint Scrutiny of Currency Production

- 4.4 Industry Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Banknotes

- 5.1.2 Payment Cards

- 5.1.3 Cheques

- 5.1.4 Personal Identification Documents

- 5.1.5 Ticketing and Transit Passes

- 5.1.6 Postage and Fiscal Stamps

- 5.1.7 Brand-Protection and Tax Banderoles

- 5.2 By Security Feature

- 5.2.1 Security Inks (UV, OVI, Optically Variable)

- 5.2.2 Holograms and DOVIDs

- 5.2.3 Watermarks and Security Threads

- 5.2.4 RFID and NFC Tags

- 5.2.5 Track-and-Trace Serialisation

- 5.3 By Printing Technology

- 5.3.1 Intaglio

- 5.3.2 Offset/Lithography

- 5.3.3 Screen and Flexo

- 5.3.4 Digital Inkjet

- 5.3.5 Gravure

- 5.4 By Substrate

- 5.4.1 Cotton-Based Paper

- 5.4.2 Polymer

- 5.4.3 Hybrid Paper-Polymer

- 5.4.4 Synthetic and Composite Films

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia and New Zealand

- 5.5.4.5 Indonesia

- 5.5.4.6 Thailand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Giesecke+Devrient GmbH

- 6.4.2 De La Rue plc

- 6.4.3 SICPA Holding SA

- 6.4.4 Koenig and Bauer AG

- 6.4.5 CCL Secure Pty Ltd

- 6.4.6 Oberthur Fiduciaire SAS

- 6.4.7 Crane Currency (Crane NXT Co.)

- 6.4.8 Toppan Inc.

- 6.4.9 IDEMIA Group S.A.S.

- 6.4.10 Komori Corporation

- 6.4.11 Note Printing Australia Ltd

- 6.4.12 Canadian Bank Note Company, Limited

- 6.4.13 Landqart AG

- 6.4.14 Orell Fussli Holding Ltd (Orell Fussli Security Printing Ltd)

- 6.4.15 China Banknote Printing and Minting Corporation

- 6.4.16 Security Printing and Minting Corporation of India Ltd (SPMCIL)

- 6.4.17 Korea Minting, Security Printing and ID Card Operating Corp. (KOMSCO)

- 6.4.18 HID Global Corp. (Citizen Identity Solutions)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

安全印刷市場規模、佔有率和趨勢分析報告:按印刷方法、應用、地區和細分市場預測(2026-2033 年)

安全印刷市場規模、佔有率和趨勢分析報告:按印刷方法、應用、地區和細分市場預測(2026-2033 年) 安全油墨市場:2026-2032年全球市場預測(按油墨類型、技術、安全等級、應用和最終用戶分類)

安全油墨市場:2026-2032年全球市場預測(按油墨類型、技術、安全等級、應用和最終用戶分類) 全球安全印刷市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球安全印刷市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 安全印刷市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、製程、最終用戶分類

安全印刷市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、製程、最終用戶分類 全球安全印刷市場未來發展趨勢(至2030年)

全球安全印刷市場未來發展趨勢(至2030年) 安全印刷市場 - 全球產業規模、佔有率、趨勢、機會及預測(按印刷類型、應用、地區和競爭格局分類,2021-2031年)

安全印刷市場 - 全球產業規模、佔有率、趨勢、機會及預測(按印刷類型、應用、地區和競爭格局分類,2021-2031年) 安全油墨市場規模、佔有率和成長分析(按類型、印刷方法、功能、應用、最終用途產業和地區分類)-2026-2033年產業預測安全印刷市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年)全球安全印刷市場預測(2025-2030)

安全油墨市場規模、佔有率和成長分析(按類型、印刷方法、功能、應用、最終用途產業和地區分類)-2026-2033年產業預測安全印刷市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年)全球安全印刷市場預測(2025-2030) 全球安全印刷市場

全球安全印刷市場