|

市場調查報告書

商品編碼

2044113

紡織化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Textile Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

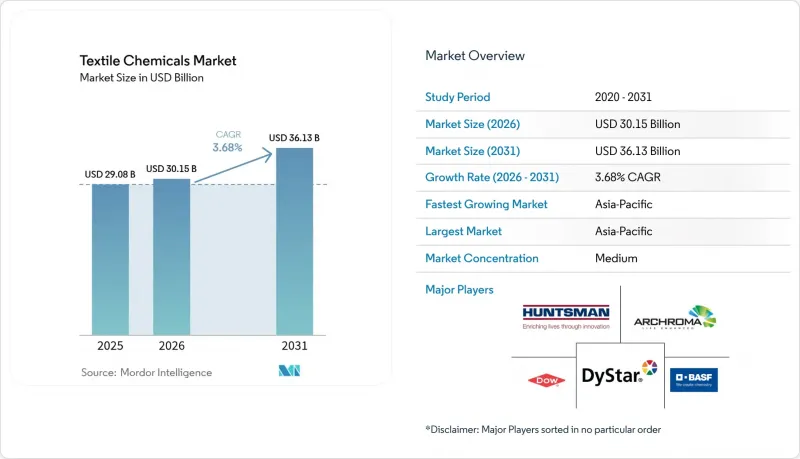

預計紡織化學品市場將從 2025 年的 290.8 億美元成長到 2026 年的 301.5 億美元,然後在 2031 年達到 361.3 億美元,2026 年至 2031 年的複合年成長率為 3.68%。

這種溫和的成長反映了紡織化學品產業正逐步成熟,以適應日益嚴格的環境法規和不斷成長的永續生產需求。亞太地區的強勁擴張、數位印花技術的日益普及以及對功能性整理劑的日益重視,正在重塑整個紡織化學品行業的競爭格局。儘管PFAS的逐步淘汰和石化產品價格的波動正在減緩短期成長勢頭,但對生物酶和水性技術的持續投資預計將維持紡織化學品行業的長期成長前景。

全球紡織化學品市場趨勢與洞察

亞太地區紡織品生產強勁成長。

全部區域紡織化學品市場正受益於產能的快速擴張和政府的支持措施。預計到2024年,中國紡織品出口額將成長5.7%,達到1,419.6億美元,主要得益於塗層、上漿和染色製程中化學品的大規模消耗。印度的生產連結獎勵計畫計畫(PLI)已撥款10683卡羅爾印度盧比用於合成纖維生產,推動了對高性能整理加工劑的長期需求。區域性供應鏈的建構促進了生物基和低VOC化學品的快速應用,進一步鞏固了亞太地區在全球紡織化學品產業的中心地位。

對工業纖維和功能性纖維的需求不斷成長

對輕量化汽車和醫療衛生要求的日益成長,促使人們制定了新的阻燃、抗菌和耐熱化學品規範標準。工業紡織品領域4.11%的複合年成長率表明,紡織化學品市場正從通用產品轉向高價、針對特定應用的配方。奈米技術驅動的整理加工劑進一步提高了性能標準,並加劇了專業供應商之間的研發競爭。

染色和表面處理工程中的污染預防成本

隨著企業努力遵守更低的化學需氧量(COD)和排放(BOD)排放基準值,維修廢水處理設施如今需要大量的資金投入。小規模的加工企業由於無法獲得生物或膜處理技術所需的資金,要么退出市場,要么進行合併,導致化學品需求集中在能夠遵守法規的大型買家手中。這種市場結構調整提高了紡織化學品市場的進入門檻,並增加了轉換成本。

細分市場分析

到2025年,塗層和漿料化學品將佔銷售額的27.96%,為梭織和針織產品的產量提供支撐。這些產品用途廣泛,即使在時尚週期放緩時期,也能確保穩定的基本需求,進而穩定紡織化學品市場。然而,創新在整理加工劑領域最為顯著,預計到2031年,該領域將以4.12%的複合年成長率成長,這主要得益於客戶對集防水、保彈和抗菌於一體的單一加工步驟的需求。

環境性能是產品平臺中的差異化因素,多功能矽聚合物混合正取代含氟防水劑。除垢劑也正轉向以生物酵素為基礎的替代品,以減少廢水排放。這些進步的結合,在保持核心收入來源的同時,提高了利潤率,進一步增強了紡織化學品市場豐富的商機。

區域分析

預計到2025年,亞太地區將佔全球銷售額的70.74%,這主要得益於中國3011億美元的出口規模以及印度預計到2030年將達到3500億美元的產業規模。區域各國政府持續津貼功能性纖維叢集,維持3.86%的複合年成長率,為全球紡織化學品市場提供了強勁支撐。從紡織紡紗到服飾製造的完整供應鏈,使得新型環保化學技術能夠迅速實用化,確保亞太地區持續保持領先地位。

北美雖然規模較小,但佔據著重要的戰略佔有率,尤其在防護、航太和醫用布料領域,這些領域更注重符合規格而非單位成本。墨西哥的近岸外包策略正在衝擊美國品牌,這帶動了該地區紗線染色廠的投資重新運作,並為高價值添加劑市場開闢了新的途徑。加州和紐約州的 PFAS 法規正在加速水性防水劑的普及,使北美成為紡織化學品行業下一代永續解決方案的試驗場。

歐洲成熟的紡織化學品產業受益於先進的機械設備和健全的法規結構,從而支持循環經濟的發展。對紡織品回收再生用化學品的投資不斷增加,其中德國和義大利在聚酯分解工廠方面處於領先地位。蓬勃發展的優質和功能性紡織品市場正在資助環保整理加工劑的研發,從而保持了歐洲在全球標準方面的影響力。雖然南美洲和中東等新興地區的生產也在不斷擴大,但基礎設施的匱乏限制了其與紡織化學品產業的全面融合。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區紡織品生產強勁成長。

- 工業和功能性紡織品的需求不斷成長

- 加強全球法規,促進低揮發性有機化合物化學品的推廣

- 數位紡織品印刷用油墨及助劑市場快速成長。

- 生物酵素處理方案的快速推廣

- 市場限制因素

- 染色和表面處理工程中的污染控制成本

- 石化原料價格波動

- 由於逐步淘汰 PFAS 和其他物質,配方變更成本增加。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 供應商的議價能力

第5章 市場規模與成長預測

- 按類型

- 塗層和上漿用化學品

- 染料和添加劑

- 整理加工劑

- 退漿劑

- 其他類型(螺紋潤滑劑、漂白劑等)

- 按成分

- 天然紡織品

- 合成紡織品

- 生物基

- 特種化學品

- 透過使用

- 服飾

- 家居佈置

- 汽車紡織品

- 工業紡織品

- 其他用途(醫用及衛生紡織品、運動紡織品等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Achitex Minerva SpA

- Albemarle Corporation

- Archroma

- BASF

- Bozzetto Group

- CHT Group

- Clariant AG

- Covestro AG

- Croda International PLC

- Dow Inc.

- DyStar Group

- Evonik Industries AG

- Huntsman International LLC

- Kemira Oyj

- Kiri Industries Ltd

- K-Tech(India)Ltd

- LN Chemical Industries

- Nouryon

- Rudolf GmbH

- Sarex

- Sumitomo Chemical Co. Ltd

- Tanatex Chemicals BV

- Wacker Chemie AG

第7章 市場機會與未來展望

The Textile Chemicals Market size market is expected to grow from USD 29.08 billion in 2025 to USD 30.15 billion in 2026 and is forecast to reach USD 36.13 billion by 2031 at 3.68% CAGR over 2026-2031.

This moderate growth reflects a maturing sector that is adapting to stricter environmental regulations and rising demand for sustainable manufacturing. Robust expansion in Asia Pacific, escalating adoption of digital printing, and heightened focus on functional finishes are together reshaping competitive priorities across the textile chemicals industry. Ongoing PFAS phase-outs and petrochemical price swings are tempering near-term momentum, yet sustained investment in bio-enzymatic and water-based technologies is expected to preserve long-run growth visibility within the textile chemicals industry.

Global Textile Chemicals Market Trends and Insights

Robust Growth in Asia Pacific Textile Production

Rapid capacity additions and supportive government incentives are lifting the textile chemicals market across Asia Pacific. China's 2024 textile exports grew 5.7% to USD 141.96 billion, sustaining large-scale chemical consumption in coating, sizing, and colorant operations. India's Production Linked Incentive program earmarking INR 10,683 crore for man-made fibres is steering long-run demand for high-performance finishes. Concentrated regional supply chains enable swift adoption of bio-based and low-VOC chemistries, reinforcing Asia Pacific's centrality within the global textile chemicals industry.

Rising Demand for Technical/Industrial Textiles

Automotive lightweighting and medical hygiene requirements are setting new specification baselines for flame-retardant, antimicrobial, and thermally resilient chemistries. The industrial textiles segment's 4.11% CAGR highlights how the textile chemicals market is transitioning from commodity volumes toward application-specific formulations that command premium pricing. Nanotechnology-enabled finishes are further elevating performance thresholds, intensifying R&D competition among specialty suppliers.

Pollution Control Costs in Dyeing and Finishing

Wastewater treatment upgrades now absorb significant capital outlays as operators strive to meet lower COD and BOD discharge limits. Smaller processors that cannot finance biological and membrane technologies are exiting or merging, consolidating chemical demand among larger, compliance-ready buyers. This restructuring raises entry barriers and raises switching costs within the textile chemicals market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Regulations Favouring Low-VOC Chemistries

- Boom in Digital-Textile Printing Inks and Auxiliaries

- Volatile Petrochemical Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coating and sizing chemicals commanded 27.96% of 2025 revenue, underpinning throughput across weaving and knitting lines. Their ubiquity secures steady baseline demand, stabilising the textile chemicals market even during fashion-cycle downturns. Innovation, however, is most visible in finishing agents, expected to grow at 4.12% CAGR through 2031 as customers request water-repellent, stretch-retentive, and antimicrobial functionalities in a single bath.

Environmental performance is differentiating product pipelines, with multifunctional silicone-polymer hybrids displacing fluorinated repellents. Desizing agents have shifted toward bio-enzymatic alternatives that reduce effluent load. Collectively these advances preserve the revenue core while elevating margins, reinforcing the wealth of opportunity in the textile chemicals market.

The Textile Chemicals Market Report is Segmented by Type (Coating and Sizing Chemicals, Colorants and Auxiliaries, and More), Raw Material (Natural Fibres, Synthetic Fibres, and More), Application (Apparel, Home Furnishing, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 70.74% revenue in 2025, supported by China's USD 301.1 billion export base and India's projected USD 350 billion industry by 2030. Regional governments continue to subsidise capacity expansion and technical-textile clusters, maintaining a 3.86% CAGR that anchors the global textile chemicals market. Supply-chain depth, from fibre spinning to garment assembly, allows rapid qualification of new green chemistries, ensuring Asia Pacific's sustained leadership.

North America holds a smaller yet strategically important share, specialising in protective, aerospace, and medical fabrics where specification compliance trumps unit cost. Mexico's near-shoring momentum to US brands is reigniting regional yarn dyehouse investments, opening fresh routes for high-value auxiliaries. California and New York PFAS rules accelerate adoption of water-based repellents, positioning North America as a testbed for next-wave sustainable options within the textile chemicals industry.

Europe's mature sector benefits from advanced machinery and a robust regulatory framework that favours circularity. Investment in textile-to-textile recycling chemicals is climbing, with Germany and Italy pioneering polyester depolymerisation plants. Strong luxury and technical segments fund R&D in low-impact finishes, upholding Europe's influence on global standards. Emerging regions in South America and the Middle East are scaling output but remain constrained by infrastructure gaps, delaying their fuller integration into the textile chemicals industry.

- Achitex Minerva SpA

- Albemarle Corporation

- Archroma

- BASF

- Bozzetto Group

- CHT Group

- Clariant AG

- Covestro AG

- Croda International PLC

- Dow Inc.

- DyStar Group

- Evonik Industries AG

- Huntsman International LLC

- Kemira Oyj

- Kiri Industries Ltd

- K-Tech (India) Ltd

- L. N. Chemical Industries

- Nouryon

- Rudolf GmbH

- Sarex

- Sumitomo Chemical Co. Ltd

- Tanatex Chemicals BV

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth in Asia Pacific textile production

- 4.2.2 Rising demand for technical/industrial textiles

- 4.2.3 Stricter global regulations favouring low-VOC chemistries

- 4.2.4 Boom in digital-textile printing inks and auxiliaries

- 4.2.5 Rapid adoption of bio-enzymatic processing solutions

- 4.3 Market Restraints

- 4.3.1 Pollution control costs in dyeing and finishing

- 4.3.2 Volatile petrochemical feedstock prices

- 4.3.3 PFAS and other substance phase-outs raising reformulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.1.1 Bargaining Power of Buyers

- 4.5.1.2 Threat of New Entrants

- 4.5.1.3 Threat of Substitutes

- 4.5.1.4 Degree of Competitive Rivalry

- 4.5.1 Bargaining Power of Suppliers

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Coating and Sizing Chemicals

- 5.1.2 Colorants and Auxiliaries

- 5.1.3 Finishing Agents

- 5.1.4 Desizing Agents

- 5.1.5 Other Types (Yarn Lubricant, Bleaching Agents, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibres

- 5.2.2 Synthetic Fibres

- 5.2.3 Bio-Based

- 5.2.4 Speciality Chemicals

- 5.3 By Application

- 5.3.1 Apparel

- 5.3.2 Home Furnishing

- 5.3.3 Automotive Textiles

- 5.3.4 Industrial Textiles

- 5.3.5 Other Applications (Medical and Hygiene Textiles, Sports Textiles, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Achitex Minerva SpA

- 6.4.2 Albemarle Corporation

- 6.4.3 Archroma

- 6.4.4 BASF

- 6.4.5 Bozzetto Group

- 6.4.6 CHT Group

- 6.4.7 Clariant AG

- 6.4.8 Covestro AG

- 6.4.9 Croda International PLC

- 6.4.10 Dow Inc.

- 6.4.11 DyStar Group

- 6.4.12 Evonik Industries AG

- 6.4.13 Huntsman International LLC

- 6.4.14 Kemira Oyj

- 6.4.15 Kiri Industries Ltd

- 6.4.16 K-Tech (India) Ltd

- 6.4.17 L. N. Chemical Industries

- 6.4.18 Nouryon

- 6.4.19 Rudolf GmbH

- 6.4.20 Sarex

- 6.4.21 Sumitomo Chemical Co. Ltd

- 6.4.22 Tanatex Chemicals BV

- 6.4.23 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球紡織整理化學品市場

全球紡織整理化學品市場 紡織助劑市場規模、佔有率和成長分析:按類型、應用、纖維類型和地區分類-2026-2033年產業預測

紡織助劑市場規模、佔有率和成長分析:按類型、應用、纖維類型和地區分類-2026-2033年產業預測 紡織化學品市場報告:按紡織品類型、產品類型、應用和地區分類(2026-2034 年)

紡織化學品市場報告:按紡織品類型、產品類型、應用和地區分類(2026-2034 年) 紡織品整理化學品市場:依化學品類型、技術、紡織品類型及應用分類-2026-2032年全球市場預測紡織化學品市場:按類型、製程、纖維類型、形態、應用和分銷通路分類-2026-2032年全球市場預測

紡織品整理化學品市場:依化學品類型、技術、紡織品類型及應用分類-2026-2032年全球市場預測紡織化學品市場:按類型、製程、纖維類型、形態、應用和分銷通路分類-2026-2032年全球市場預測 紡織化學品市場:按產品類型、最終用戶和地區分類

紡織化學品市場:按產品類型、最終用戶和地區分類 全球紡織加工化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紡織助劑市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球紡織加工化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紡織助劑市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球紡織化學品市場報告2026年全球紡織品整理化學品市場報告

2026年全球紡織化學品市場報告2026年全球紡織品整理化學品市場報告