|

市場調查報告書

商品編碼

2044149

運動穿戴裝置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Wearable Devices In Sports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

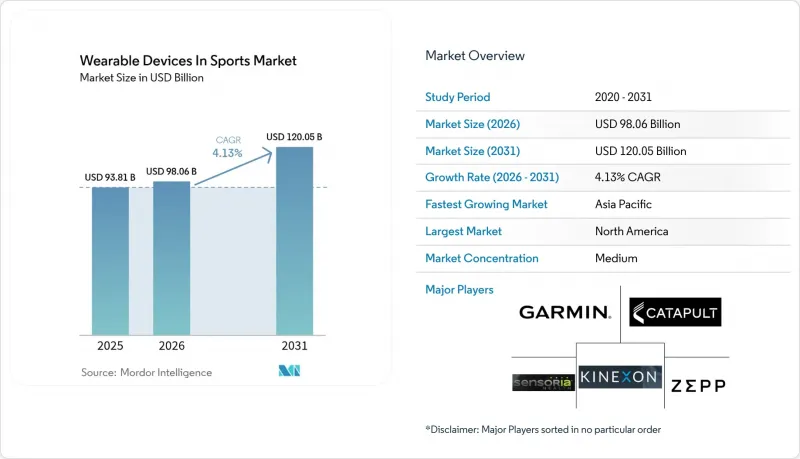

預計運動穿戴裝置的市場規模將從 2025 年的 938.1 億美元成長到 2026 年的 980.6 億美元,到 2031 年將達到 1,200.5 億美元,2026 年至 2031 年的複合年成長率為 4.13%。

職業聯賽如今已將生物辨識數據追蹤納入集體談判協議,而能夠即時計算受傷風險評分的人工智慧教練系統也越來越受到一般用戶的歡迎。索尼在2025年收購STATSports,正是平台整合趨勢的典型例證,該趨勢融合了感測器硬體和雲端分析技術。光纖整合感測器能夠捕捉運動、體溫和電生理訊號,且不會限制運動,這使得該領域不再局限於腕帶,從而滿足了人們對穿著舒適如普通運動服的穿戴式服裝的需求。北美地區的領先地位得益於NFL(美國國家橄欖球聯盟)和MLB(美國職棒大聯盟)強制監測頭部撞擊和投球生物力學數據,但隨著GPS追蹤技術在印度板球和中國學院計畫中得到應用,亞太地區的成長速度更快。主要風險在於集體談判協議中新增的資料隱私條款,這些條款可能會限制生物辨識資料出售給第三方,並延緩產品推廣。

全球穿戴式裝置市場趨勢及運動領域洞察

對數據驅動型績效分析的需求日益成長

目前,各球隊已將生物辨識數據視為合約交付內容,並將恢復評分納入球員資格條款。職業網球協會(ATP)核准在2024年比賽中使用穿戴式設備,以便根據運動負荷閾值和場地覆蓋熱圖即時調整教練策略。大學球探正在向有潛力的球員索取多年資料集,從而催生了次市場。美國國家橄欖球聯盟球員協會(NFLPA)於2024年開設了一個集中式數據存儲庫,允許球員向研究人員提供匿名數據,同時保留對商業用途的否決權。保險公司也正在根據球員以往使用穿戴式裝置的情況計算傷病風險保費,並將分析結果進一步納入合約談判。這種制度化正在將穿戴式裝置從可有可無的小玩意轉變為必不可少的基礎設施。

人工智慧驅動的多感測器穿戴裝置的整合正在穩步推進。

最新設備將慣性測量單元、體積描記法、電阻和多頻段全球導航衛星系統整合於外形規格。三星Galaxy Watch7於2026年2月發布,其內建神經網路無需雲端延遲即可對運動強度進行分類,從而降低了比賽期間資料外洩的擔憂。 Garmin HRM-600胸帶結合了心電圖等級的心率監測和跑步動態感測器,可追蹤觸地時間,專為追求臨床級精度的耐力運動員而設計。 Kinexon在歐洲籃球聯賽中採用的系統利用超寬頻(UWB)錨點三角定位球員位置,精確度小於10厘米,並將疲勞指數直接傳輸給教練。邊緣處理技術減少了對賽後分析的依賴,使得球員能夠在比賽中進行戰術調整,而此前這些調整隻能在中場休息時進行。

高昂的初始設備成本和有限的運動預算

來自 Catapult 和 STATSports 等公司的企業級設備,每支隊伍的成本超過 5 萬美元,每年的軟體費用在 1 萬到 3 萬美元之間,這對二級和三級大學計畫來說是一筆不小的負擔。休閒運動員不願意為捆綁了持續訂閱服務的設備支付 300 到 500 美元,尤其是在已有提供基本追蹤功能的免費智慧型手機應用程式的情況下。這種兩極化造成了高階專業市場和大眾消費市場的局面,限制了可能為創新提供資金的跨部門合作。

細分市場分析

到2025年,健身和心率監測器將佔據運動穿戴裝置市場38.21%的佔有率,這反映出休閒跑步者和騎乘者對這類產品的廣泛使用。智慧服裝和電子紡織品預計將以6.93%的複合年成長率成長,成長超過整體運動穿戴裝置市場,因為運動員逐漸轉向無需攜帶單一設備的服裝。 Garmin的Forerunner 970將於2025年5月發布,它採用多頻段GNSS技術,即使在人口密集的都市區也能保持定位精度。 FORM的Smart Swim 2泳鏡將於2024年8月發布,它將即時測量數據疊加到透明顯示器上,從而避免了游泳時查看手腕的干擾。

PlayerMaker與德甲聯賽的合作推動了鞋類感測器的普及,這些感測器能夠測量擊球質量,這項技術曾經僅限於實驗室。頭戴式擴增實境(AR)顯示器,例如Garmin於2026年1月推出的Xero L60i,可以將高爾夫球距離投射到眼鏡產品鏡片上,這預示著抬頭顯示介面將進一步普及。口腔感測器,例如獲得FDA核准的e-Celsius膠囊,正在被NFL球隊用於追蹤體溫,但仍面臨成本和運動員接受度方面的障礙。石墨烯增強織物可望實現可機洗的導電性,這或許能在預測期內消除對剛性感測器外殼的需求。

到2025年,足球和美式足球將佔穿戴式裝置市場總收入的26.43%,這主要得益於歐洲俱樂部為最佳化定位而將GPS追蹤技術標準化。同時,游泳和競技游泳預計將在運動市場規模成長方面超越整體穿戴式裝置市場,到2031年將維持7.01%的複合年成長率。 Prevent Biometrics公司的護齒器可以記錄美式足球運動中的頭部撞擊,並記錄腦震盪暴露情況,從而降低法律責任風險。在棒球領域,Motus Global公司的mThrow 2.0護肘正被用來監測投手尺側副韌帶的應力。

在板球領域,隨著國際板球理事會(ICC)的核准,Catapult設備的普及速度加快,印度國家隊已開始使用Catapult設備進行投球手負荷管理。自行車和鐵人三項運動員需要能夠在游泳、騎行和跑步模式之間切換的設備,Garmin的Forerunner 570正好滿足了這一需求。極限運動愛好者則更注重耐用性和數天的電池續航時間,Apple Watch Ultra 3憑藉36小時的連續使用時間和40米防水性能,完美契合了這一需求。游泳領域的快速成長也凸顯了運動追蹤器市場正從通用型產品轉向專業比賽解決方案的轉變。

區域分析

預計到2025年,北美將佔全球銷售額的41.72%,主要得益於聯盟強制要求對頭部撞擊和投擲生物力學進行監測。一級聯盟大學投入數百萬美元預算以滿足NCAA的健康指南,從而形成穩定的企業客戶群。消費者強大的購買力使平均售價保持在高階水平,為供應商創造了一個盈利的生態系統。

亞太地區預計將以4.98%的複合年成長率成長。這主要歸功於一些因素,例如中國政府支持的人才選拔學院將穿戴式裝置作為標準配備,以及印度板球聯合會將GPS追蹤技術標準化。在日本,由於人口老化,跌倒風險追蹤設備的普及率正在上升;在韓國,通訊業者透過與通訊套餐捆綁銷售的方式補貼Galaxy Watch的購買。這些因素正在將目標市場從競技運動員擴展到更廣泛的群體。

在歐洲,職業足球聯賽正努力在嚴格的GDPR要求和對運動科學的積極投資之間尋求平衡。英國和愛爾蘭雄獅隊的2025年工作負載串流舉措概述了一條透過獲利模式來抵消合規成本的途徑。中東各國政府正在投資興建配備擴增實境(AR)分析技術的體育場,以實現經濟多元化。在南美洲,由於關稅的影響,通貨膨脹持續存在,但巴西俱樂部正在引入GPS以趕上歐洲標準。非洲的GPS應用才剛起步,主要集中在南非的橄欖球和肯亞的長跑計畫上,但受到終端成本和通訊基礎設施差異的限制。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對數據驅動型績效分析的需求日益成長

- 人工智慧驅動的多感測器穿戴裝置的整合正在穩步推進。

- 拓展全球體育賽事與粉絲互動平台

- 其高度便攜和方便的外形規格正在推動其在日常生活中廣泛應用。

- 聯盟批准的生物識別數據貨幣化框架

- 用於預防傷害的光纖整合多模態感測器

- 市場限制因素

- 高昂的初始設備成本和有限的運動預算

- 消費者對資料隱私和安全的擔憂日益加劇

- 供應商之間資料生態系統的互通性差距

- 關於使用生物識別數據的集體談判限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依設備類型

- 健身和心率監測器

- 智慧服裝和電子紡織品

- GPS/GNSS追蹤器

- 配備相機和視覺功能的穿戴式設備

- 鞋類和鞋內感應器

- 頭戴式和擴增實境顯示器

- 植入式感測器和其他新興感測器

- 透過運動

- 足球

- 籃球

- 美式足球和橄欖球

- 棒球/壘球

- 蟋蟀

- 高爾夫和網球

- 自行車和鐵人三項

- 游泳和游泳比賽

- 極限冒險運動

- 最終用戶

- 職業球隊和聯賽

- 面向大學和高等教育機構的項目

- 業餘球員和俱樂部球員

- 休閒健身愛好者

- 體育學院和訓練中心

- 醫療復健機構

- 透過分銷管道

- 線上(直銷和市場)

- 體育用品專賣店

- 量販店和量販店

- 團隊/公司合約

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Kinexon GmbH

- Garmin Ltd.

- Sensoria Inc.

- Zepp Health Corporation

- Catapult Group International Ltd.

- Samsung Electronics Co., Ltd.

- Alphabet Inc.(Google LLC/Fitbit LLC)

- STATSports Group Ltd.

- Whoop, Inc.

- Polar Electro Oy

- Carre Technologies Inc.(Hexoskin)

- Zephyr Technology Corporation

- Firstbeat Technologies Oy

- Apple Inc.

- Playermaker Ltd.

- Motus Global LLC

- X2 Biosystems, Inc.

- Nix, Inc.

- hDrop Technologies, Inc.

- Adidas AG

第7章 市場機會與未來展望

The wearable devices in sports market size is expected to increase from USD 93.81 billion in 2025 to USD 98.06 billion in 2026 and reach USD 120.05 billion by 2031, growing at a CAGR of 4.13% over 2026-2031.

Professional leagues now embed biometric tracking in collective-bargaining agreements, while recreational users adopt AI-driven coaching that assigns real-time injury-risk scores. Sony's 2025 purchase of STATSports exemplifies a shift toward platform consolidation that marries sensor hardware with cloud analytics. Textile-integrated sensors that capture kinetic, thermal, and electrophysiological signals without restricting movement move the category beyond wristbands, supporting demand for garments that feel like ordinary sportswear. North American dominance rests on National Football League and Major League Baseball mandates for head-impact and pitch-biomechanics monitoring, yet Asia-Pacific posts faster growth as Indian cricket and Chinese academy programs institutionalize GPS tracking. Headline risks center on new data-privacy clauses in collective-bargaining agreements that restrict third-party sales of biometric data and slow product rollouts.

Global Wearable Devices In Sports Market Trends and Insights

Growing Demand for Data-Driven Performance Analytics

Teams now treat biometric metrics as contractual deliverables, embedding recovery scores in player-availability clauses. The Association of Tennis Professionals approved in-competition wearables in 2024, allowing real-time coaching adjustments that rely on exertion thresholds and court-coverage heat maps. Collegiate recruiters request multi-year datasets from prospects, creating a secondary market for longitudinal performance archives. The National Football League Players Association opened a centralized repository in 2024 so athletes can license anonymized data to researchers while retaining veto rights over commercial use. Insurers also price injury risk off historical wearable trends, further embedding analytics in contract negotiations. This institutionalization transforms wearables from optional gadgets into required infrastructure.

Rising Integration of AI-Powered Multi-Sensor Wearables

Modern devices fuse inertial measurement units, photoplethysmography, bioimpedance, and multi-band GNSS into single form factors. Samsung's Galaxy Watch7, released in February 2026, houses on-device neural networks that classify workout intensity without cloud latency, mitigating data-leakage fears during live competition. Garmin's HRM-600 chest strap pairs ECG-grade heart monitoring with running-dynamics pods that track ground-contact time for endurance athletes demanding clinical-level precision. Kinexon's EuroLeague deployment uses ultra-wideband anchors to triangulate player positions within 10 cm, feeding fatigue indices directly to bench coaches. Edge processing lowers dependence on post-session analysis, enabling in-game tactical pivots once confined to halftime.

High Initial Device Cost and Tight Athletics Budgets

Enterprise-grade kits from Catapult or STATSports cost more than USD 50,000 per team, with annual software fees of USD 10,000-30,000, squeezing Division II and III college programs. Recreational athletes balk at USD 300-500 devices bundled with ongoing subscriptions when free smartphone apps deliver basic tracking. This bifurcation creates premium professional tiers and commoditized consumer segments, limiting cross-subsidization that could fund feature innovation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Global Sports Events and Fan-Engagement Platforms

- Portable and Convenient Form Factors Boosting Daily Adoption

- Escalating Consumer Data-Privacy and Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, fitness and heart-rate monitors commanded 38.21% of wearable devices in sports market share, reflecting entrenched adoption among recreational runners and cyclists. Smart clothing and e-textiles are projected to grow at a 6.93% CAGR, outpacing the overall wearable devices in sports market size growth as athletes shift toward garments that eliminate the need to remember separate gadgets. Garmin's Forerunner 970, launched in May 2025, uses multi-band GNSS to retain accuracy in dense urban terrain. FORM's Smart Swim 2 goggles, released in August 2024, overlay live metrics onto transparent displays, removing the cognitive disruption of mid-stroke wrist checks.

Footwear sensors gained traction after PlayerMaker's Bundesliga partnership, measuring ball-contact quality that was once laboratory-bound. Head-mounted augmented-reality displays, such as Garmin's Xero L60i introduced in January 2026, project golf yardage onto eyewear lenses, hinting at wider acceptance of heads-up interfaces. Ingestible sensors like the FDA-cleared e-Celsius capsule track core temperature for NFL teams but face cost and athlete-acceptance barriers. Graphene-infused fabrics promise machine-washable conductivity, potentially rendering rigid sensor housings obsolete during the forecast horizon

Soccer and football held 26.43% of 2025 revenue as European clubs normalized GPS tracking for positional play optimization. Swimming and aquatics, however, will surpass overall wearable devices in sports market size growth, posting a 7.01% CAGR through 2031. Prevent Biometrics' mouthguard logs American-football head impacts to document concussion exposure for liability mitigation. Baseball leverages Motus Global's mThrow 2.0 elbow sleeve to monitor ulnar-collateral-ligament stress in pitchers.

Cricket adoption accelerated after ICC approvals, with India's national team deploying Catapult units for bowler workload management. Cycling and triathlon athletes demand devices that transition through swim, bike, and run modes, a gap Garmin filled with the Forerunner 570. Extreme-sports participants value ruggedness and multi-day battery life, met by Apple's Watch Ultra 3 rated for 36-hour runtime and 40-m depth. The aquatics surge underscores a wider pivot toward discipline-specific solutions over generic trackers.

The Wearable Devices in Sports Market Report is Segmented by Device Type (Fitness and Heart-Rate Monitors, Smart Clothing and E-Textiles, and More), Sport (Soccer / Football, Basketball, and More), End User(Professional Teams and Leagues, and More), Distribution Channel (Online, Specialty Sports Stores, Mass-Retail and Electronics Chains, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.72% revenue in 2025, powered by league mandates for head-impact and pitch-biomechanics monitoring. Division I universities dedicate seven-figure budgets to satisfy NCAA health guidelines, providing a captive enterprise clientele. High consumer purchasing power sustains premium average selling prices and supports a profitable ecosystem for vendors.

Asia-Pacific will grow at 4.98% CAGR as China's government-backed academies use wearable benchmarks for talent identification and India's cricket federation normalizes GPS tracking. Japan's aging population adopts devices to track fall risk, while South Korean carriers subsidize Galaxy Watch models through connectivity bundles. These factors simultaneously expand the addressable base beyond competitive athletes.

Europe balances stringent GDPR requirements with strong sports-science investments by professional football leagues. The British and Irish Lions' 2025 workload-streaming initiative illustrates monetization paths that offset compliance costs. Middle Eastern governments invest in stadiums wired for augmented-reality analytics to diversify economies. South America endures tariff-driven price inflation, though Brazilian clubs adopt GPS to keep pace with European standards. African uptake is nascent, anchored in South African rugby and Kenyan distance-running programs but constrained by device costs and connectivity gaps.

- Kinexon GmbH

- Garmin Ltd.

- Sensoria Inc.

- Zepp Health Corporation

- Catapult Group International Ltd.

- Samsung Electronics Co., Ltd.

- Alphabet Inc. (Google LLC / Fitbit LLC)

- STATSports Group Ltd.

- Whoop, Inc.

- Polar Electro Oy

- Carre Technologies Inc. (Hexoskin)

- Zephyr Technology Corporation

- Firstbeat Technologies Oy

- Apple Inc.

- Playermaker Ltd.

- Motus Global LLC

- X2 Biosystems, Inc.

- Nix, Inc.

- hDrop Technologies, Inc.

- Adidas AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Data-Driven Performance Analytics

- 4.2.2 Rising Integration of AI-Powered Multi-Sensor Wearables

- 4.2.3 Expansion of Global Sports Events and Fan-Engagement Platforms

- 4.2.4 Portable and Convenient Form-Factors Boosting Daily Adoption

- 4.2.5 League-Sanctioned Biometric-Data Monetization Frameworks

- 4.2.6 Textile-Integrated Multimodal Sensors for Injury Prevention

- 4.3 Market Restraints

- 4.3.1 High Initial Device Cost and Tight Athletics Budgets

- 4.3.2 Escalating Consumer Data-Privacy and Security Concerns

- 4.3.3 Interoperability Gaps Across Vendor Data Ecosystems

- 4.3.4 Collective-Bargaining Limits on Biometric Data Use

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Fitness and Heart-Rate Monitors

- 5.1.2 Smart Clothing and E-Textiles

- 5.1.3 GPS / GNSS Trackers

- 5.1.4 Camera-Based and Vision Wearables

- 5.1.5 Footwear and In-Shoe Sensors

- 5.1.6 Head-Mounted and AR Displays

- 5.1.7 Ingestible and Other Emerging Sensors

- 5.2 By Sport

- 5.2.1 Soccer / Football

- 5.2.2 Basketball

- 5.2.3 American Football and Rugby

- 5.2.4 Baseball / Softball

- 5.2.5 Cricket

- 5.2.6 Golf and Tennis

- 5.2.7 Cycling and Triathlon

- 5.2.8 Swimming and Aquatics

- 5.2.9 Extreme and Adventure Sports

- 5.3 By End User

- 5.3.1 Professional Teams and Leagues

- 5.3.2 Collegiate / University Programs

- 5.3.3 Amateur and Club Athletes

- 5.3.4 Recreational Fitness Enthusiasts

- 5.3.5 Sports Academies and Training Centers

- 5.3.6 Medical and Rehab Facilities

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct and Marketplaces)

- 5.4.2 Specialty Sports Stores

- 5.4.3 Mass-Retail and Electronics Chains

- 5.4.4 Team / Enterprise Contracts

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kinexon GmbH

- 6.4.2 Garmin Ltd.

- 6.4.3 Sensoria Inc.

- 6.4.4 Zepp Health Corporation

- 6.4.5 Catapult Group International Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Alphabet Inc. (Google LLC / Fitbit LLC)

- 6.4.8 STATSports Group Ltd.

- 6.4.9 Whoop, Inc.

- 6.4.10 Polar Electro Oy

- 6.4.11 Carre Technologies Inc. (Hexoskin)

- 6.4.12 Zephyr Technology Corporation

- 6.4.13 Firstbeat Technologies Oy

- 6.4.14 Apple Inc.

- 6.4.15 Playermaker Ltd.

- 6.4.16 Motus Global LLC

- 6.4.17 X2 Biosystems, Inc.

- 6.4.18 Nix, Inc.

- 6.4.19 hDrop Technologies, Inc.

- 6.4.20 Adidas AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

穿戴式冷卻設備市場-2026-2032年全球市場預測

穿戴式冷卻設備市場-2026-2032年全球市場預測 穿戴式支付終端市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年

穿戴式支付終端市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年 工業穿戴裝置市場報告:按產品類型、應用、產業和地區分類(2026-2034年)穿戴式空調市場:按產品類型、技術、最終用戶和分銷管道分類-2026-2032年全球預測憂鬱症監測穿戴式裝置市場按產品類型、感測器類型、年齡層、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)穿戴式攝影設備市場:按產品類型、技術、應用、最終用戶和分銷管道分類的全球預測(2026-2032年)

工業穿戴裝置市場報告:按產品類型、應用、產業和地區分類(2026-2034年)穿戴式空調市場:按產品類型、技術、最終用戶和分銷管道分類-2026-2032年全球預測憂鬱症監測穿戴式裝置市場按產品類型、感測器類型、年齡層、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)穿戴式攝影設備市場:按產品類型、技術、應用、最終用戶和分銷管道分類的全球預測(2026-2032年) 2026年全球更年期降溫穿戴式裝置市場報告

2026年全球更年期降溫穿戴式裝置市場報告 項鍊市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年2026年全球穿戴式裝置市場報告

項鍊市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年2026年全球穿戴式裝置市場報告 穿戴式支付設備市場規模、佔有率和成長分析(按設備、技術、應用和地區分類)-2026-2033年產業預測

穿戴式支付設備市場規模、佔有率和成長分析(按設備、技術、應用和地區分類)-2026-2033年產業預測