|

市場調查報告書

商品編碼

2044188

滲透測試:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

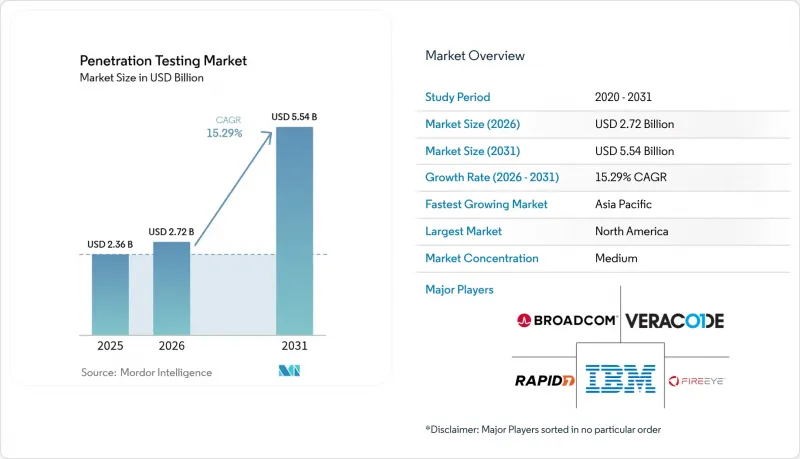

預計滲透測試市場將從 2025 年的 23.6 億美元和 2026 年的 27.2 億美元成長到 2031 年的 55.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 15.29%。

雲端工作負載的快速成長、人工智慧驅動的生成式攻擊激增以及監管合規期限的縮短,正促使滲透測試從一次性審計轉變為運作管理。企業現在將主動檢驗視為抵禦已公開漏洞的關鍵保障,因為攻擊者可能在數小時內利用這些漏洞。 HIPAA 和 PCI DSS 4.0 版的強制性年度測試,以及歐盟的《數位營運彈性法案》(DORA) 和 NIS2,正在縮短內部決策週期,並提升多年期合約的價值。供應商正在透過自主紅隊代理來應對這項挑戰,這些代理商可以將測試週期從數週縮短至數天,而與 CI/CD 管道的整合則允許開發人員在每次提交時運行測試。因此,競爭格局有利於那些能夠同時提供持續覆蓋、監管合規可見度和詳細報告功能的平台。

全球滲透測試市場趨勢及洞察

各行各業網路安全風險日益增加。

目前,漏洞揭露後數小時內即可出現公開的漏洞利用工具包,這縮短了防禦者的回應時間,也使得更頻繁的滲透測試成為必要。 Dragos 的一項研究預測,到 2026 年,將有 26 個威脅組織積極探勘營運技術 (OT),這意味著工業環境將無法再享有同等的隱藏性和安全性。在波蘭電網遭受協同攻擊後,美國網路安全和基礎設施安全局 (CISA) 呼籲關鍵基礎設施營運商進行季度測試,這表明監管機構對年度測試週期已失去耐心。 Pentera 對 500 位安全主管進行的一項調查發現,67% 的受訪者在過去一年中至少經歷過一次安全漏洞,測試預算中位數上升至 18.7 萬美元。這證實,高階主管現在將預防性檢驗視為一種保障,而非審計之外的額外環節。綜上所述,這些數據表明,威脅的加速發展正在直接推動對持續滲透測試的需求。

安全評估和合規性審計的需求日益成長

多層次的產業框架導致了強制性滲透測試要求的不斷增加,迫使各組織將多項審計整合到一個單一的程序中。 PCI DSS 4.0 版將於 2025 年 3 月生效,強制要求所有成員公司進行年度測試,並新增了先前可選的分段和無線評估。 FDA 的上市前指南要求醫療設備製造商在所有申請中包含測試結果,並保留上市後證據,其範圍已從醫院擴展到供應商。 FedRAMP 3.0 強制要求聯邦雲端提供者進行季度掃描和年度測試,而 4.0 草案提案將高影響系統的測試頻率提高一倍。紐約州修訂後的 23 NYCRR 500 規則要求董事會在 30 天內審查滲透測試結果,將測試從單純的技術操作提升為管治交付成果。這種重疊的審計促使企業尋求能夠透過單一合約滿足多項規則要求的託管服務供應商。

熟練測試人員短缺和高成本

全球對認證滲透測試人員的需求遠超過供應,導致合約費用上漲,專案等待時間延長。 ISC2 的一項調查顯示,95% 的組織機構表示網路安全人才短缺,其中攻擊性負責人是最難招募的三大職位之一。截至 2024 年,英國仍將面臨 11,200 名網路安全專業人員的缺口,而攻擊性測試人員的招募週期最長。高級 OSCP 認證的通過率仍然低於 50%,顯示學習曲線陡峭,人才儲備成長緩慢。因此,儘管企業正在轉向自動化日常運營,但在範圍界定、社交工程和攻擊後分析等方面仍需要人類的專業知識。這種持續的人才短缺限制了服務交付能力,並抑制了市場成長,儘管市場需求強勁。

細分市場分析

在2025年的滲透測試市場中,網路評估將佔據38.23%的佔有率,這表明邊界防禦和橫向移動防禦仍將是優先考慮的領域。然而,受多重雲端普及的推動,雲端滲透測試預計將以16.63%的複合年成長率成長至2031年,成為成長最快的領域。這種轉變反映了容器編排管理、無伺服器功能和以API為中心的架構等傳統網路以外的技術。 Bishop Fox於2026年將其CloudFox工具包擴展到Google Cloud Platform,顯示雲端原生測試方法已進入成熟階段。隨著攻擊者頻繁地在不同管道重複使用API和憑證填充技術,行動和Web人員編制的測試正在融合。社交工程演練現在使用深度造假音訊和影片來模擬攻擊,這一趨勢得益於生成式人工智慧。無線測試的範圍正在擴大,涵蓋工廠和物流中心的Wi-Fi 6E和5G專用網路。隨著工業資產所有者開始在沙盒環境中複製生產環境以避免停機,物聯網和營運技術 (OT) 的價值也在不斷提高。

融合網路、雲端和應用程式範圍的混合滲透測試市場正在擴張。這是因為買家傾向於簽訂一份涵蓋多個框架的單一合約。隨著合規週期的日益嚴格,提供整合儀表板和自動化複測的供應商正在贏得更多合約。人們對持續檢驗的期望也在迅速提高,Bishop Fox 的 Cosmos AI 聲稱可將評估時間縮短 40%,而 HackerOne 的代理服務則可在數小時內而非數天內報告結果。這些效率的提升使得安全團隊能夠在不增加預算的情況下安排更頻繁的測試。由於威脅行為者能夠在數小時內利用公開揭露的漏洞,企業正在從簡單地確認漏洞的存在轉向檢驗漏洞是否真的可被利用。因此,市場需求正從瞬時網路掃描轉向持續運行的雲端和運作探測,這些探測能夠直接整合到 CI/CD 管道中。

截至2025年,本地部署仍佔滲透測試市場的59.21%,因為許多受監管行業仍然傾向於本地管理。然而,在彈性擴展和與DevSecOps週期相契合的快速功能更新的推動下,雲端交付平台預計到2031年將以15.61%的複合年成長率成長。 Aikido Infinite透過讓開發人員能夠按提交執行滲透測試而無需配置伺服器,展現了SaaS產品的易用性。 PCI DSS 4.0透過明確基於雲端的測試可以滿足持卡人資料法規的要求,消除了長期存在的障礙。如今,混合環境已成為企業架構的主流,因此對雲端工作負載和本地資產的可見性至關重要。

在因主權法規而切斷外部連接的政府和國防網路中,本地滲透測試市場仍然強勁。即使在這樣的環境下,供應商也提供虛擬設備,以便在網路連線恢復後同步匿名化的測試結果。在更廣泛的市場中,訂閱定價模式正將支出從資本支出轉移到營運預算,並簡化核准流程。託管服務供應商擴大將雲端測試儀表板與滿足董事會層級報告要求的口頭報告捆綁在一起。買家也非常欣賞透過 REST API 將測試結果直接匯入工單管理系統的功能,這加快了修補程式檢驗。隨著持續配置的日益普及,企業不再僅僅將基於雲端的交付視為一種選擇,而是將其視為預設選項,除非法規禁止。

區域分析

預計到2025年,北美將佔據滲透測試市場38.27%的佔有率。這得歸功於HIPAA、PCI DSS 4.0和FedRAMP等成熟的法規結構,這些框架正式定義了年度或半年一次的測試週期。美國金融機構正在將威脅主導測試整合到其營運彈性計畫中,而加拿大醫療保健隱私法規則鼓勵醫院實施持續檢驗。墨西哥快速發展的金融科技生態系統也透過將滲透測試整合到跨境支付許可中,擴大了區域需求。創業投資資金集中在矽谷和波士頓,促使當地平台供應商持續開發人工智慧代理,以縮短國內客戶的測試週期。因此,北美仍然是新工具和服務模式的標竿市場。

亞太地區的滲透測試市場預計到2031年將以16.26%的複合年成長率成長,成為所有地區中成長最快的市場。在印度,網路安全人才缺口高達30%至50%,促使企業採用自動化平台。同時,在中國,資料本地化法規要求所有處理個人資訊的系統都必須在國內進行測試。日本修訂後的《個人資訊保護法》和韓國的關鍵基礎設施法規進一步將年度測試納入企業治理。印尼和菲律賓數位支付的快速普及凸顯了對連接到區域閘道器的小規模商家進行檢驗的必要性。這些因素共同推動了市場需求的激增,促使全球供應商在其所在區域提供基於雲端的存取點(PoP)和在地化報告服務。

在歐洲,數位營運彈性法案 (Digital Operational Resilience Act)、NIS2 以及即將訂定的網路彈性法案 (Cyber silience Act) 已確立了最低合規標準,將滲透測試從最佳實踐提升為法律義務。德國聯邦資訊安全辦公室 (BSI) 將於 2025 年發布針對關鍵基礎設施的行業特定指南,法國已擴展其 SecNumCloud 框架,將服務供應商的強制性測試納入其中。英國國家網路安全中心 (NCSC) 建議所有處理敏感資料的公司進行年度測試,以使英國脫歐後的標準與歐洲大陸的規範保持一致。南美洲、中東和非洲正成為充滿潛力的市場,巴西的資料保護法和海灣國家的國家網路安全計畫已將攻擊性測試納入其許可製度。因此,地理擴張的整體速度將取決於各司法管轄區法規從「指南」到「強制執行」的進展速度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網路安全風險正在各領域不斷上升。

- 安全評估和合規性審計的需求日益成長

- 政府指令和特定產業法規

- DevSecOps 流程需要整合持續滲透測試。

- 人工智慧驅動的自主紅隊演練可實現持續檢驗。

- 強制使用軟體材料清單(SBOM) 擴大了供應鏈滲透測試的範圍。

- 市場限制因素

- 中小企業缺乏意識

- 熟練測試人員短缺和高成本

- 在關鍵的職業治療環境中,現實世界環境中濫用行為的倫理限制

- 在跨多個司法管轄區的雲端環境中,法律責任缺乏明確性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按測試類型

- 網路滲透測試

- Web應用程式滲透測試

- 行動應用滲透測試

- 社交工程滲透測試

- 無線網路滲透測試

- 雲端滲透測試

- 其他測試類型

- 按部署模式

- 現場

- 基於雲端的

- 按組織規模

- 大公司

- 小型企業

- 按服務交付方式

- 內部測試團隊

- 第三方管理服務

- 按最終用戶行業分類

- 政府/國防

- 銀行、金融服務、保險

- 資訊科技/通訊

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 能源與公共產業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性措施與資金籌措

- 市佔率分析

- 公司簡介

- IBM Corporation

- Rapid7 Inc.

- Synopsys Inc.

- Checkmarx Ltd.

- Acunetix Ltd.

- Broadcom Inc.

- FireEye Inc.

- Veracode Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Palo Alto Networks Inc.

- Offensive Security LLC

- Core Security Technologies Inc.

- Pentera Security Ltd.

- HackerOne Inc.

- Trustwave Holdings Inc.

- IOActive Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox Inc.

第7章 市場機會與未來展望

The penetration testing market size is projected to expand from USD 2.36 billion in 2025 and USD 2.72 billion in 2026 to USD 5.54 billion by 2031, registering a CAGR of 15.29% between 2026 to 2031.

Rapid adoption of cloud workloads, a sharp rise in generative-AI driven exploits, and compressed regulatory deadlines are moving penetration testing from ad-hoc audits to an always-on control. Enterprises now treat proactive validation as essential insurance against publicly disclosed vulnerabilities that adversaries weaponize within hours. Mandatory annual tests under HIPAA and PCI DSS version 4.0, along with the European Union's Digital Operational Resilience Act and NIS2, have shortened internal decision cycles and lifted multi-year contract values. Vendors are responding with autonomous red-team agents that cut test duration from weeks to days, while integration with CI/CD pipelines enables developers to trigger tests at every commit. Competitive dynamics, therefore, favor platforms that combine continuous coverage, regulatory mapping, and granular reporting.

Global Penetration Testing Market Trends and Insights

Rising Cybersecurity Risks Across Sectors

Public exploit kits now appear within hours of vulnerability disclosure, shrinking defenders' reaction windows and forcing more frequent penetration tests. Dragos counted 26 threat groups actively probing operational technology in 2026, showing that industrial environments no longer enjoy obscurity or safety. After a coordinated attack on Poland's energy grid, CISA urged quarterly testing for critical infrastructure operators, signaling regulatory impatience with annual testing cycles. A Pentera survey of 500 security leaders found 67% suffered at least one breach in the prior year and raised testing budgets to a median of USD 187,000, confirming that executives now treat proactive validation as insurance rather than an audit luxury. Together, these data points illustrate how escalating threat velocity directly expands demand for continuous penetration testing.

Increasing Demand for Security Assessments and Compliance Audits

Layered industry frameworks are stacking mandatory penetration-testing clauses, compelling organizations to synchronize multiple audits into one program. PCI DSS version 4.0, effective March 2025, requires annual testing for all merchants, plus segmentation and wireless assessments that were previously optional. FDA pre-market guidance obliges medical-device makers to include test results in every submission and maintain post-market evidence, widening the scope beyond hospitals to their suppliers. FedRAMP 3.0 requires quarterly scanning and annual testing for federal cloud providers, with a draft 4.0 proposal to double the cadence for high-impact systems. New York's amended 23 NYCRR 500 rule requires boards to review penetration-testing findings within 30 days, elevating tests from technical exercises to governance artifacts. These overlapping audits drive enterprises toward managed service providers that can map a single engagement to multiple rulebooks.

Shortage and High Cost of Skilled Testers

Global demand for certified penetration testers far exceeds supply, driving up engagement fees and lengthening project queues. ISC2 found that 95% of organizations report cybersecurity staffing gaps, ranking offensive testing among the three hardest roles to fill. The United Kingdom still needed 11,200 additional cybersecurity workers in 2024, with offensive roles taking the longest to hire. Pass rates for advanced OSCP credentials remain below 50%, underscoring steep learning curves and slow growth in the talent pipeline. Enterprises, therefore, turn to automation for routine tasks, yet scoping, social engineering, and post-exploitation analysis still require human expertise. The persistent talent deficit caps service capacity and tempers market growth despite strong demand.

Other drivers and restraints analyzed in the detailed report include:

- Government Mandates and Industry-Specific Regulations

- DevSecOps Pipelines Require Continuous Pen-Testing Integration

- Lack of Awareness Among SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network assessments held a 38.23% market share in penetration testing in 2025, underscoring the continued priority of perimeter and lateral-movement defenses. Yet cloud penetration testing, propelled by multi-cloud adoption, is projected to advance at a 16.63% CAGR through 2031, making it the fastest-growing modality. The shift reflects container orchestration, serverless functions, and API-centric architectures that fall outside traditional network scopes. Bishop Fox expanded its CloudFox toolkit to Google Cloud Platform in 2026, signaling maturity in cloud-native testing methods. Mobile and web application tests are converging because adversaries frequently reuse API and credential-stuffing tactics across channels. Social-engineering exercises now simulate deepfake voice and video attacks, a trend made possible by generative AI. Wireless testing widens to cover Wi-Fi 6E and 5G private networks in factories and logistics hubs. IoT and operational technology assessments grow as industrial asset owners replicate production environments in sandboxes to avoid downtime.

The penetration testing market size for hybrid engagements that bundle network, cloud, and application scopes is growing, as buyers prefer a single contract that spans multiple frameworks. Vendors that offer unified dashboards and automated retesting win deals as compliance cycles tighten. Continuous validation expectations are rising quickly; Bishop Fox's Cosmos AI claims a 40% reduction in assessment time, while HackerOne's agentic service delivers findings within hours rather than days. These efficiency gains let security teams schedule more frequent tests without escalating budgets. As threat actors weaponize disclosed flaws in hours, enterprises gravitate toward modalities that confirm exploitability, not just vulnerability presence. Consequently, demand migrates from point-in-time network sweeps to always-on cloud and application probes that integrate directly into CI/CD pipelines.

On-premises deployments commanded 59.21% of the penetration testing market share in 2025, as many regulated sectors still favor on-premises control. However, cloud-delivered platforms are set to grow at a 15.61% CAGR to 2031, fueled by elastic scaling and rapid feature updates that align with DevSecOps cycles. Aikido Infinite lets developers trigger penetration tests on every commit without provisioning servers, illustrating the operational ease of SaaS delivery. PCI DSS 4.0 clarified that cloud-based tests satisfy cardholder data rules, removing a lingering barrier. Hybrid environments now dominate enterprise architectures, so visibility into both cloud workloads and on-premise assets becomes essential.

The penetration testing market for on-prem tools remains resilient in air-gapped government and defense networks, where sovereignty rules block external connectivity. Even there, vendors ship virtual appliances that synchronize anonymized findings once links are available. For the broader market, subscription pricing moves expenditure from capital to operating budgets, simplifying approvals. Managed service providers increasingly bundle cloud testing dashboards with verbal readouts that satisfy board-level reporting. Buyers also cite quicker patch validation when test results are fed directly into ticketing systems via REST APIs. As continuous deployment normalizes, organizations view cloud delivery not as an option but as the default unless a statute forbids it.

The Penetration Testing Market Report is Segmented by Testing Type (Cloud Penetration Testing, and More), Deployment Model (On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (IT and Telecom, Manufacturing, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.27% penetration testing market share in 2025, anchored by mature regulatory frameworks such as HIPAA, PCI DSS 4.0, and FedRAMP that formalize annual or semiannual testing cadences. U.S. financial institutions bundle threat-led testing into operational resilience programs, while Canadian health-privacy statutes drive hospitals to adopt continuous validation. Mexico's fast-growing fintech ecosystem also embeds penetration testing into cross-border payment licenses, widening regional demand. Venture funding is concentrated in Silicon Valley and Boston, allowing local platform vendors to iterate on AI agents that shorten test cycles for domestic clients. As a result, North America remains the reference market for new tooling and service models.

Asia-Pacific is forecast to expand its penetration testing market size at a 16.26% CAGR through 2031, the fastest regional trajectory. India's 30% to 50% cyber-talent gap encourages enterprises to adopt automated platforms, while data-localization rules in China compel in-country testing of all systems that handle personal information. Japan's revised Act on the Protection of Personal Information and South Korea's critical infrastructure mandates further hardwire annual testing into corporate governance. Rapid digital-payment adoption in Indonesia and the Philippines underscores the need for validation for small merchants connecting to regional gateways. Together, these factors create a demand surge that helps global vendors justify in-region cloud PoPs and local language reporting.

Europe benefits from a compliance floor established by the Digital Operational Resilience Act, NIS2, and the forthcoming Cyber Resilience Act, which collectively elevate penetration testing from best practice to a legal duty. Germany's BSI released sector playbooks for critical infrastructure in 2025, and France expanded its SecNumCloud framework to include mandatory testing for service providers. The United Kingdom's National Cyber Security Centre recommends annual tests for any firm handling sensitive data, to keep post-Brexit standards aligned with continental norms. South America, the Middle East, and Africa are emerging as strong markets as Brazil's data-protection law and Gulf national cyber programs embed offensive testing into licensing regimes. Overall geographic expansion is therefore paced by how quickly statutes migrate from guidance to enforcement across each jurisdiction.

- IBM Corporation

- Rapid7 Inc.

- Synopsys Inc.

- Checkmarx Ltd.

- Acunetix Ltd.

- Broadcom Inc.

- FireEye Inc.

- Veracode Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Palo Alto Networks Inc.

- Offensive Security LLC

- Core Security Technologies Inc.

- Pentera Security Ltd.

- HackerOne Inc.

- Trustwave Holdings Inc.

- IOActive Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cybersecurity Risks Across Sectors

- 4.2.2 Increasing Demand for Security Assessments and Compliance Audits

- 4.2.3 Government Mandates and Industry-Specific Regulations

- 4.2.4 DevSecOps Pipelines Require Continuous Pen-Testing Integration

- 4.2.5 AI-Driven Autonomous Red Teaming Enables Continuous Validation

- 4.2.6 Software Bill of Materials Mandates Expand Supply-Chain Pentest Scope

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness Among SMEs

- 4.3.2 Shortage and High Cost of Skilled Testers

- 4.3.3 Ethical Constraints on Live Exploitation of Critical OT Environments

- 4.3.4 Unclear Legal Liability in Multi-Jurisdiction Cloud Environments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Testing Type

- 5.1.1 Network Penetration Testing

- 5.1.2 Web Application Penetration Testing

- 5.1.3 Mobile Application Penetration Testing

- 5.1.4 Social Engineering Penetration Testing

- 5.1.5 Wireless Network Penetration Testing

- 5.1.6 Cloud Penetration Testing

- 5.1.7 Other Testing Types

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Service Delivery Mode

- 5.4.1 In-House Testing Teams

- 5.4.2 Third-Party Managed Services

- 5.5 By End-User Industry

- 5.5.1 Government and Defense

- 5.5.2 Banking, Financial Services and Insurance

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Rapid7 Inc.

- 6.4.3 Synopsys Inc.

- 6.4.4 Checkmarx Ltd.

- 6.4.5 Acunetix Ltd.

- 6.4.6 Broadcom Inc.

- 6.4.7 FireEye Inc.

- 6.4.8 Veracode Inc.

- 6.4.9 Qualys Inc.

- 6.4.10 Tenable Holdings Inc.

- 6.4.11 Palo Alto Networks Inc.

- 6.4.12 Offensive Security LLC

- 6.4.13 Core Security Technologies Inc.

- 6.4.14 Pentera Security Ltd.

- 6.4.15 HackerOne Inc.

- 6.4.16 Trustwave Holdings Inc.

- 6.4.17 IOActive Inc.

- 6.4.18 NCC Group plc

- 6.4.19 Cofense Inc.

- 6.4.20 Bishop Fox Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

穿透測試市場-2026-2032年全球市場預測

穿透測試市場-2026-2032年全球市場預測 全球穿透測試市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球穿透測試市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 穿透測試市場:依測試類型、服務類型、攻擊面、組織規模、部署模式、產業和地區分類-預測至2031年

穿透測試市場:依測試類型、服務類型、攻擊面、組織規模、部署模式、產業和地區分類-預測至2031年 穿透測試市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類滲透測試市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034年)社交工程測試服務市場:服務類型、組織規模、交付模式、參與類型、測試頻率、產業垂直領域、全球預測(2026-2032 年)

穿透測試市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類滲透測試市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034年)社交工程測試服務市場:服務類型、組織規模、交付模式、參與類型、測試頻率、產業垂直領域、全球預測(2026-2032 年) 穿透測試市場規模、佔有率和成長分析(按產品/服務、組織規模、測試方法和地區分類)-2026-2033年產業預測

穿透測試市場規模、佔有率和成長分析(按產品/服務、組織規模、測試方法和地區分類)-2026-2033年產業預測 全球滲透測試和道德駭客服務市場規模、佔有率、行業分析報告(按部署模式、服務模型、滲透測試類型、最終用途行業、區域展望和預測,2025 年至 2032 年)

全球滲透測試和道德駭客服務市場規模、佔有率、行業分析報告(按部署模式、服務模型、滲透測試類型、最終用途行業、區域展望和預測,2025 年至 2032 年) 2025-2029年全球穿透測試市場

2025-2029年全球穿透測試市場 穿透測試市場評估:零組件·部署模式·類型·企業規模·終端用戶產業·各地區的機會及預測 (2018-2032年)

穿透測試市場評估:零組件·部署模式·類型·企業規模·終端用戶產業·各地區的機會及預測 (2018-2032年)