|

市場調查報告書

商品編碼

2044151

水溶性薄膜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Water Soluble Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

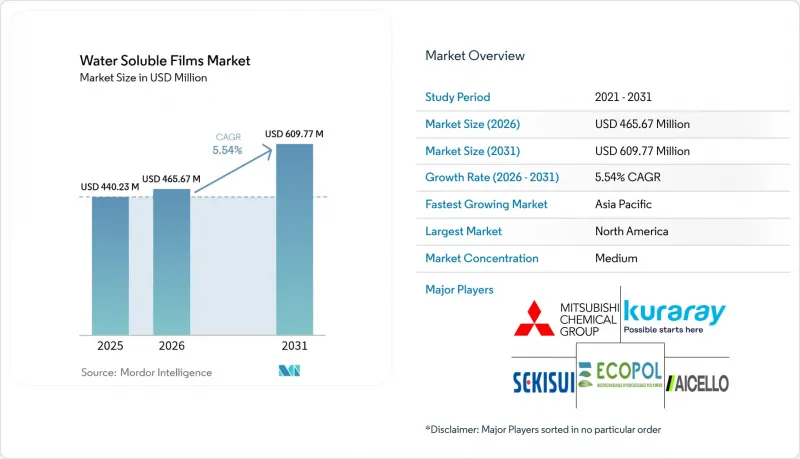

2025 年水溶性薄膜市值為 4.4023 億美元,預計到 2031 年將達到 6.0977 億美元,而 2026 年為 4.6567 億美元,預測期(2026-2031 年)複合年成長率為 5.54%。

這一成長曲線由三大支柱支撐:對便捷一次性包裝日益成長的需求、支持生物分解材料的監管趨勢,以及製造商成功開發出適合家庭洗衣習慣的冷水洗滌劑。然而,聚乙烯醇(PVA)的原料成本高於聚乙烯,其在熱帶氣候下易受潮導致物流成本增加,以及未來PVA廢水處理的不確定性,都阻礙了其發展。隨著垂直整合的中國供應商縮小與日本和歐洲老牌企業的價格差距,競爭日趨激烈;與此同時,生物基新參與企業正在探索澱粉和海藻基生產方法,這些方法預計將在未來十年重新定義成本績效。

全球水溶性薄膜市場趨勢及洞察

一次性清潔劑和清潔劑膠囊的使用量正在迅速成長。

洗衣液和餐具清潔劑品牌正不斷將銷售量轉向室溫水中即可溶解的膠囊型產品,這種產品能夠提供高濃度的活性成分,且不會造成殘留申訴。據各品牌稱,這些膠囊的價格比散裝清潔劑高出20-30%。此外,2025年推出的不透明或苦味塗層薄膜預計將使誤食風險降低約30%。目前,全自動洗衣機在美國家庭的普及率接近45%,但在印度和東南亞部分地區,由於手洗盛行,這一比例仍然很低。

擴大一次性農藥包裝小袋的使用範圍

水溶性小袋包裝有助於監管機構控制地下水污染,因為它消除了小規模農戶的稱重誤差,並將活性成分的浪費減少了高達 25%。馬哈拉斯特拉邦和卡納塔克邦的補貼計畫部分抵消了其比散裝包裝高出 10-15% 的價格溢價,印度的市場也持續保持兩位數成長。

易受潮性和儲存壽命方面的問題

由於聚乙烯醇(PVA)薄膜在相對濕度為80%的環境中會吸收高達10%的水分,加工商不得不採用貼合加工或乾燥劑包裝,這會使每平方公尺的成本增加0.05至0.08美元,並在熱帶氣候下將保存期限縮短至僅四個月。阻隔塗層可減少高達60%的水蒸氣透過率,但會減緩溶解速度,因此難以找到理想的平衡點。在新興市場,口服藥物薄膜的低溫運輸物流也會使接收成本增加15%至20%。

細分市場分析

到2025年,冷水溶性薄膜將佔水溶性薄膜市場85.26%的佔有率,這反映了家庭洗衣習慣的趨勢,即70-80%的衣物採用冷水或熱水洗滌。隨著洗衣凝珠系統在新興都市區的普及,冷水級水溶性薄膜的市場規模正以5.75%的複合年成長率成長。持續的研發工作正在最佳化塑化劑配方,以在20度C下實現30秒溶解的同時,兼顧薄膜的柔軟性。同時,對於醫院洗衣和工業染色等處理水溫超過60度C的場合,高品質熱水級水溶性薄膜仍然至關重要。

第二代熱水產品採用醋酸乙烯酯共聚物,這種共聚物在達到高溫前溶解速度較慢,可防止在潮濕的儲存環境中過早劣化,從而獲得15-20%的溢價。日本嚴格的食品接觸法規將於2025年中期生效,該法規有利於能夠提供所有添加劑證明的成熟製造商,這既能減緩新參與企業的擴張速度,又能確保在小眾高溫應用領域中產品品質的穩定性。

《水溶性薄膜市場報告》按類型(冷水溶性薄膜和熱水溶性薄膜)、溶解速率(快速溶解薄膜、中速溶解薄膜和慢速溶解薄膜)、終端用戶行業(包裝、醫藥保健及其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,北美將佔全球銷售量的39.91%,主要得益於美國都市區家庭中清潔劑和洗潔精清潔劑超過40%的滲透率。然而,成長速度正在放緩,因為未來的擴張將取決於農村消費者接受度的降低以及向農藥和醫療保健等細分市場的多元化發展,而這些領域仍然存在成本障礙。 2024年推出的自願性安全指南將繼續迫使供應商採用不透明或苦味塗層薄膜,這將使每單位成本增加幾美分,但有助於維護品牌價值。

預計亞太地區將以6.20%的複合年成長率(CAGR)實現最高成長,直至2031年。這主要得益於中國和印度實施的生產者延伸責任制(EPR)法規,該法規對多層軟包裝施加了處罰。當地供應商正利用樹脂成本低廉的優勢,拓展業務至農藥、刺繡襯裡以及透過電商平台銷售的入門級清潔劑凝珠等領域。日本的「3R+可再生」獎勵正推動市場逐步轉向生物基或高生物分解性的聚乙烯醇(PVA)產品,並對通過EN 13432認證的供應商給予獎勵。

在歐洲,隨著2030年可回收性和可堆肥性目標的臨近,廢水中殘留聚乙烯醇(PVA)的監測力度正在增加。在德國、法國和英國,洗碗機的高普及率(尤其是便利的洗滌劑膠囊)構成了市場需求的基礎,但PVA可能被歸類為微塑膠,這或許會促使市場轉向使用分解速度更快的共聚物配方。在南歐和東歐市場,基礎設施尚不完善,儘管監管目標通用,但銷售量成長正在放緩。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 一次性清潔劑和清潔劑膠囊的使用量正在迅速成長。

- 擴大一次性農藥包裝袋的尺寸

- 全球政策推廣可生物分解包裝

- 食品和飲料的單份包裝。

- 用於3D列印的可溶性支撐材料

- 市場限制因素

- 對水分敏感和保存期限的問題

- 與傳統塑膠相比,製造成本更高

- 對廢水中聚乙烯醇(PVA)的排放制定更嚴格的標準

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 按類型

- 冷水溶性薄膜

- 熱溶性薄膜

- 按溶解速率

- 快速溶解膜

- 中等溶解度膜

- 難溶性薄膜

- 按最終用戶行業分類

- 包裹

- 纖維

- 製藥和醫療保健

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 比荷盧經濟聯盟

- 奧地利

- 捷克共和國

- 波蘭

- 匈牙利

- 瑞士

- 北歐國家

- 斯洛伐克

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 摩洛哥

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AICELLO CORPORATION

- AMC(UK)Ltd

- Arrow Greentech Ltd.

- Changzhou Greencradleland Macromolecule Materials Co., Ltd.

- Cortec Corporation

- ECOMAVI SRL

- Ecopol SpA

- Foshan Polyva Materials Co. Ltd

- Green Cycles

- Guangdong Proudly New Material Technology Co. Ltd

- HARKE GROUP

- INFHIDRO

- KURARAY CO., LTD.

- Mitsubishi Chemical Group Corporation

- Mondi

- Noble Industries

- Novacel

- SEKISUI CHEMICAL CO., LTD.

- Soltec Development

第7章 市場機會與未來展望

The Water Soluble Films Market size was valued at USD 440.23 million in 2025 and is estimated to grow from USD 465.67 million in 2026 to reach USD 609.77 million by 2031, at a CAGR of 5.54% during the forecast period (2026-2031).

The growth curve rests on three pillars: rising demand for convenient unit-dose packaging, regulatory momentum favoring compostable materials, and manufacturers' success in refining cold water grades that match household washing habits. Yet progress is tempered by the high raw-material cost of polyvinyl alcohol (PVA) versus polyethylene, moisture-sensitivity that inflates logistics expenses in tropical climates, and ambiguity around future wastewater discharge limits for PVA. Competitive intensity is increasing as vertically integrated Chinese suppliers narrow the price gap with Japanese and European incumbents, while bio-based challengers explore starch or seaweed routes that could reset the cost-performance frontier over the next decade.

Global Water Soluble Films Market Trends and Insights

Surging Adoption of Unit-Dose Detergent and Dish-Wash Pods

Laundry and dishwasher brands continue to shift volume into pod formats that dissolve in ambient water, allowing concentrated actives to be delivered without residue complaints. Brands report 20-30% price premiums over bulk detergents, while opaque or bitter-coated films introduced in 2025 have cut accidental-ingestion incidents by around 30%. Penetration now stands near 45% of U.S. automatic-washer households, although handwashing prevalence keeps adoption lower in India and parts of Southeast Asia.

Expansion of Agrochemical Single-Use Sachets

Water soluble sachets eliminate measuring errors for smallholder farmers and reduce active-ingredient waste by up to 25%, helping regulators curb groundwater contamination. Subsidy programs in Maharashtra and Karnataka partially offset the 10-15% price premium versus bulk packaging, sustaining double-digit growth in India.

Moisture-Sensitivity and Shelf-Life Issues

PVA films absorb up to 10% moisture at 80% relative humidity, forcing converters to use laminated or desiccant-lined packaging that adds USD 0.05-0.08 per m2 and shortens effective shelf-life in tropical climates to as little as four months. Barrier coatings cut vapor transmission up to 60% but can slow dissolution, making a perfect balance elusive. Cold-chain distribution for pharmaceutical oral films further inflates landed costs by 15-20% in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Global Policy Push for Biodegradable Packaging

- Edible Single-Serve Food and Beverage Sachets

- High Production Costs vs. Conventional Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cold water-soluble films held 85.26% of the water soluble films market in 2025, reflecting alignment with household washing practices where 70-80% of loads use cold or warm cycles. The water soluble films market size for cold water grades is advancing at 5.75% CAGR as pod formats deepen in emerging urban centers. Ongoing R&D optimizes plasticizer blends to balance flexibility with 30-second dissolution at 20 °C, while premium hot water grades remain vital in hospital laundry and industrial dyeing where process water exceeds 60 °C.

Second-generation hot water variants command 15-20% price premiums, leveraging vinyl-acetate copolymers that delay dissolution until elevated temperatures are met, preventing premature breakdown in humid storerooms. Japan's stringent food-contact regime, enforced since mid-2025, favors incumbents able to document every additive, slowing new-entrant expansion but ensuring consistent quality in niche high-temperature applications.

The Water Soluble Films Market Report is Segmented by Type (Cold Water-Soluble Films and Hot Water-Soluble Films), Dissolution Rate (Fast-Soluble Films, Medium-Soluble Films, and Difficult-Soluble Films), End-User Industry (Packaging, Pharmaceutical and Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

North America captured 39.91% of global volume in 2025, supported by detergent and dish-wash pod penetration above 40% in U.S. metro households. Growth decelerates because incremental adoption now depends on converting late-adopter rural consumers and diversifying into agrochemical or healthcare niches where cost hurdles persist. Voluntary safety guidelines introduced in 2024 continue to push suppliers toward opaque or bitter-coated films, adding pennies per unit but protecting brand equity.

Asia-Pacific is the fastest-growing region at 6.20% CAGR through 2031 as China and India enforce EPR mandates that penalize multilayer flexibles. Local suppliers exploit lower resin costs to expand in agrochemicals, embroidery backing, and increasingly in entry-level detergent pods sold through e-commerce platforms. Japan's 3R+Renewable incentives trigger modest substitution toward bio-based or high-biodegradability PVA variants, rewarding suppliers that certify EN 13432 compliance.

In Europe, looming 2030 recyclability and compostability deadlines intensify scrutiny of residual PVA in wastewater. Germany, France, and the United Kingdom anchor demand through high dishwasher ownership rates that value pod convenience, but potential microplastic classification could spur reformulation toward faster-biodegrading copolymers. Southern and Eastern European markets lag in infrastructure, tempering volume growth despite shared regulatory ambitions.

- AICELLO CORPORATION

- AMC (UK) Ltd

- Arrow Greentech Ltd.

- Changzhou Greencradleland Macromolecule Materials Co., Ltd.

- Cortec Corporation

- ECOMAVI SRL

- Ecopol S.p.A.

- Foshan Polyva Materials Co. Ltd

- Green Cycles

- Guangdong Proudly New Material Technology Co. Ltd

- HARKE GROUP

- INFHIDRO

- KURARAY CO., LTD.

- Mitsubishi Chemical Group Corporation

- Mondi

- Noble Industries

- Novacel

- SEKISUI CHEMICAL CO., LTD.

- Soltec Development

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of unit-dose detergent and dish-wash pods

- 4.2.2 Expansion of agrochemical single-use sachets

- 4.2.3 Global policy push for biodegradable packaging

- 4.2.4 Edible single-serve food and beverage sachets

- 4.2.5 3-D-printing dissolvable support materials

- 4.3 Market Restraints

- 4.3.1 Moisture-sensitivity and shelf-life issues

- 4.3.2 High production costs vs. conventional plastics

- 4.3.3 Tightening PVA discharge limits in wastewater

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Cold Water-soluble Films

- 5.1.2 Hot Water-soluble Films

- 5.2 By Dissolution Rate

- 5.2.1 Fast-soluble Films

- 5.2.2 Medium-soluble Films

- 5.2.3 Difficult-soluble Films

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Textile

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Benelux

- 5.4.3.6 Austria

- 5.4.3.7 Czech Republic

- 5.4.3.8 Poland

- 5.4.3.9 Hungary

- 5.4.3.10 Switzerland

- 5.4.3.11 NORDIC Countries

- 5.4.3.12 Slovakia

- 5.4.3.13 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Morocco

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AICELLO CORPORATION

- 6.4.2 AMC (UK) Ltd

- 6.4.3 Arrow Greentech Ltd.

- 6.4.4 Changzhou Greencradleland Macromolecule Materials Co., Ltd.

- 6.4.5 Cortec Corporation

- 6.4.6 ECOMAVI SRL

- 6.4.7 Ecopol S.p.A.

- 6.4.8 Foshan Polyva Materials Co. Ltd

- 6.4.9 Green Cycles

- 6.4.10 Guangdong Proudly New Material Technology Co. Ltd

- 6.4.11 HARKE GROUP

- 6.4.12 INFHIDRO

- 6.4.13 KURARAY CO., LTD.

- 6.4.14 Mitsubishi Chemical Group Corporation

- 6.4.15 Mondi

- 6.4.16 Noble Industries

- 6.4.17 Novacel

- 6.4.18 SEKISUI CHEMICAL CO., LTD.

- 6.4.19 Soltec Development

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

水溶性薄膜市場-2026-2032年全球市場預測

水溶性薄膜市場-2026-2032年全球市場預測 水溶性薄膜:全球市場

水溶性薄膜:全球市場 水溶性薄膜市場規模、佔有率、趨勢和預測:按材料、應用、終端用戶產業和地區分類,2026-2034年

水溶性薄膜市場規模、佔有率、趨勢和預測:按材料、應用、終端用戶產業和地區分類,2026-2034年 全球水溶性薄膜市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球水溶性薄膜市場規模、佔有率、趨勢和成長分析報告(2026-2034) 水溶性薄膜市場商機、成長要素、產業趨勢分析及2026-2035年預測。

水溶性薄膜市場商機、成長要素、產業趨勢分析及2026-2035年預測。 水溶性薄膜市場:按類型、溶解速率、終端用途產業和地區分類。

水溶性薄膜市場:按類型、溶解速率、終端用途產業和地區分類。 水溶性薄膜市場:2035年前的產業趨勢和全球預測 - 各材料類型,各薄膜類型,各溶解速度,各終端用戶類型,不同企業規模,各主要地區水溶性薄膜市場-2025年至2030年的預測

水溶性薄膜市場:2035年前的產業趨勢和全球預測 - 各材料類型,各薄膜類型,各溶解速度,各終端用戶類型,不同企業規模,各主要地區水溶性薄膜市場-2025年至2030年的預測 2032 年水溶性薄膜市場預測:按薄膜類型、材料類型、溶解速率、厚度、分銷管道、應用和地區進行的全球分析

2032 年水溶性薄膜市場預測:按薄膜類型、材料類型、溶解速率、厚度、分銷管道、應用和地區進行的全球分析 水溶性薄膜市場,規模,佔有率,趨勢,產業分析報告:各類型,各用途,各地區 - 市場預測 2025年~2034年

水溶性薄膜市場,規模,佔有率,趨勢,產業分析報告:各類型,各用途,各地區 - 市場預測 2025年~2034年