|

市場調查報告書

商品編碼

2044111

銻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Antimony - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

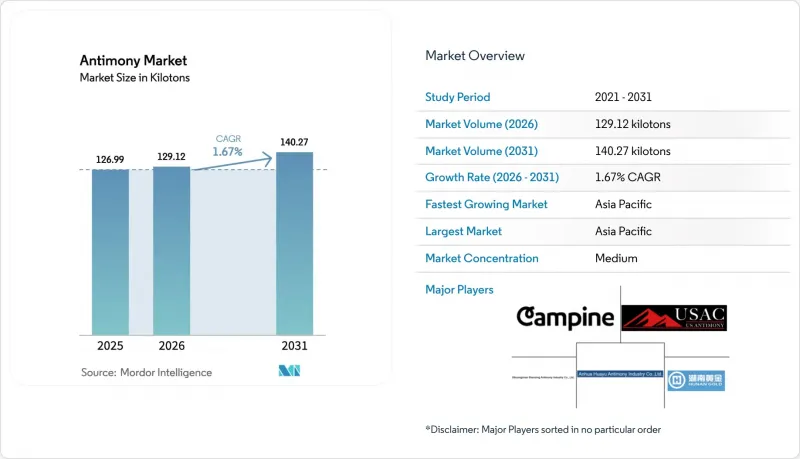

2025 年銻市場價值為 126.99 千噸,預計到 2031 年將達到 140.27 千噸,而 2026 年為 129.12 千噸,預測期(2026-2031 年)複合年成長率為 1.67%。

價格飆升暴露了對中國供應的結構性依賴。戰略需求持續轉向儲能、半導體摻雜和國防電子領域,在這些領域,銻的冶金和電子性能幾乎無可取代。為因應中國將於2024年12月實施的出口禁令,西方礦業公司、精煉商和政府正在愛達荷州、蒙大拿州和澳洲擴大新的產能。該禁令已使基準價格加倍,並促進了垂直一體化項目的開展。同時,歐洲和北美更嚴格的毒性法規正逐步加速向無鹵阻燃劑的轉型,這抑制了供應成長,但同時推高了對高純度和特種級銻的需求。競爭優勢正從成本轉向純度、產地和供應穩定性,尤其是在半導體級材料領域。

全球銻市場趨勢及洞察

亞太地區電網級鉛酸蓄電池和液態金屬蓄電池的擴張

公用事業規模的儲能系統正日益影響銻市場。 2024年2月,Ambri公司完成D輪資金籌措,並計畫向Xcel Energy和Vistra公司交付銻鉛正極的液態金屬電池。在東南亞,鉛酸電池仍然是通訊備用電源的主流選擇,但銻正被添加到電網合金中以增強其深迴圈耐久性。在中國,儘管電氣化趨勢正在加速發展,但內燃機汽車的數量仍然龐大,這支撐了銻的基準需求,並鞏固了汽車產業的銻市場地位。雖然鈣錫合金的興起可能會減少電池中銻的使用量,但電網級液態金屬系統透過每個模組消耗大量高純度銻來抵消這一趨勢。這一趨勢不僅將在中期內提振整體需求,還將提升符合嚴格純度標準的銻產品的價值。

PET樹脂的蓬勃發展推動了銻催化劑的使用。

三氧化二銻是聚對苯二甲酸乙二醇酯(PET)生產中90%以上產品的主要聚合催化劑。沙烏地阿拉伯和越南的新PET生產設施計畫於2027年運作。帝人公司近期獲得一項三元催化劑混合物專利,凸顯了業界在保持其動力學優勢的同時,努力降低殘留銻含量的努力。然而,監管機構正密切關注。歐洲化學品管理局目前正在重新評估食品接觸包裝材料的允許遷移限量。此次審查將產生合規成本,並可能促使業界轉向使用鈦基體系生產高階產品。儘管銻目前憑藉其低資本投入和成熟的技術應用仍保持著作為催化劑的優勢,但下游生產商正在積極尋求替代方案以降低監管風險。這種謹慎的做法可能會在未來兩年或更長時間內抑制銻市場的成長前景。

中國不穩定的出口配額和飆升的價格

從2023年12月到2025年2月,鹿特丹基準鋅價大幅上漲。這一快速成長擠壓了複合材料生產商和電池製造商的利潤空間,使其難以將這些成本轉嫁給消費者。在歐洲和北美,中小加工企業正直接感受到現金流緊張的影響,有些企業甚至暫停生產,直到價格穩定。韓國鋅的年供應量仍然有限,僅佔全球礦產產量的一小部分。這種有限的供應使得歐美買家極易受到北京政策變化的影響。隨著輝銻礦等項目的投產,持續的價格波動預計將影響預期的複合年成長率。

細分市場分析

三氧化二銻作為PET催化劑和阻燃劑的成熟應用,在2025年佔了56.48%的供應量。然而,由於歐洲市場轉向無鹵替代品,其成長動能受到限制。五氧化二銻的複合年成長率(CAGR)為2.5%,這主要得益於其優異的脫色和精煉性能,受到特種玻璃和太陽能製造商的青睞。韓國鋅業供應的高純度金屬錠滿足了軍工和半導體產業對高純度銻的需求。在鉛酸電池合金領域,鈣錫合金的興起導致銻含量下降,但電網級電池的普及在一定程度上抵消了這一影響。此外,一些小眾產品,例如用於煙火的硫化銻,雖然利潤率高,但產量極低,凸顯了銻市場多元化的發展趨勢。

儘管五氧化二銻的興起提升了特種產品的獲利能力,但除歐洲和北美以外,三氧化二銻的主導地位依然穩固。帝人公司在三元催化劑方面的技術進步有望透過抑制遷移而不影響反應速率,進一步鞏固三氧化二銻在PET領域的領先地位。即使在這方面取得微小的成功,也能保護全球銻需求的很大一部分免受即將到來的替代品的衝擊。因此,銻市場以高產量、受監管的三氧化二銻為基礎,輔以快速成長的五氧化二銻和利潤豐厚的高純度錠材細分市場。

到2025年,阻燃劑的消費量佔比將達到55.02%,但這一主導地位在歐洲和美國正在減弱。陶瓷和玻璃產業正以3.3%的複合年成長率成長,這主要得益於太陽能發電用玻璃的微型化以及銻摻雜單晶矽的應用。 PET聚合催化劑的需求依然強勁,但易受監管壓力的影響。以公斤計的特殊電子應用利潤率高,且具有重要的策略意義。這種應用結構表明,儘管規模有所下降,但阻燃劑正向高附加價值領域轉移,即使成熟經濟體阻燃劑的消費量下降,也能起到緩衝作用,支撐整體銷售。

陶瓷產業的需求可以對沖監管方面的不利因素,尤其是在太陽能玻璃製造商需要五氧化二銻來提高透明度和去除氣泡的情況下。電池產業也提供了另一種對沖手段。雖然汽車起動器中銻的單位用量正在下降,但電網級項目每個模組仍需要數公斤的添加劑。因此,銻市場擁有多元化的需求促進因素,降低了單一應用領域所帶來的下行風險。

本銻市場報告按產品類型(金屬錠、三氧化二銻、五氧化二銻、合金及其他)、礦石類型(輝銻礦及其他)、應用領域(阻燃劑、北美電池等)、終端用戶產業(塑膠及聚合物、汽車及運輸等)及地區(亞太地區、北美電池等)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔全球銻產量的86.67%,年複合成長率達3.12%。 2024年,中國開始提煉銻,但面臨礦石短缺和合規成本,運作能利用率僅三分之一。印度塑膠和摩托車產業需求的成長,以及越南PET需求的激增,正在鞏固亞太地區在銻市場的核心地位。儘管日本國內也有精煉業務,但仍是銻淨進口國,主要從中國和越南進口。同時,韓國鋅業正在提高產量,並計劃逐步增產,預計部分產量將銷往歐洲和美洲市場。

在北美,各方正積極籌備擴大供應。 Perpetua公司的輝銻礦開採項目以及Antimony公司在墨西哥和蒙大拿州的業務,預計將在未來幾年滿足國內相當一部分需求。這項需求主要由國防電子、電網級儲能系統和半導體製造等產業推動,尤其是在《晶片與科學法案》的推動下,國內生產得以恢復。歐洲仍高度依賴進口,而對阻燃劑更嚴格的監管正促使比利時Campine等加工商轉向回收。在中東、非洲和南美地區,玻利維亞和摩洛哥在供應多元化方面發揮著至關重要的作用,但它們的總產量對緩解供應短缺的影響有限。

儘管歐美努力實現供應來源多元化,但中國冶煉廠仍持續受益於提煉規模經濟,預計未來幾年亞太市場佔有率將略有下降。然而,出於建構穩健供應鏈的政治考量,即使絕對交易量跟不上區域需求成長,預計更大比例的銻市場交易量將透過中國以外的管道進行。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區電網級鉛酸蓄電池和液態金屬蓄電池的擴張

- PET樹脂的蓬勃發展促進了銻催化劑的使用。

- 中國的出口限制正在刺激對中國境外供應鏈的投資。

- 銻合金在下一代鈣鈉液態金屬電池中的應用

- 用於 5G 和量子裝置的半導體級銻

- 市場限制因素

- 中國出口配額波動與價格上漲

- 歐盟和北美向無鹵阻燃劑過渡

- REACH/TSCA毒理學合規成本

- 價值鏈分析

- 生產分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 供應分析

- 監理政策分析

- 貿易分析

- 價格趨勢分析

- 生產成本分析

第5章 市場規模與成長預測

- 依產品類型

- 金屬錠

- 三氧化銻

- 五氧化二銻

- 合金

- 其他產品種類(顆粒、單晶等)

- 依礦石類型

- 銻酸鹽

- 其他

- 透過使用

- 阻燃劑

- 電池

- 陶瓷和玻璃

- 催化劑

- 其他應用領域(半導體、國防等)

- 按最終用戶行業分類

- 塑膠和聚合物

- 汽車和交通運輸

- 化學品和催化劑

- 電子和半導體

- 儲能和公共產業

- 其他行業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alkane Resources Ltd.

- AMG Advanced Metallurgical Group NV

- Belmont Metals Inc.

- Campine NV

- GUANGXI HUAYUAN METAL CHEMICAL CO., LTD.

- Hunan Gold Co., Ltd.

- Hunan Province Anhua Huayu Antimony Industry Co., Ltd.

- Koreazinc

- Lambert Metals International Limited

- Nihon Seiko Co., Ltd.

- Perpetua Resources

- SPMP(Strategic and Precious Metals Processing)

- SUZUHIRO CHEMICAL CO.,LTD.

- United States Antimony Corporation

- Xikuangshan Shanxing Antimony Industry Co., Ltd.

- Yiyang City Huachang Antimony Industry Co.,Ltd

- Youngsun(Guangdong Yuxing)Fire-Retardant New Material Co.

- Yunnan Muli Antimony Industry Co., Ltd.

第7章 市場機會與未來展望

The Antimony Market size was valued at 126.99 kilotons in 2025 and is estimated to grow from 129.12 kilotons in 2026 to reach 140.27 kilotons by 2031, at a CAGR of 1.67% during the forecast period (2026-2031).

A rapid price escalation exposed structural reliance on Chinese supply. Strategic demand continues to pivot toward energy storage, semiconductor doping, and defense electronics, where antimony's metallurgical and electronic properties have few substitutes. Western miners, refiners, and governments are scaling new capacity in Idaho, Montana, and Australia to counter China's December 2024 export ban, a move that doubled benchmark prices and spurred vertically integrated projects. Meanwhile, regulatory scrutiny over toxicology in Europe and North America is accelerating a gradual shift to halogen-free flame retardants, tempering volume growth but pushing value toward higher purity and specialty grades. Competitive differentiation is shifting away from cost and toward purity, provenance, and security of supply, especially for semiconductor-grade material.

Global Antimony Market Trends and Insights

Grid-Scale Lead-Acid and Liquid-Metal Battery Expansion in Asia-Pacific

Utility-scale storage is increasingly shaping the Antimony market. In February 2024, Ambri secured Series D financing and is set to deliver liquid-metal batteries, reliant on antimony-lead cathodes, to Xcel Energy and Vistra. While lead-acid batteries continue to dominate telecom backups throughout Southeast Asia, they incorporate antimony in their grid alloys to enhance deep-cycle durability. China's vast fleet of internal-combustion vehicles, even as electrification gains momentum, bolsters baseline demand, anchoring the Antimony market firmly in the automotive sector. Although the rise of calcium-tin alloys might reduce antimony usage in batteries, grid-scale liquid-metal systems counteract this by consuming significant amounts of high-purity antimony per module. This dynamic not only boosts aggregate volumes in the medium term but also enhances the value of supply adhering to stringent purity standards.

PET Resin Boom Boosting Sb-Catalyst Use

Antimony trioxide serves as the primary polymerization catalyst for over 90% of polyethylene terephthalate (PET) production. New PET facilities in Saudi Arabia and Vietnam are set to begin operations before 2027. Teijin's recent patent on ternary catalyst mixtures underscores the industry's push to reduce residual antimony while maintaining kinetic benefits. However, regulators are keeping a close watch. The European Chemicals Agency is currently reevaluating the permissible migration limits for food-contact packaging. This scrutiny introduces compliance costs, potentially steering the industry towards titanium-based systems for premium products. While low capital expenditure and established expertise currently uphold antimony's dominance as a catalyst, downstream producers are actively exploring alternatives to mitigate regulatory risks. This cautious approach tempers the growth outlook for the antimony market beyond the immediate two-year horizon.

Volatile Chinese Export Quotas and Price Spikes

Benchmark Rotterdam prices surged significantly from December 2023 to February 2025. This sharp rise has squeezed margins for compounders and battery makers, who find it challenging to pass on these costs. In Europe and North America, small and mid-sized processors are feeling the brunt of this cash-flow strain, with some even pausing production until prices stabilize. Korea Zinc's annual supply remains limited, accounting for a small fraction of the global mined output. This limited supply leaves Western buyers vulnerable to policy shifts in Beijing. As projects like Stibnite gear up, the ongoing volatility is projected to impact the forecasted CAGR.

Other drivers and restraints analyzed in the detailed report include:

- China Export Controls Driving Non-China Supply-Chain Investment

- Antimony Alloying in Next-Gen Calcium/Sodium Liquid-Metal Batteries

- Shift Toward Halogen-Free Flame Retardants in EU and NA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antimony trioxide held 56.48% of the 2025 volume, reflecting its entrenched roles in PET catalysis and flame retardancy. However, its growth trajectory faces constraints due to Europe's shift towards halogen-free alternatives. Antimony pentoxide is expanding at a 2.5% CAGR as specialty glass and photovoltaic manufacturers seek its superior decolorizing and fining capabilities. Metal ingots, boasting a premium purity from Korea Zinc, cater to the high-purity demands of the military and semiconductor sectors. While lead-acid battery alloys are seeing reduced antimony loadings due to the rise of calcium-tin formulations, grid-scale batteries are helping to offset this decline. Additionally, niche products like antimony trisulfide, favored in pyrotechnics, command high margins but contribute negligible tonnage, highlighting the diverse dynamics within the antimony market.

While pentoxide's ascent bolsters specialty revenues, trioxide's dominance remains unchallenged outside Europe and North America. Teijin's advancements in ternary catalysts could extend trioxide's reign in the PET sector by curbing migration without compromising kinetics. Even a slight success in this endeavor could insulate a significant portion of global antimony demand from imminent substitutions. Thus, the antimony market is characterized by a volume-heavy, regulation-sensitive trioxide foundation, complemented by the rapid growth of pentoxide and a niche high-purity ingot segment that drives significant profits.

Flame retardants consumed 55.02% of the 2025 volume, but that dominance is losing momentum in the West. Ceramics and glass are growing at a 3.3% CAGR thanks to photovoltaic glass fining and antimony-doped monocrystalline silicon. Catalyst demand in PET polymerization remains substantial but is sensitive to regulatory pressure. Specialty electronic uses, measured in kilograms, carry high margins and strategic significance. This application mix indicates a transition toward fewer but higher value streams, creating a cushion for aggregate revenues even if flame-retardant tonnage erodes in mature economies.

Ceramic demand provides a hedge against regulatory headwinds, particularly as solar-glass producers secure antimony pentoxide to improve clarity and bubble removal. Batteries offer another hedge: although per-unit antimony intensity is falling in automotive starters, grid-scale projects require kilogram-level loadings per module. Therefore, the Antimony market maintains diversified demand drivers that temper downside risk from any single application class.

The Antimony Market Report is Segmented by Product Type (Metal Ingot, Antimony Trioxide, Antimony Pentoxide, Alloys, and Other Product Types), Ore Type (Stibnite and Others), Application (Flame Retardants, Batteries, and More), End-User Industry (Plastics and Polymers, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 86.67% of global volume in 2025 and is expanding at a 3.12% CAGR. In 2024, China refined antimony but operated at only one-third of its installed capacity, grappling with ore scarcity and compliance costs. Rising demand in India's plastics and two-wheeler sectors, coupled with Vietnam's PET surge, solidifies Asia-Pacific's central role in the Antimony market. Despite domestic refining, Japan remains a net importer, predominantly sourcing from China and Vietnam. Meanwhile, South Korea's Korea Zinc increased its output and plans a modest rise, with a portion of the production targeted for Western markets.

North America is gearing up for a supply expansion. Projects like Perpetua's Stibnite and operations by United States Antimony in Mexico and Montana are poised to meet a significant portion of domestic needs in the coming years. This demand is driven by sectors like defense electronics, grid-scale storage, and semiconductor fabs, especially with the reshoring push under the CHIPS and Science Act. While Europe relies heavily on imports, tightening regulations on flame retardants are prompting processors like Belgium's Campine to pivot towards recycling. In the Middle East-Africa/South America region, Bolivia and Morocco are key players in diversifying the supply, but their combined output offers only limited relief.

Despite Western diversification efforts, the Asia-Pacific market share is expected to decline slightly in the coming years, as Chinese smelters continue to benefit from economies of scale in refining. Yet, driven by political motivations for resilient supply chains, a larger portion of the Antimony market volumes is anticipated to flow through non-Chinese channels, even if the absolute tonnage doesn't keep pace with regional demand growth.

- Alkane Resources Ltd.

- AMG Advanced Metallurgical Group N.V.

- Belmont Metals Inc.

- Campine NV

- GUANGXI HUAYUAN METAL CHEMICAL CO., LTD.

- Hunan Gold Co., Ltd.

- Hunan Province Anhua Huayu Antimony Industry Co., Ltd.

- Koreazinc

- Lambert Metals International Limited

- Nihon Seiko Co., Ltd.

- Perpetua Resources

- SPMP (Strategic and Precious Metals Processing)

- SUZUHIRO CHEMICAL CO.,LTD.

- United States Antimony Corporation

- Xikuangshan Shanxing Antimony Industry Co., Ltd.

- Yiyang City Huachang Antimony Industry Co.,Ltd

- Youngsun (Guangdong Yuxing) Fire-Retardant New Material Co.

- Yunnan Muli Antimony Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-scale lead-acid and liquid-metal battery expansion in Asia-Pacific

- 4.2.2 PET resin boom boosting Sb-catalyst use

- 4.2.3 China export controls driving non-China supply-chain investment

- 4.2.4 Antimony alloying in next-gen calcium/sodium liquid-metal batteries

- 4.2.5 Semiconductor-grade Sb for 5G and quantum devices

- 4.3 Market Restraints

- 4.3.1 Volatile Chinese export quotas and price spikes

- 4.3.2 Shift toward halogen-free flame retardants in EU and NA

- 4.3.3 REACH/TSCA toxicology compliance costs

- 4.4 Value Chain Analysis

- 4.5 Production Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Supply Analysis

- 4.8 Regulatory Policy Analysis

- 4.9 Trade Analysis

- 4.10 Price Trend Analysis

- 4.11 Production Cost Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Metal Ingot

- 5.1.2 Antimony Trioxide

- 5.1.3 Antimony Pentoxide

- 5.1.4 Alloys

- 5.1.5 Other Product Types (Granules, Single Crystals, etc.)

- 5.2 By Ore type

- 5.2.1 Stibnite

- 5.2.2 Others

- 5.3 By Application

- 5.3.1 Flame Retardants

- 5.3.2 Batteries

- 5.3.3 Ceramics and Glass

- 5.3.4 Catalyst

- 5.3.5 Other Applications (Semiconductor, Defense, etc.)

- 5.4 By End-user Industry

- 5.4.1 Plastics and Polymers

- 5.4.2 Automotive and Transportation

- 5.4.3 Chemicals and Catalysts

- 5.4.4 Electronics and Semiconductor

- 5.4.5 Energy Storage and Utilities

- 5.4.6 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacifc

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacifc

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles

- 6.4.1 Alkane Resources Ltd.

- 6.4.2 AMG Advanced Metallurgical Group N.V.

- 6.4.3 Belmont Metals Inc.

- 6.4.4 Campine NV

- 6.4.5 GUANGXI HUAYUAN METAL CHEMICAL CO., LTD.

- 6.4.6 Hunan Gold Co., Ltd.

- 6.4.7 Hunan Province Anhua Huayu Antimony Industry Co., Ltd.

- 6.4.8 Koreazinc

- 6.4.9 Lambert Metals International Limited

- 6.4.10 Nihon Seiko Co., Ltd.

- 6.4.11 Perpetua Resources

- 6.4.12 SPMP (Strategic and Precious Metals Processing)

- 6.4.13 SUZUHIRO CHEMICAL CO.,LTD.

- 6.4.14 United States Antimony Corporation

- 6.4.15 Xikuangshan Shanxing Antimony Industry Co., Ltd.

- 6.4.16 Yiyang City Huachang Antimony Industry Co.,Ltd

- 6.4.17 Youngsun (Guangdong Yuxing) Fire-Retardant New Material Co.

- 6.4.18 Yunnan Muli Antimony Industry Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 Recycling of end-of-life lead-acid batteries

- 7.2 Development of domestic refining outside China

- 7.3 White-space and unmet-need assessment

銻市場報告:按產品類型、應用、終端用戶產業和地區分類(2026-2034 年)

銻市場報告:按產品類型、應用、終端用戶產業和地區分類(2026-2034 年) 銻市場:全球市場按產品類型、形態、純度和應用分類的預測 - 2026-2032年

銻市場:全球市場按產品類型、形態、純度和應用分類的預測 - 2026-2032年 電子元件用銻市場:策略性洞察與預測(2026-2031)銻市場規模、佔有率、成長及全球產業分析:按應用和地區分類的洞察與預測(2026-2034 年)全球三氧化二銻市場規模、佔有率、趨勢和成長分析報告(2026-2034年)銻全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

電子元件用銻市場:策略性洞察與預測(2026-2031)銻市場規模、佔有率、成長及全球產業分析:按應用和地區分類的洞察與預測(2026-2034 年)全球三氧化二銻市場規模、佔有率、趨勢和成長分析報告(2026-2034年)銻全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球銻市場報告掩蔽化合物市場依固化類型、技術、形態、通路、最終用途產業和應用分類-2026-2032年全球預測電子級砷化氫市場按混合類型、純度等級、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測

2026年全球銻市場報告掩蔽化合物市場依固化類型、技術、形態、通路、最終用途產業和應用分類-2026-2032年全球預測電子級砷化氫市場按混合類型、純度等級、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測 銻市場規模、佔有率及成長分析(按類型、應用、最終用途產業和地區分類)-產業預測(2026-2033 年)

銻市場規模、佔有率及成長分析(按類型、應用、最終用途產業和地區分類)-產業預測(2026-2033 年)