|

市場調查報告書

商品編碼

2044081

網站寄存:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Web Hosting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

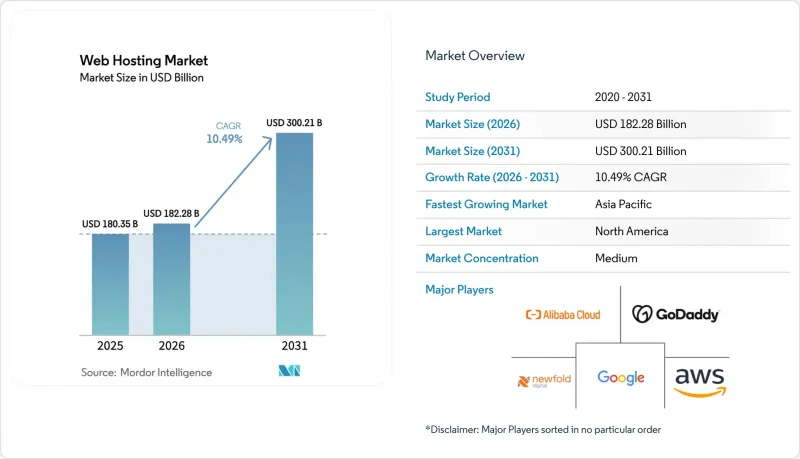

2025 年網站寄存市場價值 1803.5 億美元,預計到 2031 年將達到 3002.1 億美元,而 2026 年為 1822.8 億美元,預測期(2026-2031 年)複合年成長率為 10.49%。

隨著生成式人工智慧工作負載的日益普及,企業正遷移到傳統共用伺服器無法處理的、支援GPU的邊緣基礎架構。歐盟、印度和中國的資料居住法規正在加速混合部署的進程,企業將應用程式分佈在本地、主權雲端和超大規模雲端。在無程式碼平台上推出數位商店的小規模企業要求99.99%的運轉率,這促使他們將支出轉向雲端服務和託管WordPress方案。基本的運轉率保證如今已成為必備條件,因此服務提供者正透過捆綁可觀測性工具和碳中和認證來展開競爭。

全球網站寄存市場趨勢與洞察

中小企業電子商務的爆炸性成長。

到2024年底,全球將有460萬家企業使用無代碼電商平台,迫使服務供應商提供能夠應對限時搶購流量的彈性基礎設施。小規模零售商現在期望獲得包含PCI-DSS掃描和整合付款閘道的捆綁式解決方案,其價值也從單純的伺服器容量轉向提供隨時可用的線上店鋪環境。將託管功能整合到端到端電商套件中的服務供應商正在贏得那些沒有專門DevOps負責人的企業的市場佔有率。在東南亞,跨境電商需要邊緣資料中心來將延遲保持在100毫秒以下,這加速了區域資料中心的部署。月度訂閱合約提高了零售商的靈活性,但也增加了託管服務提供者的客戶流失風險,促使他們投資於預測性客戶維繫工具。

對高可用性和低延遲網站的需求激增。

金融監管機構現已將數位管道運作列為合規指標,歐洲銀行管理局 (EBA) 強制要求銀行的可用性達到 99.95%。影片串流媒體、即時遊戲和遠端醫療依賴用戶 50 公里半徑範圍內的邊緣快取,而只有超大規模資料中心業者和成熟的 CDN 供應商才能大規模提供這種能力。無伺服器運算的興起使全球分散式執行成為常態,消除了單一區域來源伺服器造成的瓶頸。與自動駕駛汽車和工業IoT相關的對延遲敏感的工作負載需要整合 5G 的邊緣託管,而傳統的共同託管難以彌補這一差距。能夠即時顯示延遲和錯誤率的可觀測性儀表板正成為超越基本運轉率保證的差異化優勢。

雲端認證託管工程師嚴重短缺

根據領英(LinkedIn)的報告,到2025年,雲端架構技能的需求將超過供應的2.3倍。超過15萬美元的年薪中位數正吸引來自託管服務供應商、金融科技公司和SaaS獨角獸企業的工程師。人手不足的團隊正在延誤客戶期待的自動化項目,而持續數月的技能提升計劃可能收效甚微。遠距辦公正在縮小傳統的薪資差距,而招募週期也在延長,因為僅憑學歷已不足以保證勝任能力。

細分市場分析

共同託管在2025年佔總營收的37.28%,但隨著入門級用戶也紛紛遷移到提供自動擴展和強大安全性的雲端平台,這一細分市場正在萎縮。雲端主機預計將以10.53%的年成長率成長,並預計在2031年佔據網路主機市場的重要佔有率。 VPS和獨立主機則在需要root權限的開發人員和需要單一租用戶硬體的受監管產業中佔有一席之地。託管服務吸引了那些希望外包設施運作但又想維持實體控制權的公司。託管WordPress方案捆綁了快取和測試環境,使機構能夠專注於內容而非基礎設施。

2024年至2025年間,隨著服務供應商逐步淘汰基於cPanel的方案並優先發展Kubernetes編配的雲端平台,向雲端遷移的趨勢加速發展。多重雲端成為主流,78%的企業在至少兩家供應商的伺服器上運行工作負載,這反映出企業為避免被單一供應商鎖定而採取的策略性舉措。託管型WordPress服務供應商目前正在添加無頭CMS功能,允許客戶將靜態資源推送到邊緣網路,從而縮短頁面載入時間,並將網站寄存市場擴展到現代Jamstack工作流程。

儘管到2025年,公共雲端仍將佔總支出的45.58%,但隨著合規性要求推動工作負載分散化,混合雲和多重雲端環境預計將在2031年之前以10.75%的複合年成長率成長。這種轉變將擴大混合解決方案在資料位置法規嚴格的地區的網路託管市場佔有率。在強制要求實體隔離的環境中,私有雲端仍然至關重要,但託管的私有服務正在模糊專用環境和多租戶環境之間的界限。

管理混合環境需要身份同步、資料庫複製和一致的標籤。 Kubernetes 提供了可移植性,而 FinOps 團隊則最佳化了在不進行任何更改的情況下遷移始終線上運作時產生的成本激增。敏感運算(Intel SGX、AMD SEV、ARM TrustZone)的興起使得混合部署成為可能,即使在處理過程中,敏感資料也始終保持加密狀態,從而解決了以往迫使處理個人識別資訊 (PII) 的工作負載部署在本地的監管問題。

區域分析

北美地區憑藉高密度超大規模資料中心叢集和企業對雲端運算的早期採用,預計到2025年將佔全球營收的38.63%。儘管隨著該地區接近飽和,成長速度有所放緩,但主權雲和專用於人工智慧的GPU集群的多樣化發展仍在維持投資。南美洲的託管需求集中在巴西和阿根廷,這兩個國家的通貨膨脹波動和貨幣貶值迫使服務提供者使用美元作為合約貨幣,並實施根據外匯波動每月調整的動態定價。

亞太地區預計將以10.93%的複合年成長率成長,這主要得益於印度數位支付的日益普及。在印度,UPI交易量在2024年突破了1000億筆。印尼和越南的金融科技公司正在雅加達和胡志明市部署低延遲節點,以符合當地法規。像Telehouse這樣的供應商將在2024年新增15個資料中心,將主要都會地區的往返延遲從180毫秒降低到50毫秒以下。

在歐洲,需要在GDPR的詳細要求和規模需求之間取得平衡。 OVHcloud和Hetzner等區域性公司正在推廣區域資料存儲,而AWS則在2024年推出了獨立的「歐洲主權雲端」來應對這項挑戰。中東和非洲是新興市場,行動網際網路普及率高(阿拉伯聯合大公國和沙烏地阿拉伯的智慧型手機普及率超過80%),這推動了對高延遲和不穩定蜂巢式網路最佳化的託管服務的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 中小企業電子商務的爆炸性成長。

- 對高可用性和低延遲網站的需求激增。

- 快速過渡到混合/多重雲端架構

- 透過碳中和綠色託管實現差異化

- 對具備生成式人工智慧功能的邊緣伺服器和GPU伺服器的需求激增

- 市場限制因素

- 雲端認證託管工程師嚴重短缺

- 網路攻擊日益加劇,資料主權監管也日益嚴格。

- 零價格競爭會對利潤率造成壓力。

- 能源價格波動和電廠投資通膨

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 永續發展舉措和綠色主機代管舉措

第5章 市場規模與成長預測

- 按主機類型

- 共同託管

- 虛擬專用伺服器 (VPS) 主機

- 專用主機

- 雲端託管

- 託管主機

- 託管式 WordPress 主機

- 經銷商主機

- 其他主機類型

- 部署模式

- 公共雲端

- 私有雲端

- 混合/多重雲端

- 按最終用戶行業分類

- 大公司

- 中小企業

- 個人部落客與創作者

- 軟體開發商和SaaS新創公司

- 透過使用

- 公開訪問的網站

- 電子商務商店

- Web應用程式

- 行動應用程式和API

- SaaS/PaaS平台

- 其他用途

- 定價模式

- 訂閱(定期合約)

- 計量型/付費使用制

- 分級(使用等級)

- 免費增值模式與廣告收入模式

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services

- Google LLC

- Microsoft Corporation

- GoDaddy Inc.

- Newfold Digital

- Alibaba Cloud

- Tencent Cloud

- Liquid Web LLC

- DigitalOcean

- OVH Groupe SA

- Hetzner Online GmbH

- WP Engine

- 1and1 IONOS

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting LLC

- Kinsta Inc.

- DreamHost LLC

- GreenGeeks LLC

- InMotion Hosting Inc.

- The Constant Company LLC

- Namecheap Inc.

- HostGator LLC

第7章 市場機會與未來展望

The Web Hosting market size was valued at USD 180.35 billion in 2025 and estimated to grow from USD 182.28 billion in 2026 to reach USD 300.21 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Ongoing adoption of generative AI workloads is steering enterprises toward GPU-ready edge infrastructure that legacy shared servers cannot support. Data-residency rules in the European Union, India, and China are accelerating hybrid deployments as firms distribute applications across on-premise, sovereign, and hyperscale clouds. Small merchants launching digital storefronts on no-code platforms are demanding 99.99% uptime, which is shifting spend toward cloud and managed WordPress tiers. Providers now compete on bundled observability tools and carbon-neutral credentials because basic uptime promises have become table stakes.

Global Web Hosting Market Trends and Insights

Explosive E-Commerce Expansion Among SMEs

No-code commerce platforms counted 4.6 million global merchants in late 2024, forcing providers to deliver elastic infrastructure that can absorb flash-sale traffic. Micro-retailers now expect bundles with PCI-DSS scans and integrated payment gateways, so value is shifting from raw server capacity to turnkey storefront enablement. Providers that embed hosting inside end-to-end commerce suites gain share among merchants lacking DevOps staff. Cross-border shopping in Southeast Asia requires edge points of presence to keep latency under 100 milliseconds, encouraging regional data-center rollouts. Monthly subscription contracts improve agility for retailers but raise churn risk for hosts, prompting investment in predictive-retention tooling.

Surging Demand for High-Availability and Low-Latency Sites

Financial regulators now classify digital-channel uptime as a compliance metric; European Banking Authority rules mandate 99.95% availability for banks. Video streaming, real-time gaming and tele-medicine rely on edge caching within 50 kilometers of users, which only hyperscalers and mature CDN operators can supply at scale. The rise of serverless computing has normalized globally distributed execution, removing the bottleneck of single-region origin servers. Latency-sensitive workloads tied to autonomous vehicles and industrial IoT require 5G-integrated edge hosting, a gap that traditional shared hosts struggle to bridge. Observability dashboards exposing latency and error rates in real time have become differentiators more than basic uptime guarantees.

Acute Shortage of Cloud-Certified Hosting Engineers

LinkedIn reported demand for cloud architecture skills outpacing supply by 2.3 times in 2025. Median salaries above USD 150,000 tempt engineers to move from hosting vendors to fintechs and SaaS unicorns. Under-staffed teams delay automation projects that customers expect, while multi-month reskilling programs carry uncertain returns. Remote work narrows traditional wage arbitrage, and credentials alone no longer guarantee competence, lengthening hiring cycles.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Migration to Hybrid and Multi-Cloud Architectures

- Carbon-Neutral Green Hosting Differentiation

- Escalating Cyber-Attacks and Data-Sovereignty Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shared hosting controlled 37.28% revenue in 2025 yet the segment is losing ground as even entry-level users migrate to cloud platforms offering auto-scaling and stronger security. Cloud hosting is forecast to grow at 10.53% and is expected to command a sizeable share of the Web Hosting market size by 2031. VPS and dedicated hosting hold niche positions among developers wanting root access and regulated industries needing single-tenant hardware. Colocation attracts firms retaining physical control while outsourcing facilities operations. Managed WordPress tiers bundle caching and staging, enabling agencies to focus on content rather than infrastructure.

The shift toward cloud accelerated in 2024-2025 as providers deprecated cPanel-based plans in favor of Kubernetes-orchestrated stacks. Multi-cloud became mainstream with 78% of enterprises running workloads across at least two vendors, reflecting strategic avoidance of lock-in. Managed WordPress players now add headless CMS features so clients can push static assets to edge networks, shrinking page-load times and extending the Web Hosting market reach into modern Jamstack workflows.

Public cloud still accounts for 45.58% of 2025 spend; however, hybrid and multi-cloud environments are projected to grow at a 10.75% CAGR through 2031 as compliance requirements drive workload distribution. This shift will increase the Web Hosting market share of hybrid solutions in regions that enforce strict data-location laws. Private cloud remains relevant where physical isolation is mandated, though hosted private services blur the line between dedicated and multitenant.

Managing hybrid estates demands synchronized identity, replicated databases, and consistent tagging. Kubernetes delivers portability, while FinOps teams optimize cost spikes that occur when always-on workloads migrate unmodified. The rise of confidential computing-Intel SGX, AMD SEV, ARM TrustZone-enables hybrid deployments where sensitive data remains encrypted even during processing, addressing regulatory concerns that previously forced on-premise deployment of workloads handling personally identifiable information.

The Web Hosting Market is Segmented by Hosting Type (Shared Hosting, Virtual Private Server Hosting, and More), Deployment Mode (Public Cloud, Private Cloud, and More), End-User Vertical (Large Enterprises, Small and Medium-Sized Enterprises, and More), Application (Public Websites, and More), Pricing Model (Subscription, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.63% of 2025 revenue, supported by dense hyperscale data-center clusters and early enterprise cloud adoption. Growth is moderating as the region approaches saturation, yet sovereign-cloud variants and AI-specific GPU farms sustain investment. outh America's hosting demand concentrates in Brazil and Argentina, where inflation volatility and currency devaluation force providers to denominate contracts in U.S. dollars and implement dynamic pricing that adjusts monthly based on exchange-rate fluctuations.

Asia-Pacific is projected to expand at a 10.93% CAGR, underpinned by the proliferation of digital payments in India, where UPI volumes crossed 100 billion transactions in 2024. Indonesian and Vietnamese fintechs deploy low-latency nodes in Jakarta and Ho Chi Minh City to comply with national regulations. Edge expansions by providers such as Telehouse added 15 data centers in 2024, cutting round-trip latency from 180 milliseconds to under 50 milliseconds in key metros.

Europe balances GDPR nuances with the need for scale. Regional companies such as OVHcloud and Hetzner promote in-region data storage, while AWS responded in 2024 with an isolated European Sovereign Cloud. Middle East and Africa represent nascent markets where mobile-first internet adoption-smartphone penetration exceeds 80% in UAE and Saudi Arabia-drives demand for hosting optimized for cellular networks with high latency and intermittent connectivity.

List of Companies Covered in this Report:

- Amazon Web Services

- Google LLC

- Microsoft Corporation

- GoDaddy Inc.

- Newfold Digital

- Alibaba Cloud

- Tencent Cloud

- Liquid Web LLC

- DigitalOcean

- OVH Groupe SA

- Hetzner Online GmbH

- WP Engine

- 1and1 IONOS

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting LLC

- Kinsta Inc.

- DreamHost LLC

- GreenGeeks LLC

- InMotion Hosting Inc.

- The Constant Company LLC

- Namecheap Inc.

- HostGator LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Explosive E-Commerce Expansion Among SMEs

- 4.1.2 Surging Demand For High-Availability and Low-Latency Sites

- 4.1.3 Rapid Migration To Hybrid/Multi-Cloud Architectures

- 4.1.4 Carbon-Neutral Green Hosting Differentiation

- 4.1.5 Gen-AI-Ready Edge and GPU Server Demand Surge

- 4.2 Market Restraints

- 4.2.1 Acute Shortage of Cloud-Certified Hosting Engineers

- 4.2.2 Escalating Cyber-Attacks and Data-Sovereignty Regulation

- 4.2.3 Margin Pressure From Race-To-Zero Pricing

- 4.2.4 Energy-Price Volatility And Power-CAPEX Inflation

- 4.3 Value Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Sustainability Positioning and Green Hosting Initiatives

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hosting Type

- 5.1.1 Shared Hosting

- 5.1.2 Virtual Private Server (VPS) Hosting

- 5.1.3 Dedicated Hosting

- 5.1.4 Cloud Hosting

- 5.1.5 Colocation Hosting

- 5.1.6 Managed WordPress Hosting

- 5.1.7 Reseller Hosting

- 5.1.8 Other Hosting Types

- 5.2 By Deployment Mode

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid/Multi-Cloud

- 5.3 By End-user Vertical

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.3.3 Individual Bloggers/Creators

- 5.3.4 Software Developers and SaaS Start-ups

- 5.4 By Application

- 5.4.1 Public Websites

- 5.4.2 E-commerce Stores

- 5.4.3 Web Applications

- 5.4.4 Mobile Applications and APIs

- 5.4.5 SaaS/PaaS Platforms

- 5.4.6 Other Applications

- 5.5 By Pricing Model

- 5.5.1 Subscription (Fixed-Term)

- 5.5.2 Metered/Pay-as-you-go

- 5.5.3 Tiered (Usage-Bracket)

- 5.5.4 Freemium and Ad-Supported

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 GoDaddy Inc.

- 6.4.5 Newfold Digital

- 6.4.6 Alibaba Cloud

- 6.4.7 Tencent Cloud

- 6.4.8 Liquid Web LLC

- 6.4.9 DigitalOcean

- 6.4.10 OVH Groupe SA

- 6.4.11 Hetzner Online GmbH

- 6.4.12 WP Engine

- 6.4.13 1and1 IONOS

- 6.4.14 Hostinger International Ltd.

- 6.4.15 SiteGround Hosting Ltd.

- 6.4.16 A2 Hosting LLC

- 6.4.17 Kinsta Inc.

- 6.4.18 DreamHost LLC

- 6.4.19 GreenGeeks LLC

- 6.4.20 InMotion Hosting Inc.

- 6.4.21 The Constant Company LLC

- 6.4.22 Namecheap Inc.

- 6.4.23 HostGator LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

網路託管服務市場:全球市場預測,2026-2032年

網路託管服務市場:全球市場預測,2026-2032年 2026年全球主機託管市場報告

2026年全球主機託管市場報告 全球網路託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球無伺服器資料處理市場報告2026年全球網站託管服務市場報告2026年全球碳智慧型網路託管市場報告

全球網路託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球無伺服器資料處理市場報告2026年全球網站託管服務市場報告2026年全球碳智慧型網路託管市場報告 串流媒體託管市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類網路託管服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類

串流媒體託管市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類網路託管服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類 日本網路託管服務市場規模、佔有率、趨勢及預測(按服務類型、部署類型、應用程式、最終用戶和地區分類),2026-2034年

日本網路託管服務市場規模、佔有率、趨勢及預測(按服務類型、部署類型、應用程式、最終用戶和地區分類),2026-2034年 網路託管服務市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、部署、地區和競爭格局分類,2021-2031年)

網路託管服務市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、部署、地區和競爭格局分類,2021-2031年)