|

市場調查報告書

商品編碼

2044130

硬脂酸鈣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Calcium Stearate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

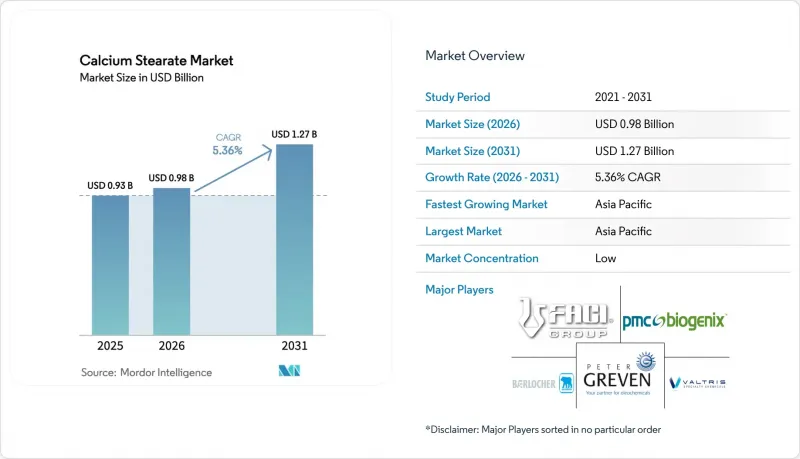

2025 年硬脂酸鈣市場價值為 9.3 億美元,預計到 2031 年將達到 12.7 億美元,而 2026 年為 9.8 億美元,預測期(2026-2031 年)複合年成長率為 5.36%。

這一成長趨勢主要受以下因素驅動:從有毒金屬基穩定劑轉向鈣基體系;潮濕地區對耐濕混凝土添加劑的需求不斷成長;以及為履行品牌所有者的永續發展承諾而逐步過渡到植物油基原料。歐盟第923/2023號法規對聚氯乙烯(PVC)中鉛含量設定了上限,該法規將於2024年11月生效,使得鉛穩定劑在歐洲的經濟效益難以為繼,從而引發了配方方面的快速轉變。這導致對硬脂酸鈣的需求增加,硬脂酸鈣在PVC擠出過程中可同時起到熱穩定劑和潤滑劑的作用。同時,亞太地區的基礎設施項目對硬脂酸鈣的需求也不斷成長。尤其是在季風敏感的沿海特大城市,混凝土外加劑生產商使用水泥含量0.5%至1.5%的硬脂酸鈣來堵塞毛細孔,防止氯離子滲入。在北美,具有永續發展意識的品牌所有者現在指定使用非棕櫚油衍生的植物性成分,買家也願意支付 10-15% 的溢價來保護供應鏈免受森林砍伐的風險,這促成了價格的強勁成長。

全球硬脂酸鈣市場趨勢及洞察

建築化學品和混凝土外加劑的擴張

硬脂酸鈣在混凝土中用作疏水性孔隙密封劑。韓國的實驗室測試表明,添加1%(以水泥重量計)的硬脂酸鈣,養護28天后,可使吸水率降低23%,氯離子滲透率降低31%。其有效性在從雅加達到清奈的海岸工程項目中尤為顯著。隨著東南亞國協政府投資擴大港口和建設高架公路,並實施經濟獎勵策略,對硬脂酸鈣的需求不斷成長,從而在水泥生產商和外加劑生產商之間形成良性循環。雖然這種添加劑的初始成本高於傳統的減水劑,但其兼具防水性和潤滑性的雙重功能,可以減少外加劑的用量。一旦完成ASTM C494的重新認證,預計該添加劑將被長期廣泛應用。

從鉛基穩定劑轉向鈣基穩定劑

根據歐盟法規 (EU) 923/2023,PVC 中鉛含量的閾值值為 0.1%,這意味著傳統的含鉛穩定劑無法再以維持顏色和耐熱性所需的用量使用。歐洲加工商的庫存非常有限,必須立即為新配方申請認證,這促使以硬脂酸鈣為中心的鈣鋅系統推廣。主要的穩定劑供應商正在積極應對這一趨勢。貝爾洛赫 (Baerlocher) 於 2023 年在印度德瓦斯 (Dewas)運作了一座低碳工廠,並已將其英國工廠的產能提高了 50% 以上。這種連鎖反應在墨西哥和越南也顯而易見,隨著全球目的地設備製造商 (OEM) 為簡化採購審核而對配方進行標準化,硬脂酸鈣在全球範圍內的應用正在不斷擴大。

硬脂酸原料價格波動

棕櫚油價格從2024年1月的每噸7481元人民幣飆升至12月的每噸10070元人民幣,並在兩個月後直接影響了硬脂酸價格。由於硬脂酸約佔硬脂酸鈣現金成本的68%,現貨經銷商的毛利率受到嚴重擠壓,導致山東和江蘇兩省的小規模獨立生產商出現一系列臨時停產。避險操作仍不均衡,許多生產商缺乏進行長期棕櫚油期貨交易所需的信貸額度,導致利潤波動加劇。

細分市場分析

預計到2025年,粉狀產品仍將佔總產量的約48.22%,這反映了傳統PVC生產線的基礎設施已相當完善。然而,在德國和日本的無人化生產單元中,為了符合ISO 45001審核標準,顆粒狀產品已被指定使用。隨著硬脂酸鈣市場向自動化稱重轉型,預計在預測期(2026-2031年)內,顆粒狀產品的市場佔有率將以5.87%的複合年成長率成長,超過粉狀產品。片狀產品仍用於橡膠的內部混煉機,但仍屬於小眾產品。由於水性塗料採用便利的「即插即用」噴塗方式,水性分散液的價格仍維持約25%的溢價。

因此,隨著原始設備製造商 (OEM) 追求無塵標準,顆粒狀產品在硬脂酸鈣市場的佔有率將會上升。早期採用者已證實,他們可以減少 15-20% 的添加劑浪費,從而直接降低廢品率。設備供應商報告稱,配備減重螺旋輸送機的 40 立方米不銹鋼筒倉訂單強勁,這表明熱塑性塑膠的商業性價值正得到整個價值鏈的認可。

區域分析

預計亞太地區將在2025年佔據主導地位,佔全球硬脂酸鈣市場佔有率的44.57%,並預計在預測期(2026-2031年)內保持這一成長勢頭,年複合成長率(CAGR)為5.63%。印尼接近性棕櫚油人工林,確保了硬脂酸原料的穩定供應;印度的國家基礎建設規劃正在擴大對PVC管道的需求。日本沿海建築規範強制要求使用可限制氯離子滲透的添加劑,儘管該地區整體建築量不大,但高品質硬脂酸鈣添加劑的使用正在推廣。

歐洲近期價格飆升與歐盟第923/2023號法規禁止使用鉛有關。未來,交聯聚乙烯取代聚氯乙烯(PVC)可能會減緩成長,但對食品接觸應用和醫藥級純度有要求的細分市場支撐了價格走強。北美轉向大豆衍生產品有助於減輕永續棕櫚油圓桌會議(RSPO)的處罰,並符合美國零售商防止森林砍伐的承諾。

拉丁美洲和中東的複合年成長率相近,這主要得益於土木工程項目儲備和新興製藥產業叢集的推動。 Bearrocker位於巴西的工廠自2013年以來分階段擴建,目前已向鄰國出口硬脂酸金屬,這表明單一地點可以如何影響區域供應鏈。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築化學品和混凝土添加劑的擴張

- 從鉛基穩定劑轉向鈣基穩定劑

- 原始設備製造商正在推廣採用無塵顆粒狀添加劑,以改善工作條件並推進工廠車間的自動化。

- 用於水性塗料的無溶劑分散體的發展

- 食品接觸包裝材料過渡到植物油衍生的硬脂酸鈣等級

- 市場限制因素

- 硬脂酸原料價格波動

- 對高活性藥物輔料中微量金屬的容許含量標準更加嚴格

- 與環境、社會及公司治理(ESG)掛鉤的貸款會懲罰棕櫚油供應鏈

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按產品形式

- 粉末

- 顆粒

- 薄片

- 分散/乳液

- 按最終用戶行業分類

- 塑膠和橡膠

- 建造

- 個人護理和藥品

- 紙

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Akrochem Corporation

- Baerlocher GmbH

- Corporacion Sierra Madre

- Dover Chemical Corporation

- FACI Corporate SpA

- GOVI NV

- Hummel Croton Inc.

- Kemipex

- Peter Greven GmbH & Co. KG

- PMC Biogenix, Inc.

- Sinwon Chemical Co., Ltd.

- Univar Solutions LLC

- Valtris Specialty Chemicals

第7章 市場機會與未來展望

The Calcium Stearate Market size was valued at USD 0.93 billion in 2025 and is estimated to grow from USD 0.98 billion in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031).

This growth path is anchored in the transition from toxic-metal stabilizers toward calcium-based systems, stronger demand for moisture-resistant concrete additives in humid regions, and a gradual pivot to vegetable-oil feedstocks to meet brand-owner sustainability pledges. Regulatory ceilings on lead in polyvinyl chloride (PVC), published under Regulation (EU) 923/2023 and effective November 2024, dismantled the economic case for lead stabilizers in Europe, triggering rapid reformulation activity that amplifies demand for calcium stearate, which simultaneously behaves as a heat stabilizer and a lubricant during PVC extrusion. Parallel growth stems from Asia-Pacific infrastructure projects where concrete admixture formulators rely on calcium stearate at 0.5-1.5% cement loading to block capillary pores and fight chloride intrusion, especially in coastal megacities vulnerable to monsoon cycles. In North America, sustainability-conscious brand owners now specify non-palm vegetable derivatives, adding price resilience as buyers accept 10-15% premiums to de-risk supply chains from deforestation exposure.

Global Calcium Stearate Market Trends and Insights

Expansion of Construction Chemicals and Concrete Additives

Calcium stearate acts as a hydrophobic pore blocker in concrete. Laboratory trials in South Korea demonstrated that 1 % dosage by cement weight lowered water absorption by 23 % and chloride penetration by 31% after 28 days of curing, benefits that resonate in coastal projects from Jakarta to Chennai. Demand intensifies as ASEAN governments channel stimulus into port expansions and elevated highways, creating a virtuous loop between cement manufacturers and admixture blenders. Although the additive's upfront cost is higher than conventional water-reducers, dual functionality, water repellency, and lubricity shrink total admixture recipes, supporting long-term adoption once ASTM C494 requalification is complete.

Switch from Lead-Based to Calcium-Based Stabilizers

The 0.1 % lead threshold in PVC under Regulation (EU) 923/2023 renders historical lead stabilizers unusable at the loadings necessary for color retention and heat stability. European converters have little buffer inventory and must certify new formulations immediately, propelling calcium-zinc systems with calcium stearate at their core. Major stabilizer vendors have responded: Baerlocher commissioned a low-carbon plant in Dewas, India, during 2023, while its United Kingdom site lifted capacity by over 50% earlier. Spill-over is evident in Mexico and Vietnam, where global OEMs (Original Equipment Manufacturers) unify recipes to streamline procurement audits, raising global calcium stearate uptake.

Volatile Stearic-Acid Feedstock Pricing

Palm oil rallied from CNY 7,481 per ton in January 2024 to CNY 10,070 per ton by December, feeding directly into stearic-acid prices with a two-month lag. Given that stearic acid forms about 68% of calcium stearate's cash cost, gross margins for spot sellers compressed markedly, prompting short production stoppages among small independents in Shandong and Jiangsu. Hedging adoption remains uneven, and many producers lack the credit lines required for long-dated palm-oil futures, heightening earnings volatility.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Dust-Free Pelletized Additives

- Growth in Solvent-Free Dispersions for Water-Borne Coatings

- Tightening Trace-Metal Limits in Pharma Excipients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Roughly 48.22% of the 2025 volume remained powder, reflecting entrenched infrastructure in legacy PVC lines. Yet lights-out molding cells in Germany and Japan now specify pellets to meet ISO 45001 audits. Granular product forms are expected to capture a 5.87% CAGR during the forecast period (2026-2031), overtaking powders, as the calcium stearate market transitions to automated dosing. Flakes persist in rubber internal-mixers but remain niche. Water-dispersions command roughly 25% price premiums thanks to their plug-and-spray convenience for water-borne coatings.

The calcium stearate market share of pelletized forms will therefore climb as OEMs chase dust-free benchmarks. Early adopters confirm 15-20% savings in additive waste, converting directly into lower scrap rates. Equipment suppliers report brisk orders for 40-m3 stainless silos fitted with loss-in-weight screws, evidence that the commercial case is accepted across thermoplastic value chains.

The Calcium Stearate Market Report is Segmented by Product Form (Powder, Granules, Flakes, and Dispersion/Emulsion), End-User Industry (Plastics and Rubber, Construction, Personal Care and Pharmaceutical, Paper, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated the Calcium Stearate market in 2025 at 44.57% and should keep momentum with a 5.63% CAGR during the forecast period (2026-2031). Proximity to Indonesian palm plantations secures stearic feedstock, while India's National Infrastructure Pipeline advances PVC pipe intakes. Japanese coastal codes mandate admixtures that limit chloride ingress, prompting high-grade calcium stearate admixture usage despite the region's modest overall construction volume.

Europe's immediate spike is linked to Regulation 923/2023 lead bans. Over the horizon, PVC substitution by cross-linked polyethylene could temper growth, though food-contact and pharma purity niches reinforce price resilience. North America's tilt toward soybean-based derivatives alleviates RSPO (Roundtable on Sustainable Palm Oil) penalties and aligns with the United States retailer deforestation pledges.

Latin America and the Middle East each advance at a similar CAGR, paced by civil-works pipelines and nascent pharma clusters. Baerlocher's Brazil site, expanded in phases since 2013, now exports metal stearates to neighboring countries, showing how a single hub can shape regional supply.

- Akrochem Corporation

- Baerlocher GmbH

- Corporacion Sierra Madre

- Dover Chemical Corporation

- FACI Corporate S.p.A.

- GOVI NV

- Hummel Croton Inc.

- Kemipex

- Peter Greven GmbH & Co. KG

- PMC Biogenix, Inc.

- Sinwon Chemical Co., Ltd.

- Univar Solutions LLC

- Valtris Specialty Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of construction chemicals and concrete additives

- 4.2.2 Switch from lead-based to Ca-based stabilizers

- 4.2.3 OEM push for dust-free pelletised additives to improve shopfloor health and automation

- 4.2.4 Growth in solvent-free dispersions for water-borne coatings

- 4.2.5 Food-contact packaging shift to vegetable-oil-derived calcium stearate grades

- 4.3 Market Restraints

- 4.3.1 Volatile stearic-acid feed-stock pricing

- 4.3.2 Tightening trace-metal limits in high-potency pharma excipients

- 4.3.3 ESG-linked loans penalising palm-oil based supply chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Form

- 5.1.1 Powder

- 5.1.2 Granules

- 5.1.3 Flakes

- 5.1.4 Dispersion / Emulsion

- 5.2 By End-user Industry

- 5.2.1 Plastics and Rubber

- 5.2.2 Construction

- 5.2.3 Personal Care and Pharmaceutical

- 5.2.4 Paper

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Akrochem Corporation

- 6.4.2 Baerlocher GmbH

- 6.4.3 Corporacion Sierra Madre

- 6.4.4 Dover Chemical Corporation

- 6.4.5 FACI Corporate S.p.A.

- 6.4.6 GOVI NV

- 6.4.7 Hummel Croton Inc.

- 6.4.8 Kemipex

- 6.4.9 Peter Greven GmbH & Co. KG

- 6.4.10 PMC Biogenix, Inc.

- 6.4.11 Sinwon Chemical Co., Ltd.

- 6.4.12 Univar Solutions LLC

- 6.4.13 Valtris Specialty Chemicals

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment