|

市場調查報告書

商品編碼

2044171

印刷基板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Printed Circuit Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

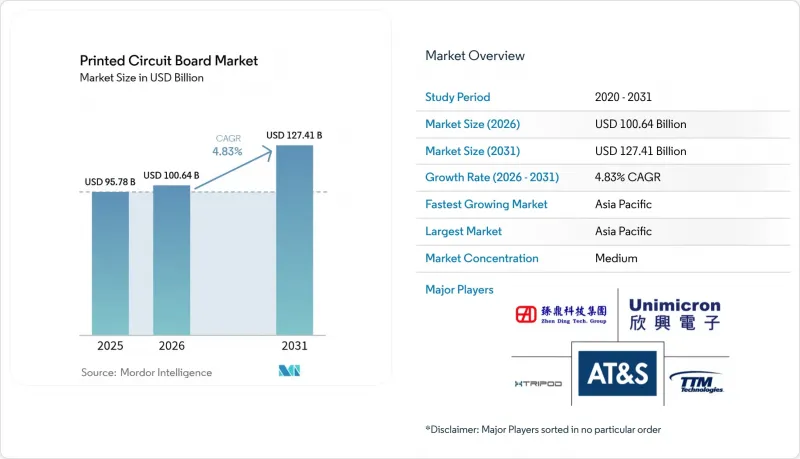

預計到 2025 年,印刷基板市場規模將達到 957.8 億美元,到 2026 年將達到 1,006.4 億美元,到 2031 年將達到 1,274.1 億美元,預測期內複合年成長率為 4.83%。

市場需求正從傳統消費性電子設備轉向人工智慧 (AI) 伺服器、電動車 (EV) 電力電子設備和下一代通訊網路等高價值應用,這些應用都需要更多層、更嚴格的公差和更高品質的介電材料基板。超大規模資料中心營運商正在升級到每通道 112 Gbps 的訊號傳輸速度,他們現在訂購的是 40 層或更多層的背板,其售價約為 8 層智慧型手機基板的四倍。美國《晶片與科學法案》的獎勵以及歐洲的自主人工智慧法規等區域性政策正在刺激北美和中歐的新型製造業發展,而亞太地區傳統的規模經濟效益則相對下降。材料替代也是一個利好因素,隨著超大規模資料中心業者向 800 Gbps 和 1.6 Tbps光纖通訊轉型,超低損耗基板的市場佔有率也在不斷擴大。同時,原料價格波動和更嚴格的廢水法規給通用製造商的利潤率帶來了壓力,導致行業結構重組,有利於印刷基板市場高階細分市場的供應商。

全球印刷基板市場趨勢與洞察

人工智慧伺服器和高效能運算需求激增

到2025年,超大規模營運商將部署約120萬台針對人工智慧最佳化的伺服器。每台伺服器將配備8至16個GPU加速器,每個插槽的功耗超過1.0千瓦。這些平台需要40至60層的背板,其微孔尺寸小於75微米,並採用雷射穿孔的多層通孔和嵌入式散熱通孔,用於散發液冷冷板產生的熱量。此類基板的單價超過200美元,而傳統伺服器電路板的單價僅為50美元,這提高了能夠滿足公差範圍要求的台灣專業製造商的毛利率。 AMD的Instinct MI350專案採用晶片組拓撲結構,需要嵌入式走線電路基板,這將推動2026年後對電路板的需求成長。因此,印刷基板市場將直接受益於層數增加和先進基板配置多樣化所帶來的需求成長。

電動汽車用電力電子元件的快速擴張

預計2025年交付的電池式電動車,其逆變器、充電器和電池管理單元等PCB板的總成本將達到150至200美元,是內燃機車型PCB板成本的兩倍。碳化矽(SiC)功率模組的開關電壓為800V,結溫超過175 度C,迫使設計人員使用玻璃化轉變溫度高於260 度C的聚醯亞胺或陶瓷基板,以及厚度達210μm的銅箔來承受400A的電流。 IATF 16949汽車級認證正在縮小供應商的選擇範圍,增強現有供應商的定價權,並從以金額為準擴大PCB市場。

銅和環氧樹脂價格長期波動

2024年至2025年間,智利和秘魯礦業營運中斷,加上電動車需求的投機性預期,導致銅期貨價格在每噸8,200美元至10,500美元之間波動。由於銅箔佔成品基板成本的40%之多,現貨價格的飆升給沒有避險策略的亞洲中小型製造商的利潤率帶來了壓力。 2025年,台灣一家前驅工廠發生火災,導致雙酚A產量下降,進而推高了環氧樹脂價格。這導致層壓板供應商啟動不可抗力條款,並延遲了對北美的出貨。此類價格波動使資本投資模型的發展變得更加複雜,並減緩了PCB市場的短期成長。

細分市場分析

2025年,標準多層基板在印刷基板市場中仍將佔據29.64%的佔有率,這主要得益於汽車車身電子和工業驅動系統的需求成長。同時,軟性電路板預計到2031年將以5.39%的複合年成長率成長,因為折疊式智慧型手機、穿戴式健康監測器和超薄汽車內裝模組需要小於3毫米的彎曲半徑。光是三星Galaxy Z系列預計在2025年就將出貨1000萬部,每部設備都配備了三塊或更多由日本邁創(Nippon Mectron)和Flexium公司提供的聚醯亞胺軟性電路板。能夠支援75微米線寬的多相機陣列的高密度佈線設計已成為高階智慧型手機的事實標準。需要0.4毫米球柵陣列和10微米走線的基板的價格是8層伺服器板的4到5倍,但它們仍然是一個規模雖小但盈利的細分市場。

軟硬複合結構在航太和植入式醫療設備領域市場佔有率不斷擴大,其抗振性和節省空間的特性使其30-50%的成本溢價物有所值。金屬基板和陶瓷基板則應用於LED頭燈和汽車雷達,受益於固態照明和高級駕駛輔助系統(ADAS)的普及。同時,由於深圳和蘇州的工廠面臨激烈的價格競爭,通用四層產品的生產線利潤率受到擠壓。擁有IPC-6012 3級或MIL-PRF-55110認證的專業基板製造商保持著價格優勢,因為國防和醫療客戶不太可能轉向低等級供應商。總體而言,儘管通用產品的產量保持平穩,但由於構成比向軟式電路板、軟硬複合和積體電路基板轉變,印刷基板基板正在擴張。

區域分析

預計到2025年,亞太地區將佔全球產量的82.54%,年均成長率達4.86%。這主要得益於廣東、江蘇和珠江三角洲一體化的產業生態Delta,該地區元件採購、組裝化學品和組裝生產線集中於同一區域。台灣在先進基板領域扮演核心角色,Unimicron、南亞PCB和Kinsus等公司經營半導體級無塵室,並為英特爾和台積電(TSMC)供貨。中國的深南電路和DSBJ在智慧型手機HDI生產領域處於領先地位,但由於美國的出口限制,它們面臨產能瓶頸。日本的IBIDEN、Shinko Electric和Meiko Electronics利用其在通孔填充和表面處理方面的製程專利,專注於生產高可靠性的汽車和工業基板,這些產品定位為高價位產品。韓國的三星馬達和LG Innotek先前主要專注於行動電話,現在正加大汽車雷達和資料中心電路基板的投資。

預計到2025年,北美將佔印刷基板市場規模的約8%,但在美國《晶片與科學法案》的稅額扣抵和國防沖銷條款的推動下,其市場規模正在擴大。 TTM Technologies公司正在紐約州投資1.5億美元,建造軟硬複合生產線。大型國防公司要求關鍵任務設計必須採用國內採購,這提高了亞利桑那州和加州小規模專業製造商的運轉率。墨西哥正利用其「加工出口區」(maquiladora)的地位,使用進口基板組裝伺服器和通訊設備,這種模式在更廣泛的區域供應鏈中維持了一定的生產水準。加拿大的業務規模仍然局限於工業和航太原型產品的多品種、小批量生產。

到2025年,歐洲的晶片產量將僅佔全球總產量的約6%,但它受益於總額達430億歐元(約507億美元)的「歐洲晶片法案」。該法案為先進基板津貼,並鼓勵汽車安全系統採用雙重採購模式。 AT&S在奧地利和馬來西亞的多元化生產策略與這家德國汽車製造商強調風險分散的策略相契合。瑞士電子公司(Schweizer Electronic)正在考慮在亞利桑那州成立一家合資企業,這體現了其為贏得國防和醫療領域的客戶而開展的跨大西洋合作。波蘭和捷克等東歐國家由於人事費用低廉且符合歐盟法規,對中等規模的多層基板生產具有吸引力。包括拉丁美洲、中東和非洲在內的世界其他地區仍處於小規模生產階段,主要從亞洲進口基板進行最終組裝。歐洲的RoHS指令和美國的TSCA法案等環境法規正在推動全球統一的材料標準,間接提高了新興市場的品質標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對人工智慧伺服器和高效能運算的需求正在激增。

- 電動車中電力電子設備安裝量的加速成長

- 向 5G 和新興的 6G 過渡正在推動 HDI 的採用。

- 向先進積體電路基板過渡,實現晶片整合

- 美國和歐盟鼓勵關鍵印刷電路板供應鏈回流的獎勵。

- 採用超低損耗材料實現 112-224 Gbps 訊號傳輸。

- 市場限制因素

- 銅和環氧樹脂價格長期波動

- 先進PCB設計和程式工程。

- 與污水和 PFAS 移除相關的 ESG 合規成本不斷增加。

- 地緣政治出口限制了先進基板製造設備的製造。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按PCB類型

- 標準基板(非HDI)

- 硬質單面/雙面

- 高密度互連(HDI)

- 軟性印刷電路(FPC)

- IC基板(構裝基板)

- 軟硬複合

- 其他PCB類型

- 按基板

- 玻璃環氧樹脂(FR-4)

- 高速/低損耗

- 聚醯亞胺(PI)

- 包裝樹脂(BT 和 ABF)

- 其他基板

- 按最終用戶行業分類

- 家用電子電器

- 計算和資料中心

- 通訊和5G

- 汽車和電動車

- 工業與電力

- 醫療保健

- 航太/國防

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 台灣

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 世界其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Zhen Ding Technology Holding Ltd.

- Unimicron Technology Corp.

- Nippon Mektron Ltd.

- TTM Technologies Inc.

- Samsung Electro-Mechanics Co., Ltd.

- Compeq Manufacturing Co., Ltd.

- Tripod Technology Corporation

- Shennan Circuits Co., Ltd.

- Young Poong Electronics Co., Ltd.

- Ibiden Co., Ltd.

- HannStar Board Corp.

- AT&S AG

- LG Innotek Co., Ltd.

- Kinwong Electronic Co., Ltd.

- DSBJ(Dongshan Precision)

- Kingboard Holdings Ltd.

- Shinko Electric Industries Co., Ltd.

- Flexium Interconnect Inc.

- Nan Ya PCB Corp.

- Isola Group

第7章 市場機會與未來展望

The printed circuit board market size is projected to be USD 95.78 billion in 2025, USD 100.64 billion in 2026, and reach USD 127.41 billion by 2031, translating to a 4.83% CAGR over the forecast period. Demand is shifting from legacy consumer devices toward higher-value deployments in artificial-intelligence servers, electric-vehicle power electronics, and next-generation telecom networks, each of which specifies boards with more layers, tighter tolerances, and premium dielectric materials. Hyperscale data-center operators upgrading to 112 Gbps per-lane signaling now order 40-plus-layer backplanes that carry selling prices nearly four times those of eight-layer smartphone boards. Regional policy, led by United States CHIPS and Science Act incentives and European sovereign-AI mandates, is encouraging new fabrication in North America and Central Europe while tempering Asia-Pacific's historic scale advantage. Material substitution is another tail-wind, with ultra-low-loss substrates gaining share as hyperscalers shift to 800 Gbps and 1.6 Tbps optics. At the same time, raw-material volatility and tightening wastewater rules are thinning margins for commodity makers, prompting consolidation that should favor suppliers positioned in premium niches of the printed circuit board market.

Global Printed Circuit Board Market Trends and Insights

Surge in AI Server and High-Performance Computing Demand

Hyperscale operators deployed roughly 1.2 million AI-optimized servers in 2025, each integrating 8-16 GPU accelerators that draw more than 1.0 kW per socket. These platforms specify 40-to-60-layer backplanes with microvias under 75 μm, laser-drilled stacked vias, and embedded thermal vias that dissipate heat from liquid-cooled cold plates. Unit pricing for such substrates exceeds USD 200 compared with USD 50 for legacy server boards, expanding gross margins for Taiwanese specialists able to meet the tolerance window. AMD's Instinct MI350 program employs chiplet topologies that require embedded-trace substrates, driving incremental demand through 2026 and beyond. The printed circuit board market therefore captures a direct uplift from both higher layer counts and richer mixes of advanced substrates.

Accelerated EV Power Electronics Content

Battery-electric vehicles delivered in 2025 contained USD 150-200 worth of PCB content across inverters, chargers, and battery-management units, double that of internal-combustion models. Silicon-carbide power modules switching at 800 V create junction temperatures above 175 °C, forcing designers to adopt polyimide or ceramic boards with glass-transition values above 260 °C and thick copper foils up to 210 μm to carry 400 A. Automotive-grade validation under IATF 16949 narrows the supplier pool, increasing pricing power for incumbents and enlarging the PCB market in value terms.

Prolonged Copper and Epoxy-Resin Price Volatility

Copper futures oscillated between USD 8,200 and USD 10,500 per metric ton during 2024-2025 as mine disruptions in Chile and Peru collided with speculative EV demand. Because copper foil can represent up to 40% of finished-board cost, spot spikes erode margins for smaller Asian fabricators lacking hedging programs. Epoxy-resin prices jumped after a 2025 Taiwanese precursor plant fire cut bisphenol-A output, leading laminate suppliers to invoke force-majeure clauses that delayed shipments to North America. Such volatility complicates capital-investment models and dampens short-term growth in the PCB market.

Other drivers and restraints analyzed in the detailed report include:

- 5G and Emerging 6G Transition Boosting HDI Adoption

- Shift Toward Advanced IC Substrates for Chiplet Integration

- Escalating ESG Compliance Costs for Wastewater and PFAS Elimination

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard multilayer boards retained 29.64% printed circuit board market share in 2025, anchored by automotive body electronics and industrial drives. Flexible circuits, however, are set to expand at a 5.39% CAGR through 2031 as foldable smartphones, wearable health monitors, and thin automotive interior modules demand bend radii below 3 mm. Samsung's Galaxy Z series alone shipped 10 million units in 2025, each carrying three or more polyimide flexes supplied by Nippon Mektron and Flexium. High-density interconnect designs have become the de facto choice for premium handsets because 75 µm line widths accommodate multi-camera arrays. IC substrates remain a small but lucrative niche, priced four to five times higher than eight-layer server boards because they require 0.4 mm ball-grid arrays and 10 µm traces.

Rigid-flex constructions are carving share in aerospace and implantable medical devices where vibration resistance and space savings justify a 30-50% cost premium. Metal-core and ceramic boards serve LED headlamps and automotive radar, benefiting from the move to solid-state lighting and advanced driver-assistance systems. Commodity four-layer product runs face margin compression as Shenzhen and Suzhou factories compete aggressively on price. Conversely, specialty fabricators that hold IPC-6012 Class 3 or MIL-PRF-55110 certifications enjoy insulated pricing because defense and medical customers will not switch to lower-grade suppliers. Overall, the printed circuit board market size gains value as the mix shifts toward flex, rigid-flex, and IC substrates even while commodity unit volumes level off.

The Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer, High-Density Interconnect, Flexible Circuits, and More), Substrate Material (Glass Epoxy, High-Speed and Low-Loss, and More), End-User Industry (Consumer Electronics, Computing and Data Center, Telecommunications and 5G, Automotive and EV, Healthcare and Medical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 82.54% of global production in 2025 and is forecast to grow 4.86% annually, supported by integrated ecosystems in Guangdong, Jiangsu, and the Pearl River Delta where component sourcing, plating chemistry, and assembly lines co-locate. Taiwan anchors the advanced-substrate stack, with Unimicron, Nan Ya PCB, and Kinsus running semiconductor-grade clean rooms that feed both Intel and Taiwan Semiconductor Manufacturing Company. China's Shennan Circuits and DSBJ dominate smartphone HDI volumes but face tooling bottlenecks under United States export controls. Japan's Ibiden, Shinko Electric, and Meiko concentrate on high-reliability automotive and industrial boards, leveraging process patents in via fill and surface finish that command premium pricing. South Korean groups Samsung Electro-Mechanics and LG Innotek, historically captive to mobile phones, now channel capex toward automotive radar and data-center substrates.

North America captured roughly 8% printed circuit board market size in 2025 yet is scaling under United States CHIPS and Science Act tax credits and defense-offset clauses. TTM Technologies is investing USD 150 million in New York State for rigid-flex lines dedicated to avionics and radar. Defense primes stipulate domestic sourcing for mission-critical designs, raising utilization in smaller specialty shops across Arizona and California. Mexico leverages maquiladora status to assemble servers and telecom gear with imported boards, a conduit that keeps some volume inside the broader regional supply chain. Canada's footprint remains limited to high-mix, low-volume industrial and aerospace prototypes.

Europe held about 6% of 2025 volume yet benefits from the EUR 43 billion (USD 50.7 billion) European Chips Act that subsidizes advanced substrates and encourages dual sourcing for automotive safety systems. AT&S's Austrian and Malaysian split-site strategy aligns with German carmakers' preference for diversified risk. Schweizer Electronic is evaluating a joint venture in Arizona, reflecting trans-Atlantic attempts to secure defense and medical accounts. Eastern European countries such as Poland and the Czech Republic pitch lower labor costs plus European Union compliance, appealing for mid-range multilayer runs. Rest-of-world regions, including Latin America, Middle East and Africa, stay subscale, importing boards primarily from Asia for final assembly. Environmental regulations such as RoHS in Europe and TSCA in the United States drive uniform material standards worldwide, indirectly lifting quality benchmarks in emerging markets.

List of Companies Covered in this Report:

- Zhen Ding Technology Holding Ltd.

- Unimicron Technology Corp.

- Nippon Mektron Ltd.

- TTM Technologies Inc.

- Samsung Electro-Mechanics Co., Ltd.

- Compeq Manufacturing Co., Ltd.

- Tripod Technology Corporation

- Shennan Circuits Co., Ltd.

- Young Poong Electronics Co., Ltd.

- Ibiden Co., Ltd.

- HannStar Board Corp.

- AT&S AG

- LG Innotek Co., Ltd.

- Kinwong Electronic Co., Ltd.

- DSBJ (Dongshan Precision)

- Kingboard Holdings Ltd.

- Shinko Electric Industries Co., Ltd.

- Flexium Interconnect Inc.

- Nan Ya PCB Corp.

- Isola Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI Server and High-Performance Computing Demand

- 4.2.2 Accelerated EV Power Electronics Content

- 4.2.3 5G and Emerging 6G Transition Boosting HDI Adoption

- 4.2.4 Shift Toward Advanced IC Substrates for Chiplet Integration

- 4.2.5 Re-shoring Incentives in U.S. and EU for Critical PCB Supply Chains

- 4.2.6 Adoption of Ultra-Low-Loss Materials for 112-224 Gbps Signalling

- 4.3 Market Restraints

- 4.3.1 Prolonged Copper and Epoxy Resin Price Volatility

- 4.3.2 Talent Shortages in Advanced PCB Design and Process Engineering

- 4.3.3 Escalating ESG Compliance Costs for Waste-Water and PFAS Elimination

- 4.3.4 Geopolitical Export Controls Limiting Advanced Substrate Equipment

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By PCB Type

- 5.1.1 Standard Multilayer (non-HDI)

- 5.1.2 Rigid 1-2 Sided

- 5.1.3 High-Density Interconnect (HDI)

- 5.1.4 Flexible Circuits (FPC)

- 5.1.5 IC Substrates (Package Substrates)

- 5.1.6 Rigid-Flex

- 5.1.7 Other PCB Types

- 5.2 By Substrate Material

- 5.2.1 Glass Epoxy (FR-4)

- 5.2.2 High-Speed and Low-Loss

- 5.2.3 Polyimide (PI)

- 5.2.4 Packaging Resins (BT and ABF)

- 5.2.5 Other Substrate Materials

- 5.3 By End-User Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Computing and Data Centers

- 5.3.3 Telecommunications and 5G

- 5.3.4 Automotive and EV

- 5.3.5 Industrial and Power

- 5.3.6 Healthcare and Medical

- 5.3.7 Aerospace and Defense

- 5.3.8 Other End-User Industries

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Taiwan

- 5.4.3.3 Japan

- 5.4.3.4 India

- 5.4.3.5 South Korea

- 5.4.3.6 Southeast Asia

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Rest of World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Zhen Ding Technology Holding Ltd.

- 6.4.2 Unimicron Technology Corp.

- 6.4.3 Nippon Mektron Ltd.

- 6.4.4 TTM Technologies Inc.

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Compeq Manufacturing Co., Ltd.

- 6.4.7 Tripod Technology Corporation

- 6.4.8 Shennan Circuits Co., Ltd.

- 6.4.9 Young Poong Electronics Co., Ltd.

- 6.4.10 Ibiden Co., Ltd.

- 6.4.11 HannStar Board Corp.

- 6.4.12 AT&S AG

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 Kinwong Electronic Co., Ltd.

- 6.4.15 DSBJ (Dongshan Precision)

- 6.4.16 Kingboard Holdings Ltd.

- 6.4.17 Shinko Electric Industries Co., Ltd.

- 6.4.18 Flexium Interconnect Inc.

- 6.4.19 Nan Ya PCB Corp.

- 6.4.20 Isola Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

印刷基板市場規模、佔有率和成長分析:按產品類型、最終用戶和地區分類-2026-2033年產業預測

印刷基板市場規模、佔有率和成長分析:按產品類型、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球印刷基板(PCB)市場

2026-2030年全球印刷基板(PCB)市場 印刷基板市場:2026-2032年全球市場預測(依類型、基板結構、材料、元件安裝方式、層數、製造流程、應用、終端用戶產業及銷售管道)

印刷基板市場:2026-2032年全球市場預測(依類型、基板結構、材料、元件安裝方式、層數、製造流程、應用、終端用戶產業及銷售管道) AI推理伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年)

AI推理伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年) 印刷基板市場規模、佔有率和趨勢分析報告:按產品類型、基板材料、最終用途、地區和細分市場預測(2026-2033 年)通用伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年)

印刷基板市場規模、佔有率和趨勢分析報告:按產品類型、基板材料、最終用途、地區和細分市場預測(2026-2033 年)通用伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年) 印刷基板(PCB) 市場預測:至 2034 年-按類型、基板型、應用和地區分類的全球分析5G印刷基板市場:按基板類型、基板材料、層數和應用分類-全球預測,2026-2032年光學模組印刷電路基板技術市場:依技術類型、材料類型、層數、頻率範圍及最終用途分類-2026年至2032年全球預測

印刷基板(PCB) 市場預測:至 2034 年-按類型、基板型、應用和地區分類的全球分析5G印刷基板市場:按基板類型、基板材料、層數和應用分類-全球預測,2026-2032年光學模組印刷電路基板技術市場:依技術類型、材料類型、層數、頻率範圍及最終用途分類-2026年至2032年全球預測 高密度互連(HDI)印刷基板市場規模、佔有率、趨勢和預測:按HDI層數、最終用途行業和地區分類,2026-2034年

高密度互連(HDI)印刷基板市場規模、佔有率、趨勢和預測:按HDI層數、最終用途行業和地區分類,2026-2034年