|

市場調查報告書

商品編碼

2044178

電腦視覺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Computer Vision - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

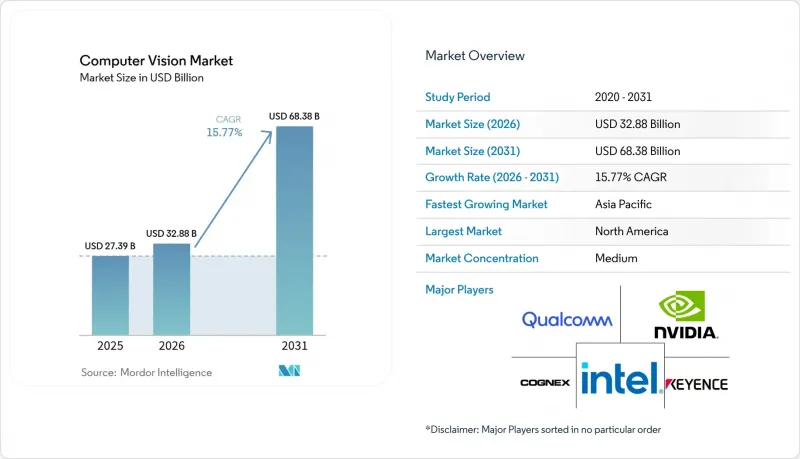

預計到 2031 年,電腦視覺市場規模將達到 683.8 億美元,2026 年至 2031 年的複合年成長率為 15.77%,預計從 2025 年的 273.9 億美元成長到 2026 年的 328.8 億美元。

低延遲邊緣推理晶片組的出現、所有新車必須配備高級駕駛輔助系統 (ADAS) 攝影機的法規,以及製藥和食品行業的品管標準,共同促成了以視覺技術為中心的多年資本投資預算的鞏固。北美根據《晶片與科學法案》(CHIPS and Science Act) 提供的補貼正在推動感測器供應,而亞太地區的獎勵則在推動工廠車間的快速部署。硬體仍然是主要的收入來源,但基於訂閱的深度學習軟體正在擴大利潤空間,而隨著歐盟和中國的資料主權法律限制傳輸到雲端,邊緣部署正在以最快的速度成長。隨著視覺加速器現在被整合到 AMD、高通和英特爾的處理器中,在許多應用場景中不再需要獨立顯示卡,競爭壓力正在加劇。

全球電腦視覺市場趨勢與洞察

邊緣AI晶片組可降低裝置視覺的延遲和功耗。

NVIDIA 的 Rubin 平台整合了 HBM4 記憶體和專用視覺處理單元,使 YOLOv8 能夠以 240 幀/秒的速度運行,功耗低於 15 瓦。這消除了傳統上阻礙雲端系統發展的網路開銷。高通驍龍 X2 Plus 內建 Hexagon 神經網路處理單元,可提供 75 TOPS 的運算能力,使行動電話製造商能夠在不快速耗盡電池電量的情況下進行臉部辨識。 AMD 的 Ryzen AI 400 系列加速了用於工業檢測的捲積模型,使電子組裝能夠用自適應分類器替換可程式邏輯控制器 (PLC) 中的視覺堆疊。 Ambarella 的 CV7 以 5 瓦的功耗提供 120 TOPS 的運算能力,為一級汽車供應商提供符合 ISO 26262 標準的車載攝影機運算資源。在整個產品系列中,往返延遲已從 80 毫秒減少到不到 10 毫秒——這是機器人抓取和緊急車輛煞車所需的閾值。

汽車ADAS攝影機的整合應用正在迅速增加。

特斯拉的「完全自動駕駛v13」採用八個環景顯示攝影機和一個客製化的推理晶片,可在美國47個州無需駕駛員確認即可完成車道變換。比亞迪的「Seal」轎車結合了SONY感測器和地平線機器人公司的晶片,以比同類歐美車型低30%的價格提供L2+等級的自動駕駛功能,加速了其在東南亞的普及。梅賽德斯-奔馳已將「Drive Pilot」系統擴展至加州高速公路,該系統融合了立體攝影機和雷射雷達技術,滿足L3級別的認證要求,使駕駛員在交通堵塞時能夠將視線從道路上移開。大眾汽車的電動車「ID.7」採用以紅外線為基礎的眼動追蹤技術,符合歐洲新車安全評估協會(Euro NCAP)2025年的駕駛監控法規。加之中國和歐洲的安全法規要求到2026年必須配備前向碰撞預警系統,預計到2026年,全球ADAS攝影機的出貨量將達到2.4億台,高於2025年的2億台。

複雜的系統整合要求

使用 GigE Vision、CoaXPress 和 Camera Link 將新攝影機連接到可程式邏輯控制器 (PLC) 時,需要中間件將專有串流格式轉換為 OPC UA 或 MQTT 格式。這可能會消耗高達 40% 的專案預算,並將試運行週期延長三個月。使用多家供應商混合產品的公司會面臨韌體衝突,導致成本增加和大量生產延誤。一家歐洲汽車零件供應商不得不額外支付 25 萬美元,用於將 Basler 攝影機與 Cognex 處理器同步,迫使其將生產推遲了六週。年度軟體維護費用平均佔許可價格的 18%,且每次生產線重新配置時都需要進行調整工作。沒有內部自動化專家的小規模工廠必須聘請每小時 150 至 300 美元的整合商,除非是年產量超過 50 萬台的大批量生產線,否則該專案往往無利可圖。由於缺乏與 MLPerf 等效的標準化基準,買家不得不進行冗長的概念驗證(PoC) 測試,這減緩了電腦視覺市場的普及速度。

細分市場分析

預計到2025年,硬體銷售額將佔總銷售額的65.21%,主要得益於製造商採購高解析度相機、專用處理器和可控照明光學元件。在該領域,Basler的工業相機出貨量超過40萬台,Teledyne FLIR擴展了其A700熱成像產品線,Allied Vision推出了一款適用於高速輸送機的2050萬像素全局百葉窗單元。儘管電腦視覺市場的硬體規模預計將穩定成長,但隨著企業從永久授權轉向包含更新和雲端連接的訂閱模式,軟體層面的成長速度預計將更快。

OpenCV 4.9、TensorFlow Lite 2.15 以及來自 AWS Panorama 和 Azure IoT Edge 的商業中間件正在簡化部署,並將推動軟體市場到 2031 年的複合年成長率達到 15.87%。企業重視這些平台,因為它們透過量化和剪枝縮短了產品上線時間,並降低了設備的運算負載。因此,電腦視覺市場對提供承包推理堆疊而非單一攝影機或電路板的供應商的需求日益成長。

到2025年,製造業將佔據電腦視覺市場佔有率的28.49%,這主要得益於電子產品生產線和食品包裝生產線的大規模檢測需求。康耐視(Cognex)、Keyence)和OMRON)憑藉其針對工業環境最佳化的光學元件、照明設備和軟體組合,在該領域佔據主導地位。生命科學領域將佔12%,這主要得益於製藥公司為符合修訂後的附件1法規而加強管瓶檢測;國防和安全領域將達到8%,這主要得益於泰萊達因(Teledyne)FLIR產品的銷售成長。

同時,汽車產業以18.23%的複合年成長率呈現最高增速,這主要得益於每輛車攝影機數量的持續成長。到2025年,特斯拉、賓士和比亞迪將累計新增超過2億個ADAS攝影機,並且由於歐洲新車安全評鑑協會(Euro NCAP)強制要求對駕駛員進行監控,車載攝影機正被引入到量產車型中。在預測期內,隨著企業維修支援電動車生產的工廠,以及整車製造商(OEM)致力於實現L3級自動駕駛,預計更多投資將流向汽車行業,這將加劇對系統整合人才的競爭。

本電腦視覺市場報告按組件(硬體和軟體)、終端用戶產業(生命科學、製造業、汽車、零售、物流、農業等)、應用程式(偵測、測量、分類、監控、3D建模)、部署模式(邊緣、本地部署、雲端)和地區進行細分。市場預測以美元計價。

區域分析

預計到2025年,北美將佔全球銷售額的49.01%,這得益於《晶片創新與應用法案》(CHIPS Act)提供的520億美元獎勵,該法案擴大了美國國內視覺處理器晶圓廠的產能。一份價值4.2億美元的美國國防部熱成像技術合約增強了泰萊科技(Teledyne FLIR)的產品線,而加拿大的人工智慧中心,例如Vector Institute,則與汽車零件供應商合作開發ADAS演算法。 2020年至2025年的歷史複合年成長率為13.2%,預計2026年至2031年將上升至14.8%。這主要歸功於美國食品藥物管理局(FDA)對醫療影像人工智慧指南的澄清,這將使先前因疫情而推遲的醫院投資得以釋放。

亞太地區是成長最快的地區,預計複合年成長率將達到16.39%。到2025年,光是中國就將佔全球銷售額的22%,但美國對高階GPU的出口限制正推動市場轉向華為昇騰處理器。印度的生產連結獎勵計畫計畫已向電子工廠提供20億美元,用於部署表面黏著技術檢測視覺系統。日本已資助340個智慧工廠示範項目,韓國已投資18億美元用於行動神經形態感測器的商業化。澳洲和紐西蘭正在採用視覺引導運輸卡車,使礦石開採率提高了30%。

預計到2025年,歐洲將佔據18%的市場。德國已投入5億歐元用於升級到工業4.0,但歐盟人工智慧法規的合規性評估費用約為每個系統30萬歐元,這阻礙了中小型工廠的發展。英國計劃在2025年將1,200萬個ADAS攝影機整合到生產線中,法國已將視覺檢測技術應用於渦輪葉片。中東地區(如沙烏地阿拉伯和阿拉伯聯合大公國)的智慧城市計畫正在部署數百萬個攝影機組成的網路,南美洲的農業正在轉向無人機成像技術,該技術有望減少40%的農藥使用量。這些部署共同表明,電腦視覺市場的全球基礎正在不斷擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 視覺引導機器人技術在製造業的應用日益廣泛

- 受監管行業嚴格的品管要求

- 汽車上ADAS攝影機的應用正在迅速增加。

- 邊緣AI晶片組可降低裝置內視覺的延遲和功耗。

- 高光譜遙測和神經形態感測器開啟了新的應用場景

- 物聯網零售業中智慧攝影機的快速普及

- 市場限制因素

- 複雜的系統整合要求

- 熟練的電腦視覺工程師短缺

- 數據標註成本不斷上升

- 對先進視覺處理器的出口限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 相機

- 處理器(GPU/ASIC/FPGA)

- 光學/照明

- 軟體

- 傳統演算法

- 深度學習框架

- 邊緣中介軟體

- 按最終用戶行業分類

- 生命科學

- 製造業

- 電子設備組裝

- 食品/飲料

- 包裹

- 國防/安全

- 車

- 零售與電子商務

- 物流/倉儲

- 農業和林業

- 其他終端用戶產業

- 透過使用

- 檢驗和品質保證

- 測量和稱重

- 分類和排序

- 監測和監視

- 3D建模與重建

- 不同的發展

- 邊緣

- 現場

- 雲

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Intel Corporation

- Cognex Corporation

- Keyence Corporation

- Qualcomm Inc.

- NVIDIA Corporation

- Omron Corporation

- Basler AG

- Teledyne FLIR LLC

- Sony Group Corp.

- Google LLC

- Advanced Micro Devices(AMD)

- Adlink Technology Inc.

- Hikvision Robotics

- Stemmer Imaging AG

- Dahua Technology

- Zebra Technologies Corp.

- Amazon Web Services Inc.

- Clarifai Inc.

- Allied Vision Technologies GmbH

- OpenCV.ai

- Matrox Imaging

第7章 市場機會與未來展望

The computer vision market size is projected to be USD 27.39 billion in 2025, USD 32.88 billion in 2026, and reach USD 68.38 billion by 2031, growing at a CAGR of 15.77% from 2026 to 2031.

Edge-inference chipsets that collapse latency, regulatory mandates pushing Advanced Driver-Assistance Systems (ADAS) cameras into every new vehicle, and quality-control rules in pharmaceuticals and food have combined to anchor multi-year capital budgets around vision technologies. North American subsidies under the CHIPS and Science Act are strengthening sensor supply, while Asia-Pacific incentives are driving rapid adoption on the factory floor. Hardware still dominates revenue, yet subscription-based deep-learning software is capturing margin, and edge deployment is rising fastest as data-sovereignty laws in the EU and China limit cloud transfers. Competitive pressure intensifies as processors from AMD, Qualcomm, and Intel now embed vision accelerators, eliminating the need for discrete cards in many use cases.

Global Computer Vision Market Trends and Insights

Edge-AI Chipsets Lowering Latency and Power for On-Device Vision

NVIDIA's Rubin platform integrates HBM4 memory with a dedicated vision-processing unit, executing YOLOv8 at 240 frames per second while drawing under 15 watts, and therefore removes the network overhead that previously hindered cloud-dependent systems. Qualcomm's Snapdragon X2 Plus embeds a Hexagon neural-processing unit that delivers 75 TOPS, allowing handset makers to run facial recognition without rapidly draining batteries. AMD's Ryzen AI 400 Series accelerates convolutional models for industrial inspection, letting electronics assemblers replace programmable-logic-controller vision stacks with adaptive classifiers. Ambarella's CV7 delivers 120 TOPS at 5 watts, giving Tier-1 automotive suppliers ISO 26262-ready compute budgets for cabin cameras. Across these families, round-trip latency has fallen from 80 milliseconds to below 10 milliseconds, the threshold needed for robotic grasping and emergency vehicle braking.

Surge in Automotive ADAS Camera Integration

Tesla's Full Self-Driving v13 uses eight surround-view cameras and a custom inference chip to execute lane changes without driver confirmation in 47 U.S. states. BYD's Seal sedan pairs Sony sensors with Horizon Robotics silicon to deliver Level 2+ capability at price points 30% below comparable Western models, accelerating uptake in Southeast Asia. Mercedes-Benz expanded Drive Pilot to California highways, employing stereo cameras and LiDAR fusion to satisfy Level 3 certification that lets drivers avert their gaze in slow traffic. Volkswagen's ID.7 electric vehicle uses infrared-based gaze tracking to comply with Euro NCAP's 2025 driver-monitoring rule. Combined with Chinese and European safety mandates that make forward-collision warning compulsory by 2026, global ADAS camera shipments are expected to reach 240 million in 2026, up from 200 million in 2025.

Complex System-Integration Requirements

Connecting new cameras using GigE Vision, CoaXPress, and Camera Link to programmable-logic controllers demands middleware that translates proprietary streams into OPC UA or MQTT, consuming up to 40% of project budgets and extending commissioning by three months. Enterprises juggling multi-vendor estates face firmware conflicts that inflate costs and delay ramps; a European auto supplier spent an extra USD 250,000 synchronizing Basler cameras with Cognex processors, postponing production by six weeks. Annual software-maintenance fees average 18% of license price, and recalibration labor resurfaces each time lines are re-tooled. Smaller plants lacking in-house automation talent must hire integrators who charge USD 150-300 per hour, making projects economical only for high-volume lines that exceed 500,000 units yearly. The absence of standardized benchmarks equivalent to MLPerf obliges buyers to run long proof-of-concept trials, slowing computer vision market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Vision-Guided Robotics in Manufacturing

- Stringent Quality-Control Mandates Across Regulated Industries

- Shortage of Skilled Computer-Vision Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware delivered 65.21% of 2025 revenue as manufacturers bought high-resolution cameras, specialized processors, and controlled-illumination optics. Within this slice, Basler shipped more than 400,000 industrial cameras, Teledyne FLIR broadened its A700 thermal line, and Allied Vision released a 20.5-megapixel global-shutter unit ideal for fast conveyors. The computer vision market size for hardware is forecast to grow steadily, but the software layer is set to expand faster as enterprises transition from perpetual licenses to subscription models that bundle updates and cloud connectivity.

OpenCV 4.9, TensorFlow Lite 2.15, and commercial middleware from AWS Panorama and Azure IoT Edge simplify deployment, spurring a 15.87% CAGR for software through 2031. Enterprises value these platforms because they shorten time-to-production and lower device-side compute needs via quantization and pruning. As a result, the computer vision market increasingly rewards vendors that package turnkey inferencing stacks rather than stand-alone cameras or boards.

Manufacturing contributed 28.49% of the computer vision market share in 2025 thanks to large-scale inspection on electronics lines and food-packaging belts. Cognex, Keyence, and Omron dominate here by offering bundled optics, lighting, and software tuned for industrial conditions. Life sciences held 12% after drug makers upgraded vial inspection to meet revised Annex 1 rules, while defense and security reached 8% on the back of Teledyne FLIR sales.

Automotive, however, is charting the highest growth at an 18.23% CAGR because camera counts per vehicle continue to climb. Tesla, Mercedes-Benz, and BYD collectively added more than 200 million ADAS cameras in 2025, and Euro NCAP mandates for driver monitoring are pushing in-cabin units into mass-market models. Over the forecast horizon, plant retrofits supporting electric-vehicle production and OEM commitments to Level 3 autonomy will tilt incremental spending toward automotive, tightening competition for integration talent.

The Computer Vision Market Report is Segmented by Components (Hardware and Software), End-User Industry (Life Sciences, Manufacturing, Automotive, Retail, Logistics, Agriculture, and More), Application (Inspection, Measurement, Classification, Surveillance, and 3D Modeling), Deployment (Edge, On-Premise, and Cloud), and Geography. The Market Forecasts are in Value (USD).

Geography Analysis

North America held 49.01% of 2025 revenue, buoyed by USD 52 billion in CHIPS Act incentives that expanded domestic fab capacity for vision processors. U.S. defense contracts worth USD 420 million for thermal imaging strengthened Teledyne FLIR's pipeline, while Canadian AI hubs such as the Vector Institute partnered with auto suppliers on ADAS algorithms. Historical 2020-2025 CAGR of 13.2% is stepping up to 14.8% during 2026-2031 because FDA clarity on medical-image AI unlocks deferred hospital investment.

Asia-Pacific is the fastest-growing region, projected at a 16.39% CAGR. China alone generated 22% of global 2025 revenue, but U.S. export controls on high-end GPUs are motivating a shift toward Huawei Ascend processors. India's Production-Linked Incentive scheme funnels USD 2 billion into electronics plants that consume vision systems for surface-mount inspection. Japan funds 340 smart-factory pilots, and South Korea invests USD 1.8 billion to commercialize mobile neuromorphic sensors. Australia and New Zealand rely on vision-guided haul trucks that raise ore-extraction rates by 30%.

Europe captured 18% share in 2025. Germany disbursed EUR 500 million for Industrie 4.0 upgrades, yet EU AI Act conformity assessments costing about EUR 300,000 per system slow smaller plants. The United Kingdom integrated 12 million ADAS cameras in 2025 production, while France applied vision inspection to turbine blades. Middle Eastern smart-city projects in Saudi Arabia and the UAE are installing multi-million-camera networks, and South American agriculture is turning to drone imaging that cuts pesticide use by 40%. Collectively, these deployments showcase a widening global foundation for the computer vision market.

- Intel Corporation

- Cognex Corporation

- Keyence Corporation

- Qualcomm Inc.

- NVIDIA Corporation

- Omron Corporation

- Basler AG

- Teledyne FLIR LLC

- Sony Group Corp.

- Google LLC

- Advanced Micro Devices (AMD)

- Adlink Technology Inc.

- Hikvision Robotics

- Stemmer Imaging AG

- Dahua Technology

- Zebra Technologies Corp.

- Amazon Web Services Inc.

- Clarifai Inc.

- Allied Vision Technologies GmbH

- OpenCV.ai

- Matrox Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Vision-Guided Robotics in Manufacturing

- 4.2.2 Stringent Quality-Control Mandates Across Regulated Industries

- 4.2.3 Surge in Automotive ADAS Camera Integration

- 4.2.4 Edge-AI Chipsets Lowering Latency and Power for On-Device Vision

- 4.2.5 Hyperspectral and Neuromorphic Sensors Opening New Use-Cases

- 4.2.6 Rapid Proliferation of Smart Cameras in IoT-Enabled Retail

- 4.3 Market Restraints

- 4.3.1 Complex System-Integration Requirements

- 4.3.2 Shortage of Skilled Computer-Vision Engineers

- 4.3.3 Escalating Data-Labeling Cost Inflation

- 4.3.4 Export-Control Curbs on Advanced Vision Processors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Components

- 5.1.1 Hardware

- 5.1.2 Cameras

- 5.1.3 Processors (GPUs / ASIC / FPGA)

- 5.1.4 Optics and Lighting

- 5.1.5 Software

- 5.1.6 Traditional Algorithms

- 5.1.7 Deep-Learning Frameworks

- 5.1.8 Edge Middleware

- 5.2 By End-User Industry

- 5.2.1 Life Sciences

- 5.2.2 Manufacturing

- 5.2.3 Electronics Assembly

- 5.2.4 Food and Beverage

- 5.2.5 Packaging

- 5.2.6 Defense and Security

- 5.2.7 Automotive

- 5.2.8 Retail and E-Commerce

- 5.2.9 Logistics and Warehousing

- 5.2.10 Agriculture and Forestry

- 5.2.11 Other End-User Industries

- 5.3 By Application

- 5.3.1 Inspection and Quality Assurance

- 5.3.2 Measurement and Metrology

- 5.3.3 Classification and Sorting

- 5.3.4 Surveillance and Monitoring

- 5.3.5 3D Modeling and Reconstruction

- 5.4 By Deployment

- 5.4.1 Edge

- 5.4.2 On-Premise

- 5.4.3 Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Cognex Corporation

- 6.4.3 Keyence Corporation

- 6.4.4 Qualcomm Inc.

- 6.4.5 NVIDIA Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Basler AG

- 6.4.8 Teledyne FLIR LLC

- 6.4.9 Sony Group Corp.

- 6.4.10 Google LLC

- 6.4.11 Advanced Micro Devices (AMD)

- 6.4.12 Adlink Technology Inc.

- 6.4.13 Hikvision Robotics

- 6.4.14 Stemmer Imaging AG

- 6.4.15 Dahua Technology

- 6.4.16 Zebra Technologies Corp.

- 6.4.17 Amazon Web Services Inc.

- 6.4.18 Clarifai Inc.

- 6.4.19 Allied Vision Technologies GmbH

- 6.4.20 OpenCV.ai

- 6.4.21 Matrox Imaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

監控市場中的電腦視覺:按組件、技術、部署、應用和最終用戶分類-2026-2032年全球市場預測自動化領域的電腦視覺:按組件、技術、應用和最終用戶產業分類的市場預測,2026-2032 年製造業電腦視覺市場:2026-2032年全球市場預測(依產品、規模、資料類型、應用、產業、企業規模及部署類型分類)電腦視覺在導航領域的應用:2026-2032年全球市場預測(按組件、技術、車輛類型、應用、部署模式和最終用戶產業分類)電腦視覺市場:按組件、技術、應用和部署模式分類-2026-2032年全球市場預測

監控市場中的電腦視覺:按組件、技術、部署、應用和最終用戶分類-2026-2032年全球市場預測自動化領域的電腦視覺:按組件、技術、應用和最終用戶產業分類的市場預測,2026-2032 年製造業電腦視覺市場:2026-2032年全球市場預測(依產品、規模、資料類型、應用、產業、企業規模及部署類型分類)電腦視覺在導航領域的應用:2026-2032年全球市場預測(按組件、技術、車輛類型、應用、部署模式和最終用戶產業分類)電腦視覺市場:按組件、技術、應用和部署模式分類-2026-2032年全球市場預測 2026年全球電腦視覺市場報告

2026年全球電腦視覺市場報告 電腦視覺市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、功能、部署類型和解決方案分類

電腦視覺市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、功能、部署類型和解決方案分類 電腦視覺市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

電腦視覺市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 2026-2030年全球醫療保健電腦視覺市場

2026-2030年全球醫療保健電腦視覺市場 電腦視覺市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、產品類型、應用、垂直產業、地區和競爭格局分類,2021-2031年預測

電腦視覺市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、產品類型、應用、垂直產業、地區和競爭格局分類,2021-2031年預測