|

市場調查報告書

商品編碼

2044089

模擬半導體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Analog Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

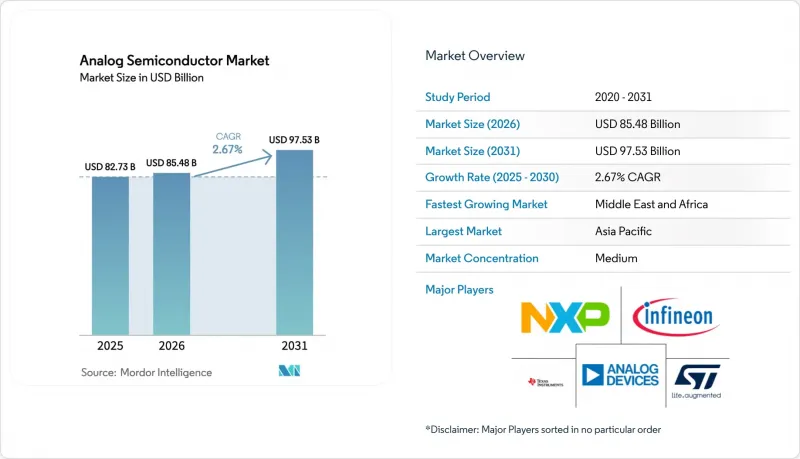

模擬半導體市場預計將從 2026 年的 854.8 億美元成長到 2031 年的 975.3 億美元,2026 年至 2031 年的複合年成長率為 2.67%。

預計出貨量將從2026年的2,447.3億顆增加至2031年的3,428.8億顆,複合年成長率(CAGR)為6.98%。在通用型晶片持續面臨價格壓力的情況下,銷售成長與營收成長之間的差距將進一步擴大。儘管專用類比IC在2025年仍保持著可觀的銷售基礎,但邊緣運算和工廠自動化硬體日益標準化,正促使許多新設計轉向通用型組件,從而加劇了整個產品系列的競爭。亞太地區的製造商佔據了全球近一半的需求,這主要得益於氮化鎵(GaN)快速充電生態系統的推動。同時,中東地區的國防相關計畫也為抗輻射前端創造了豐厚的商機。同時,德克薩斯州和德勒斯登 300 毫米晶圓廠產能的提升旨在緩解長期存在的晶圓供應瓶頸,但對於依賴外部代工廠的無廠半導體公司而言,短期供應不穩定的風險仍然存在。

全球模擬半導體市場趨勢與洞察

快速充電適配器在亞洲智慧型手機生態系統中的普及

亞洲行動電話製造商計劃在2025年前實現USB-PD 3.1和專有的65W-240W快充協議的標準化。這項轉變需要採用具有更高開關頻率和更低發熱量的氮化鎵(GaN)電源管理IC。 Navitas為這些轉接器出貨超過1億顆GaN元件,而瑞薩電子則透過整合式USB-C控制器和GaN閘極驅動器,將外部元件數量減少了五分之一。本地二級OEM廠商迅速接受了元件成本的降低,加快了設計週期,並進一步鞏固了亞太地區在模擬半導體市場的主導地位。

北美工業IoT的普及推動了對高精度資料轉換器的需求。

預計到2025年,美國工廠將部署超過1,500萬個物聯網感測器節點,每個節點都需要一個16位元或更高精度的類比數位轉換器(ADC),且雜訊基底需達到微伏特。 ADI公司的多感測器前端減少了40%的分立元件數量,而德州儀器(德克薩斯)則提供了支援40kHz取樣率的Delta-Σ轉換器,用於振動分析。由此帶來的需求成長推動了目錄產品的銷售,使得高精度轉換器在模擬半導體市場中始終處於高階價格區間。

300mm晶圓廠產能瓶頸限制了PMIC的供應。

儘管德克薩斯和全球晶圓代工廠都新增了生產線,但台積電仍將其大部分300毫米製程設備用於生產先進邏輯晶片,而傳統製程的模擬晶片產能仍然過剩。 2025年下半年,前置作業時間超過20週,由於積體電路製造商將晶圓轉用於自身需求,汽車專案出現了嚴重的供不應求。這種產能緊張的局面持續限制著大批量電源管理積體電路的生產,減緩了模擬半導體市場的短期擴張。

細分市場分析

儘管通用積體電路預計在2025年僅佔銷售額的一小部分,但其複合年成長率預計將達到6.52%,這主要得益於其與主導工業自動化領域的模組化硬體平台的兼容性。隨著原始設備製造商(OEM)採用現成組件將開發週期縮短數月,與這些目錄產品(例如放大器和比較器)相關的類比半導體市場規模也將隨之擴大。

到2025年,專用積體電路(ASIC)仍將佔銷售額的45.71%,但隨著客製化ASIC專案需要更長的檢驗週期,其成長預計將會放緩。汽車電池管理ASIC和5G射頻前端表明,客製化類比元件在大規模生產領域仍然至關重要,但隨著可配置目錄產品性能的提升,它們在模擬半導體市場的佔有率將逐漸趨於正常化。工業ASIC旨在承受嚴苛環境,安森美半導體的Treo平台整合了用於碳化矽(SiC)牽引逆變器的隔離式閘極驅動器和電流偵測功能。

受醫療和工業終端高精度感測需求的推動,運算放大器預計將以 5.83% 的複合年成長率成長。具有微伏特失調電壓的高階擴大機保持著較高的平均售價,並持續為訊號調理元件的類比半導體市場貢獻價值。 ADI 公司的 AD7380 是一款 16 位元逐次逼近型 ADC,整合了電壓基準,無需外部高精度電阻,從而減少了 30% 的印刷基板面積。

電源管理組件預計到2025年將佔據29.83%的市場佔有率,但由於智慧型手機和筆記型電腦OEM廠商的採購能力增強,其價格正面臨更大幅度的下降。同時,高解析度轉換器和高可靠性介面收發器受益於更嚴格的電磁相容性(EMC)標準,儘管晶圓成本不斷上漲,但仍能保持穩定的利潤率。二極體和電晶體在靜電放電(ESD)保護和負載切換方面發揮重要作用,但隨著整合解決方案市場佔有率的成長,預計到2025年,分立元件的出貨量將年減5%。

區域分析

亞太地區繼續保持其作為模擬半導體市場中心的地位,預計到2025年將佔全球銷售額的45.72%。中國、日本和韓國的供應鏈正在消化智慧型手機、汽車功率模組和5G無線設備所需的大量類比半導體。政府獎勵,例如中國3,440億元人民幣(約470億美元)的國家積體電路基金和日本的設備稅額扣抵,正在支持當地產能擴張並增強區域自主性。印度的半導體獎勵計畫也吸引了模擬半導體晶圓廠的提案,但由於監管核准需要超過24個月的時間,預計產能擴張將延後到2027年。

預計到2031年,中東地區將以7.02%的複合年成長率實現最高增速,這主要得益於國防機構對航空電子設備和衛星有效載荷的現代化改造。阿拉伯聯合大公國和沙烏地阿拉伯的努力促使兩國投資建造專門從事抗輻射加固前端的設計中心,從而在模擬半導體市場中創造了一個高階細分領域。

北美約佔全球銷售額的四分之一,其中《晶片法案》(CHIPS Act)提供的390億美元津貼促進了北美晶圓生產。歐洲緊隨其後,約佔五分之一,歐盟《晶片法案》提供了430億歐元(469億美元)的援助。南美和非洲合計佔比不到10%,但汽車和離網能源系統領域的需求較為集中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐洲48V輕度混合動力車電氣化進程迅速推進

- 快速充電電源適配器在亞洲智慧型手機生態系統中的普及

- 北美工業IoT的普及推動了對高精度資料轉換器的需求成長。

- 5G基礎設施的部署將擴大東亞地區對射頻類比IC的需求。

- 中東地區國防現代化進程的加速推動了對耐輻射模擬元件的採購。

- AI加速的邊緣設備需要超低功耗的資料擷取IC。

- 市場限制因素

- 300mm晶圓廠產能瓶頸限制了PMIC的供應。

- 模擬晶圓代工價格波動

- 延長小眾汽車專用積體電路的商業化時間:設計引進週期

- 東南亞假冒被動元件損害了可靠性

- 價值鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模及成長預測(價值及數量)

- 按設備類型(數量和金額)

- 通用類比IC

- 放大器和比較器

- 介面

- 電源管理

- 訊號轉換

- 用於特定應用的類比類比IC

- 車

- 溝通

- 電腦

- 消費者

- 產業

- 通用類比IC

- 按組件

- 電阻器

- 電容器

- 電感器

- 二極體

- 電晶體

- 運算放大器

- 按晶圓尺寸

- 200 mm

- 300 mm

- 其他尺寸

- 按最終用戶行業分類

- 家用電子電器

- 資訊科技和通訊

- 汽車和交通運輸

- 工業和製造業

- 醫療設備

- 航太/國防

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Texas Instruments Inc.

- Analog Devices Inc.

- STMicroelectronics NV

- Infineon Technologies AG

- NXP Semiconductors NV

- onsemi

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Rohm Co., Ltd.

- Skyworks Solutions Inc.

- Cirrus Logic Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems Inc.

- Diodes Incorporated

- Vicor Corp.

- Power Integrations Inc.

- Semtech Corp.

- Qorvo Inc.

- Allegro MicroSystems Inc.

- Vishay Intertechnology Inc.

- Maxim Integrated Products Inc.

- Richtek Technology Corp.

- Broadcom Inc.

- Tower Semiconductor Ltd.

- AnalogicTech Corp.

- Nordic Semiconductor ASA(Analog Front-End ICs)

- Alpha & Omega Semiconductor Ltd.

- Silergy Corp.

第7章 市場機會與未來展望

The analog semiconductor market size is expected to increase from USD 85.48 billion in 2026 to USD 97.53 billion by 2031, growing at a CAGR of 2.67% over 2026-2031. Volume shipments will climb from 244.73 billion units in 2026 to 342.88 billion units by 2031, a 6.98% CAGR that widens the gap between unit and revenue growth as price pressure persists in commodity categories. Application-specific analog ICs retained a sizeable revenue base in 2025, yet rising standardization in edge-computing and factory-automation hardware is steering many new designs toward general-purpose parts, tightening competitive dynamics across catalog portfolios. Asia-Pacific manufacturers account for almost half of global demand, propelled by gallium-nitride fast-charging ecosystems, while defense-driven projects in the Middle East create premium opportunities for radiation-hardened front-ends. Simultaneously, 300 mm fab ramps in Texas and Dresden aim to relieve long-standing wafer bottlenecks, but near-term allocation risk remains for fabless suppliers that depend on external foundries.

Global Analog Semiconductor Market Trends and Insights

Proliferation Of Fast-Charging Power Adapters In Asian Smartphone Ecosystems

Asian handset makers standardized USB-PD 3.1 and proprietary 65 W-240 W fast-charge protocols in 2025, a shift that required gallium-nitride power management ICs with higher switching frequencies and reduced thermal budgets. Navitas shipped more than 100 million GaN devices into these adapters, while Renesas integrated USB-C controllers and GaN gate drivers to cut external components by one-fifth. Local tier-two OEMs quickly embraced the lower bill-of-materials cost, accelerating design cycles and reinforcing Asia-Pacific's dominance within the analog semiconductor market.

Industrial IoT Adoption Elevating Demand For High-Precision Data Converters In North America

Factories across the United States deployed over 15 million IoT sensor nodes in 2025, each calling for 16-bit-plus ADCs with microvolt-level noise floors. Analog Devices' multisensor front-ends trimmed discrete counts by 40%, and Texas Instruments delivered delta-sigma converters supporting 40 kHz sampling for vibration analytics. The resulting demand uplift bolsters catalog revenues and keeps high-accuracy converters at premium price points within the analog semiconductor market.

300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

Texas Instruments and GlobalFoundries added new lines, yet TSMC still allocates most 300 mm tools to advanced logic, leaving analog runs on legacy nodes oversubscribed. Lead times stretched beyond 20 weeks in late 2025 and automotive programs felt acute shortages as integrated device manufacturers diverted wafers to in-house needs. The tight capacity continues to restrain output of high-volume power-management ICs, tempering near-term expansion in the analog semiconductor market.

Other drivers and restraints analyzed in the detailed report include:

- Roll-Out Of 5G Infrastructure Amplifying RF Analog IC Demand In East Asia

- AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- Volatility In Analog Wafer-Foundry Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General-purpose ICs accounted for modest revenue in 2025 yet are projected to lead growth at a 6.52% CAGR, reflecting their fit with modular hardware platforms that dominate industrial automation. The analog semiconductor market size tied to these catalog amplifiers and comparators will expand as OEMs adopt off-the-shelf parts to shave months from development schedules.

Application-specific designs, while still responsible for 45.71% revenue in 2025, face slower gains as custom ASIC projects require longer validation windows. Automotive battery-management ASICs and 5G RF front-ends illustrate how high-volume sectors will keep bespoke analog relevant, but their share of the analog semiconductor market will gradually normalize as configurable catalog alternatives improve performance envelopes. Industrial ASICs address harsh environments, with onsemi's Treo platform integrating isolated gate drivers and current sensing for silicon carbide traction inverters

Operational amplifiers are forecast to post a 5.83% CAGR, driven by precision sensing in medical and industrial endpoints. Premium amplifiers with microvolt offset voltages sustain higher average selling prices, preserving value contribution within the analog semiconductor market size for signal-conditioning devices. Analog Devices' AD7380, a 16-bit successive-approximation ADC with integrated voltage reference, eliminates external precision resistors and reduces printed circuit board area by 30%.

Power-management parts, holding 29.83% share in 2025, confront steeper price erosion because smartphone and notebook OEMs wield greater purchasing leverage. Conversely, high-resolution converters and rugged interface transceivers benefit from tighter electromagnetic-compatibility standards, helping stabilize margins despite rising wafer costs. Diodes and transistors serve niche roles in electrostatic discharge protection and load switching, yet discrete shipments declined 5% year-over-year in 2025 as integrated solutions gained share.

The Analog Semiconductor Market Report is Segmented by Device Type (General Purpose Analog IC and Application-Specific Analog IC), Component (Resistors, Capacitors, Inductors, and More), Wafer Size (200mm, 300mm, and More), End-User Industry (Consumer Electronics, IT and Telecom, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the center of gravity for the analog semiconductor market, accounting for 45.72% of revenue in 2025. Supply ecosystems in China, Japan, and South Korea absorb high-volume analog for smartphones, automotive power modules, and 5G radios. Government incentives such as China's CNY 344 billion (USD 47 billion) National IC Fund and Japan's equipment tax credits underpin local capacity expansions, reinforcing regional self-reliance. India's semiconductor incentive program attracted proposals for analog fabs, yet regulatory approvals extended beyond 24 months, delaying capacity additions until 2027.

The Middle East is projected to chart the fastest CAGR of 7.02% through 2031 as defense agencies modernize avionics and satellite payloads. United Arab Emirates and Saudi Arabia initiatives funnel capital into design centers that specialize in radiation-tolerant front-ends, carving out a premium sub-segment within the analog semiconductor market.

North America accounts for roughly one-quarter of global revenue, with CHIPS Act grants totaling USD 39 billion catalyzing domestic wafer production. Europe follows at nearly one-fifth share, supported by the EUR 43 billion (USD 46.9 billion) EU Chips Act, while South America and Africa collectively represent less than 10% yet display selective uptake in automotive and off-grid energy systems.

List of Companies Covered in this Report:

- Texas Instruments Inc.

- Analog Devices Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- onsemi

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Rohm Co., Ltd.

- Skyworks Solutions Inc.

- Cirrus Logic Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems Inc.

- Diodes Incorporated

- Vicor Corp.

- Power Integrations Inc.

- Semtech Corp.

- Qorvo Inc.

- Allegro MicroSystems Inc.

- Vishay Intertechnology Inc.

- Maxim Integrated Products Inc.

- Richtek Technology Corp.

- Broadcom Inc.

- Tower Semiconductor Ltd.

- AnalogicTech Corp.

- Nordic Semiconductor ASA (Analog Front-End ICs)

- Alpha & Omega Semiconductor Ltd.

- Silergy Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge in 48 V Mild-Hybrid Vehicles Across Europe

- 4.2.2 Proliferation of Fast-Charging Power Adapters in Asian Smartphone Ecosystems

- 4.2.3 Industrial IoT Adoption Elevating Demand for High-Precision Data Converters in North America

- 4.2.4 Roll-Out of 5 G Infrastructure Amplifying RF Analog IC Demand in East Asia

- 4.2.5 Escalating Defense Modernization Driving Radiation-Hardened Analog Procurement in the Middle East

- 4.2.6 AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- 4.3 Market Restraints

- 4.3.1 300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

- 4.3.2 Volatility in Analog Wafer-Foundry Pricing

- 4.3.3 Design-In Cycles Stretching Time-to-Revenue for Niche Automotive ASICs

- 4.3.4 Counterfeit Passive Components Undermining Reliability in South-East Asia

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Device Type (Value and Volume)

- 5.1.1 General Purpose Analog IC

- 5.1.1.1 Amplifiers and Comparators

- 5.1.1.2 Interface

- 5.1.1.3 Power Management

- 5.1.1.4 Signal Conversion

- 5.1.2 Application-Specific Analog IC

- 5.1.2.1 Automotive

- 5.1.2.2 Communications

- 5.1.2.3 Computer

- 5.1.2.4 Consumer

- 5.1.2.5 Industrial

- 5.1.1 General Purpose Analog IC

- 5.2 By Component (Value)

- 5.2.1 Resistors

- 5.2.2 Capacitors

- 5.2.3 Inductors

- 5.2.4 Diodes

- 5.2.5 Transistors

- 5.2.6 Operational Amplifiers

- 5.3 By Wafer Size (Value)

- 5.3.1 200 mm

- 5.3.2 300 mm

- 5.3.3 Other Sizes

- 5.4 By End-User Industry (Value)

- 5.4.1 Consumer Electronics

- 5.4.2 IT and Telecom

- 5.4.3 Automotive and Transportation

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Healthcare Devices

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Analog Devices Inc.

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Infineon Technologies AG

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 onsemi

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Rohm Co., Ltd.

- 6.4.10 Skyworks Solutions Inc.

- 6.4.11 Cirrus Logic Inc.

- 6.4.12 Silicon Laboratories Inc.

- 6.4.13 Monolithic Power Systems Inc.

- 6.4.14 Diodes Incorporated

- 6.4.15 Vicor Corp.

- 6.4.16 Power Integrations Inc.

- 6.4.17 Semtech Corp.

- 6.4.18 Qorvo Inc.

- 6.4.19 Allegro MicroSystems Inc.

- 6.4.20 Vishay Intertechnology Inc.

- 6.4.21 Maxim Integrated Products Inc.

- 6.4.22 Richtek Technology Corp.

- 6.4.23 Broadcom Inc.

- 6.4.24 Tower Semiconductor Ltd.

- 6.4.25 AnalogicTech Corp.

- 6.4.26 Nordic Semiconductor ASA (Analog Front-End ICs)

- 6.4.27 Alpha & Omega Semiconductor Ltd.

- 6.4.28 Silergy Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

模擬半導體市場機會、成長要素、產業趨勢分析及2026-2035年預測。

模擬半導體市場機會、成長要素、產業趨勢分析及2026-2035年預測。 模擬半導體市場:按類型、組件、封裝尺寸、產業、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

模擬半導體市場:按類型、組件、封裝尺寸、產業、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 2026-2030年全球模擬半導體市場

2026-2030年全球模擬半導體市場 仿生半導體機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、功能、最終用戶分類

仿生半導體機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、功能、最終用戶分類 模擬半導體市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件、產業垂直領域、地區和競爭格局分類,2021-2031年

模擬半導體市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件、產業垂直領域、地區和競爭格局分類,2021-2031年 模擬半導體市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)

模擬半導體市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034) 模擬半導體市場:按產品類型、技術、應用和地區分類

模擬半導體市場:按產品類型、技術、應用和地區分類 模擬半導體市場規模、佔有率和成長分析(按類型、組件、外形規格、最終用途和地區分類)—產業預測(2026-2033 年)

模擬半導體市場規模、佔有率和成長分析(按類型、組件、外形規格、最終用途和地區分類)—產業預測(2026-2033 年) 2032 年全球模擬半導體市場分析與預測:按產品類型、材料、應用、最終用戶和地區全球模擬半導體市場:未來預測(2025-2030)

2032 年全球模擬半導體市場分析與預測:按產品類型、材料、應用、最終用戶和地區全球模擬半導體市場:未來預測(2025-2030)