|

市場調查報告書

商品編碼

2044128

歐洲安全檢測:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

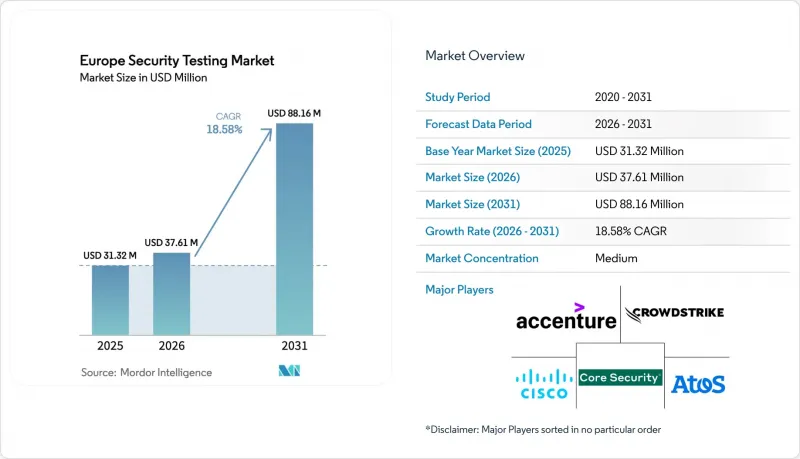

歐洲安全測試市場預計將從 2025 年的 3,132 萬美元和 2026 年的 3,761 萬美元成長到 2031 年的 8,816 萬美元,2026 年至 2031 年的年複合成長率(CAGR)為 18.58%。

這一強勁成長是由一系列監管期限、關鍵基礎設施安全漏洞激增以及雲端優先開發模式的快速普及所驅動的。德國中型企業(Mittelstand)工廠、法國公共部門數位主權計畫以及英國金融服務韌性議程正在影響採購優先事項,而混合部署架構正成為平衡資料主權需求與按需擴充性的標準方法。隨著全球顧問公司、應用安全平台和區域主要企業競相提供捆綁式託管測試訂閱服務以彌補日益擴大的技能缺口,供應商之間的競爭日益激烈。同時,能夠減少誤報的人工智慧(AI)分析也開始影響採購決策,尤其對於那些不堪重負的組織更是如此。

歐洲安全測試市場的趨勢與洞察

自 2023 年以來,針對電力和鐵路行業關鍵基礎設施的網路攻擊愈演愈烈。

2024年至2025年間,歐洲電力和交通網路嚴重事故激增68%,使得持續測試從最佳實踐轉變為董事會強制要求。 2024年德國鐵路公司遭受的勒索軟體攻擊以及2024年底波蘭一家公共產業公司遭受的DDoS攻擊,暴露了營運技術(OT)環境中曾經被認為孤立的協議漏洞。監管機構現在對未進行季度漏洞掃描的業者處以高達全球收入2%的罰款,這促使鐵路和電網營運商加快簽署多年期託管測試合約。能夠分析Modbus、DNP3和IEC 61850流量的供應商正在贏得契約,因為他們能夠提供可帶來切實改進的洞察,而不僅僅是提供一般諮詢服務。短期內,由於對OT專家的激烈競爭,諮詢服務的供應將變得緊張,導致專案日費率上漲。此外,工具製造商正在加快努力,將工業協議庫直接整合到自動化掃描器中。

歐盟加速NIS2和DORA的合規期限

NIS2 將受監管機構的數量從約 2 萬家擴大到 16 萬家,而 DORA 則對 2.2 萬家金融機構增加了嚴格的基於場景的滲透測試要求。這兩項法規共同催生了對新買家的穩定需求,而先前這些需求主要依賴自我聲明。在德國和法國等早期實施這些法規的國家,如果發現關鍵漏洞,公司必須在 72 小時內提交測試報告,這迫使它們遷移到能夠按需產生證據的 SaaS 平台。為銀行提供服務的雲端供應商和 MSP 也必須接受審計,合規壓力正在蔓延至整個供應鏈。從中長期來看,這種法律架構將使安全測試成為一項持續的營運支出,從而穩定供應商的收入預測,並提高整個歐洲的最低需求門檻。

CREST認證安全測試人員短缺

到2025年,歐洲至少需要6,000名CREST認證專業人員,但目前僅有4,200人註冊。高級測試人員的日薪在兩年內上漲了40%,而受監管的穿透測試的預約等待時間已延長至三個月。一些買家為了確保專案順利進行,降低了資質要求,這破壞了監管機構旨在實現的標準化。工具供應商正透過推廣持續自動化掃描作為臨時替代方案來填補這一缺口,但監管機構尚未驗證此類自動化是否符合DORA(國防安全審查法案)以威脅主導的範圍。短期內,人才短缺將繼續阻礙歐洲安全測試市場的成長,並加速薪資上漲,尤其是德國和荷蘭。

細分市場分析

2025年,雲端平台營收佔比達48.23%,反映出以掃描次數收費和零設備開銷在歐洲安全測試市場極具吸引力。隨著企業優先考慮快速擴展以進行季度漏洞掃描,市場需求在2026年依然強勁。然而,混合模式的複合年成長率最高,達到18.73%,因為受監管的銀行和醫院將敏感資料保留在本地,僅將元資料傳輸到SaaS主機以集中執行策略。這種配置既滿足了國家資料主權法規,又沒有犧牲彈性運算能力,從而使擁有本地資料中心的供應商更具優勢。

目前,本地部署設備主要面向國防相關企業和空氣間隙的營運技術工廠等日益萎縮的細分市場,但在禁止外部連接的環境中,它們仍然至關重要。供應商正透過提供容器化掃描器來解決這個問題,這些掃描器以虛擬鏡像的形式交付,可以整合到現有的私有雲端堆疊中,為未來的混合部署奠定基礎。在預測期內,敏感運算晶片組的改進和歐盟級認證體系的完善有望縮小人們對風險的認知差距,即使是那些先前落後的公司也將轉向至少部分雲端協作。

應用層級技術將在2025年佔據42.73%的收入佔有率,證實了在歐洲安全測試市場,可利用的程式碼路徑(而非邊界防火牆)將不再是企業風險的決定性因素。在這一類別中,雲端應用安全測試正以19.26%的複合年成長率加速成長,因為微服務、無伺服器函數和臨時容器無法使用傳統的網路探測手段進行掃描。靜態分析、動態分析和軟體配置分析已常規整合到持續整合/持續交付(CI/CD)管道中,大規模DevOps組織每月會進行數千次掃描。

行動和 Web 應用程式的測試仍然至關重要,尤其對於受 PSD2 安全通訊條款約束的數位銀行和電子商務提供者而言更是如此。然而,最大的創新在於向雲端原生運行時可見性轉變,互動式測試工具透過在程式碼中嵌入檢測點並關聯資料流證據,顯著降低誤報率。目前,供應商之間的差異化體現在平台與 GitHub Actions、GitLab CI 和 Bitbucket 工作流程的整合程度,以及能否在合併拉取請求之前識別出存在漏洞的開放原始碼程式庫。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 自 2023 年以來,針對電力和鐵路行業關鍵基礎設施的網路攻擊愈演愈烈。

- 歐盟加速NIS2和DORA的合規期限

- 在軟體供應鏈中實施左移DevSecOps

- 德國中型(Mittelstand)工廠工業IoT的採用率。

- 歐洲公共部門競標中的強制性穿透測試。

- 向抗量子密碼學過渡的先導計畫

- 市場限制因素

- CREST認證安全測試人員短缺

- 歐盟27個成員國凍結中小企業預算,以因應2024年信貸緊縮的局面。

- 資料主權法規的碎片化正在減緩基於雲端的測試發展。

- 由於假陽性結果造成的疲勞,檢測頻率降低

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 不同的發展

- 現場

- 雲

- 混合

- 按類型

- 網路安全測試

- VPN測試

- 防火牆測試

- 其他服務類型

- 應用程式安全測試

- 行動應用安全測試

- Web應用程式安全性測試

- 雲端應用安全測試

- 企業應用安全測試

- 網路安全測試

- 按測試類型

- SAST

- DAST

- IAST

- RASP

- 按最終用戶行業分類

- 政府

- BFSI

- 衛生保健

- 製造業

- 資訊科技和通訊

- 零售

- 其他終端用戶產業

- 透過測試工具

- Web應用程式測試工具

- 程式碼審查工具

- 滲透測試工具

- 軟體測試工具

- 其他測試工具

- 國家

- 英國

- 德國

- 法國

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Atos SE

- Cisco Systems, Inc.

- Core Security, LLC

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Tenable Holdings, Inc.

- Micro Focus International plc

- Snyk Limited

- HackerOne, Inc.

- Offensive Security, LLC

- Orange Cyberdefense SAS

- Paladion Networks Private Limited

- PricewaterhouseCoopers International Limited

- Qualys, Inc.

- Securonix, Inc.

- Synopsys, Inc.

- Veracode, Inc.

- Rapid7, Inc.

- Checkmarx Ltd.

- NCC Group plc

- TUV Rheinland AG

- Bureau Veritas SA

第7章 市場機會與未來展望

The Europe Security Testing Market size is projected to expand from USD 31.32 million in 2025 and USD 37.61 million in 2026 to USD 88.16 million by 2031, registering a CAGR of 18.58% between 2026 to 2031.

Robust growth is underpinned by synchronized regulatory deadlines, a sharp rise in critical-infrastructure breaches, and the rapid spread of cloud-first development models. Germany's Mittelstand factories, France's public-sector digital-sovereignty programs, and the United Kingdom's financial-services resilience agenda are shaping procurement priorities, while hybrid deployment architectures are becoming the default path to balance data-sovereignty needs with on-demand scalability. Vendor competition is intensifying as global consultancies, pure-play application security platforms, and local champions vie to offer bundled managed-testing subscriptions that address a widening skills gap. At the same time, artificial-intelligence analytics that suppress false positives are beginning to dictate buying decisions, especially among organizations fatigued by alert overload.

Europe Security Testing Market Trends and Insights

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

A 68% jump in serious incidents against European power and transport networks between 2024-2025 has moved continuous testing from a best practice to a board mandate. The 2024 ransomware disruption at Deutsche Bahn and the late-2024 DDoS attacks on Polish utilities exposed protocol weaknesses in operational-technology (OT) environments once thought to be insulated. Regulators now fine entities up to 2% of global turnover for failing to run quarterly vulnerability scans, prompting rail and grid operators to pre-book multi-year managed-testing contracts. Vendors able to decode Modbus, DNP3, and IEC 61850 traffic are winning deals because they offer actionable insights instead of generic advisories. In the short term, the scramble for OT specialists is tightening consulting supply, lifting project day rates and encouraging tool makers to embed industrial-protocol libraries directly into automated scanners.

Accelerated EU NIS2 and DORA Compliance Deadlines

NIS2 expanded the pool of regulated organizations from roughly 20,000 to 160,000 and DORA added heavy, scenario-based penetration-test obligations for 22,000 financial entities. Together, the statutes have created a steady pipeline of first-time buyers that previously relied on self-attestation. Early-enforcing states such as Germany and France already ask for test reports within 72 hours of critical findings, pushing enterprises toward SaaS platforms that can generate evidence artifacts on demand. Cloud providers and MSPs serving banks must also undergo audits, cascading compliance pressure through the supply chain. Over the medium term, this legal architecture institutionalizes security testing as a recurring operating expense, smoothing revenue visibility for vendors and raising the baseline demand floor across the continent.

Shortage of CREST-Certified Security Testers

Europe needed at least 6,000 CREST-accredited professionals in 2025 but had only 4,200 on the rolls. Daily rates for senior testers rose 40% in two years, lengthening scheduling queues to as long as three months for regulated penetration tests. Some buyers have downgraded credential requirements to keep projects on track, eroding the standardization regulators intended. Tool vendors are exploiting the gap by touting continuous automated scanning as an interim substitute, but supervisors have yet to confirm whether such automation satisfies DORA's threat-led scope. In the near term, the talent drought will remain a drag on Europe security testing market growth and will amplify wage inflation, especially in Germany and the Netherlands.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left DevSecOps Adoption in Software Supply-Chain

- Industrial IoT Penetration in German Mittelstand Factories

- Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms generated 48.23% of 2025 revenue, reflecting the appeal of pay-per-scan economics and zero appliance overhead in the Europe security testing market size. Demand stayed strong into 2026 as enterprises prioritized rapid scale-up for quarterly vulnerability sweeps. Hybrid approaches, however, show the highest 18.73% CAGR because regulated banks and hospitals keep sensitive data on-premise, routing only metadata to SaaS consoles for centralized policy enforcement. The arrangement satisfies national data-sovereignty statutes without sacrificing elastic compute, giving vendors with local datacenter footprints an edge.

On-premise appliances now serve a shrinking niche of defense contractors and air-gapped OT plants, but they remain non-negotiable where external connections are prohibited. Vendors are responding with containerized scanners shipped as virtual images that slot into existing private-cloud stacks, creating a stepping stone toward future hybrid conversions. Over the forecast window, improvements in confidential-computing chipsets and EU-level certification schemes are likely to narrow the perceived risk gap, nudging late adopters toward at least partial cloud orchestration.

Application-level techniques represented 42.73% of 2025 turnover, confirming that exploitable code paths, not perimeter firewalls, now define enterprise exposure across the Europe security testing market. Within this bucket, cloud application security testing is accelerating at 19.26% CAGR because microservices, serverless functions, and ephemeral containers cannot be scanned by legacy network probes. Static analysis, dynamic analysis, and software composition analysis are routinely chained together in CI/CD pipelines, pushing scan counts into the thousands each month for large DevOps shops.

Mobile and web application testing remains relevant, particularly among digital-banking and e-commerce providers bound by PSD2 secure-communication clauses. Yet the deepest innovation capital is migrating to cloud-native runtime visibility, where interactive testing tools instrument code and correlate data-flow evidence to slash false positives. Vendor differentiation now stems from how seamlessly platforms slot into GitHub Actions, GitLab CI, and Bitbucket workflows, and from their ability to flag vulnerable open-source libraries before pull requests are merged.

The Europe Security Testing Market Report is Segmented by Deployment (On-Premise, Cloud, and Hybrid), Type (Network Security Testing Including VPN Testing, and Application Security Testing Including Mobile), Testing Type (SAST, DAST, IAST, and RASP), End-User Industry (Government, BFSI, and More), Testing Tool (Web Application Testing Tool, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Atos SE

- Cisco Systems, Inc.

- Core Security, LLC

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Tenable Holdings, Inc.

- Micro Focus International plc

- Snyk Limited

- HackerOne, Inc.

- Offensive Security, LLC

- Orange Cyberdefense SAS

- Paladion Networks Private Limited

- PricewaterhouseCoopers International Limited

- Qualys, Inc.

- Securonix, Inc.

- Synopsys, Inc.

- Veracode, Inc.

- Rapid7, Inc.

- Checkmarx Ltd.

- NCC Group plc

- TUV Rheinland AG

- Bureau Veritas S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

- 4.2.2 Accelerated EU NIS2 and DORA Compliance Deadlines

- 4.2.3 Shift-Left DevSecOps Adoption in Software Supply-Chain

- 4.2.4 Industrial IoT Penetration in German Mittelstand Factories

- 4.2.5 Mandatory Penetration-Testing Clauses in European Public-Sector Tenders

- 4.2.6 Quantum-Resistant Crypto Migration Pilots

- 4.3 Market Restraints

- 4.3.1 Shortage of CREST-Certified Security Testers

- 4.3.2 Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

- 4.3.3 Fragmented Data-Sovereignty Rules Slowing Cloud-Based Testing

- 4.3.4 False-Positive Fatigue Reducing Test Frequency

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Type

- 5.2.1 Network Security Testing

- 5.2.1.1 VPN Testing

- 5.2.1.2 Firewall Testing

- 5.2.1.3 Other Service Types

- 5.2.2 Application Security Testing

- 5.2.2.1 Mobile Application Security Testing

- 5.2.2.2 Web Application Security Testing

- 5.2.2.3 Cloud Application Security Testing

- 5.2.2.4 Enterprise Application Security Testing

- 5.2.1 Network Security Testing

- 5.3 By Testing Type

- 5.3.1 SAST

- 5.3.2 DAST

- 5.3.3 IAST

- 5.3.4 RASP

- 5.4 By End-User Industry

- 5.4.1 Government

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 IT and Telecom

- 5.4.6 Retail

- 5.4.7 Other End-User Industries

- 5.5 By Testing Tool

- 5.5.1 Web Application Testing Tool

- 5.5.2 Code Review Tool

- 5.5.3 Penetration Testing Tool

- 5.5.4 Software Testing Tool

- 5.5.5 Other Testing Tools

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Atos SE

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Core Security, LLC

- 6.4.5 CrowdStrike Holdings, Inc.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 IBM Corporation

- 6.4.9 Tenable Holdings, Inc.

- 6.4.10 Micro Focus International plc

- 6.4.11 Snyk Limited

- 6.4.12 HackerOne, Inc.

- 6.4.13 Offensive Security, LLC

- 6.4.14 Orange Cyberdefense SAS

- 6.4.15 Paladion Networks Private Limited

- 6.4.16 PricewaterhouseCoopers International Limited

- 6.4.17 Qualys, Inc.

- 6.4.18 Securonix, Inc.

- 6.4.19 Synopsys, Inc.

- 6.4.20 Veracode, Inc.

- 6.4.21 Rapid7, Inc.

- 6.4.22 Checkmarx Ltd.

- 6.4.23 NCC Group plc

- 6.4.24 TUV Rheinland AG

- 6.4.25 Bureau Veritas S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

安全測試市場報告:按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年

安全測試市場報告:按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年 安全測試市場:按類型、組件、調查方法、產業、部署模型和組織規模分類-2026-2032年全球市場預測

安全測試市場:按類型、組件、調查方法、產業、部署模型和組織規模分類-2026-2032年全球市場預測 2026年全球安全測試市場報告

2026年全球安全測試市場報告 全球安全測試市場:按類型、網路安全測試、應用測試工具分類-預測(至 2031 年)

全球安全測試市場:按類型、網路安全測試、應用測試工具分類-預測(至 2031 年) 安全測試市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類日本安全測試市場報告(按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年)

安全測試市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類日本安全測試市場報告(按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年) 全球安全測試市場:市場規模、佔有率和趨勢分析(按類型、技術、部署方法、組織規模、最終用途和地區)、按細分市場預測(2025-2033)

全球安全測試市場:市場規模、佔有率和趨勢分析(按類型、技術、部署方法、組織規模、最終用途和地區)、按細分市場預測(2025-2033) 安全測試市場:按測試類型、按部署模式、按組織規模、垂直行業和按地區

安全測試市場:按測試類型、按部署模式、按組織規模、垂直行業和按地區 安全測試市場規模、佔有率和成長分析(按測試類型、部署模式、網路安全測試類型、組織規模、垂直和地區)- 2025-2032 年產業預測

安全測試市場規模、佔有率和成長分析(按測試類型、部署模式、網路安全測試類型、組織規模、垂直和地區)- 2025-2032 年產業預測 亞太安全測試 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太安全測試 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)