|

市場調查報告書

商品編碼

2044179

多層陶瓷電容器(MLCC):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Multilayer Ceramic Capacitor (MLCC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

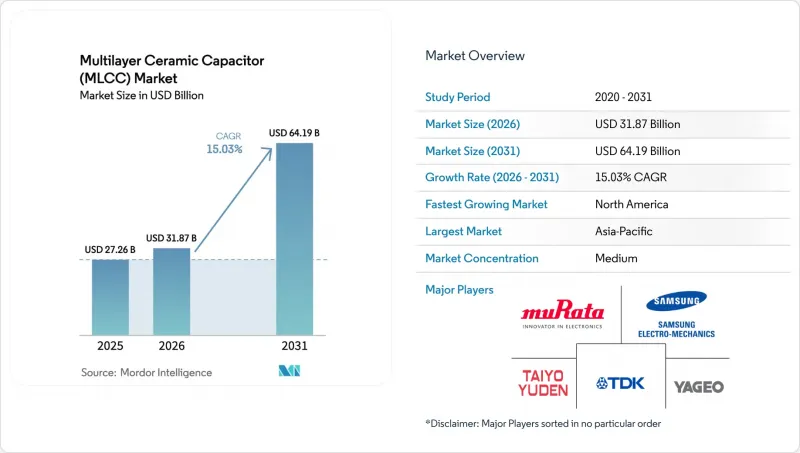

預計多層陶瓷電容器(MLCC)的市場規模將從2025年的272.6億美元和2026年的318.7億美元成長到2031年的641.9億美元,2026年至2031年的複合年成長率為15.03%。

這一成長軌跡反映了隨著汽車電氣化、人工智慧 (AI) 基礎設施和邊緣運算的整合,對被動元件的需求激增,給傳統供應鏈帶來了持續壓力。一級耐溫介電材料在安全關鍵型設計中仍然備受青睞,而 0402 封裝正成為高效能伺服器的首選封裝形式,在這些伺服器中,超低等效串聯電感比絕對面積縮小更為重要。儘管地理位置分散的海外生產正在擴大印度和東南亞的產能,但 AEC-Q200 元件漫長的認證週期導致短期供應緊張。掌握鈦酸鋇粉末和鎳電極冶金技術的垂直整合型關鍵企業保持著競爭優勢,尤其是在鎳和鈀價格波動加劇積層陶瓷電容市場成本風險的情況下。

全球積層陶瓷電容(MLCC)市場趨勢及洞察

800V電動車架構正在加速高壓MLCC的需求。

隨著汽車製造商向 800V 電池平台轉型,他們需要能夠承受超過 1000V 工作電壓的多層陶瓷電容器 (MLCC)。為此,供應商正在增加鎳鈀電極的厚度並改進亞微米級介質沉積技術。三星馬達計劃於 2025 年推出碳化矽逆變器的 2000V X7R 系列產品。同時,村田製作所的 GCM32 系列產品將 1000V 額定電壓與 100nH 的等效串聯電感結合,以抑制雜訊。 IDTechEx 預測,到 2028 年,800V 汽車將佔汽車產量的 40%,預計這將使每輛車的 MLCC 用量增加約四分之一。儘管認證瓶頸依然存在,例如汽車級壽命測試仍需在 150°C 下進行 1000 小時的測試,但克服這些挑戰的供應商能夠在多層陶瓷電容器 (MLCC) 市場以溢價銷售產品。

生成式 AI 伺服器的擴充功能將加速超低 ESL 和高 CV MLCC 的採用。

每個插槽功耗高達 700W 的推理加速器會產生電壓瞬變,因此需要將 0402 封裝的 MLCC 電容放置在距離晶片 2mm 以內的位置。 2025 年 7 月,村田製作所開始出貨 47µF 4V 0402 封裝的 MLCC 電容,該電容採用 800 層堆疊結構,厚度僅為 0.6µm。京瓷 AVX 已將其低靜電放電伺服器產品線的產能加倍,因為每個 GPU 闆卡現在最多可配備 3000 個電容,遠遠超過 CPU 系統。根據 TrendForce 預測,2025 年伺服器用 MLCC 電容的出貨量將成長 35%,遠超伺服器整體出貨量的成長速度。隨著主動層超過 600 層時故障率的增加,日本精密元件製造商與其他公司的差距正在進一步拉大。

鎳和鈀的價格波動推高了物料清單成本。

受印尼出口限制的影響,鎳價在2024年初飆升42%,隨後在2025年底回落18%。同時,受俄羅斯供應擔憂的影響,鈀金價格在每金衡盎司900至1400美元之間波動。電極金屬成本上漲10%將使成品多層陶瓷電容器(MLCC)的成本上漲3%至5%,這將給消費品產業的供應商帶來壓力,而這些供應商的年價格降幅已接近8%。 TDK表示,原物料價格飆升將使其被動元件利潤率在2026會計年度下降120個基點,從而加速銅電極的替代品。村田製作所正在重新談判其與鎳期貨價格掛鉤的季度定價條款,將部分風險轉移給其資料中心客戶。沒有避險計畫的亞洲中小型供應商在2025年下半年削減了汽車產量,加劇了供不應求。

細分市場分析

到2025年,1類裝置將佔據積層陶瓷電容(MLCC)市場62.69%的佔有率,這反映了汽車製造商對車輛15年使用壽命內無漂移性能的需求。隨著寬能隙逆變器和醫療用電子設備轉向零溫度係數陶瓷,預計該細分市場的複合年成長率將達到15.83%,高於整體多層陶瓷電容器市場。村田製作所的1250V COG系列產品標誌著電極厚度的增加,旨在抑制電遷移,同時維持亞ppm級的溫度漂移。相較之下,2類鈦酸鋇裝置仍然主導智慧型手機市場,因為其高體積效率可以彌補劣化造成的電容損失,但在安全性至關重要的設計領域,它們的市場佔有率正在下降。

基板安裝面積與穩定性之間的權衡仍然是一項重大挑戰。雖然 1 類電容器的佔地面積是 2 類電容器的五倍,但其可預測的電容值消除了昂貴的設計裕量,使其在符合 ISO 26262 標準的動力傳動系統控制單元中至關重要。儘管監管機構並未明確規定介質的選擇,但 AEC-Q200 壽命測試實際上引導設計傾向於 1 類配方。因此,多層陶瓷電容器 (MLCC) 市場仍呈現兩極化:高價值的汽車和工業領域優先考慮 1 類電容器的穩定性,而家用電子電器。

到2025年,0,201尺寸的多層陶瓷電容器(MLCC)將佔據56.48%的市場。這主要得益於智慧型手機和穿戴式裝置對尺寸小於1mm的小型元件的需求。然而,0402尺寸的產品正以每年16.02%的速度成長,這主要得益於人工智慧伺服器對47µF去耦電容的需求,這些電容通常與700W的GPU相鄰。 2025年7月,村田製作所發表了一款800層0402尺寸的元件,其電容密度是上一代產品的兩倍。京瓷AVX隨後也發表了一款用於智慧型手錶模組的10µF 0402系列元件。

0402及更小尺寸元件的製造流程日益複雜,需要光刻級無塵室及雷射修邊等先進技術。因此,產能集中在日本和韓國的三家主要公司,預計到2026年初,交貨前置作業時間將延長至20週。同時,中國參與企業則在生產更通用的0603和0805尺寸產品。隨著GPU主機板擴大採用3000個MLCC電容,預計0402尺寸元件的供應將持續緊張,這可能會導致多層陶瓷電容市場整體價格居高不下。

區域分析

2025年,亞太地區佔據了多層陶瓷電容器(MLCC)全球57.69%的市場。這反映了日本的精密陶瓷技術、韓國的多產品製造能力以及中國龐大的消費性電子產品出口基礎。儘管中國工廠曾供應全球高達75%的MLCC產量,但地緣政治緊張局勢促使原始設備製造商(OEM)轉向透過其在日本、韓國和印度的基地進行雙重採購。村田製作所、TDK和太陽誘電均已擴大其在菲律賓和印度的產能,以滿足友邦的回流需求,並將於2026年初全面運作。同樣,三星電機也已運作運轉,將為比亞迪的800V汽車供應零件,並加強其在菲律賓的生產基地。

預計到2031年,北美市場將以16.07%的年均成長率成長,這主要得益於《晶片與科學法案》(CHIPS and Science Act)的獎勵,該法案旨在將半導體和被動元件的供應帶回美國。微軟和亞馬遜等超超大規模資料中心業者在2025年將其伺服器級MLCC訂單加倍,以尋求用於人工智慧加速器的超低ESL解耦元件。由於人事費用和漫長的AEC-Q200認證週期,美國計劃建造的晶圓廠仍處於延期狀態,因此墨西哥工廠正在根據美墨加協定(USMCA)的貿易條款承接剩餘的組裝。加拿大的市佔率雖然目前較小,但隨著其關鍵礦產政策提振國內鎳和鈀的供應,其市場潛力巨大。

預計到2025年,歐洲將維持約15%的市場佔有率,這主要得益於德國的汽車產業走廊和斯堪的納維亞半島的可再生能源項目。儘管歐盟的「晶片法」鼓勵本地生產,但嚴格的RoHS和REACH標準延長了認證流程,並使成本比亞洲高出15%。伍爾特電子正在擴大其汽車級晶片的生產,但仍從日本進口亞微米級介電粉末。其他地區,南美洲和中東及非洲的市場佔有率較低,僅為個位數,成長主要集中在巴西電動車的普及以及海灣國家優先考慮低電感MLCC的資料中心建設。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 800V電動車架構正在加速高壓MLCC的需求。

- 通用人工智慧伺服器建設的擴展正在推動超低ESL和高CV MLCC的採用。

- 裝置端人工智慧和先進的穿戴式裝置需要尺寸為 1005 或更小的超小型 MLCC(微晶聚合物)。

- 由於被動元件供應鏈的地理多元化而產生的「回流」現象

- 永續性法規傾向於使用無鉛和可回收陶瓷多層陶瓷電容器 (MLCC)。

- 透過半導體子系統的協同設計,MLCC 被整合到晶片組中。

- 市場限制因素

- 鎳和鈀價格的波動推高了物料清單成本。

- 汽車用多層陶瓷電容器(MLCC)的供給能力失衡問題依然存在。

- 中國在通用型MLCC市場發起的價格主導,正給全球利潤率帶來壓力。

- 介電層厚度(小於 1 µm)所造成的物理限制阻礙了靜態電容的提升。

- 宏觀經濟因素對市場的影響

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按介電類型

- 一年級

- 二年級

- 按箱尺寸

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 其他尺寸

- 按額定電壓

- 低電壓(低於500伏特)

- 中壓(500-1000伏特)

- 高壓(1000伏特或以上)

- 按實現類型

- 表面黏著技術

- 金屬帽

- 徑向引線

- 最終用途

- 航太/國防

- 車

- 家用電子電器

- 工業的

- 醫療設備

- 電力/公共產業

- 溝通

- 其他最終用途

- 按地區

- 北美洲

- 美國

- 北美其他地區

- 歐洲

- 德國

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 世界其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Murata Manufacturing Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Yageo Corporation

- TDK Corporation

- Kyocera AVX Components Corporation

- Walsin Technology Corporation

- Vishay Intertechnology, Inc.

- Wurth Elektronik GmbH and Co. KG

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Maruwa Co., Ltd.

- Samwha Capacitor Group

- Panasonic Holdings Corporation

- Shenzhen Torch Technology Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Shenzhen Eyang Technology Development Co., Ltd.

- Johanson Dielectrics, Inc.

- KEMET Corporation(Yageo Group)

- Shenzhen Sunlord Electronics Co., Ltd.

第7章 市場機會與未來展望

The multilayer ceramic capacitor (MLCC) market size is projected to expand from USD 27.26 billion in 2025 and USD 31.87 billion in 2026 to USD 64.19 billion by 2031, registering a 15.03% CAGR between 2026 and 2031. The growth trajectory reflects surging demand for passive components as vehicle electrification, artificial-intelligence infrastructure, and edge computing converge, placing sustained pressure on legacy supply chains. Class 1 temperature-stable dielectrics continue to gain traction in safety-critical designs, while 0402 packages are becoming the preferred form factor for high-performance servers that prize ultra-low equivalent series inductance over absolute footprint savings. Geo-diversified friend-shoring is unlocking incremental capacity in India and Southeast Asia, yet long qualification cycles for AEC-Q200 parts keep near-term supply tight. Competitive dynamics favor vertically integrated leaders that control barium-titanate powders and nickel electrode metallurgy, especially as volatility in nickel and palladium prices raises cost risk across the multilayer ceramic capacitor market.

Global Multilayer Ceramic Capacitor (MLCC) Market Trends and Insights

800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

Automakers shifting to 800 V battery platforms need MLCCs that withstand >=1,000 V operating margins, prompting suppliers to thicken nickel-palladium electrodes and refine sub-micrometer dielectric deposition. Samsung Electro-Mechanics released a 2,000 V X7R family in 2025 for silicon-carbide inverters, while Murata's GCM32 series pairs 1,000 V ratings with 100 nH equivalent series inductance for noise suppression. IDTechEx expects 800 V vehicles to represent 40% of production by 2028, lifting MLCC content per car by roughly one-quarter. Qualification bottlenecks persist because automotive-grade life testing still spans 1,000 hours at 150 °C, yet suppliers mastering these hurdles enjoy premium pricing in the multilayer ceramic capacitor (MLCC) market.

Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

Inference accelerators drawing 700 W per socket create voltage transients that demand 0402 MLCCs positioned within 2 mm of the die. Murata began shipping a 47 µF 4 V 0402 device in July 2025 that stacks 800 layers only 0.6 µm thick. KYOCERA AVX doubled capacity for its low-ESL server portfolio because each GPU board now carries up to 3,000 capacitors, far above CPU systems. TrendForce reported 35% MLCC unit growth in servers during 2025, well ahead of server shipment growth. Japanese precision houses therefore widen their lead as defect rates climb when active layers exceed 600.

Volatile Nickel and Palladium Prices Inflate BOM Costs

Nickel spiked 42% in early 2024 after Indonesian export curbs, then swung 18% lower by late 2025, while palladium fluctuated between USD 900 and USD 1,400 per troy ounce amid Russian supply uncertainty. A 10% rise in electrode-metal cost lifts finished MLCC bills by 3-5%, squeezing suppliers in consumer tiers where annual price erosion already approaches 8%. TDK said raw-material inflation trimmed its passive-component margin by 120 bps in fiscal 2026, accelerating copper electrode substitution. Murata is renegotiating quarterly price clauses tied to nickel futures, passing some risk to data-center clients. Smaller Asian suppliers without hedging programs cut automotive output in late 2025, deepening shortage conditions.

Other drivers and restraints analyzed in the detailed report include:

- On-Device AI and Advanced Wearables Require Sub-1005 Miniature MLCCs

- Geo-Diversified Friend-Shoring of Passive-Component Supply Chains

- Persistent Capacity Mismatch for Automotive-Grade MLCCs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 1 devices accounted for 62.69% multilayer ceramic capacitor (MLCC) market share in 2025, reflecting automakers' need for drift-free performance over 15-year vehicle lifespans. The segment is set to grow at a 15.83% CAGR, faster than the broader multilayer ceramic capacitor market size, as wide-bandgap inverters and medical electronics migrate to zero-temp-coefficient ceramics. Murata's 1,250 V C0G series exemplifies the shift toward thicker electrodes that combat electromigration while maintaining sub-ppm temperature tracking. In contrast, Class 2 barium-titanate parts still dominate smartphones because their higher volumetric efficiency offsets aging losses, yet they lose share in safety-critical designs.

The trade-off between board real estate and stability remains central. Class 1 capacitors occupy up to five times the footprint of Class 2 equivalents, yet predictable capacitance eliminates costly design margins, which matters in ISO 26262-compliant powertrain control units. Regulatory bodies do not explicitly mandate dielectric selection, but AEC-Q200 life testing implicitly steers designs toward Class 1 formulations. Consequently, the MLCC market continues to bifurcate: high-value automotive and industrial nodes lean on Class 1 stability, while consumer electronics retain Class 2 density.

The 0201 footprint captured 56.48% of the multilayer ceramic capacitor (MLCC) market in 2025, driven by smartphones and wearables chasing sub-millimetre components. Yet 0402 units are rising 16.02% annually, supported by AI servers that need 47 µF decoupling capacitors contiguous to 700 W GPUs. Murata's July 2025 release of an 800-layer 0402 part doubled capacitance density over its previous generation. KYOCERA AVX followed with a 10 µF 0402 range for smart-watch modules.

Manufacturing complexity scales sharply below 0402, requiring photolithography-grade clean rooms and laser trim. This concentrates capacity among three Japanese and Korean leaders, extending lead times to 20 weeks in early 2026, while Chinese entrants compete in commoditised 0603 and 0805 lines. As GPU boards swell to 3,000 MLCCs each, supply tightness in 0402 parts is likely to persist, underpinning premium price realisation across the multilayer ceramic capacitor market.

The Multilayer Ceramic Capacitor (MLCC) Market Report is Segmented by Dielectric Type (Class 1, and Class 2), Case Size (0 201, 0 402, 0 603, 1 005, 1 210, and More), Voltage Rating (Low-Range Voltage, Mid-Range Voltage, and More), Mounting Type (Surface-Mount, Metal-Cap, and Radial-Lead), End User (Automotive, Consumer Electronics, Industrial, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 57.69% of multilayer ceramic capacitor revenue in 2025, reflecting Japan's mastery of precision ceramics, South Korea's high-mix production, and China's vast consumer-electronics export engine. Chinese factories supplied up to 75% of global MLCC output, yet geopolitical tension spurred OEMs to dual-source through Japanese, Korean, and Indian sites. Murata, TDK, and Taiyo Yuden all ran full utilisation in early 2026 and expanded capacity in the Philippines and India to satisfy friend-shoring mandates. Samsung Electro-Mechanics, likewise running at capacity, channelled parts to BYD's 800 V vehicles while fortifying its Philippine campus.

North America is growing at 16.07% through 2031, buoyed by CHIPS and Science Act incentives that pull semiconductor and passive-component supply back onshore. Hyperscalers such as Microsoft and Amazon doubled server-grade MLCC orders during 2025, chasing ultra-low-ESL decoupling for AI accelerators. Proposed U.S. fabs remain delayed by labour cost and lengthy AEC-Q200 qualification cycles, so Mexican sites pick up overflow assembly under USMCA trade terms. Canada's piece is small but may rise as critical-mineral policies support domestic nickel and palladium supply.

Europe held a mid-teens share in 2025, tied to Germany's automotive corridor and Nordic renewable-energy projects. The European Union Chips Act encourages localisation, though strict RoHS and REACH standards extend qualification and inflate costs by up to 15% versus Asia. Wurth Elektronik is scaling automotive-grade output, yet still imports sub-micron dielectric powders from Japan. Elsewhere, South America, the Middle East, and Africa represent a low-single-digit slice, with growth centring on Brazil's electric-vehicle rollout and Gulf data-center builds that value low-inductance MLCCs.

List of Companies Covered in this Report:

- Murata Manufacturing Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Yageo Corporation

- TDK Corporation

- Kyocera AVX Components Corporation

- Walsin Technology Corporation

- Vishay Intertechnology, Inc.

- Wurth Elektronik GmbH and Co. KG

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Maruwa Co., Ltd.

- Samwha Capacitor Group

- Panasonic Holdings Corporation

- Shenzhen Torch Technology Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Shenzhen Eyang Technology Development Co., Ltd.

- Johanson Dielectrics, Inc.

- KEMET Corporation (Yageo Group)

- Shenzhen Sunlord Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

- 4.2.2 Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

- 4.2.3 On-Device AI and Advanced Wearables Require Sub-1 005 Miniature MLCCs

- 4.2.4 Geo-Diversified "Friend-Shoring" of Passive Component Supply Chains

- 4.2.5 Sustainability Mandates Favor Lead-Free and Recycled-Ceramic MLCCs

- 4.2.6 Semiconductor-Subsystem Co-Design Embeds MLCCs inside Chiplets

- 4.3 Market Restraints

- 4.3.1 Volatile Nickel and Palladium Prices Inflate BOM Costs

- 4.3.2 Persistent Capacity Mismatch for Automotive-Grade MLCCs

- 4.3.3 China Price-Led Offensive in Commodity MLCCs Erodes Global Margins

- 4.3.4 Physical Limits on Dielectric Layer Thickness (Less than 1 µm) Stall Capacitance Gains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage Rating

- 5.3.1 Low Voltage (Less than 500 V)

- 5.3.2 Mid Voltage (500 - 1000 V)

- 5.3.3 High Voltage (Above 1000 V)

- 5.4 By Mounting Type

- 5.4.1 Surface-Mount

- 5.4.2 Metal-Cap

- 5.4.3 Radial-Lead

- 5.5 By End-Use Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunications

- 5.5.8 Rest of End-Use Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 Samsung Electro-Mechanics Co., Ltd.

- 6.4.3 Taiyo Yuden Co., Ltd.

- 6.4.4 Yageo Corporation

- 6.4.5 TDK Corporation

- 6.4.6 Kyocera AVX Components Corporation

- 6.4.7 Walsin Technology Corporation

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Wurth Elektronik GmbH and Co. KG

- 6.4.10 Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- 6.4.11 Maruwa Co., Ltd.

- 6.4.12 Samwha Capacitor Group

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Shenzhen Torch Technology Co., Ltd.

- 6.4.15 Holy Stone Enterprise Co., Ltd.

- 6.4.16 Shenzhen Eyang Technology Development Co., Ltd.

- 6.4.17 Johanson Dielectrics, Inc.

- 6.4.18 KEMET Corporation (Yageo Group)

- 6.4.19 Shenzhen Sunlord Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

多層陶瓷電容器市場-2026-2032年全球市場預測

多層陶瓷電容器市場-2026-2032年全球市場預測 多層陶瓷電容器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、額定電壓範圍、介質類型、最終用途產業、地區和競爭格局分類,2021-2031年

多層陶瓷電容器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、額定電壓範圍、介質類型、最終用途產業、地區和競爭格局分類,2021-2031年 多層包裝市場預測至2034年-按材料、產品類型、層級構造、技術、應用、最終用戶和地區分類的全球分析積層陶瓷電容市場預測—按類型、介質類型、電壓範圍、最終用戶和地區分類的全球分析—2034年

多層包裝市場預測至2034年-按材料、產品類型、層級構造、技術、應用、最終用戶和地區分類的全球分析積層陶瓷電容市場預測—按類型、介質類型、電壓範圍、最終用戶和地區分類的全球分析—2034年 多層陶瓷電容器市場報告:按類型、電壓範圍、介質類型、最終用途和地區分類(2026-2034 年)

多層陶瓷電容器市場報告:按類型、電壓範圍、介質類型、最終用途和地區分類(2026-2034 年) 積層陶瓷電容市場分析與預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、功能、安裝方式、解決方案

積層陶瓷電容市場分析與預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、功能、安裝方式、解決方案 全球多層陶瓷電容器市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球多層陶瓷電容器市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 2026年全球多層陶瓷電容器市場報告

2026年全球多層陶瓷電容器市場報告 多層陶瓷電容器市場規模、佔有率及成長分析(按類型、額定電壓範圍、封裝尺寸及地區分類)-2026-2033年產業預測

多層陶瓷電容器市場規模、佔有率及成長分析(按類型、額定電壓範圍、封裝尺寸及地區分類)-2026-2033年產業預測 多層陶瓷片式電容器市場規模、佔有率及成長分析(按類型、介質類型、額定電壓、終端用戶產業及地區分類)-2026-2033年產業預測

多層陶瓷片式電容器市場規模、佔有率及成長分析(按類型、介質類型、額定電壓、終端用戶產業及地區分類)-2026-2033年產業預測