|

市場調查報告書

商品編碼

2044126

礦山機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Mining Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

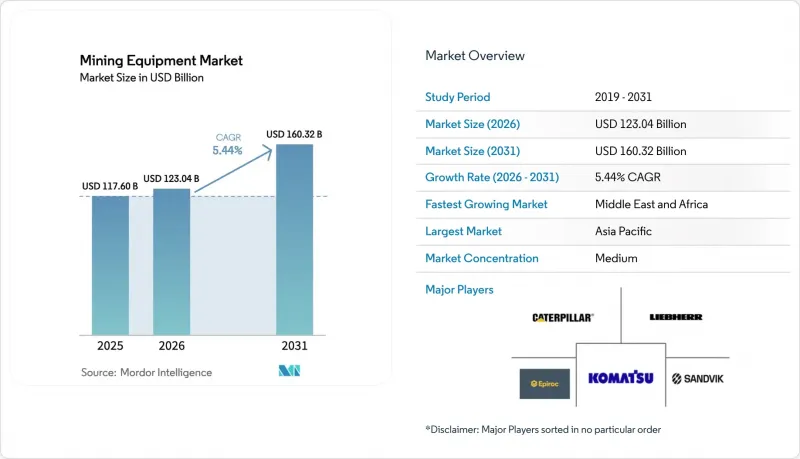

預計到 2025 年,採礦機械市場規模將達到 1,176 億美元,到 2026 年將達到 1,230.4 億美元,到 2031 年將達到 1,603.2 億美元,2026 年至 2031 年的複合年成長率為 5.44%。

這一成長主要得益於對電池礦產項目的強勁資本投資、加拿大、智利和澳洲柴油車的快速淘汰,以及西澳大利亞和巴西鐵礦石開發的重啟。儘管地面車輛仍佔據採購預算的很大一部分,但隨著鋰和銅礦礦床向更深更窄的區域轉移,對地下裝載機和鑽孔機的需求正在迅速成長。與已證實的排放措施掛鉤的資金籌措已使零排放卡車的租賃成本降低了150-200個基點,進一步刺激了對純電動車型的需求。雖然徐工和三一重工的售價低於歐美汽車製造商,但隨著Caterpillar和日本小松公司試圖透過各自的數位化平台將客戶捆綁到服務合約中來捍衛市場佔有率,競爭壓力正在加劇。

全球礦業機械市場趨勢及洞察

電池供應鏈關鍵礦物需求激增(亞洲和美國)

鋰、鈷和鎳產量的擴張正在重塑採購系統。電池金屬礦山需要與基底金屬礦山截然不同的高產能破碎機和浮選機。智利的海水礦計畫正在採用太陽能水泵,以顯著降低柴油消耗。同時,西澳大利亞的硬岩鋰礦正在指定使用超過1000馬力的運輸卡車來運輸密度高於鐵礦石的鋰輝石。在美國,《通膨控制法案》下的採購法規鼓勵買家選擇Caterpillar和日本小松公司的設備,以獲得國內採購稅額扣抵。剛果的鈷礦計畫正在從人工開採過渡到半自動裝載機,以符合可追溯性法規;印尼的紅土鎳礦礦商正在引入迴轉窯和電弧爐,為礦物加工設備創造了新的市場。這些因素正推動礦業機械市場向專業化、高利潤系統轉型,以在普遍存在的成本壓力下維持定價權。

加速加拿大、智利和澳洲強制性礦場電氣化進程

在加拿大,地下礦場必須確保至少50%的移動車輛為零排放車輛,並計畫在2030年將這一比例提高到75%。新南威爾斯州已引入通風成本課稅,旨在為深層礦場中的電池動力裝載機創造公平的競爭環境。由於這些政策,礦業公司淘汰柴油設備的速度遠超原計劃,導致Epiroc的ST18電池和Sandvik的LH518B電池的需求激增。此外,貸款機構現在要求企業制定符合ISO 14001標準的轉型計劃,作為提供融資的條件,這表明脫碳努力與資金籌措便利性之間的聯繫日益緊密。

礦石品位下降導致總擁有成本上升。

2024年,埃斯孔迪達銅礦銅品位下降,迫使必和必拓大幅增加廢棄物清除量,並導致輪胎磨損顯著加劇。同樣,西非金礦品位下降也導致破碎機礦石處理量大幅增加。低品位礦石會增加停產造成的成本。例如,在低品位銅礦,自動卸貨卡車發生故障如今會造成重大損失。為了解決這個問題,礦業公司選擇使用負載容量較高的卡車,以延長零件的使用壽命。然而,這種方法會顯著增加初始資本投入,並降低盈利。礦內破碎和運輸是一種潛在的解決方案,但它依賴長期蘊藏量的確定性,而目前許多礦床都缺乏這種確定性。

細分市場分析

到2025年,礦用卡車將佔礦山機械市場佔有率的59.22%,鞏固其作為整個礦山機械市場最大收入來源的地位。超大型運輸卡車在負載容量超過360噸、運輸距離超過5公里的大規模銅礦和鐵礦中仍然至關重要。儘管礦用卡車佔據如此巨大的市場佔有率,採購負責人仍在削減15%至20%的自動駕駛車輛,並將資金重新分配到能夠最大限度提高作業週期效率的高精度周邊設備。

預計2026年至2031年間,鑽孔機和破碎機的複合年成長率將達到6.91%,在所有設備類型中增速最高。這主要歸因於對高功率旋轉鑽機、長孔鑽機以及即使在200兆帕的高壓環境下也能可靠運作的破碎機的需求不斷成長,因為礦床越來越深、越來越堅硬。自主鑽井系統透過提高爆破破碎的均勻性並降低下游壓裂過程的能源需求,進一步提高了生產效率。這種轉變正在重塑籌資策略。營運商將鑽井自動化軟體包與卡車訂單相結合,以確保對整合調度管理和數據分析的支援。這一趨勢正在增強原始設備製造商(OEM)在礦業設備市場的交叉銷售優勢。

截至2025年,人工操作車輛佔礦山機械市場佔有率的81.65%,但全自動設備的運轉率顯著高於有人操作設備,大幅提高了單一設備的年運作。預計到2031年,全自動設備的複合年成長率將達到15.01%。在保險公司為無事故記錄提供大幅保費折扣的推動下,礦場機械市場正經歷自動駕駛系統的快速擴張。數據透明度的提高和培訓要求的降低,正推動著該行業從半自動解決方案向完全無人系統轉型。

在小規模採礦區或易受工會影響的地區,人工操作仍然普遍存在;而在地下密閉空間,人工監控又受到通訊延遲的限制。儘管監管延誤減緩了澳洲、加拿大和智利以外地區的核准進程,但一旦相關框架到位,被抑制的需求可能會引發巨大轉變。電池驅動的電動系統具有瞬時扭矩和更少的機械部件,簡化了控制邏輯,使其自然適用於自動駕駛,並加強了電氣化和自動化的良性循環。

區域分析

亞太地區預計2025年將維持59.35%的礦場機械市場佔有率,主要得益於中國煤炭開採機械化、印尼鎳產量擴張以及印度鐵礦石開採現代化。隨著煤炭產量趨於穩定和排放法規日益嚴格,中國的車輛更新換代速度已趨於平緩;而印尼則隨著不銹鋼產能的擴張,訂購了多輛運輸卡車。澳洲正從擴張轉向更新換代,以期從柴油車轉向自動駕駛純電動車(BEV),從而實現2030年的目標。日本和韓國的大部分設備都依賴進口,但日本本土企業日本小松公司、日立和現代也出口了相當一部分產品。

預計到2031年,中東和非洲地區的複合年成長率將達到8.04%,主要成長動力來自沙烏地阿拉伯的磷酸鹽生產、南非鉑金礦的現代化改造以及剛果的銅礦開採。近期,Maaden公司在該地區下了迄今為止最大的訂單,為瓦德沙馬爾礦(Waad al-Shamal mine)訂購了大量Caterpillar795F AC卡車。為了回應南非即將實施的柴油粒狀物排放法規,英帕拉鉑金公司(Impala Platinum)採取一項策略性舉措,大量訂購山特維克(Sandvik)的純電動裝載機。同時,位於剛果民主共和國的卡莫阿卡庫拉礦(Kamoa Kakura mine)正在引領新興市場的能源創新,引入了由太陽能和電池儲能相結合的微電網運作的自動駕駛卡車。

在北美,發展趨勢是增加對自動駕駛車輛的現代化投資和改造。在加拿大,紐蒙特礦業公司的博登金礦被定位為一座全電動地下金礦,凸顯了車輛電氣化的發展方向。

同時,在南美洲的智利,銅礦引進了台車輔助運輸技術,顯著降低了每噸礦石的柴油消耗量。巴西正在加強其鐵礦石產能,計劃在未來幾年內引進更多利勃海爾T 284型礦用挖土機。然而,歐洲卻面臨挑戰。近期,監管政策的不確定性阻礙了新建硬岩礦場獲得資金籌措,導致資本流入停滯不前。這些區域差異凸顯了政策和商品市場趨勢對礦業機械市場的重要影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電池供應鏈關鍵礦物需求激增(亞洲和美國)

- 加速加拿大、智利和澳洲強制性礦場電氣化進程

- 非洲銅、鈷、鋰專案的資本支出(CAPEX)持續成長。

- 與排放掛鉤的融資將降低電動車隊的資本成本。

- 西澳大利亞和巴西新鐵礦石計畫的恢復

- 預測性維護的興起正在推動售後零件銷售的成長。

- 市場限制因素

- 礦石品位降低導致總擁有成本增加。

- 偏遠礦區的電網限制延緩了電池電動車(BEV)的引進。

- 無人駕駛運輸卡車營運人員短缺

- 新建露天礦許可證取得時間的差異(歐盟和美國)

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值,10億美元)

- 透過裝置

- 露天採礦機械

- 地下採礦機械

- 礦物加工機械

- 鑽頭和破碎機

- 破碎、研磨、分類

- 裝載機和自動卸貨卡車

- 按自動化級別

- 手動設備

- 半自動自主設備

- 全自動設備

- 依動力傳動系統類型

- 內燃機車

- 電池式電動車

- 混合動力汽車

- 依輸出類型

- 不到500馬力

- 500至1000馬力

- 超過1000馬力

- 透過使用

- 金屬礦開採

- 礦產開採

- 採煤

- 按採礦類型分類

- 露天採礦

- 地下礦井

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 智利

- 秘魯

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 瑞典

- 其他歐洲地區

- 亞洲

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 其他亞洲地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 剛果民主共和國

- 尚比亞

- 其他非洲地區

- 大洋洲

- 澳洲

- 紐西蘭

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Liebherr-International AG

- Epiroc AB

- Hitachi Construction Machinery Co., Ltd.

- Atlas Copco AB

- Volvo Construction Equipment AB

- Metso Outotec Oyj

- Doosan Infracore Co.

- BEML Ltd.

- XCMG Group

- SANY Heavy Equipment

- Hyundai Construction Equipment Co.

- Terex Corporation

- Joy Global(Komatsu Mining)

- CNH Industrial NV

- JCB Ltd.

第7章 市場機會與未來展望

The mining equipment market size is projected to be USD 117.60 billion in 2025, USD 123.04 billion in 2026, and reach USD 160.32 billion by 2031, growing at a CAGR of 5.44% from 2026 to 2031.

Growth is driven by brisk capital spending on battery-mineral projects, the accelerated replacement of diesel fleets in Canada, Chile, and Australia, and renewed iron-ore developments in Western Australia and Brazil. Surface fleets continue to dominate procurement budgets, yet underground loaders and drill rigs are scaling rapidly as lithium and copper ore bodies move deeper and narrower. Financing linked to verified emission reductions is saving 150-200 basis points from lease rates on zero-emission trucks, further tilting demand toward battery-electric models. Competitive pressure is intensifying as XCMG and SANY underprice Western OEMs, while Caterpillar and Komatsu defend share through proprietary digital platforms that lock customers into bundled service contracts.

Global Mining Equipment Market Trends and Insights

Surging Demand for Critical Minerals for Battery Supply Chains (Asia and United States)

Lithium, cobalt, and nickel expansions are reshaping procurement, as battery-metal mines require high-throughput crushers and flotation cells distinct from base-metal circuits. Chilean brine projects now deploy solar-powered pumps that cut diesel use significantly, whereas Western Australia's hard-rock lithium sites specify above 1,000-horsepower haul trucks to manage spodumene densities higher than iron ore. In the United States, the Inflation Reduction Act sourcing rules steer buyers toward Caterpillar and Komatsu to capture domestic-content tax credits. Congolese cobalt projects are upgrading from manual excavators to semi-autonomous loaders to meet traceability rules, and Indonesian nickel laterite operators are installing rotary kilns and electric arc furnaces that create an addressable market for mineral-processing equipment. These factors push the mining equipment market toward specialized, higher-margin systems that command pricing power despite broader cost pressure.

Accelerated Mine Electrification Mandates in Canada, Chile and Australia

Canada requires underground mines to field zero-emission units for at least 50% of mobile fleets, rising to 75% by 2030 . New South Wales rolled out a ventilation-cost levy, leveling the playing field for battery-electric loaders at significant depths. As a result of these policies, operators are now retiring diesel assets much earlier than anticipated, leading to a surge in demand for Epiroc's ST18 Battery and Sandvik's LH518B. Additionally, lenders are now mandating ISO 14001-compliant transition plans as a prerequisite for disbursement of funds, underscoring the growing nexus between decarbonization efforts and capital accessibility.

Ore-Grade Deterioration Inflating Total Cost-Of-Ownership

In 2024, copper grades at Escondida have declined, prompting BHP to move significantly more waste material and substantially increase tire usage. Similarly, gold grades in West Africa have also dropped, leading to a notable rise in ore processing through crushers. Lower grades amplify the costs of downtime; for example, a haul-truck malfunction at a low-grade copper pit now results in significant losses. In response, operators are opting for larger-payload trucks to extend component lifespan. However, this approach significantly raises initial capital investment and reduces returns. While in-pit crushing and conveying provides a potential solution, it depends on long-term reserve certainty, which many deposits currently lack.

Other drivers and restraints analyzed in the detailed report include:

- Sustained Capex Up-Cycle in African Copper, Cobalt and Lithium Projects

- Recovery of Greenfield Iron-Ore Projects in Western Australia and Brazil

- Grid Constraints at Remote Mines Delaying BEV Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mining trucks captured 59.22% of the mining equipment market share in 2025, cementing their status as the single-largest revenue contributor to the overall mining equipment market. Ultra-class haulage remains indispensable at large copper and iron-ore pits where payloads exceed 360 tonnes and haul distances stretch beyond 5 kilometers. Despite this dominance, procurement managers are trimming absolute truck counts by 15-20% in autonomous fleets, reallocating capital toward high-precision peripheral gear that maximizes cycle efficiency.

Drills and breakers are projected to post a 6.91% CAGR from 2026 to 2031, the fastest rate among equipment types, as deeper, harder orebodies boost demand for high-power rotary rigs, long-hole drills, and rock-breakers that can operate reliably in 200 megapascal ground. Autonomous drilling systems add a further productivity kicker by delivering tighter blast fragmentation, reducing downstream energy needs in crushing circuits. This shift reshapes procurement strategies: operators are bundling truck orders with drill-automation packages to secure integrated dispatch and data analytics support. This pattern strengthens OEM cross-selling leverage within the mining equipment market.

Manual fleets held 81.65% of the mining equipment market share in 2025, yet fully autonomous units had notably higher availability compared to their manned counterparts, resulting in considerably more annual running hours per unit. Fully autonomous equipment is set to grow at a 15.01% CAGR by 2031. The mining equipment market is witnessing a rapid expansion in autonomous systems, driven by insurers offering substantial premium reductions for accident-free records. The industry is shifting away from semi-autonomous solutions toward fully driverless systems, driven by superior data clarity and reduced training requirements.

Manual gear persists in artisanal and union-sensitive jurisdictions, and underground latency issues limit manual oversight in narrow areas. Regulatory inertia outside Australia, Canada, and Chile slows approvals, but once frameworks are codified, suppressed demand could trigger a step-change. Battery-electric drive trains align naturally with autonomy because instant torque and fewer mechanical parts simplify control logic, strengthening the virtuous cycle between electrification and automation.

The Mining Equipment Market Report is Segmented by Equipment Type (Loaders, Excavators, and More), Automation Level (Manual Equipment, and More), Powertrain Type (Internal-Combustion Engine Vehicles, and More), Power Output (Less Than 500 HP, and More) Application (Metal Mining and More), Mining Type (Surface Mining and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

The Asia-Pacific region maintained a 59.35% mining equipment market share in 2025, buoyed by Chinese coal mechanization, Indonesian nickel growth, and Indian iron-ore upgrades. Chinese fleet renewals plateau as coal volumes stabilize and emission rules tighten, but Indonesia ordered several haul trucks to feed stainless-steel capacity. Australia transitions from expansion to replacement demand, swapping diesel for autonomous BEVs to meet 2030 targets. Japan and South Korea import most of their equipment, yet their domestic firms-Komatsu, Hitachi, and Hyundai-export a notable share of their output.

The Middle East and Africa region is poised for an 8.04% CAGR through 2031, driven by Saudi phosphate, South African platinum modernization, and Congolese copper. Recently, Ma'aden placed the region's most significant single order, securing a substantial number of Caterpillar 795F AC trucks for Wa'ad Al Shamal. Responding to South Africa's upcoming diesel particulate limits, Impala Platinum made a strategic move by ordering a significant number of Sandvik BEV loaders. Meanwhile, DRC's Kamoa-Kakula is pioneering energy innovation in frontier markets, operating autonomous trucks powered by a solar-plus-battery microgrid.

North America trends toward replacement spending and autonomy retrofits. In Canada, Newmont's Borden was positioned as an all-electric underground gold mine, highlighting the direction of fleet electrification.

Whereas in South America, Chile, copper pits are adopting trolley assists, achieving a considerable reduction in diesel consumption per ton hauled. Brazil is bolstering its iron-ore capacity, with additional Liebherr T 284s set to arrive over the next few years. However, Europe is facing challenges: recently, no greenfield hard-rock mine secured financial closure due to regulatory uncertainties, stalling capital influx. These regional disparities highlight the significant impact of policy and commodity dynamics on the mining equipment market.

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Liebherr-International AG

- Epiroc AB

- Hitachi Construction Machinery Co., Ltd.

- Atlas Copco AB

- Volvo Construction Equipment AB

- Metso Outotec Oyj

- Doosan Infracore Co.

- BEML Ltd.

- XCMG Group

- SANY Heavy Equipment

- Hyundai Construction Equipment Co.

- Terex Corporation

- Joy Global (Komatsu Mining)

- CNH Industrial N.V.

- JCB Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Critical Minerals for Battery Supply Chains (Asia and US)

- 4.2.2 Accelerated Mine Electrification Mandates in Canada, Chile and Australia

- 4.2.3 Sustained CAPEX Up-Cycle in African Copper, Cobalt and Lithium Projects

- 4.2.4 Emissions-Linked Financing Lowering Cost of Capital for Electric Fleets

- 4.2.5 Recovery of Greenfield Iron-Ore Projects in Western Australia and Brazil

- 4.2.6 Shift To Predictive Maintenance Driving Aftermarket Parts Pull-Through

- 4.3 Market Restraints

- 4.3.1 Ore-Grade Deterioration Inflating Total Cost-Of-Ownership

- 4.3.2 Grid Constraints at Remote Mines Delaying BEV Deployment

- 4.3.3 Talent Shortage for Autonomous Haul-Truck Operations

- 4.3.4 Uneven Permitting Timelines for New Surface Mines (EU and US)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Equipment Type

- 5.1.1 Surface Mining Equipment

- 5.1.2 Underground Mining Equipment

- 5.1.3 Mineral Processing Equipment

- 5.1.4 Drills and Breakers

- 5.1.5 Crushing, Pulverizing and Screening

- 5.1.6 Loaders and Haul Trucks

- 5.2 By Automation Level

- 5.2.1 Manual Equipment

- 5.2.2 Semi-Autonomous Equipment

- 5.2.3 Fully Autonomous Equipment

- 5.3 By Powertrain Type

- 5.3.1 Internal-Combustion Engine Vehicles

- 5.3.2 Battery-Electric Vehicles

- 5.3.3 Hybrid Vehicles

- 5.4 By Power Output

- 5.4.1 Less than 500 HP

- 5.4.2 500 - 1,000 HP

- 5.4.3 Above 1,000 HP

- 5.5 By Application

- 5.5.1 Metal Mining

- 5.5.2 Mineral Mining

- 5.5.3 Coal Mining

- 5.6 By Mining Type

- 5.6.1 Surface Mining

- 5.6.2 Underground Mining

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Chile

- 5.7.2.3 Peru

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Sweden

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Indonesia

- 5.7.4.6 Rest of Asia

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Democratic Republic of Congo

- 5.7.6.3 Zambia

- 5.7.6.4 Rest of Africa

- 5.7.7 Oceania

- 5.7.7.1 Australia

- 5.7.7.2 New Zealand

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Sandvik AB

- 6.4.4 Liebherr-International AG

- 6.4.5 Epiroc AB

- 6.4.6 Hitachi Construction Machinery Co., Ltd.

- 6.4.7 Atlas Copco AB

- 6.4.8 Volvo Construction Equipment AB

- 6.4.9 Metso Outotec Oyj

- 6.4.10 Doosan Infracore Co.

- 6.4.11 BEML Ltd.

- 6.4.12 XCMG Group

- 6.4.13 SANY Heavy Equipment

- 6.4.14 Hyundai Construction Equipment Co.

- 6.4.15 Terex Corporation

- 6.4.16 Joy Global (Komatsu Mining)

- 6.4.17 CNH Industrial N.V.

- 6.4.18 JCB Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球機械化採礦設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球機械化採礦設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 礦山機械市場:市場規模、佔有率和趨勢分析(按設備、動力來源、產量、應用和地區分類),細分市場預測(2026-2033 年)

礦山機械市場:市場規模、佔有率和趨勢分析(按設備、動力來源、產量、應用和地區分類),細分市場預測(2026-2033 年) 礦山機械市場規模、佔有率、趨勢和預測:按類型、設備、應用和地區分類,2026-2034年

礦山機械市場規模、佔有率、趨勢和預測:按類型、設備、應用和地區分類,2026-2034年 礦山機械市場:按類型、應用和地區分類

礦山機械市場:按類型、應用和地區分類 自動化採礦設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球礦業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本礦山機械市場規模、佔有率、趨勢和預測:按類型、設備、應用和地區分類,2026-2034年

自動化採礦設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球礦業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本礦山機械市場規模、佔有率、趨勢和預測:按類型、設備、應用和地區分類,2026-2034年 2026年全球行動採礦設備市場報告2026年全球電動採礦設備市場報告2026年全球礦業設備市場報告

2026年全球行動採礦設備市場報告2026年全球電動採礦設備市場報告2026年全球礦業設備市場報告