|

市場調查報告書

商品編碼

2044146

環境智慧:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Ambient Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

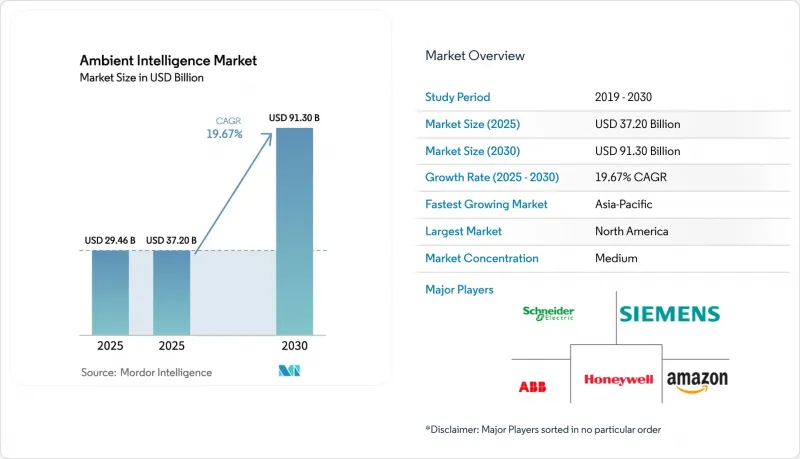

預計到 2031 年,環境智慧市場規模將從 2026 年的 372 億美元成長至 913 億美元,2026 年至 2031 年的複合年成長率為 19.67%。

功耗低於10瓦的邊緣推理晶片、主要經濟體對自主人工智慧的監管以及強制性的隱私納入設計原則,正在加速人工智慧的商業化應用。供應商正積極回應,推出嵌入式神經處理單元,服務供應商也開始提供超越初始部署期限的預測性維護合約。中國、印度和海灣國家的智慧城市建設計畫降低了私人投資者的部署風險,而美國遠端患者監護的報銷政策則擴大了醫療保健領域的需求。隨著消費性電子巨頭將智慧家庭生態系統部署到商業建築中,競爭壓力日益加劇,迫使成熟的工業自動化公司在其控制器中整合增值分析功能。

全球環境智慧市場趨勢與洞察

人工智慧和物聯網設備的普及

低功耗邊緣處理器消除了與雲端往返通訊相關的延遲,這在汽車、工業和醫療領域至關重要。商用智慧型手機現在整合了超寬頻無線電技術,實現了厘米級定位,表明消費級硬體已準備好處理企業級工作負載。行動作業系統中聯邦學習的引入,證明了無需向外部傳輸原始資料即可改進模型的能力,為辦公室中受隱私保護的佔用檢測樹立了先例。網狀網路和低功耗推理技術使電池壽命可達數年,使得感測器網路能夠覆蓋大面積樓層,且只需極少的維修。確定性網路標準也隨著這些技術的進步而融合,從而實現了安全聯鎖裝置,該裝置必須在環境閾值超出時在毫秒內做出反應。

政府的智慧城市計劃

中國已撥款1.2兆元(約1,680億美元)用於900多個智慧城市示範項目,這些項目融合了交通、空氣品質和安全分析能力。同時,印度的「智慧城市計畫」已向100個大都會區撥款4,800億印度盧比(約約57.6億美元)。除了沙烏地阿拉伯耗資5000億美元的NEOM計畫外,馬來西亞和東南亞小規模經濟體的津貼也反映了公共部門對數位化城市基礎設施的承諾。這些項目正在建立通用數據平台,展示可衡量的節能效果,並吸引配套的私人投資。符合在地採購要求和資料主權條款的供應商正在獲得優先進入許可權,並加速銷售管道拓展。由此產生的案例研究顯示了互通性框架的有效性,這些框架隨後被小規模的市政當局採用,擴大了環境智慧市場。

資料安全和隱私問題

2018年至2025年間,歐洲監管機構已對違反GDPR的企業處以45億歐元(約51億美元)的罰款。由於使用者授權流程不明確和資料保存時間過長,環境系統面臨更嚴厲的處罰。歐盟2024年人工智慧法案將公共場所的生物識別列為高風險技術,強制要求進行冗長的合規性評估,延緩了其商業化進程。如果感測器無意中捕獲了受保護的健康訊息,美國醫療保健機構將根據《健康保險流通與責任法案》(HIPAA)承擔法律責任。聯邦學習會將原始數據保留在設備上,但監管機構尚未明確聚合模型的更新是否構成個人數據,這造成了法律上的模糊性。隨著消費者意識的提高,買家要求提供詳細的選擇嵌入系統式儀表板,這導致開發成本增加和銷售週期延長。

細分市場分析

到2025年,硬體收入將佔總收入的59.61%,這主要得益於對感測器、閘道器和邊緣伺服器的資本投資,這些設備構成了所有環境的基礎。隨著終端用戶轉向基於訂閱的分析、遠端診斷和持續的網路安全補丁,以保護關鍵任務運營,服務領域的環境智慧市場預計將以20.17%的複合年成長率成長。微機電感測器和藍牙無線模組成本的降低,以及推理加速器量產的增加,正在對硬體利潤率構成壓力,促使製造商提供將軟體和支援與其設備整合的解決方案。

業務收益也受益於演算法客製化的複雜性,這種複雜性體現在能夠根據當地建築的物理特性和居住者的行為進行調整。供應商透過整合專業知識、法規遵循管理和基於結果的能源保障,正在建立比單一設備銷售更牢固的客戶關係。傳統原始設備製造商 (OEM) 與分析新創公司之間的合併預示著未來市場格局的轉變:差異化的關鍵不在於晶片,而在於以託管服務形式提供的可操作洞察。

預計到2025年,低功耗藍牙(BLE)將佔技術收入的24.43%,這反映了其在智慧型手機和信標網路中的廣泛應用,以及其長達數年的電池續航力。同時,超寬頻(UWB)預計到2031年將以21.72%的複合年成長率成長,這主要得益於汽車安全標準和倉庫機器人定位對30公分以下精度的需求。 UWB相關的環境智慧市場規模正受益於IEEE 802.15.4z標準的合規性,該標準促進了新興資產追蹤生態系統中多廠商的互通性。

在精度要求達到米級的供應鏈應用中,傳統RFID仍然效用。同時,感測器融合技術整合了運動、溫度和氣體偵測器,以增強情境察覺。邊緣軟體代理程式能夠動態調整各設備的頻寬和功率預算,即使節點數量激增至數千個,也能最佳化網路彈性。嵌入混凝土和結構鋼中的奈米技術感測器正在開闢新的檢測工作流程,而情感運算模組則支援在零售和醫療保健環境中進行即時情感分析。

區域分析

預計到2025年,北美將佔全球收入的34.84%,這得益於智慧建築維修的加速推進、聯邦津貼以及支持遠端患者監護的醫療報銷政策。美國各市已利用1.6億美元的智慧城市和社區資金,實施環保應用試點項目,這些項目已證明可減少碳排放和營運成本。加拿大對隱私保護型邊緣分析的投資與該國的AI倫理戰略相符,而墨西哥的製造業叢集正在採用工業IoT來提高生產力並增強近岸外包的競爭力。該地區的一大特點是擁有強大的系統整合商網路,這些整合商正在縮短部署時間並促進多年服務合約的簽訂。

預計到2031年,亞太地區的複合年成長率將達到20.44%。中國900多個智慧城市示範計畫、印度4,800億盧比的預算撥款以及韓國21億美元的智慧城市基金,為大規模部署感測器創造了有利條件。日本的「社會5.0」計畫透過將環境智慧融入城市規劃和災害應變的各個層面,展現了人性化的整合設計理念。澳洲和紐西蘭正致力於維修為淨零能耗建築,並利用入住率分析來實現雄心勃勃的碳排放目標。儘管數據在地化方面的技術標準和法規存在差異,使得跨境協調變得複雜,但政府的資本支出和快速的都市化仍在推動這一趨勢。

歐洲的成長得益於嚴格的隱私和能源指令,這些指令鼓勵設備端處理。德國、法國、英國、義大利和西班牙佔據了該地區的大部分支出,因為企業業主正在升級其設施以符合日益嚴格的建築能源標準。在中東,以沙烏地阿拉伯耗資5000億美元的「NEOM」和阿拉伯聯合大公國的「智慧城市2030」計畫為首的大型企劃,從規劃階段就開始整合環境平台,為無縫居住者體驗樹立了標竿。待開發區和南美洲正在湧現新的機遇,行動優先的人口正在跨越固定基礎設施,部署電池供電的感測器網路,在市政預算有限的情況下提供基本的安全和環境功能。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧和物聯網設備的普及

- 政府的智慧城市計劃

- 節能智慧建築的需求

- 在醫療保健領域引入環境支持型生活(AAL)

- 聯邦學習增強了設備的上下文感知能力。

- 將環境智慧數位雙胞胎結合,用於預測性設施管理

- 市場限制因素

- 資料安全和隱私問題

- 缺乏互通性標準

- 人工智慧決策中存在較高的情境偏誤風險

- 傳統建築中複雜推理的設備端功耗預算限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體和解決方案

- 服務

- 透過技術

- Bluetooth Low Energy

- RFID

- 感應器

- 軟體表格

- 情感運算

- 奈米科技

- 生物識別

- 超寬頻

- 其他

- 按最終用戶行業分類

- 住宅

- 零售

- 衛生保健

- 產業

- 辦公大樓

- 車

- 車

- 教育

- 其他

- 透過使用

- 智慧建築管理

- 環境支持型生活

- 智慧家庭自動化

- 智慧零售分析

- 智慧製造和工業IoT

- 智慧運輸與交通

- 公共安全保障

- 能源管理

- 環境監測

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- Siemens Aktiengesellschaft

- Honeywell International Inc.

- ABB Ltd.

- Amazon.com, Inc.

- Koninklijke Philips NV

- Johnson Controls International plc

- Google LLC

- Apple Inc.

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- Robert Bosch GmbH

- Cisco Systems, Inc.

- Legrand SA

- Ingersoll Rand Inc.

- Tunstall Healthcare (UK) Ltd.

- CareTech AB

- GETEMED Medizin-und Informationstechnik AG

- Televic NV

- VITAPHONE GmbH

- Xiaomi Corporation

- Assisted Living Technologies, Inc.

第7章 市場機會與未來展望

The ambient intelligence market size is expected to increase from USD 37.20 billion in 2026 to reach USD 91.30 billion by 2031, growing at a CAGR of 19.67% over 2026-2031.

Edge inference chips that consume less than 10 watts, sovereign-AI rules in major economies, and privacy-by-design mandates are accelerating commercial adoption. Hardware vendors are responding with embedded neural-processing units while service providers package predictive-maintenance contracts that stretch beyond initial installations. Smart-city capital programs in China, India, and the Gulf states are lowering deployment risk for private investors, and reimbursement codes for remote patient monitoring in the United States are widening healthcare demand. Competitive pressure is intensifying as consumer-electronics giants port smart-home ecosystems into commercial buildings, forcing industrial-automation incumbents to bundle value-added analytics with their controllers.

Global Ambient Intelligence Market Trends and Insights

Proliferation Of AI And IoT Devices

Low-power edge processors are eliminating latency linked to cloud round-trips, which is essential in automotive, industrial, and healthcare settings. Commercial smartphones now integrate ultra-wideband radios that provide centimetric positioning, demonstrating consumer hardware's readiness for enterprise workloads. Federated-learning rollouts on mobile operating systems have proven that models can improve without exporting raw data, setting precedents for privacy-preserving occupancy sensing in offices. Multi-year battery life achieved through mesh networking and power-efficient inference allows sensor grids to blanket large floorplates with minimal retrofit disruption. Deterministic networking standards are converging with these advances, enabling safety interlocks that must react within milliseconds when environmental thresholds are breached.

Government Smart-City Initiatives

China earmarked CNY 1.2 trillion (USD 168 billion) for more than 900 smart-city pilots that embed traffic, air-quality, and safety analytics, while India's Smart Cities Mission allocated INR 48,000 crore (USD 5.76 billion) across 100 urban centers. Saudi Arabia's USD 500 billion NEOM project, plus grants in Malaysia and smaller Southeast Asian economies, underscores public-sector commitment to digital urban infrastructure. These programs establish common data platforms, demonstrate measurable energy savings, and attract complementary private investments. Vendors that satisfy local content and data-sovereignty clauses gain preferential access, accelerating regional sales pipelines. The resulting reference sites validate interoperability frameworks that smaller municipalities later adopt, expanding the ambient intelligence market.

Data Security And Privacy Concerns

European regulators levied EUR 4.5 billion (USD 5.1 billion) in GDPR fines between 2018 and 2025, with ambient systems facing rising penalties for vague consent flows and excessive retention. The 2024 EU AI Act classifies public-space biometric identification as high risk, forcing lengthy conformity assessments that slow revenue conversion. U.S. healthcare providers confront HIPAA liability when sensors inadvertently capture protected health information. Although federated learning keeps raw data on-device, regulators have yet to clarify whether aggregated model updates count as personal data, creating legal ambiguity. Rising consumer awareness means buyers demand granular opt-in dashboards, raising development costs and elongating sales cycles.

Other drivers and restraints analyzed in the detailed report include:

- Demand For Energy-Efficient Smart Buildings

- Adoption Of Ambient-Assisted Living In Healthcare

- Lack Of Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 59.61% of 2025 revenue, driven by capital outlays on sensors, gateways, and edge servers that anchor every ambient deployment. The ambient intelligence market size for services is projected to expand at a 20.17% CAGR as end users pivot toward subscription analytics, remote diagnostics, and continuous cybersecurity patching that safeguard mission-critical operations. Cost declines in microelectromechanical sensors and Bluetooth radios, along with volume production of inference accelerators, are compressing hardware margins and nudging manufacturers toward integrated offerings that wrap software and support around their devices.

Services revenue also benefits from the complexity inherent in tuning algorithms to local building physics and occupant behavior. Providers bundle domain expertise, regulatory compliance management, and outcome-based energy guarantees, creating stickier relationships than one-time equipment sales. Mergers between traditional OEMs and analytics startups foreshadow a landscape where differentiation hinges less on silicon and more on actionable insights delivered as a managed service.

Bluetooth Low Energy accounted for 24.43% technology revenue in 2025, reflecting its ubiquity in smartphones and beacon networks that enable multi-year battery life. Ultra-wideband, however, is on track to post a 21.72% CAGR through 2031 as automotive safety mandates and warehouse-robot localization demand sub-30 centimeter accuracy. The ambient intelligence market size linked to ultra-wideband benefits from IEEE 802.15.4z compliance, which fosters multivendor interoperability in emerging asset-tracking ecosystems.

Legacy RFID maintains relevance in supply-chain applications that tolerate meter-level precision, while sensor-fusion stacks integrate motion, temperature, and gas detectors to enrich contextual awareness. Edge software agents dynamically balance bandwidth and power budgets among devices, optimizing network resilience as node counts surge into the thousands. Nanotechnology-enabled sensors embedded in concrete or structural steel open new inspection workflows, while affective-computing modules surface real-time sentiment analytics in retail and healthcare environments.

Ambient Intelligence Market Report is Segmented by Component (Hardware, Software, and Services), Technology (BLE, RFID, Sensors, Biometrics, UWB, and More), End-User (Residential, Retail, Healthcare, Industrial, Office, and More), Application (Building Management, AAL, Home Automation, Retail Analytics, Manufacturing IoT, Mobility, Safety, Energy, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 34.84% of global revenue in 2025, supported by early smart-building retrofits, federal grants, and healthcare reimbursement codes that underwrite remote patient monitoring. U.S. municipalities leveraged USD 160 million in Smart Cities and Communities funding to pilot ambient applications that showcase carbon and operational savings. Canadian investments in privacy-preserving edge analytics align with national AI-ethics strategies, while Mexico's manufacturing clusters adopt industrial IoT to lift productivity and shore up near-shoring competitiveness. A robust cadre of system integrators distinguishes the region, shortening deployment timelines and fostering multiyear service contracts.

Asia-Pacific is projected to post a 20.44% CAGR through 2031 as China's 900-plus smart-city pilots, India's INR 48,000 crore allocation, and South Korea's USD 2.1 billion smart-city fund create fertile ground for large-scale sensor rollouts. Japan's Society 5.0 agenda embeds ambient intelligence across urban planning and disaster response, demonstrating integrated human-centric design. Australia and New Zealand concentrate on net-zero building retrofits, using occupancy analytics to meet aggressive carbon targets. Technical-standard fragmentation and data-localization statutes complicate cross-border harmonization, yet government capital outlays and rapid urbanization sustain momentum.

Europe's growth is anchored by stringent privacy and energy directives that favor on-device processing. Germany, France, the United Kingdom, Italy, and Spain capture the bulk of regional expenditure as corporate real-estate owners upgrade to comply with increasingly rigorous building-energy codes. The Middle East's greenfield megaprojects, led by Saudi Arabia's USD 500 billion NEOM and the United Arab Emirates' Smart City 2030 blueprint, integrate ambient platforms from inception, setting benchmarks for seamless occupant experiences. Africa and South America are emerging opportunity zones where mobile-first populations leapfrog fixed infrastructure, deploying battery-powered sensor networks that deliver foundational security and environmental functions despite constrained municipal budgets.

- Schneider Electric SE

- Siemens Aktiengesellschaft

- Honeywell International Inc.

- ABB Ltd.

- Amazon.com, Inc.

- Koninklijke Philips N.V.

- Johnson Controls International plc

- Google LLC

- Apple Inc.

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- Robert Bosch GmbH

- Cisco Systems, Inc.

- Legrand S.A.

- Ingersoll Rand Inc.

- Tunstall Healthcare (UK) Ltd.

- CareTech AB

- GETEMED Medizin- und Informationstechnik AG

- Televic N.V.

- VITAPHONE GmbH

- Xiaomi Corporation

- Assisted Living Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI and IoT Devices

- 4.2.2 Government Smart-City Initiatives

- 4.2.3 Demand for Energy-Efficient Smart Buildings

- 4.2.4 Adoption of Ambient-Assisted Living in Healthcare

- 4.2.5 Federated Learning Enhancing On-Device Context Awareness

- 4.2.6 Integration of Ambient Intelligence with Digital Twins for Predictive Facility Management

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns

- 4.3.2 Lack of Interoperability Standards

- 4.3.3 High Contextual Bias Risks in AI Decision-Making

- 4.3.4 Limited On-Device Power Budget for Complex Inference in Legacy Buildings

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software and Solutions

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Bluetooth Low Energy

- 5.2.2 RFID

- 5.2.3 Sensors

- 5.2.4 Software Agents

- 5.2.5 Affective Computing

- 5.2.6 Nanotechnology

- 5.2.7 Biometrics

- 5.2.8 Ultra-Wideband

- 5.2.9 Other Technologies

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Retail

- 5.3.3 Healthcare

- 5.3.4 Industrial

- 5.3.5 Office Building

- 5.3.6 Automotive

- 5.3.7 Automotive

- 5.3.8 Education

- 5.3.9 Other End-user Industries

- 5.4 By Application

- 5.4.1 Smart Building Management

- 5.4.2 Ambient-Assisted Living

- 5.4.3 Smart Home Automation

- 5.4.4 Smart Retail Analytics

- 5.4.5 Smart Manufacturing and Industrial IoT

- 5.4.6 Smart Mobility and Transportation

- 5.4.7 Public Safety and Security

- 5.4.8 Energy Management

- 5.4.9 Environmental Monitoring

- 5.4.10 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Siemens Aktiengesellschaft

- 6.4.3 Honeywell International Inc.

- 6.4.4 ABB Ltd.

- 6.4.5 Amazon.com, Inc.

- 6.4.6 Koninklijke Philips N.V.

- 6.4.7 Johnson Controls International plc

- 6.4.8 Google LLC

- 6.4.9 Apple Inc.

- 6.4.10 Microsoft Corporation

- 6.4.11 Samsung Electronics Co., Ltd.

- 6.4.12 Robert Bosch GmbH

- 6.4.13 Cisco Systems, Inc.

- 6.4.14 Legrand S.A.

- 6.4.15 Ingersoll Rand Inc.

- 6.4.16 Tunstall Healthcare (UK) Ltd.

- 6.4.17 CareTech AB

- 6.4.18 GETEMED Medizin- und Informationstechnik AG

- 6.4.19 Televic N.V.

- 6.4.20 VITAPHONE GmbH

- 6.4.21 Xiaomi Corporation

- 6.4.22 Assisted Living Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

環境臨床智慧市場:預測至 2034 年 - 按組件、代理類型、部署模式、技術、應用、最終用戶和地區分類的全球分析

環境臨床智慧市場:預測至 2034 年 - 按組件、代理類型、部署模式、技術、應用、最終用戶和地區分類的全球分析 2026-2030年全球環境臨床智慧市場

2026-2030年全球環境臨床智慧市場 環境智慧市場:按組件、技術、應用和地區分類

環境智慧市場:按組件、技術、應用和地區分類 2026年全球環境計算市場報告

2026年全球環境計算市場報告 環境智慧市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年

環境智慧市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年 環境智慧市場:依組件、技術、連結與網路、部署模式、產業、應用與組織規模分類-2026年至2032年全球市場預測2026年基於位置的環境智慧全球市場報告

環境智慧市場:依組件、技術、連結與網路、部署模式、產業、應用與組織規模分類-2026年至2032年全球市場預測2026年基於位置的環境智慧全球市場報告 環境智慧市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類全球環境情報市場規模、佔有率、趨勢和成長分析報告(2026-2034)

環境智慧市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類全球環境情報市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球環境運算市場:按技術、應用、組件、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和未來預測(2025-2032年)

全球環境運算市場:按技術、應用、組件、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和未來預測(2025-2032年)