|

市場調查報告書

商品編碼

2044181

印度金屬加工產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Metal Fabrication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

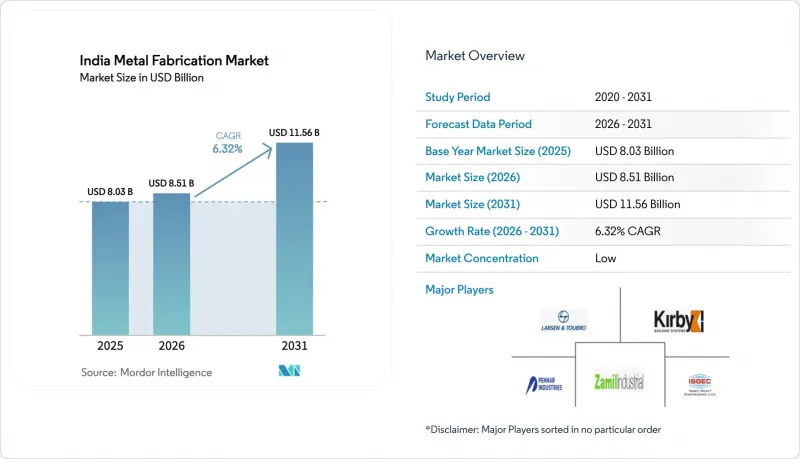

印度金屬加工市場預計將從 2025 年的 80.3 億美元成長到 2026 年的 85.1 億美元,到 2031 年達到 115.6 億美元,2026 年至 2031 年的複合年成長率為 6.32%。

這一成長反映了公共部門資本形成能力的增強和鋼鐵產能的全面復甦。截至2025年11月,國內粗鋼產量達2.35億噸,但政策目標仍為2030年達到3億噸。大規模公共工程項目支撐著對結構鋼、鐵路系統和車站基礎設施的多年需求,同時國防領域的國內產量也在成長,導致訂單轉向具有更嚴格可追溯性的認證供應商。資料中心部署和能源轉型專案的擴張推動了對模組化機架、夾具和壓力容器的訂單,進而刺激了對焊接品質和耐腐蝕塗層的投資。出口導向生產商正在為歐盟碳邊境調節機制(CBAM)做準備,該機制將於2026年1月1日生效,要求轉向低排放路線,並提高隱含排放的文件標準。

印度金屬加工市場趨勢與洞察

可再生能源原始設備製造商在風力塔和太陽能移動製造系統中的本地化

為降低供應鏈風險,一系列措施和政策獎勵正推動組件製造(包括組件、塔架和安裝系統)回歸國內市場。 「核准模型製造商名錄」和「基本關稅」的實施促進了國內生產,使光學模組)、追蹤器和鍍鋅結構的穩定訂單。風力發電機組件產能已接近18吉瓦,隨著沿海和高風速地區新塔架製造商名錄的製定、焊接標準和認證要求的提高,國產化進程進一步加強。 「國家綠色氫能計畫」已撥款146.6億盧比用於電解槽一體化,並將精密框架和高壓容器納入認證工廠的範圍(如括號內所示,原文為146.6億盧比,約合1.767億美元)。隨著長壽命太陽能和風能發電設備的出現,買家擴大轉向使用預鍍鋅或熱浸鍍鋅鋼材以及高等級緊固件,以延長高鹽高濕地區建築物的使用壽命。這推高了單位成本,但同時也減少了現場故障。自2026年9月起,印度標準局(BIS)的X方案將強制要求某些大型電氣設備和安裝設備進行國內認證。這將迫使那些落後的小規模工廠要么加強其內部測試能力,要么退出關鍵供應鏈。

Ghati Shakti 和 NIP 的基礎設施超級週期

公共投資在2025-2026會計年度維持強勁勢頭,資本支出達11.21兆盧比,並向各邦提供1.5兆盧比的50年期無息貸款,用於基礎建設。這些資金將用於支持鋼鐵密集型公路、鐵路和城市交通項目,以括號內所示外匯計算,分別相當於1,351億美元和181億美元(括號內為當前匯率)。公路運輸和公路部在2026會計年度撥款28.7兆盧比用於擴建國家公路網,以括號內所示匯率計算,相當於346億美元(28.7兆盧比,346億美元)。印度鐵路公司在2026會計年度投入創紀錄的2.652兆盧比用於資本投資,優先用於車輛和車站的現代化改造以及走廊運力的擴建,這推動了對認證結構製造的需求成長。這相當於319億美元(2,652,000印度盧比,319億美元),括號內為原始數字。地鐵專案是支撐複雜鋼骨訂單的重要支柱,這些訂單需要更高的焊接標準和嚴格的文件記錄。其中包括印多爾地鐵段,該項目已於2025年授予一個大型財團,合約金額為218.9億盧比,括號內為2.637億美元的美元訂單(2,189印度盧比,2.637億美元)。這些訂單維持了印度金屬加工市場多年的訂單儲備,從而提高了產能運轉率,並推動了對先進切割、成型和檢測系統的投資。

與鋁和鋼鐵出口相關的碳排放合規成本

歐盟碳邊境調節機制(CBAM)將於2026年1月1日全面實施。這意味著歐盟進口商將購買與目標產品排放掛鉤的CBAM證書。鑑於印度粗鋼的排放強度約為每噸2.55噸二氧化碳,如果生產商不降低排放強度以達到歐洲基準,將會出現顯著的價格差異,這將給高爐煉鋼製程帶來壓力。印度對歐盟的鋼鐵和鋁出口額已從2024會計年度的77.1億美元下降至2025會計年度的58.2億美元,顯示這對出口導向鋼鐵廠和下游供應商構成風險。分析估計,印度每年的CBAM負擔約為10億至25億美元,其中鋼鐵出口占其出口的大部分。這將使引入以廢鋼為燃料的電爐(EAF)和使用可再生能源的現場發電變得更加重要。對於許多出口商而言,制定測量、報告和檢驗(MRV) 計劃是一項新的要求,而具有記錄在案的低排放原料的價值正在印度金屬加工市場中不斷成長。

細分市場分析

到2025年,機械加工將佔服務型銷售額的34.28%,並將繼續成為電力、石油天然氣和國防等產業高精度加工的基礎。在這些行業中,尺寸公差和表面光潔度目標決定了印度金屬加工市場的製程選擇。買家經常要求檢驗可追溯性和正式的流程控制,這推動了對具備線上測量功能並能與數位化品質系統整合的先進加工中心的需求。規範的供應商正在調整產能以匹配長週期資本訂單,優先考慮運轉率以及對PQR和WPS協議的遵守情況,從而確保穩定的產量。持續投資於自動化和維護的服務供應商往往擁有較高的機器運轉率和穩定的準時交付率,這使其在印度金屬加工市場中保持了領先地位。 ISO 3834-2和EN 1090等認證系統透過將焊接品質和結構部件符合性納入一級買家的採購清單,進一步推動了這一趨勢。

隨著塔架、追蹤器框架和國防結構對焊接品質的要求日益提高,預計到2031年,焊接市場將以7.34%的複合年成長率成長,從而提升焊接工藝在印度金屬加工市場的價值。可預見的風能和太陽能發電裝置組裝製程需求傾向於潛弧焊接和機器人MIG焊接單元,而國防和鐵路相關組件則需要經過認證的TIG焊接和專用耗材來焊接較厚的零件。整合供應商利用離線夾具、焊接定位器和最終檢驗記錄來支援大規模生產,並確保各批次輪胎邊緣品質的一致性。記錄層間溫度、熱輸入和焊接後後處理的工廠能夠提供更完善的文檔,並減少審核中不合格報告(NCR)的出現。這縮短了周期時間,並減少了大型組件的返工。在預測期內,服務導向的專業化將在印度金屬加工市場繼續佔據主導地位,因為機械加工將專注於高精度加工,而焊接將在可再生能源和鐵路車輛組裝獲得更大的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基礎設施超級週期(Ghati Shakti,NIP)刺激了對結構鋼的需求。

- 可再生能源原始設備製造商(風力塔、太陽能移動儲存系統)的在地化

- 國防領域的補償合約加速了精密加工。

- 資料中心的快速成長正在推動大規模模組化製造。

- 對更輕型電動車和電池組的需求,催生了對鋁製子組件的需求。

- 綠色鋼鐵採購義務(自2026會計年度起公開採購)

- 市場限制因素

- 煉焦用進口煤價格波動

- 中小微型企業電力供應瓶頸

- 品質保證系統的碎片化限制了出口準備工作。

- 與鋁和鋼鐵出口相關的碳排放合規成本

- 價值/供應鏈分析

- 政府法規和重點舉措

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 近期全球動盪對印度金屬加工市場的影響

第5章 市場規模及成長預測(價值,十億美元)

- 按服務類型

- 切割

- 成型/彎曲

- 焊接

- 加工

- 沖壓/沖壓

- 表面處理/精加工

- 其他(組裝等)

- 材料

- 碳鋼

- 不銹鋼和合金鋼

- 鋁

- 其他材質(銅、黃銅、特殊合金、金屬薄板(冷軋鋼板、鍍鋅鋼板、熱軋鋼板))

- 按最終用戶行業分類

- 建築和基礎設施

- 汽車及汽車零件

- 鐵路和地鐵

- 電力/公共產業

- 航太/國防

- 石油、天然氣和煉油廠

- 海洋/造船

- 製造業 - 重型機械/耐久性消費品

- 其他(合約製造、農業機械、電氣設備、耐用消費品等)

- 按地區

- 印度西部(馬哈拉斯特拉邦、古吉拉突邦、果阿邦)

- 南印度(泰米爾納德邦、卡納塔克邦、特倫甘納邦、安得拉邦、喀拉拉邦)

- 印度北部(新德里、哈里亞納邦、旁遮普邦、北方邦、北阿坎德邦、喜馬偕爾邦、拉賈斯坦邦)

- 印度東部(西孟加拉邦、賈坎德邦、奧裡薩邦、比哈爾邦、恰蒂斯加爾邦)

- 印度中部(中央邦和恰蒂斯加爾邦部分地區)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Larsen & Toubro Ltd

- Kirby Building Systems India

- Zamil Industrial Investment Co.

- ISGEC Heavy Engineering Ltd

- Pennar Industries Ltd

- Salasar Techno Engineering Ltd

- JSW Severfield Structures Ltd

- Godrej Process Equipment

- Diamond Engineering(India)Pvt Ltd

- TEMA India Ltd

- Novatech Projects(India)Pvt Ltd

- Karamtara Engineering Pvt Ltd

- Bharat Heavy Electricals Ltd(Fabrication Div.)

- Tata Projects Ltd

- Welspun Corp Ltd

- Hindustan Dorr-Oliver Ltd

- Jindal Stainless-Fabrication Unit

- Bharat Forge Ltd(Fabrication Business)

- Essar Heavy Engineering Services

- Techno-Fab Engineering Ltd

第7章 市場機會與未來展望

The India Metal Fabrication Market size is expected to increase from USD 8.03 billion in 2025 to USD 8.51 billion in 2026 and reach USD 11.56 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

Growth reflects stronger public capital formation and a broad rebound in steel capacity, as domestic crude steel reached 235 million tonnes by November 2025, while policy targets still point to 300 million tonnes by 2030. Large public programs are sustaining multi-year demand for structural steel, rail systems, and station infrastructure, and defence indigenization has lifted domestic output and shifted orders toward certified suppliers with tighter traceability. Rising data center deployments and energy transition projects are pulling orders for modular racks, mounting structures, and pressure vessels, which is prompting investment in welding quality and corrosion-resistant coatings. Export-facing producers are preparing for the EU's Carbon Border Adjustment Mechanism from January 1, 2026, which raises the need for lower-emission routes and higher documentation standards on embedded emissions.

India Metal Fabrication Market Trends and Insights

Renewable-Energy OEM Localization For Wind Towers And Solar MMS

Defense against supply chain risk and policy incentives are bringing component manufacturing onshore across modules, towers, and mounting systems. Solar module manufacturing capacity nearly doubled from 38 GW in March 2024 to 74 GW by March 2025 as the Approved List of Models and Manufacturers and Basic Customs Duty supported domestic build-out, translating to steady orders for MMS, trackers, and galvanized structures. Wind turbine component capacity stands near 18 GW, and localization is reinforced by new lists that raise the bar on welding standards and certification for tower makers that serve coastal and high-wind sites. The National Green Hydrogen Mission has earmarked INR 14.66 billion for electrolyzer integration, which pulls precision frames and high-pressure vessels into the workload of certified shops, equal to USD 176.7 million in parentheses next to the original value (INR 14.66 billion, USD 176.7 million). Long-life solar and wind assets are shifting buyers toward pre-galvanized or hot-dip galvanized steel and higher-grade fasteners to extend structure life in saline and humid zones, increasing unit value while reducing field failures. From September 2026, BIS Scheme-X will demand domestic certification on specified heavy electrical and mounting equipment, which will push lagging small shops to upgrade in-house testing or exit sensitive supply chains.

Infrastructure Super-Cycle with Gati Shakti And NIP

Public investment has sustained momentum into FY 2025-26 with INR 11.21 lakh crore in capital expenditure and a 50-year interest-free loan of INR 1.5 lakh crore to states for infrastructure, which together support steel-intensive highways, rail, and urban transit programs, equal to USD 135.1 billion and USD 18.1 billion respectively at the prevailing exchange rate in parentheses next to the original values (INR 11.21 lakh crore, USD 135.1 billion) and (INR 1.5 lakh crore, USD 18.1 billion). The Ministry of Road Transport and Highways allocated INR 2.87 lakh crore for FY26 to expand the national highway network, equal to USD 34.6 billion in parentheses next to the original value (INR 2.87 lakh crore, USD 34.6 billion). Indian Railways' record capex of INR 2,65,200 crore for FY26 prioritizes rolling stock, station moder nization, and corridor capacity additions that intensify demand for certified structural fabrication, equal to USD 31.9 billion in parentheses next to the original value (INR 2,65,200 crore, USD 31.9 billion). Metro rail packages are anchoring complex steelwork orders that require higher welding standards and stronger documentation, including an underground stretch in Indore awarded to a large consortium during 2025 at an order value of INR 2,189 crore, equal to USD 263.7 million in parentheses next to the original value (INR 2,189 crore, USD 263.7 million). These commitments keep the India metal fabrication market aligned with multi-year pipelines, which support capacity utilization and encourage investment in advanced cutting, forming, and inspection systems.

CBAM-Linked Carbon-Compliance Cost on Aluminum and Steel Exports

The EU's Carbon Border Adjustment Mechanism enters full financial enforcement on January 1, 2026, which means EU importers will purchase CBAM certificates linked to embedded emissions in covered goods. Indian crude steel emission intensity near 2.55 tonnes CO2 per tonne implies a sizable price wedge if producers do not reduce emissions intensity toward European benchmarks, which puts pressure on blast furnace routes. India's steel and aluminium shipments to the EU already fell from USD 7.71 billion in FY24 to USD 5.82 billion in FY25, signaling exposure for export-oriented mills and downstream suppliers. Analytical estimates put annual CBAM liability for India near USD 1-2.5 billion, with iron and steel accounting for most covered exports, which strengthens the case for scrap-based EAFs and renewable captive power. Planning for measurement, reporting, and verification is a new requirement for many exporters, which increases the value of documented, lower-emission inputs across the India metal fabrication market.

Other drivers and restraints analyzed in the detailed report include:

- Defence Offsets and Indigenization Lifting Precision Fabrication

- Data-Center Build-Out Driving Heavy Modular Fabrication

- MSME Power-Supply Bottlenecks and Cost Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Machining held 34.28% of the 2025 service-type revenue and continues to anchor high-precision workload in power, oil and gas, and defence, where dimensional tolerance and surface finish targets dictate process choice in the India metal fabrication market. Buyers frequently require inspection traceability and formal process control, which sustains demand for advanced machining centers with in-line metrology, and encourages integration with digital quality systems. Organized suppliers align capacity around long-cycle capital orders that prioritize uptime and adherence to PQR and WPS protocols, which stabilizes throughput. Service providers with sustained investments in automation and maintenance tend to report higher machine utilization and consistent delivery performance, which maintains their position in the India metal fabrication market. Certification regimes like ISO 3834-2 and EN 1090 support this profile by embedding welding quality and structural component compliance into the sourcing checklist for tier-1 buyers.

Welding is projected to expand at a 7.34% CAGR through 2031 as tower sections, tracker frames, and defense structures introduce higher welding-quality expectations, which raises the process value within the India metal fabrication market. Predictable demand from wind and solar assembly runs favors submerged arc and robotic MIG cells, while defense and rail packages pull in certified TIG and specialized consumables for thicker sections. Integrated suppliers use offline fixtures, weld-positioners, and end-of-line inspection records to support serial production and to maintain consistent bead quality across batches. Shops that record interpass temperature, heat input, and post-weld treatment provide stronger documentation and face fewer NCRs in audits, which shortens cycle time and reduces rework on large modules. Over the forecast period, service-type specialization will remain visible as machining concentrates on high-precision workloads and welding absorbs a larger share of renewable and rolling-stock assemblies within the India metal fabrication market.

The India Metal Fabrication Market is Segmented by Service Type (Cutting, and Others), by Material (Carbon Steel, and Others), by End-User Industry (Construction & Infrastructure, and Others), and by Region (Western India, Southern India, Northern India, Eastern India, and Central India). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Larsen & Toubro Ltd

- Kirby Building Systems India

- Zamil Industrial Investment Co.

- ISGEC Heavy Engineering Ltd

- Pennar Industries Ltd

- Salasar Techno Engineering Ltd

- JSW Severfield Structures Ltd

- Godrej Process Equipment

- Diamond Engineering (India) Pvt Ltd

- TEMA India Ltd

- Novatech Projects (India) Pvt Ltd

- Karamtara Engineering Pvt Ltd

- Bharat Heavy Electricals Ltd (Fabrication Div.)

- Tata Projects Ltd

- Welspun Corp Ltd

- Hindustan Dorr-Oliver Ltd

- Jindal Stainless - Fabrication Unit

- Bharat Forge Ltd (Fabrication Business)

- Essar Heavy Engineering Services

- Techno-Fab Engineering Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure super-cycle (Gati Shakti, NIP) unleashing structural-steel demand

- 4.2.2 Renewable-energy OEM localisation (wind towers, solar MMS)

- 4.2.3 Defence offsets accelerating precision fabrication

- 4.2.4 Data-center boom driving heavy modular fabrication

- 4.2.5 EV & battery-pack light-weighting creating aluminium sub-assembly demand

- 4.2.6 Green-steel procurement mandates (public tenders from FY-26)

- 4.3 Market Restraints

- 4.3.1 Imported coking-coal cost volatility

- 4.3.2 MSME power-supply bottlenecks

- 4.3.3 Fragmented quality-assurance ecosystem limits export readiness

- 4.3.4 CBAM-linked carbon-compliance cost for aluminium/steel exports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Government Regulations & Key Initiatives

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Recent Global Disruptions on the India Metal Fabrication Market

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Service Type

- 5.1.1 Cutting

- 5.1.2 Forming / Bending

- 5.1.3 Welding

- 5.1.4 Machining

- 5.1.5 Punching / Stamping

- 5.1.6 Finishing / Surface Treatment

- 5.1.7 Others (Assembling, etc.)

- 5.2 By Material

- 5.2.1 Carbon Steel

- 5.2.2 Stainless & Alloy Steel

- 5.2.3 Aluminium

- 5.2.4 Others (Copper, Brass, Specialty Alloys, Sheet Metal (CRCA, GI, HR))

- 5.3 By End-User Industry

- 5.3.1 Construction & Infrastructure

- 5.3.2 Automotive & Auto Components

- 5.3.3 Railways & Metro

- 5.3.4 Power & Utilities

- 5.3.5 Aerospace & Defence

- 5.3.6 Oil, Gas & Refinery

- 5.3.7 Marine and Shipbuilding

- 5.3.8 Manufacturing - Heavy Machinery & Consumer Durables

- 5.3.9 Others (Job shops, Agricultural Equipment, Electricals, Consumer Durables, etc)

- 5.4 By Region

- 5.4.1 Western India (Maharashtra, Gujarat, Goa)

- 5.4.2 Southern India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala)

- 5.4.3 Northern India (Delhi NCR, Haryana, Punjab, Uttar Pradesh, Uttarakhand, Himachal Pradesh, Rajasthan)

- 5.4.4 Eastern India (West Bengal, Jharkhand, Odisha, Bihar, Chhattisgarh)

- 5.4.5 Central India (Madhya Pradesh, parts of Chhattisgarh)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Larsen & Toubro Ltd

- 6.4.2 Kirby Building Systems India

- 6.4.3 Zamil Industrial Investment Co.

- 6.4.4 ISGEC Heavy Engineering Ltd

- 6.4.5 Pennar Industries Ltd

- 6.4.6 Salasar Techno Engineering Ltd

- 6.4.7 JSW Severfield Structures Ltd

- 6.4.8 Godrej Process Equipment

- 6.4.9 Diamond Engineering (India) Pvt Ltd

- 6.4.10 TEMA India Ltd

- 6.4.11 Novatech Projects (India) Pvt Ltd

- 6.4.12 Karamtara Engineering Pvt Ltd

- 6.4.13 Bharat Heavy Electricals Ltd (Fabrication Div.)

- 6.4.14 Tata Projects Ltd

- 6.4.15 Welspun Corp Ltd

- 6.4.16 Hindustan Dorr-Oliver Ltd

- 6.4.17 Jindal Stainless - Fabrication Unit

- 6.4.18 Bharat Forge Ltd (Fabrication Business)

- 6.4.19 Essar Heavy Engineering Services

- 6.4.20 Techno-Fab Engineering Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

電動開捲機市場規模、佔有率和成長分析:按類型、產能、應用、最終用途、分銷和地區分類-2026-2033年產業預測

電動開捲機市場規模、佔有率和成長分析:按類型、產能、應用、最終用途、分銷和地區分類-2026-2033年產業預測 金屬加工設備市場報告:按類型、應用和地區分類 2026-2034 年

金屬加工設備市場報告:按類型、應用和地區分類 2026-2034 年 軋輥市場:按產品類型、應用、最終用戶和地區分類

軋輥市場:按產品類型、應用、最終用戶和地區分類 繞線機市場:2026-2032年全球市場預測(按型號、材料、線圈形狀、額定輸出、最終用戶和應用分類)鈑金加工設備市場:按設備類型、技術、產業和最終用戶分類-2026-2032年全球預測特種模具及工具、模具組、夾具及固定裝置市場:依產品類型、機器類型、材料、最終用戶產業、應用及通路分類-全球預測,2026-2032年

繞線機市場:2026-2032年全球市場預測(按型號、材料、線圈形狀、額定輸出、最終用戶和應用分類)鈑金加工設備市場:按設備類型、技術、產業和最終用戶分類-2026-2032年全球預測特種模具及工具、模具組、夾具及固定裝置市場:依產品類型、機器類型、材料、最終用戶產業、應用及通路分類-全球預測,2026-2032年 全球開捲機市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球開捲機市場規模、佔有率、趨勢和成長分析報告(2026-2034) 珠寶機械市場規模、佔有率和趨勢分析報告:按產品、最終用途、運作方法、地區和細分市場預測,2026-2033年2026-2034年全球金屬加工市場規模、佔有率、趨勢和成長分析報告日本金屬加工市場規模、佔有率、趨勢及預測(依材料類型、服務類型、最終用途產業及地區分類),2026-2034年

珠寶機械市場規模、佔有率和趨勢分析報告:按產品、最終用途、運作方法、地區和細分市場預測,2026-2033年2026-2034年全球金屬加工市場規模、佔有率、趨勢和成長分析報告日本金屬加工市場規模、佔有率、趨勢及預測(依材料類型、服務類型、最終用途產業及地區分類),2026-2034年