|

市場調查報告書

商品編碼

2044147

牛皮紙袋:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Sack Kraft Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

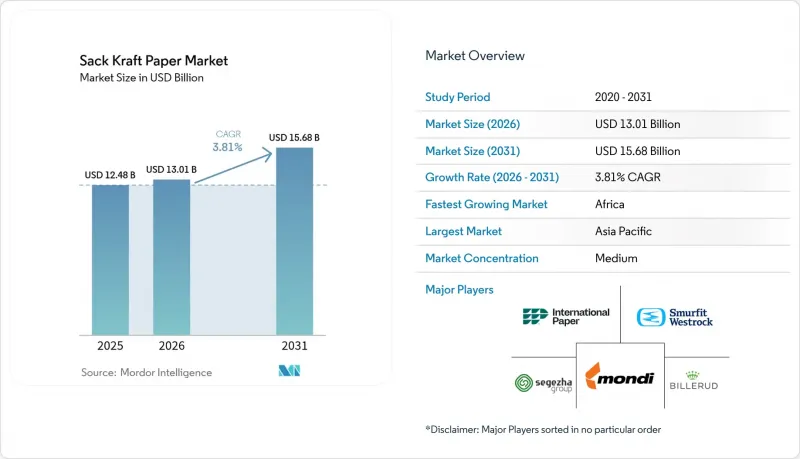

2025年牛皮紙袋市值為124.8億美元,預計到2031年將達到156.8億美元,而2026年為130.1億美元,2026年至2031年的年複合成長率(CAGR)為3.81%。

在這強勁的成長動能背後,蘊藏著一場結構性變革。塑膠禁令、碳邊境調節機制以及數位化供應鏈正在加速水泥、食品配料和礦物加工等行業從編織聚丙烯噸袋轉向可回收多層紙袋的轉變。一體化製造商正在升級其生產設施,引入阻隔塗層和RFID技術生產線,以確保獲得高價值合約;而加工商則在加速採用成型-填充-封口(FFS)設備,以提高製袋速度並降低三分之一的人事費用。儘管原生紙漿和廢棄舊瓦楞紙板箱等原料價格的波動持續對利潤率構成壓力,但垂直整合和長期纖維合約正在緩解價格波動的影響。出於減少運輸過程中排放氣體的需求,輕質單層可拉伸紙袋正成為25-50公斤水泥和化肥包裝的主要包裝形式。相容自動化且可作為生活垃圾回收的設計正在支撐未來的需求,這使得牛皮紙袋市場能夠從全球循環經濟計劃中策略性地獲益。

全球牛皮紙袋市場趨勢及洞察。

塑膠禁令正在加速向紙本文件的轉變。

一次性塑膠禁令正在縮短聚丙烯織物在散裝包裝中的更換週期。針對一次性塑膠的監管措施正在加速散裝包裝應用中聚丙烯織物袋的更換過程。歐盟的《包裝和包裝廢棄物條例》將於2024年最終確定,該條例規定到2030年,65%的包裝材料必須可回收利用,並全面禁止Oxo可分解塑膠。這迫使水泥和化肥經銷商轉向使用多層牛皮紙袋,這些紙袋可納入市政紙張回收系統。在英國,生產者延伸責任制(EPR)計畫將從2025年起對不可回收包裝附加稅,這將使聚丙烯軟性集裝袋(FIBC)的接收成本增加18-22%,從而促使採購轉向可避免此項額外費用的紙質替代品。這一因素對牛皮紙袋市場的影響最為積極,因為合規是強制性的,需要即時採取行動。

水泥產業的脫碳正在促進可回收包裝袋的使用。

全球水泥製造商正將範圍 3 包裝相關排放納入其淨零排放藍圖。一項 2025 年生命週期評估表明,考慮到使用後的回收利用,牛皮紙袋的二氧化碳排放量比同類聚丙烯袋低 60%。值得關注的項目包括 Mondi 和 Cemex 聯合推出的“SolmixBag”,這是一種水溶性單層牛皮紙袋,已在西班牙上市;以及 UltraTech Cement 承諾到 2027 年將其在印度的零售產品組合中 30% 的包裝材料替換為再生牛皮紙。一項歐洲循環建築試點計畫正在測試可重複使用牛皮紙袋的押金返還機制,獎勵回收空袋的承包商。由於水泥在 2025 年的需求量佔比超過五分之二,該產業的脫碳選擇將在中期內顯著重塑牛皮紙袋市場格局。

PP編織軟性貨櫃在散裝包裝中的廣泛應用。

具有導電和防靜電性能的軟性中型散貨箱(FIBC)能夠滿足化學品和易燃粉末的安全性和可重複使用性需求,而牛皮紙袋則無法滿足這些需求。 C型FIBC的成本為每個8至12美元,而同等規格的閉合迴路包裝材料,對牛皮紙袋市場造成了0.6%的負面影響。

細分市場分析

成型-填充-封口 (FFS) 包裝袋在牛皮紙袋市場佔據重要佔有率,年複合成長率 (CAGR) 達 4.78%。這是因為自動化生產線每小時可填充多達 1800 個包裝袋,速度是閥式包裝系統的兩倍。水泥和化學製造商正在採用 FFS 技術,以減少 30-40% 的縫紉工作量並提高包裝精度,同時,摩擦係數可控的 FFS 相容紙張能夠保持密封強度。預計到 2025 年,閥式包裝袋將佔據 41.32% 的市場佔有率,在以粉塵控制和傳統氣動填充為主導的領域,閥式包裝袋仍然至關重要。開口式和捏底包裝袋則滿足了食品和種子等需要金屬檢測和垂直零售展示的細分市場需求。在亞太地區,薪資上漲縮小了自動化與傳統包裝袋之間的成本差距,從而推動了對 FFS 技術的投資。同時,在北美,與倉庫管理軟體整合的嵌入式 RFID 的 FFS 包裝袋正發揮主導作用。總體而言,高速自動化包裝工廠的持續發展支撐了牛皮紙袋市場對各種包裝類型的持續需求。

第二代FFS包裝設計現已整合線上RFID標籤插入、可變資料列印和堆疊機器人。加工商正在銷售承包線,承諾庫存準確率超過99%,此價值提案帶來的效益遠超初始投資。同時,歐洲造紙商正在調整紙張成型工藝,以適應再生牛皮紙基材所需的超音波密封。雖然閥口袋在粉塵較多的水泥廠環境中佔據主導地位,但由於FFS系統在填充過程中具有衛生優勢,因此在化肥、寵物食品和顏料製造廠也越來越受歡迎。因此,競爭的重點在於材料規格和機器相容性,包裝成型成為牛皮紙袋市場成長要素。

到2025年,塗佈牛皮紙和阻隔牛皮紙將佔牛皮紙袋市場37.21%的佔有率,複合年成長率(CAGR)最高,達到4.69%。這反映了客戶從塑膠背襯袋轉向具有防潮防氧性能的完全可回收紙張。生物基塗層已成功將水蒸氣透過率降低至10 g/m²/24 h以下,使其能夠應用於咖啡、麵粉和糖等散裝產品,且不影響其可回收性。標準牛皮紙由於其優異的抗張強度和印刷性能,仍然是水泥和礦產品的主要包裝材料,儘管其成長速度相對較慢。半拉伸和拉伸等級的牛皮紙用於磨料和角狀肥料,其斷裂伸長率達到6-8%,以防止在搬運過程中爆裂。奈米纖維預塗層和在線分散阻隔層使更薄的產品能夠通過50公斤的跌落測試,有助於實現碳評估協議規定的減重目標。

投資一條一步式阻隔塗層生產線,與離線複合製程相比,可降低高達18%的加工成本,使高性能產品即使是中型用戶也能負擔得起。歐洲咖啡烘焙商和亞洲香辛料貿易商擴大指定使用礦物基氧氣阻隔材料,以避免使用含PFAS化學物質的產品。諸如縐紋紙和濕強牛皮紙等特殊等級的牛皮紙滿足緩衝和戶外儲存的要求,豐富了產品線。如此廣泛的產品系列確保了每個性能等級都擁有穩定的基本客群,從而增強了牛皮紙袋市場等級的深度。

區域分析

預計到2025年,亞太地區將佔全球銷售額的32.54%,主要得益於中國水泥消費量的成長和印度對農業包裝的需求。然而,基礎設施投資放緩和塑膠禁令執行不力抑制了短期成長。人事費用上升促使加工商實現FFS(灌裝封裝包裝)自動化,同時對高性能、可拉伸紙張的需求也不斷成長。越南和印尼產能的提升反映了造紙企業為滿足東南亞日益成長的需求並規避中國進口限制而採取的策略。然而,外匯波動和對進口紙漿的依賴意味著成本結構仍然脆弱。

非洲是成長最快的地區,複合年成長率達4.77%,主要得益於奈及利亞包裝市場的強勁成長。預計奈及利亞包裝市場規模將從2024年的20億美元成長到2032年的35億美元。奈及利亞和南非的塑膠禁令,加上歐盟20%的年成長率,催生了對水泥袋和郵寄袋的需求。然而,供應仍受到限制,因為該地區只有不到40%的造紙廠使用可再生能源,這限制了其獲得FSC認證和進入歐盟市場。非洲大陸自由貿易區(AfCFTA)促進了區域內運輸,並推動了本地加工投資和區域專業化發展。

歐洲和北美是成熟市場,需求穩定,這主要得益於基礎設施維修和永續性法規的推動。將於2026年生效的碳邊境調節關稅將鼓勵國內生產低排放紙張,並對來自燃煤發電廠的進口紙張進行懲罰。南美洲的前景與農產品出口密切相關。巴西不斷擴大的紙漿產量增加了該地區的纖維供應,而隨著各國政府逐步淘汰塑膠製品,安地斯山脈地區的建築工程也擴大使用紙袋。這些區域間的細微差異共同構成了機會與風險並存的複雜格局,進而推動了牛皮紙袋市場的全球擴張。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值/價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 塑膠禁令正在加速向紙質產品的轉變。

- 水泥產業的脫碳正在促進可回收包裝袋的使用。

- 在電子商務中採用可回收、耐用的郵寄袋來裝生活垃圾。

- 散裝食品原料包裝袋改用經認證的紙袋。

- 具備RFID功能的紙袋簡化了倉庫自動化流程。

- 碳邊境調節機制將提振歐盟對低排放紙袋的需求。

- 市場限制因素

- PP編織軟性貨櫃在散裝包裝中的廣泛應用。

- 原生纖維和再生紙(OCC)價格波動

- 可溶性纖維基大宗包裝薄膜的興起正在縮小小眾應用領域。

- 區域內缺乏可再生能源限制了造紙廠獲得綠色認證的能力。

- 監理情勢

- 技術展望

第5章 市場規模及成長預測,金額

- 按包裝類型

- 帶閥門的袋子

- 開口袋

- 捏底袋

- 泡棉填充密封(FFS)袋

- 其他

- 按年級

- 工藝

- 部分可調整大小

- 可放大

- 塗佈紙/阻隔紙

- 其他

- 按層數

- 1層

- 2層

- 3層

- 4 層或更多層

- 按最終用戶行業分類

- 建築材料及水泥

- 食品和飲料原料

- 化學品和肥料

- 農業和動物飼料

- 礦物和顏料

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mondi plc

- Smurfit Kappa Group plc

- WestRock Company

- Billerud AB

- International Paper Company

- Segezha Group PJSC

- Stora Enso Oyj

- Gascogne Groupe SA

- Nordic Paper AS

- Natron-Hayat doo

- Horizon Pulp and Paper Ltd.

- Canfor Corporation

- Klabin SA

- SCG Packaging Public Company Limited

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Ltd.

- Sappi Limited

- Heinzel Holding GmbH

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- Daio Paper Corporation

- Ahlstrom Oyj

第7章 市場機會與未來展望

The sack kraft paper market size was valued at USD 12.48 billion in 2025 and estimated to grow from USD 13.01 billion in 2026 to reach USD 15.68 billion by 2031, at a CAGR of 3.81% during 2026-2031.

The steady headline figure hides a structural transformation as plastic-ban legislation, carbon border adjustment mechanisms and digitized supply chains accelerate substitution of woven polypropylene bulk bags with recyclable multiwall paper sacks across cement, food ingredients and minerals handling. Integrated producers are upgrading mills with barrier coating and RFID-ready converting lines to secure premium contracts, while converters race to install form-fill-seal (FFS) equipment that doubles bagging speeds and cuts labor outlays by one-third. Raw-material volatility in virgin pulp and old corrugated containers continues to squeeze margins, but vertical integration and long-term fiber contracts are mitigating price swings. Lightweight single-ply extensible papers, supported by the need to curb freight emissions, are becoming the format of choice for 25-50 kilogram cement and fertilizer applications. Automation-ready, curbside-recyclable designs underpin future demand, positioning the sack kraft paper market as a strategic beneficiary of circular-economy policies worldwide.

Global Sack Kraft Paper Market Trends and Insights

Plastic-Ban Legislation Accelerating Paper Substitution

Single-use plastic prohibitions are compressing the replacement cycle for woven polypropylene across bulk packaging. Legislative momentum against single-use plastics is compressing the substitution timeline for woven polypropylene sacks across bulk packaging applications. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024, mandates that 65% of packaging materials be recyclable by 2030 and bans oxo-degradable plastics outright, forcing cement and fertilizer distributors to transition to multiwall kraft sacks that qualify for municipal paper recycling streams. In the United Kingdom, the Extended Producer Responsibility scheme imposed a GBP 200 per tonne levy on non-recyclable packaging in 2025, raising the landed cost of polypropylene FIBCs by 18-22% and tilting procurement toward paper alternatives that avoid the surcharge. This driver exerts the largest positive swing on the sack kraft paper market because compliance is mandatory and immediate.

Cement-Sector Decarbonization Favoring Recyclable Sacks

Global cement producers are embedding Scope 3 packaging emissions into net-zero roadmaps. A 2025 life-cycle assessment verified that kraft sacks deliver 60% lower CO2 than polypropylene equivalents when end-of-life recycling is counted. Flagship projects include Mondi and Cemex's SolmixBag, a dissolvable single-ply kraft sack already commercial in Spain, and UltraTech Cement's pledge to shift 30% of its Indian retail portfolio to recycled kraft by 2027. European circular-construction pilots are trialing deposit-return schemes for reusable kraft sacks, rewarding contractors for recovering empty bags. Because cement represented more than two-fifths of 2025 demand, decarbonization choices by this sector meaningfully recalibrate the sack kraft paper market trajectory over the medium term.

Penetration of Woven-PP FIBCs in Bulk Packaging

Conductive and antistatic flexible intermediate bulk containers fill safety and reusability needs that kraft cannot match in chemicals and flammable powders. Type C FIBCs cost USD 8-12 each against USD 15-20 for equivalent multiwall kraft with antistatic liners, a gap widened by their ability to complete 5-10 shipping cycles. Closed-loop supply chains in plastics resins, mineral concentrates and automotive parts therefore continue to specify polypropylene, placing a -0.6% drag on the sack kraft paper market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Adoption of Curbside-Recyclable Heavy-Duty Mailers

- Food-Grade Bulk Ingredients Shifting to Certified Paper Sacks

- Volatile Virgin-Fiber and OCC Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Form-fill-seal sacks accounted for a meaningful proportion of the sack kraft paper market size and post a 4.78% CAGR because automated lines fill up to 1,800 units per hour, twice the speed of valve systems. Cement and chemical producers adopt FFS to cut stitching labor by 30-40% and boost bagging accuracy, while FFS-ready papers with controlled coefficient of friction maintain seal integrity. Valve sacks, holding 41.32% share in 2025, remain indispensable where dust control and legacy pneumatic filling dominate. Open-mouth and pinch-bottom formats fill niches in food and seed applications that require metal detection or upright retail display. Asia-Pacific drives FFS investments as rising wages narrow the cost gap versus automation, and North America leads on RFID-embedded FFS sacks that integrate with warehouse management software. Overall, the continuous shift toward high-speed automated packaging plants underpins sustained demand across all packaging types within the sack kraft paper market.

Second-generation FFS designs now integrate inline RFID tag insertion, variable data printing and palletizing robotics. Converters market turnkey lines that promise inventory accuracy above 99%, a value proposition that outweighs the upfront capital. Meanwhile, European mills calibrate paper formation to accommodate ultrasonic sealing demanded by recycled kraft substrates. Although valve sacks dominate in dusty cement environments, FFS systems are infiltrating fertilizer, pet food and pigment facilities due to superior filling hygiene. The competitive battle therefore centers on material specifications and machine compatibility, cementing packaging type as a decisive growth vector for the sack kraft paper market.

Coated and barrier kraft held 37.21% of sack kraft paper market share in 2025 and post the fastest 4.69% CAGR, reflecting customer migration from plastic-lined sacks to fully recyclable papers with moisture and oxygen barriers. Bio-based coatings achieve water-vapor transmission below 10 g/m2/24 h, opening applications in bulk coffee, flour and sugar without compromising recyclability. Standard kraft remains the workhorse for cement and minerals because tensile strength and printability trump barrier performance, though its growth is more subdued. Semi-extensible and extensible grades serve abrasives and jagged fertilizers, with 6-8% elongation at break preventing rupture during handling. Nanofiber pre-coatings and inline dispersion barriers now enable thinner gauges to pass 50-kilogram drop tests, supporting lightweighting targets mandated by carbon assessment protocols.

Investment in single-step barrier coating lines lowers conversion costs by up to 18% versus offline lamination, bringing premium performance within reach of mid-volume users. European coffee roasters and Asian spice traders increasingly specify mineral-based oxygen barriers that avoid PFAS chemistry. Specialty sub-grades such as creped or wet-strength kraft fill cushioning and outdoor storage requirements, rounding out a diverse product spectrum. This breadth ensures that each performance tier finds a stable customer base, reinforcing grade-level depth in the sack kraft paper market.

The Sack Kraft Paper Market Report is Segmented by Packaging Type (Valve Sacks, Open Mouth Sacks, Pinch-Bottom Sacks, Form-Fill-Seal Sacks, and More), Grade (Kraft, Semi-Extensible, Extensible, Coated/Barrier Kraft, and More), Ply/Layer Count (1-Ply, 2-Ply, and More), End-User Industry (Building Materials and Cement, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 32.54% of 2025 global revenue behind China's cement consumption and India's agricultural packaging needs. Yet infrastructure moderation and patchy plastic-ban enforcement temper near-term growth. Rising labor costs push converters toward FFS automation, boosting demand for high-performance extensible grades. Capacity additions in Vietnam and Indonesia reflect mill owners' strategy to serve Southeast Asian growth corridors and hedge against Chinese import restrictions. Currency volatility and imported pulp dependence, however, keep cost structures exposed.

Africa is the fastest-growing region at a 4.77% CAGR, propelled by Nigeria's packaging market, which rises from USD 2 billion in 2024 to USD 3.5 billion by 2032. Plastic bans in Nigeria and South Africa, paired with 20% annual e-commerce growth, create demand for cement sacks and mailers. Supply constraints persist because fewer than 40% of regional mills run on renewable energy, limiting FSC certification and EU market access. The African Continental Free Trade Area eases intra-regional shipments, encouraging localized converting investments and regional specialization.

Europe and North America account for mature but stable demand shaped by infrastructure refurbishment and sustainability regulations. Carbon border adjustment tariffs effective in 2026 incentivize domestic low-emission paper and penalize imports from coal-fired mills. South America's outlook is tied to agricultural exports; Brazilian pulp expansions add regional fiber availability, while Andean construction projects use more paper sacks as governments phase out plastic. Collectively, these geographic nuances create a mosaic of opportunities and risks, sustaining global expansion for the sack kraft paper market.

- Mondi plc

- Smurfit Kappa Group plc

- WestRock Company

- Billerud AB

- International Paper Company

- Segezha Group PJSC

- Stora Enso Oyj

- Gascogne Groupe SA

- Nordic Paper AS

- Natron-Hayat d.o.o.

- Horizon Pulp and Paper Ltd.

- Canfor Corporation

- Klabin S.A.

- SCG Packaging Public Company Limited

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Ltd.

- Sappi Limited

- Heinzel Holding GmbH

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- Daio Paper Corporation

- Ahlstrom Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value / Supply-Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Market Drivers

- 4.5.1 Plastic-ban Legislation Accelerating Paper Substitution

- 4.5.2 Cement-sector Decarbonization Favoring Recyclable Sacks

- 4.5.3 E-commerce Adoption of Curbside-recyclable Heavy-duty Mailers

- 4.5.4 Food-grade Bulk Ingredients Shifting to Certified Paper Sacks

- 4.5.5 Radio-frequency-identifiable Sack Papers Simplifying Warehouse Automation

- 4.5.6 Carbon Border Adjustment Mechanisms Boosting EU Demand for Low-Emission Sack Papers

- 4.6 Market Restraints

- 4.6.1 Penetration of Woven-PP FIBCs in Bulk Packaging

- 4.6.2 Volatile Virgin-fiber and OCC Prices

- 4.6.3 Emergence of Soluble Fiber-based Bulk Packaging Films Eroding Niche Applications

- 4.6.4 Regional Shortfall of Renewable Energy Access Limiting Mill Green Certifications

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

5 MARKET SIZE AND GROWTH FORECASTS, VALUE

- 5.1 By Packaging Type

- 5.1.1 Valve Sacks

- 5.1.2 Open Mouth Sacks

- 5.1.3 Pinch-Bottom Sacks

- 5.1.4 Form-Fill-Seal Sacks

- 5.1.5 Rest of Packaging Type

- 5.2 By Grade

- 5.2.1 Kraft

- 5.2.2 Semi-Extensible

- 5.2.3 Extensible

- 5.2.4 Coated / Barrier Kraft

- 5.2.5 Rest of Grade

- 5.3 By Ply / Layer Count

- 5.3.1 1-Ply

- 5.3.2 2-Ply

- 5.3.3 3-Ply

- 5.3.4 More than 3-Ply

- 5.4 By End-User Industry

- 5.4.1 Building Materials and Cement

- 5.4.2 Food and Beverage Ingredients

- 5.4.3 Chemicals and Fertilizers

- 5.4.4 Agriculture and Animal Feed

- 5.4.5 Minerals and Pigments

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mondi plc

- 6.4.2 Smurfit Kappa Group plc

- 6.4.3 WestRock Company

- 6.4.4 Billerud AB

- 6.4.5 International Paper Company

- 6.4.6 Segezha Group PJSC

- 6.4.7 Stora Enso Oyj

- 6.4.8 Gascogne Groupe SA

- 6.4.9 Nordic Paper AS

- 6.4.10 Natron-Hayat d.o.o.

- 6.4.11 Horizon Pulp and Paper Ltd.

- 6.4.12 Canfor Corporation

- 6.4.13 Klabin S.A.

- 6.4.14 SCG Packaging Public Company Limited

- 6.4.15 Oji Holdings Corporation

- 6.4.16 Nine Dragons Paper Holdings Ltd.

- 6.4.17 Sappi Limited

- 6.4.18 Heinzel Holding GmbH

- 6.4.19 Georgia-Pacific LLC

- 6.4.20 Rengo Co., Ltd.

- 6.4.21 Daio Paper Corporation

- 6.4.22 Ahlstrom Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

牛皮紙袋市場:按等級、包裝類型、最終用途行業和地區分類。

牛皮紙袋市場:按等級、包裝類型、最終用途行業和地區分類。 牛皮紙袋市場規模、佔有率及成長分析(依等級、紙張重量、應用、終端用戶產業及地區分類)-2026-2033年產業預測

牛皮紙袋市場規模、佔有率及成長分析(依等級、紙張重量、應用、終端用戶產業及地區分類)-2026-2033年產業預測 全球紙袋牛皮紙市場規模:依等級、包裝類型、最終用途行業、區域範圍和預測

全球紙袋牛皮紙市場規模:依等級、包裝類型、最終用途行業、區域範圍和預測