|

市場調查報告書

商品編碼

2044148

網路應用程式防火牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Web Application Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

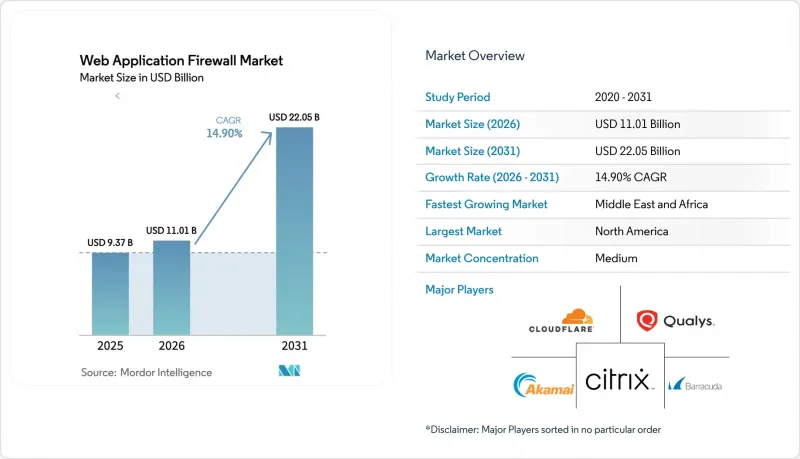

2025 年網路應用程式防火牆(WAF) 市值為 93.7 億美元,預計到 2031 年將達到 220.5 億美元,而 2026 年為 110.1 億美元,2026 年至 2031 年預測期內的複合年成長率為 14.9%。

此次擴張主要受四大趨勢驅動:API 層漏洞利用激增,迫使對 GraphQL、gRPC 和 WebSocket 流量進行檢查;向雲原生微服務的快速轉型;日益嚴格的全球隱私法規將即時監控提升為法律要求;以及邊緣原生防禦技術在邊緣位置應用機器學習分析,從而降低延遲。隨著超大規模企業將原生 WAF 與雲端訂閱捆綁銷售、專業 CDN 供應商實現亞毫秒級檢測的商業化,以及傳統設備供應商透過虛擬版本進行現代化改造,市場競爭日益激烈。創業投資資金正瞄準那些採用擴展型柏克萊資料包過濾器 (eBPF) 進行核心級檢測的早期新創公司。儘管開放原始碼核心規則集的普及削弱了定價權,但對託管 SOC 整合的需求仍然強勁。預算緊張的中小型企業正以前所未有的速度湧入網路應用程式防火牆市場,因為基於雲端的收費系統無需設備資本投資,並將部署時間從數週縮短至數小時。

全球網路應用程式防火牆市場趨勢與洞察

API攻擊激增

目前,API 端點吸引了絕大多數惡意流量,2024 年記錄的 API 特定事件高達 1,500 億起。隨著攻擊者利用模式自省和批量更改,這一數字還在持續成長。從 2023 年第一季到 2024 年第四季度,第 7 層 DDoS 攻擊活動成長了 94%,每月請求量超過 1.1 兆次,這使得只能分析基本 HTTP 語義的傳統引擎不堪重負。為了因應這種情況,企業正在添加基於契約的檢驗功能,以拒絕違反 OpenAPI 定義的請求,這種轉變有效地將邊界防禦擴展到了微服務契約。由於傳統的簽章資料庫無法理解複雜的有效負載結構,整合 GraphQL 解析器和 gRPC 解碼器的供應商正在網路應用程式防火牆市場中佔據越來越大的佔有率。這一趨勢正在推動能夠將 API 流量與機器人管理訊號和行為模式關聯起來以實現自動攔截的平台的普及。

雲端原生和微服務的興起

超過 70% 的 Kubernetes 企業會產生數千個臨時 Pod,每個 Pod 都會產生生命週期短暫的端點,這使得靜態裝置配置無法滿足需求。一種能夠在 150 毫秒內啟動 WAF 執行個體的邊緣架構,既契合無伺服器生命週期,又能適應工作負載彈性,從而確保網路應用程式防火牆市場能夠在不因回環路由而導致效能下降的情況下提供保護。服務網格邊車將偵測直接整合到叢集內流量中,消除了網路繞行,同時繼承了聲明式 YAML 管道中的措施。部署的關鍵在於能夠以程式碼形式管理 WAF,將規則嵌入基礎架構即程式碼 (IaC) 範本中,以便所有建置都能繼承增強的預設設定。無法將偵測功能與硬體分離的供應商正面臨市場佔有率下降的困境,因為容器原生買家更注重部署速度而非機架式吞吐量。

高誤報率會擾亂業務營運。

核心規則集的預設警報等級會導致 10-15% 的誤報率,在黑色星期五期間,這會阻塞購物車並增加支援諮詢量。零售商面臨收入損失和詐欺增加的雙重困境,迫使他們投資於沙盒調優環境和即時規則回滾功能。機器學習疊加層可將負載平衡準確率提高 45%,但需要持續的重新訓練和高品質的標籤,從而增加營運成本。商業供應商現在提供託管調優訂閱服務,承諾誤報率低於 1%,這在網路應用程式防火牆市場中是一個差異化因素。買家在簽訂多年合約之前,越來越要求提供實證數據,以證明在閃購模擬中客戶流失率降低。

細分市場分析

混合架構的興起源自於監管機構的要求,即保護醫療資訊和擁有者資料必須保留在本地,而將公共網站部署在雲端。儘管到2025年,雲端產品在網路應用程式防火牆市場佔據了64.11%的佔有率,但混合架構預計將以15.57%的複合年成長率成長,成為同類產品中成長最快的。財務長們重視混合架構在控制資本支出(CAPEX)方面的能力,同時也能說服那些禁止在海外進行檢查的審計人員。然而,本地設備和雲端主機之間規則語法的差異導致策略繁多,給安全負責人帶來了許多困擾。集中式管理系統將統一的JSON模式推送至F5設備、AWS WAF和Azure應用程式閘道器,正成為減少組態差異的關鍵採購標準。隨著標準化進程的推進,所有強制執行點都將被整合到一個統一的控制面板中,缺乏多重雲端抽象能力的供應商正面臨客戶流失。隨著印度和中國強制推行資料本地化,對包含本地金鑰的本地 POP 部署套件的需求不斷成長,擴大了與混合部署相關的網路應用程式防火牆的市場規模。

同時,採用純雲端模式的公司仍然對供應商鎖定問題十分敏感。使用 Terraform 模組的遷移策略正日益受到青睞,因為它們承諾即使價格上漲也能保持可攜性。市場驅動的收費模式加速了概念驗證(PoC) 的部署,使團隊能夠在不到一小時內運作計量收費的Web 應用防火牆 (WAF)——這種速度在透過採購委員會申請硬體報價時是無法實現的。因此,傳統設備的收入僅在高度監管的細分市場中成長,而訂閱 ARR(年度經常性收入)則隨著每個部署到生產環境的新微服務而成長。

到2025年,解決方案將佔總支出的71.29%,但由於人才市場緊張,專業服務和託管服務的複合年成長率將達到15.97%,成為成長最快的組成部分。買家會根據諸如遏制零日攻擊所需時間和解決誤報平均所需時間等指標來評估服務提供者,這些指標對合約續約決策有顯著影響。託管安全營運中心(SOC)套餐現在將WAF遙測資料與端點和網路感測器整合,以創建統一的攻擊鏈,從而加快速度。缺乏全天候服務的中型企業正湧向提供持續每月更新而無需經過變更諮詢委員會的承包服務,這推動了網路應用程式防火牆市場經常性收入的成長。

供應商正透過利用自身的威脅情報來源和語言模型助手來實現差異化競爭,這些助手能夠自動產生符合規範的 ModSecurity 正規表示式。這些功能吸引了那些先前因擔心供應商資訊不透明而對託管安全服務敬而遠之的客戶。在低階市場,白牌平台使通訊業者能夠轉售自有品牌的Web 應用防火牆 (WAF),從而擴展分銷網路,並促使檢測功能更深入地整合到寬頻套餐中。因此, 網路應用程式防火牆市場正朝著「即服務」模式轉變,而永久授權則傾向於繼續沿用傳統的續約週期。

區域分析

至2025年,北美將佔網路應用程式防火牆)市場收入的38.73%。從CCPA的擴展到強制性的PCI DSS v4.0合規性,持續的監管要求正在塑造一種新的採購文化,這種文化將WAF視為必不可少的附加元件,而不僅僅是可選項。超大規模資料中心業者資料中心驅動的邊緣網路飽和,加上最高密度的安全營運中心(SOC)人才,正在推動WAF的快速部署,並定義了全球對WAF功能性的預期。加拿大各省的隱私法正在推動混合型解決方案的需求,而墨西哥的近岸部署則將新的電子商務流量導向位於美國的檢測節點,從而維持了跨境管理服務的收入。

在歐洲,GDPR、NIS2 和 DORA 等法規對企業實施嚴格監管,要求企業提供即時監控和全天候事件報告。 Schrems II 裁決使跨大西洋資料流變得更加複雜,促使許多企業在歐盟主權雲中部署區域性 WAF叢集,從而擴大了歐洲在網路應用程式防火牆市場的佔有率。德國聯邦資訊安全局 (BSI) 和法國國家資訊安全局 (ANSSI) 等國家機構發布了針對特定行業的框架,這些框架影響供應商的產品藍圖,特別是要求以特定語言格式提供防篡改的審計日誌。英國脫歐意味著英國將維持類似但平行的標準,迫使跨國銀行建立雙重合規體系。

中國《個人資訊保護法》和《機器學習隱私法2.0》的實施,以及印度《數位個人資料保護法》的最終定稿,正推動亞太地區網路安全技術快速普及。這兩項法律均強制要求進行國內檢查,從而鼓勵外國供應商在國內建造資料中心。日本金融廳針對金融科技應用發布的指導意見以及韓國《個人資訊保護法》(PIPA)的實施,也促使電子支付服務提供者維持高支出。印尼和越南的新創公司傾向於選擇能夠兼顧區域合規要求和成本控制的雲端訂閱方案,進一步擴大了亞太地區的網路應用程式防火牆市場。

預計到2031年,中東和非洲將以15.79%的年複合成長率(CAGR)保持最高水平,這主要得益於阿拉伯聯合大公國的《資料保護和資料保護法》(DPDP)以及沙烏地阿拉伯的網路安全法規的推動。隨著「2030願景」大型企劃推進公共服務的數位化,市場對阿拉伯語日誌支援以及與本地安全營運中心(SOC)整合的需求日益成長。以色列的創新生態系統正在催生人工智慧驅動的Web應用防火牆(WAF)新創企業,這些企業正將產品出口到波灣合作理事會(GCC)成員國。南美洲緊隨其後,巴西以《通用資料保護法》(LGPD)主導的現代化進程以及明確強制金融機構實施WAF的第4.893號決議,推動了市場發展。非洲仍處於起步階段,但南非的《個人資料保護法》(POPIA)正在鼓勵銀行和通訊業者進行試點部署,逐步創造對全球網路應用程式防火牆市場的需求。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- API攻擊激增

- 雲端原生和微服務的興起

- 加強全球資料保護條例

- 邊緣/CDN 整合以提升性能

- 邊緣人工智慧增強威脅分析

- 實施“安全即代碼”DevSecOps

- 市場限制因素

- 高誤報率會擾亂業務營運。

- 高級調音技術熟練人員短缺

- QUIC/HTTP-3 加密檢查成本

- 使用開放原始碼WAF進行稀釋

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 替代品的威脅

- 供應商的議價能力

- 買方的議價能力

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的WAF

- 現場/設備

- 混合

- 按組件

- 解決方案

- 專業服務及託管服務

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技和通訊

- 工業與國防

- 零售與電子商務

- 能源與公共產業

- 製造業

- 其他

- 按公司規模

- 中小企業

- 大公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- F5, Inc.

- Akamai Technologies, Inc.

- Cloudflare, Inc.

- Imperva(Thales Digital Identity and Security)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Fortinet, Inc.

- Barracuda Networks, Inc.

- Radware Ltd.

- Fastly, Inc.

- Citrix Systems, Inc.

- StackPath, LLC

- Sophos Limited

- Palo Alto Networks, Inc.

- Trend Micro Inc.

- A10 Networks, Inc.

- Reblaze Technologies Ltd.

- Datadog Inc.

第7章 市場機會與未來展望

The Web application firewall market size was valued at USD 9.37 billion in 2025 and estimated to grow from USD 11.01 billion in 2026 to reach USD 22.05 billion by 2031, at a CAGR of 14.9% during the forecast period 2026-2031.

The expansion pivots on four powerful trends: skyrocketing API-layer abuse that forces inspection of GraphQL, gRPC and WebSocket traffic, rapid shift to cloud-native micro-services, tightening global privacy mandates that elevate real-time monitoring to a legal necessity, and edge-native defenses that lower latency while applying machine-learning analytics at the point of presence. Competitive intensity accelerates as hyperscale's bundle native WAF into cloud subscriptions, specialist CDNs monetize sub-10-millisecond inspection, and legacy appliance vendors modernize through virtual editions. Venture funding targets early-stage start-ups embedding extended Berkeley Packet Filter (eBPF) for kernel-level inspection, while open-source Core Rule Set adoption tempers pricing power but not demand for managed SOC integration. Budget-constrained small and medium enterprises enter the Web application firewall market at record pace because cloud consumption pricing removes appliance capex and reduces deployment from weeks to hours.

Global Web Application Firewall Market Trends and Insights

API-Attack Volume Surge

API endpoints now attract the majority of hostile traffic, with 150 billion API-specific events logged in 2024, a figure that continues to climb as attackers exploit schema introspection and batched mutations. Layer 7 DDoS activity rose 94% between Q1 2023 and Q4 2024, passing 1.1 trillion requests a month, pressuring legacy engines that only parse basic HTTP semantics. Enterprises respond by adding contract-driven validation that rejects requests violating OpenAPI definitions, a shift that effectively extends perimeter defense into micro-service contracts. Vendors embedding GraphQL parsers and gRPC decoders win share in the Web application firewall market as traditional signature databases fail to understand rich payload constructs. The trend drives procurement toward platforms able to correlate API traffic with bot-management signals and behavioural baselines for automated cutoff.

Cloud-Native and Micro-Services Proliferation

Seventy-plus percent of enterprises running Kubernetes generate thousands of ephemeral pods, each spawning short-lived endpoints that overwhelm static appliance configurations. Edge architectures capable of spinning a WAF instance in under 150 milliseconds now align with serverless life cycles, matching workload elasticity and ensuring the Web application firewall market provides protection without hairpin routing penalties. Service-mesh sidecars push inspection directly into intra-cluster traffic, eliminating network detours while inheriting policy from declarative YAML pipelines. Central to adoption is the ability to manage WAF as code, embedding rules inside Infrastructure-as-Code templates so every build inherits hardened defaults. Vendors unable to decouple inspection from hardware see share erosion as container-native buyers prize speed of deployment over rack-mounted throughput.

High False-Positive Business Disruption

Default paranoia levels in Core Rule Set trigger 10-15% false positives, blocking carts on Black Friday and inflating support call volume. Retailers confront a lose-lose scenario of lost revenue versus added fraud, prompting them to invest in sandbox tuning environments and real-time rule rollback features. Machine-learning overlays improve balanced accuracy by 45% but demand continuous retraining and high-quality labels, raising operational cost. Commercial vendors now package managed-tuning subscriptions that promise sub-1% false-positive rates, a differentiator within the Web application firewall market. Buyers increasingly request proof points showing decreased customer drop-offs during flash-sale simulations before signing multiyear contracts.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Data-Protection Mandates

- Edge/CDN Integration for Performance

- Talent Gap for Advanced Tuning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures captured growing mindshare once regulators insisted that protected health information and cardholder data remain on premises while public websites stayed in cloud. The Web application firewall market share for cloud-based offerings stood at 64.11% in 2025, but hybrid is projected to advance at a 15.57% CAGR, the category's fastest pace. CFOs like hybrid's ability to cap capex while appeasing auditors who prohibit foreign inspection points. Policy sprawl, however, bedevils security staff because on-premises appliances and cloud consoles expose dissimilar rule syntax. Central managers that push a unified JSON schema to F5 appliances, AWS WAF and Azure Application Gateway reduce drift, making them a key purchase criterion. Vendors without multi-cloud abstraction see churn as buyers standardize on single dashboards that track every enforcement point. As India and China enforce data-localization, demand rises for local pop deployment kits bundled with on-premises keys, expanding the Web application firewall market size associated with hybrid rollouts.

Simultaneously, cloud-only adopters remain sensitive to vendor lock-in. Exit strategies rooted in Terraform modules gain favour because they promise portability should pricing spike. Marketplace billing accelerates proof-of-concepts, letting teams activate pay-as-you-go WAF in under an hour, a speed impossible with procurement committees requesting hardware quotes. Consequently, legacy appliance revenue grows only in regulated niches, whereas subscription ARR scales with each new micro-service pushed into production.

Solutions dominated spending at 71.29% in 2025, but tight labour markets push professional and managed services toward a 15.97% CAGR, the quickest trajectory within components. Buyers benchmark providers on time-to-contain zero-day injections and mean-time-to-resolve false positives, metrics that strongly influence renewal decisions. Managed SOC bundles now stitch WAF telemetry to endpoint and network sensors, building a unified kill chain that accelerates response. Because middle-market companies lack 24 7 coverage, they flock to turnkey offerings that issue rolling monthly updates without change-advisory boards, boosting recurring revenue across the Web application firewall market size.

Providers differentiate using proprietary threat-intelligence feeds and language-model assistants that auto-generate ModSecurity regex in plain English. Those capabilities win accounts that traditionally shunned managed security for fear of vendor opacity. Down-market, white-label platforms allow telecom carriers to resell branded WAF, widening distribution and embedding inspection deeper into broadband bundles. The Web application firewall market therefore tilts toward as-a-service consumption, relegating perpetual licenses to legacy renewal cycles.

The Web Application Firewall Market Report is Segmented by Deployment Mode (Cloud-Based WAF, On-Premises/Appliance, and Hybrid), Component (Solutions, and Professional and Managed Services), End-User Industry (BFSI, Healthcare, IT and Telecom, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America supplied 38.73% of Web application firewall market revenue in 2025. Continuous mandates from CCPA expansions to mandatory PCI DSS v4.0 compliance create a buyer culture that treats WAF as essential infrastructure rather than optional add-on. Edge-network saturation by hyperscalers, coupled with the highest density of SOC talent, fosters rapid feature rollouts that set functional expectations worldwide. Canada's provincial privacy acts drive hybrid demand, while Mexican near-shore expansions funnel new e-commerce traffic through U.S.-based inspection nodes, sustaining cross-border managed-service revenue.

Europe maintains strict oversight through GDPR, NIS2 and DORA, pushing enterprises to demonstrate real-time monitoring and 24-hour incident reporting. Schrems II rulings complicate trans-Atlantic data flows, so many firms deploy regional WAF clusters inside EU sovereign clouds, enlarging the European slice of the Web application firewall market. National agencies like Germany's BSI and France's ANSSI issue sector frameworks that influence vendor product roadmaps, especially the requirement for tamper-evident audit logs delivered in language-specific formats. Brexit leaves the United Kingdom maintaining parallel yet similar standards, forcing multinational banks to map dual compliance regimes.

Asia-Pacific shows the steepest adoption curve as China enforces PIPL and MLPS 2.0 and India finalizes its Digital Personal Data Protection Act. Both regimes require in-country inspection, stimulating domestic data-center buildouts by foreign vendors. Japan's FSA guidance for fintech apps and South Korea's PIPA sustain high spend among electronic payments providers. Start-ups in Indonesia and Vietnam prefer cloud subscriptions that remix regional compliance with cost control, further enlarging the Web application firewall market size across APAC.

The Middle East and Africa projects the highest CAGR at 15.79% through 2031, spurred by UAE DPDP Act mandates and Saudi Arabia's cybersecurity controls. Vision 2030 megaprojects digitize public services, requiring Arabic-language log support and local SOC integration. Israel's innovation ecosystem spawns AI-driven WAF start-ups that export to Gulf Cooperation Council neighbours. South America follows with LGPD-driven modernization in Brazil and resolution 4.893 that explicitly requires WAF for financial institutions. Africa remains early-stage, though South Africa's POPIA nudges banking and telecom operators toward pilot deployments, adding incremental volume to the global Web application firewall market.

- F5, Inc.

- Akamai Technologies, Inc.

- Cloudflare, Inc.

- Imperva (Thales Digital Identity and Security)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Fortinet, Inc.

- Barracuda Networks, Inc.

- Radware Ltd.

- Fastly, Inc.

- Citrix Systems, Inc.

- StackPath, LLC

- Sophos Limited

- Palo Alto Networks, Inc.

- Trend Micro Inc.

- A10 Networks, Inc.

- Reblaze Technologies Ltd.

- Datadog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 API-Attack Volume Surge

- 4.2.2 Cloud-Native and Micro-Services Proliferation

- 4.2.3 Stricter Global Data-Protection Mandates

- 4.2.4 Edge/CDN Integration for Performance

- 4.2.5 AI-Enhanced Threat Analytics at the Edge

- 4.2.6 "Security-as-Code" DevSecOps Adoption

- 4.3 Market Restraints

- 4.3.1 High False-Positive Business Disruption

- 4.3.2 Talent Gap for Advanced Tuning

- 4.3.3 QUIC/HTTP-3 Encryption Inspection Cost

- 4.3.4 Open-Source WAF Dilution

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based WAF

- 5.1.2 On-Premises / Appliance

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Professional and Managed Services

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Retail and E-Commerce

- 5.3.6 Energy and Utilities

- 5.3.7 Manufacturing

- 5.3.8 Other End-User Industry

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 F5, Inc.

- 6.4.2 Akamai Technologies, Inc.

- 6.4.3 Cloudflare, Inc.

- 6.4.4 Imperva (Thales Digital Identity and Security)

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC

- 6.4.8 Fortinet, Inc.

- 6.4.9 Barracuda Networks, Inc.

- 6.4.10 Radware Ltd.

- 6.4.11 Fastly, Inc.

- 6.4.12 Citrix Systems, Inc.

- 6.4.13 StackPath, LLC

- 6.4.14 Sophos Limited

- 6.4.15 Palo Alto Networks, Inc.

- 6.4.16 Trend Micro Inc.

- 6.4.17 A10 Networks, Inc.

- 6.4.18 Reblaze Technologies Ltd.

- 6.4.19 Datadog Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

網路應用程式防火牆市場:按部署模式和區域分類

網路應用程式防火牆市場:按部署模式和區域分類 全球網路應用程式防火牆市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球網路應用程式防火牆市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球網路應用防火牆市場報告

2026年全球網路應用防火牆市場報告 網路應用程式防火牆市場規模、佔有率、趨勢和預測:按部署類型、組織規模、服務、最終用戶產業和地區分類,2026-2034年Web應用防火牆市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034)

網路應用程式防火牆市場規模、佔有率、趨勢和預測:按部署類型、組織規模、服務、最終用戶產業和地區分類,2026-2034年Web應用防火牆市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034) 網路應用程式防火牆市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模、垂直產業、地區和競爭格局分類,2021-2031年)日本Web應用防火牆市場報告(按服務、部署方式、組織規模、最終用戶產業和地區分類,2026-2034年)

網路應用程式防火牆市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模、垂直產業、地區和競爭格局分類,2021-2031年)日本Web應用防火牆市場報告(按服務、部署方式、組織規模、最終用戶產業和地區分類,2026-2034年) 網路應用程式防火牆市場規模、佔有率和成長分析(按組件、部署方式、組織規模、安全模型、最終用戶和地區分類)- 產業預測(2026-2033年)

網路應用程式防火牆市場規模、佔有率和成長分析(按組件、部署方式、組織規模、安全模型、最終用戶和地區分類)- 產業預測(2026-2033年) 網路應用程式防火牆(WAF)的全球市場:各零件,保全類別,不同企業規模,各終端用戶產業,各地區,機會,預測,2018年~2032年

網路應用程式防火牆(WAF)的全球市場:各零件,保全類別,不同企業規模,各終端用戶產業,各地區,機會,預測,2018年~2032年