|

市場調查報告書

商品編碼

2044109

高抗張強度鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)High Strength Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

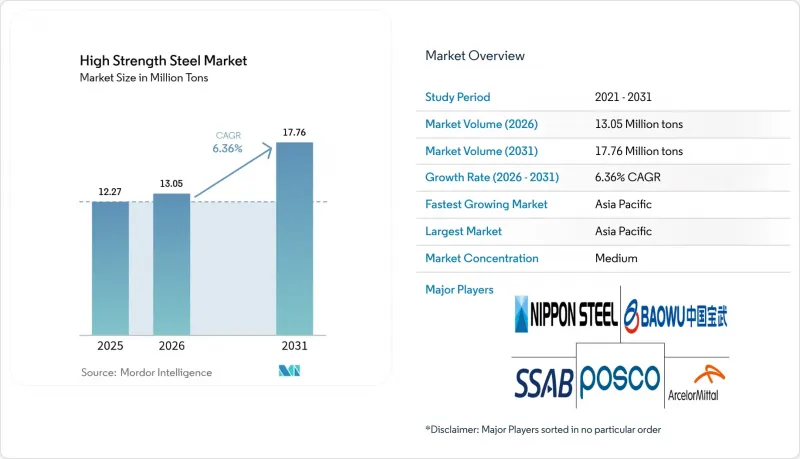

預計高抗張強度鋼市場將從 2025 年的 1,227 萬噸成長到 2026 年的 1,305 萬噸,然後從 2026 年到 2031 年以 6.36% 的複合年成長率成長,到 2031 年達到 1,776 萬噸。

對輕量化汽車、模組化高層建築和離岸風力發電塔架日益成長的需求,直接推動了抗張強度超過600兆帕且具有高衝擊能量吸收能力的鋼材訂單的成長。雙相鋼因其鐵素體-馬氏體基體即使在複雜的成形過程中也能維持延伸率,因此價格較高。汽車製造商利用這項特性製造車門內裝件和輪圈罩等沖壓件。熱成型鋼在電池式電動車底盤框架領域迅速普及,這些框架必須能夠承受側面碰撞測試,同時還要保護鋰離子電池模組免受熱失控的影響。同時,微合金鐵素體-貝氏體鋼板正逐漸成為氫兼容管道的理想材料,這表明隨著大直徑幹線管道從試驗階段走向商業化規模,它們將成為未來的成長中心。

全球高抗張強度鋼市場趨勢及洞察

汽車輕量化和碰撞安全法規

歐盟對車隊二氧化碳排放量設定的上限為95克/公里,美國則設定了54.5英里/加侖的燃油效率目標,這迫使汽車製造商從普通鋼材轉向能夠將車身本體重量降低20-30%的鋼材,同時還要通過日益嚴格的小重疊碰撞和側面碰撞測試。美國公路安全保險協會(IIHS)的測試規程更新提高了乘員生存空間標準,導致對熱沖壓1500兆帕B柱的需求增加。通用汽車(GM)表示,基於Ultium鋼的卡車現在在駕駛室結構中使用980兆帕雙相鋼,使車輛重量減輕180公斤,扭轉剛度提高15%。中國的GB 38900-2020測試標準結合了側柱碰撞和車頂壓潰測試,這種組合有利於在A柱和B柱設計中使用馬氏體鋼和雙相鋼。福特公司已確認,採用壓硬化鋼製成的電池外殼符合聯邦機動車輛安全標準 305 (FMVSS 305),無需額外的鋁擠壓件,並簡化了底盤組裝。

模組化高層建築的快速成長

預製鋼模組使S460-S690級鋼柱能夠以更薄的壁厚承受相同的荷載,從而使建築商在城市地區將工期縮短30%,並釋放出可出租的占地面積。新加坡建設局(BCA)預測,到2025年,模組化建築將在22%的住宅項目中得到應用,大多數開發商會指定使用高強度中空鋼型材以滿足生產力指標。寶鋼為深圳一座高層建築提供了8.5萬噸Q460/Q550鋼板,使工期縮短了六個月。 2024年國際建築規範(IBC)提高了ASTM A913 65級鋼材在抗震區域的允許應力限值,擴大了其在加州和日本的應用範圍。塔塔鋼鐵公司於2024年推出的S700MC鋼材,目標客戶是需要可在-40 度C以下溫度下保持夏比衝擊韌性的可焊接結構鋼的斯堪地那維亞模組化建築公司。

生產成本和合金元素成本上升

印尼對提煉鎳出口的限制,加上電池需求的激增,推動鎳價在2025年平均達到每噸18,500美元,較2024年上漲22%。南非的勞資糾紛擾亂了供應,導致鉻現貨價格飆升至每噸11,200美元,使不銹鋼和高抗張強度鋼的生產成本增加了10-15%。由於智利礦場因缺水而減產,鉬價一度達到每公斤45美元。安賽樂米塔爾透露,合金價格飆升已使其汽車用鋼業務的利潤率下降了180個基點,促使該公司每季與汽車製造商重新談判價格。東南亞的小型鋼廠正在推遲馬氏體鋼生產線的運作,直到合金市場穩定下來,導致產量成長放緩。

細分市場分析

雙相鋼預計在2025年將佔高抗張強度鋼市場規模的25.16%,並將在2031年之前以6.72%的複合年成長率成長。這主要歸功於其優異的成形性和600-1200兆帕的抗張強度,符合大多數碰撞安全標準。大眾汽車的MEB平台側樑和後地板橫樑採用DP 980鋼材,在滿足最新Euro NCAP側面碰撞標準的前提下,使車輛重量減輕了12%。

抗張強度超過1200 MPa的馬氏體和熱成型鋼在車門橫樑和電池外殼中的應用日益廣泛,但由於加工成本高且成形性有限,其應用仍面臨挑戰。局部雷射修整技術可以有效緩解這些問題。具有優異孔徑擴張比的複合相鋼板被用於承受多軸載荷的懸吊臂,而鐵素體和貝氏體鋼板則被用於重型卡車的底盤縱梁,因為焊接性能至關重要。硬化劈裂鋼目前仍處於試驗階段,但其2000 MPa的抗張強度和10%的延伸率表明,如果能夠解決規模化生產方面的難題,未來有望在整體成型門環中得到廣泛應用。

《高抗張強度鋼市場報告》依產品類型(雙相鋼、複合相鋼、馬氏體鋼等)、終端用戶產業(汽車及交通運輸、建築及施工、施工機械及採礦、航太及國防等終端用戶產業)及地區(亞太地區、北美地區、歐洲地區、南美地區、中東及非洲地區)進行細分。市場預測以噸為單位。

區域分析

預計亞太地區將成為高抗張強度鋼市場的主要驅動力,到2025年將佔據全球63.69%的市場。隨著電池式電動車產量的增加和基礎設施投資的擴大,預計到2031年,該地區將維持6.81%的複合年成長率。中國計劃在2025年生產940萬輛插電式混合動力汽車,並正在實施GB 38900-2020測試標準,引導汽車製造商採用雙相和熱成型解決方案。印度的「Bharatmala」計畫二期工程將新建12,000公里高速公路。日本和韓國正在引進1,800兆帕的壓鑄硬化門環,使混合動力轎車的重量減輕20%。同時,東南亞國協政府正在吸引中國和日本的汽車製造商,並推動區域捲材中心運作連續退火生產線。

在北美,美國的《通膨控制法》鼓勵國內採購,促使紐柯鋼鐵公司和克利夫蘭-克里夫斯公司擴建其連續退火設備,以供應滑板底盤所需的鋼坯。加拿大正在投資130億加幣(96億美元)用於電池製造,在工廠建設期間需要大量高抗張強度鋼樑和鋼板。墨西哥計劃在2025年生產380萬輛汽車,隨著跨國供應鏈轉向電動皮卡,每輛車的先進鋼材用量將高達280公斤。

在歐洲,碳邊境調節稅(CBAM)正在加速到廢鋼基電弧爐的轉型,旨在減少地下排放。德國汽車製造商正積極利用這項價值提案來實現其範圍3減排目標。英國離岸風力發電裝置容量已達16吉瓦,消耗大量S460/S500單樁鋼板。同時,法國已採用S690鋼材製造核能發電廠存儲殼,為核子反應爐建設帶來了高品質的鋼材需求。南美、中東和非洲的鋼材產量雖然小規模,但以兩位數的速度成長,這主要得益於巴西礦用卡車和沙烏地阿拉伯氫氣管道的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 車輛減重和碰撞安全法規

- 模組化高層建築的快速成長

- 離岸風力發電塔架建設的擴張正在加速需求成長。

- 適用於含氫高抗張強度鋼(HSS)的微量合金管路規範

- 電池驅動滑板底盤的普及

- 市場限制因素

- 生產成本和合金元素成本上升

- 原物料價格波動(鐵礦石、合金)

- 高強度鋼連接和焊接面臨的挑戰

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 供應分析

- 監理政策分析

- 貿易分析

第5章 市場規模與成長預測

- 依產品類型

- 兩相(DP)

- 複合相(CP)

- 馬氏體

- 鐵氧體貝氏體(FB)

- 熱成型(HF)

- 其他產品類型(例如,硬化鋼、分區(QandP))

- 按最終用戶行業分類

- 汽車和交通運輸

- 建築/施工

- 施工機械和採礦

- 航太/國防

- 其他終端用戶產業(例如可再生能源)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AM/NS India

- ArcelorMittal

- BlueScope

- China Baowu Steel Group Corp., Ltd.

- ChinaSteel

- CITIC Pacific Special Steel

- Cleveland-Cliffs Inc.

- Gerdau S/A

- HYUNDAI STEEL

- JFE Steel Corporation

- JSW Steel

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SSAB

- Tata Steel

- thyssenkrupp Steel Europe

- United States Steel Corporation

- Voestalpine AG

第7章 市場機會與未來展望

The High Strength Steel Market size is expected to grow from 12.27 Million tons in 2025 to 13.05 Million tons in 2026 and is forecast to reach 17.76 Million tons by 2031 at 6.36% CAGR over 2026-2031.

Automotive lightweighting mandates, modular high-rise construction, and offshore-wind tower build-outs are translating directly into larger order books for grades that couple tensile strengths above 600 MPa with high crash energy absorption. Dual-phase steel commands price premiums because its ferrite-martensite matrix preserves elongation during complex forming, a property automakers exploit for door inners and wheel-housing stampings. Hot-formed steel is scaling quickly in battery-electric chassis frames that must withstand side-impact tests while shielding lithium-ion modules from thermal runaway. At the same time, micro-alloyed ferritic-bainitic plate has emerged as the material of choice for hydrogen-ready pipelines, signalling a future growth node once large-diameter trunk lines move from pilot to commercial scale.

Global High Strength Steel Market Trends and Insights

Automotive Lightweighting and Crash-Safety Mandates

Fleet CO2 caps of 95 g/km in the European Union and a 54.5 miles-per-gallon target in the United States oblige automakers to swap mild steel for grades that remove 20-30% body-in-white mass while passing ever tougher small-overlap and side-impact tests. Updates to the Insurance Institute for Highway Safety protocol raised the bar for occupant survival space, which in turn lifted demand for 1,500 MPa B-pillars formed by hot stamping. General Motors reports that Ultium-based trucks now use dual-phase 980 MPa sheet in cab structures, trimming 180 kg from curb weight and raising torsional rigidity 15%. China's GB 38900-2020 test regimen couples side-pole impacts with roof-crush metrics, a combination that rewards martensitic and complex-phase steels in A- and B-pillar designs. Ford confirms that press-hardened steel battery enclosures satisfy Federal Motor Vehicle Safety Standard 305 without adding aluminum extrusions, simplifying under-body assembly.

Rapid Growth of Modular High-Rise Construction

Prefabricated steel modules allow contractors to cut inner-city build schedules by 30% because columns of S460-S690 grade carry identical loads at thinner wall thicknesses, freeing rentable floor space. Singapore's Building and Construction Authority states that modular starts rose to 22% of residential projects in 2025, and most developers specify high strength hollow sections to comply with productivity metrics. Baosteel supplied 85,000 tons of Q460/Q550 plate for Shenzhen towers that shaved six months off traditional timelines. The 2024 International Building Code permits higher stress limits for ASTM A913 Grade 65 in seismic zones, widening usage in California and Japan. Tata Steel's S700MC launch in 2024 targets Scandinavian modular firms that require weldable sections with Charpy toughness below -40 °C.

High Production and Alloying-Element Cost Inflation

Nickel averaged USD 18,500 per ton in 2025, 22% above 2024, after Indonesia tightened matte exports and battery demand surged. Chromium spot prices rose to USD 11,200 per ton when South African labor strikes disrupted supply, lifting stainless and high strength production costs 10-15%. Molybdenum reached USD 45 per kg as Chilean mines curtailed output amid water scarcity. ArcelorMittal disclosed a 180-basis-point margin squeeze in its automotive steel business due to alloy inflation, prompting quarterly price renegotiations with automakers. Southeast Asian mini-mills have postponed martensitic line start-ups until alloy markets stabilize, delaying incremental volume.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Tower Build-Out Accelerates Demand

- Hydrogen-Ready Pipeline Specifications for Micro-Alloyed HSS

- Joining and Welding Challenges for High-Strength Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dual-phase (DP) captured a 25.16% share of the high strength steel market size in 2025 and is forecast to advance at a 6.72% CAGR through 2031, benefiting from an attractive mix of formability and 600-1,200 MPa tensile strength that meets most crash-safety targets. Volkswagen's MEB platform uses DP 980 in side sills and rear floor cross-members, trimming vehicle mass 12% while satisfying latest Euro NCAP side-impact norms.

Martensitic and hot-formed grades above 1,200 MPa are expanding in door-intrusion beams and battery enclosures but incur higher processing costs and limited formability, issues mitigated by localized laser trimming. Complex-phase sheet with superior hole-expansion ratio wins suspension arms that experience multi-axial loads, while ferritic-bainitic plate secures chassis rails in heavy trucks that prioritize weldability. Quenched-and-partitioned steel remains pilot scale, yet its 2,000 MPa tensile strength plus 10% elongation profile signals future penetration in one-piece door rings once scaling challenges resolve.

The High Strength Steel Market Report is Segmented by Product Type (Dual-Phase, Complex Phase, Martensitic, and More), End-User Industry (Automotive and Transportation, Building and Construction, Yellow Goods and Mining, Aerospace and Defense, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominated the high strength steel market with 63.69% volume in 2025; rising battery-electric output and infrastructure spending will sustain a 6.81% CAGR to 2031. China built 9.4 million plug-in vehicles in 2025 and enforces GB 38900-2020 test norms that steer automakers toward dual-phase and hot-formed solutions. India's Bharatmala Phase II adds 12,000 km of highways. Japan and South Korea are introducing 1,800 MPa press-hardened door rings that cut mass by 20% in hybrid sedans, while ASEAN governments court Chinese and Japanese carmakers, pushing regional coil centers to commission continuous-annealing lines.

In North America, the U.S. Inflation Reduction Act incentivizes domestic sourcing, prompting Nucor and Cleveland-Cliffs to add continuous-annealing capacity to supply skateboard chassis blanks. Canada committed CAD 13 billion (USD 9.6 billion) to battery manufacturing that will absorb a large amount of high strength beams and plates during plant builds. Mexico produced 3.8 million vehicles in 2025, with per-unit advanced steel content up to 280 kg as cross-border supply chains pivot to electric pickups.

In Europe, Carbon Border Adjustment fees accelerate the switch to scrap-based electric-arc furnaces for lower embedded emissions, a value proposition German automakers embrace to meet scope-3 targets. Offshore-wind capacity in the United Kingdom reached 16 GW, consuming S460/S500 monopile plate, while France adopted S690 for nuclear containment shells, opening a high-grade opportunity in reactor builds. South America and the Middle-East and Africa clock smaller volumes yet post double-digit growth, anchored by Brazilian mining trucks and Saudi Arabian hydrogen pipelines.

- AM/NS India

- ArcelorMittal

- BlueScope

- China Baowu Steel Group Corp., Ltd.

- ChinaSteel

- CITIC Pacific Special Steel

- Cleveland-Cliffs Inc.

- Gerdau S/A

- HYUNDAI STEEL

- JFE Steel Corporation

- JSW Steel

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SSAB

- Tata Steel

- thyssenkrupp Steel Europe

- United States Steel Corporation

- Voestalpine AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive lightweighting and crash-safety mandates

- 4.2.2 Rapid growth of modular high-rise construction

- 4.2.3 Offshore-wind tower build-out accelerates demand

- 4.2.4 Hydrogen-ready pipeline specifications for micro-alloyed HSS

- 4.2.5 Battery-electric skateboard chassis adoption

- 4.3 Market Restraints

- 4.3.1 High production and alloying-element cost inflation

- 4.3.2 Raw-material price volatility (iron ore, alloys)

- 4.3.3 Joining and welding challenges for high-strength grades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Supply Analysis

- 4.7 Regulatory Policy Analysis

- 4.8 Trade Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Dual-Phase (DP)

- 5.1.2 Complex Phase (CP)

- 5.1.3 Martensitic

- 5.1.4 Ferritic-Bainitic (FB)

- 5.1.5 Hot-Formed (HF)

- 5.1.6 Other Product Types (Quenched and Partitioned (QandP), etc.)

- 5.2 By End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Yellow Goods and Mining

- 5.2.4 Aerospace and Defense

- 5.2.5 Other End-user Industries (Renewable Energy, etc.)

- 5.3 By Geography (Volume)

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacifc

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AM/NS India

- 6.4.2 ArcelorMittal

- 6.4.3 BlueScope

- 6.4.4 China Baowu Steel Group Corp., Ltd.

- 6.4.5 ChinaSteel

- 6.4.6 CITIC Pacific Special Steel

- 6.4.7 Cleveland-Cliffs Inc.

- 6.4.8 Gerdau S/A

- 6.4.9 HYUNDAI STEEL

- 6.4.10 JFE Steel Corporation

- 6.4.11 JSW Steel

- 6.4.12 LIBERTY Steel Group

- 6.4.13 NIPPON STEEL CORPORATION

- 6.4.14 Nucor Corporation

- 6.4.15 POSCO

- 6.4.16 SSAB

- 6.4.17 Tata Steel

- 6.4.18 thyssenkrupp Steel Europe

- 6.4.19 United States Steel Corporation

- 6.4.20 Voestalpine AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球先進高抗張強度鋼(AHSS)市場展望、詳細分析及至2032年預測

全球先進高抗張強度鋼(AHSS)市場展望、詳細分析及至2032年預測 先進鋼材和高強度合金市場預測至2034年-按產品類型、製造流程、應用、最終用戶和地區分類的全球分析高強度纖維材料市場:預測至2034年-按纖維類型、形狀、製造流程、應用、最終用戶和地區分類的全球分析

先進鋼材和高強度合金市場預測至2034年-按產品類型、製造流程、應用、最終用戶和地區分類的全球分析高強度纖維材料市場:預測至2034年-按纖維類型、形狀、製造流程、應用、最終用戶和地區分類的全球分析 先進高抗張強度鋼市場:按形狀、加工流程、等級、塗層類型、應用和分銷管道分類-2026-2032年全球市場預測

先進高抗張強度鋼市場:按形狀、加工流程、等級、塗層類型、應用和分銷管道分類-2026-2032年全球市場預測 造船用鋼市場規模、佔有率和成長分析:按鋼材產品類型、材質等級/規格、船舶應用、供應厚度和地區分類-2026-2033年產業預測

造船用鋼市場規模、佔有率和成長分析:按鋼材產品類型、材質等級/規格、船舶應用、供應厚度和地區分類-2026-2033年產業預測 全球高強度鋼市場:市場規模、佔有率和趨勢分析(按類型、應用和地區分類),細分市場預測(2026-2033 年)高強度鋼市場:依鋼種、塗層類型及終端用戶產業分類,全球預測(2026-2032年)

全球高強度鋼市場:市場規模、佔有率和趨勢分析(按類型、應用和地區分類),細分市場預測(2026-2033 年)高強度鋼市場:依鋼種、塗層類型及終端用戶產業分類,全球預測(2026-2032年) 高強度竹複合材料市場分析與預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形式、製程、安裝類型、解決方案

高強度竹複合材料市場分析與預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形式、製程、安裝類型、解決方案 全球高強度鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球高強度鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 超高強度鋼市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用戶產業、地區及競爭格局分類,2021-2031年)

超高強度鋼市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用戶產業、地區及競爭格局分類,2021-2031年)