|

市場調查報告書

商品編碼

2044079

電子廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)E-waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

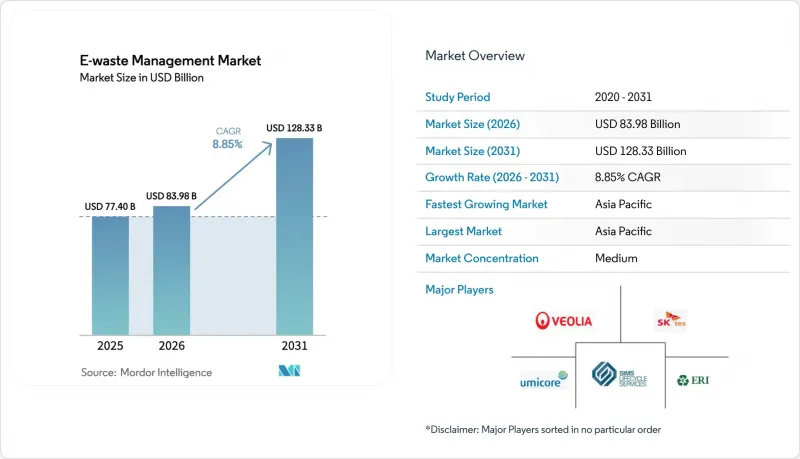

電子廢棄物管理市場預計將從 2025 年的 774 億美元成長到 2026 年的 839.8 億美元,到 2031 年達到 1,283.3 億美元,2026 年至 2031 年的複合年成長率為 8.85%。

2025年《巴塞爾公約》修正案收緊了事先同意(PIC)規定;歐盟正式實施生產者延伸責任制(EPR),設定了70-80%的回收目標;印度和中國也正式實施了生產者延伸責任制(EPR),設定了70-80%的回收目標;此外,美國聯邦政府向電池回收廠提供了超過30億美元的津貼。所有這些因素都促使電子垃圾流向從非正式拆解點轉向配備濕式和乾式冶煉生產線的持證加工設施。持證回收商正在擴大採用機器人技術和按需剝離黏合劑來降低拆解成本。同時,超大規模資料中心的更新換代正在向經合組織市場供應富含貴金屬的高品質印刷電路基板。銅、鎳和鋰等大宗商品價格的強勁上漲支撐了城市採礦的經濟合作暨發展組織可行性,而中國、加拿大和巴西新的省級回收法規正在擴大合法回收範圍,進一步推動了電子廢棄物管理市場的成長。隨著像 Umicoa 和 Aurubis 這樣的金屬提煉整合到回收和分揀等上游工程中,以確保原料的穩定供應,競爭公司之間的競爭正在加劇。

全球電子廢棄物管理市場趨勢與洞察

歐盟、印度和中國:70-80% 的生產者責任延伸回收強制目標和即時證書交易。

歐盟的《廢棄電子電氣設備指令》(WEEE指令)、印度的《2022年電子廢棄物管理條例》以及中國的補貼計畫均要求製造商實現70-80%(按以重量為準計)的回收率。透過布魯塞爾、新德里和北京的即時數位入口網站,製造商可以從回收商購買電子證書,從而將合規性轉化為可交易資產,並為電子廢棄物管理市場注入流動性。在印度,截至2024年5月,已有1,200家生產者責任組織(PRO)在入口網站上註冊,這將降低20-30%的管理成本,並刺激合法回收量的成長。中國將在2025年前向獲得許可的拆解企業提供3.9億美元的資金,以提高處理能力並遏制非法處理量。這些政策共同作用,正在加速對自動化工廠的投資,並重振再生原料供應鏈。

2025 年《巴塞爾電子廢棄物公約》擬議的更嚴格的修正案將強制要求全球事先同意 (PIC)。

2025年1月《巴塞爾公約》的修訂將電子廢棄物重新分類為危險品(A1181)和非危險品(Y49),要求出口商在裝運前獲得書面核准。合規相關的文書工作使運輸時間延長了4-8週,運費上漲了15-25%,導致2025年上半年全球跨境運輸量較2024年下降了12%。歐盟和北美的持證加工商能夠獲得先前流向非正規收集點的原料,從而提高了加工能力並支持了電子廢棄物管理市場的發展。由於行政負擔加重,小規模仲介業者退出了貿易,大型物流公司之間的整合也加速進行。中期來看,預計這項規定將建立正規的供應鏈,並削弱非正規經營者的成本優勢。

南亞和東南亞根深蒂固的非正式拆除生態系統正在扭曲材料的流動。

在印度、巴基斯坦、孟加拉、越南、印尼和菲律賓,非正規回收商仍處理這些國家70-80%的電子垃圾,他們依賴露天焚燒和酸浸等方法,使工人暴露於有毒金屬之中。這些非正規經營者透過規避環境法規和稅收,將價格定得比合法企業低20-30%,導致原料從合法工廠流失到非正規場所。童工問題依然嚴峻,世界衛生組織(世衛組織)估計,全球有1800萬未成年人從事非正規廢棄物,其中許多人從事電子廢棄物。在大都會圈以外,新的生產者責任延伸(EPR)門戶網站的實施情況參差不齊,使得非法垃圾處理點得以繼續存在。這些流失阻礙了合法處理商的回收工作,並對電子廢棄物管理市場的獲利能力造成了壓力。

細分市場分析

到2025年,金屬將佔電子廢棄物市場佔有率的56.96%。這反映了金屬相對於塑膠和玻璃更高的內在價值。目前,從廢棄電子產品中回收的銅可滿足15%的精煉需求,而從印刷基板中提取的金和鈀則以溢價現貨交易。 2025年,Aurvis公司位於呂嫩和漢堡的聯合工廠將處理超過一百萬噸電子廢料,為半導體和電線製造商回收銅、金和銀。隨著中國減少出口配額,從硬碟回收的稀土元素磁鐵也成為釹和鏑的重要來源。

城市採礦的經濟可行性得益於倫敦金屬交易所 (LME) 價格的持續高點以及原生礦山平均品位的下降,這導致資金轉向回收工廠。 UmiCore 位於霍博肯的濕式冶金浸出生產線已將鋰離子電池用黑料中鋰、鈷和鎳的回收率提高至 95%。 ISO 14001 和 R2v3 認證是採購的必要條件,高品質的原料集中在獲得認證的冶煉廠。隨著歐盟《關鍵原料法案》下關鍵原料分配的最終確定,金屬回收預計將以 10.45% 的複合年成長率成長,這將進一步擴大電子廢棄物管理市場中金屬的市場規模。

區域分析

預計到2025年,亞太地區將佔全球電子廢棄物管理市場的44.45%,並將以9.5%的複合年成長率持續成長至2031年。中國將在2025年提供3.9億美元的拆解補貼,這將促使非正規經營者走向正規化,並使前十大城市的年處理量翻倍。印度已運作中的生產者責任延伸(EPR)認證入口網站正在加速正規回收流程,允許生產商立即履行其義務,並對不合規的品牌處以罰款。日本的《家用電器回收法》和韓國的《生產者回收制度》的回收率均超過70%,為高價值金屬形成了成熟的通路。東協新興經濟體正在製定國家框架,但仍在努力實施,非正規拆解場所仍在遍遠地區普遍存在。

預計到2025年,歐洲在全球廢棄電子電氣設備指令(WEEE指令)和強化後的《巴塞爾公約》優先回收和回收(PIC)法規的支持下,將廢棄物留在區域內,其排名將位居第二。然而,2023年僅有三個成員國實現了65%的回收目標,歐盟平均仍為37.5%。布魯塞爾方面目前正提議提案更嚴格的罰款和關鍵金屬回收配額,這有望提升該地區的濕式冶煉能力。隨著出口下降,市場領導者威立雅(Veolia)、ALBA和Stena Metal正在收購小型公司以確保原料供應。根據2024/884號指令,光伏發電(PV)的各項義務將促使新的玻璃對玻璃(G2G)生產線運作,從而實現收入來源多元化。

在北美,由於IIJA和BIL提供的30億美元津貼,處理能力正在迅速提升。 Redwood Materials、Ascend Elements和American Battery Technologies等公司正在新建工廠並擴大現有工廠,而Recycle Cycle已與嘉能可簽署收購協議,收購其黑球業務。加州、紐約州和華盛頓州的州級生產者責任延伸制度(EPR)以及加拿大各省的相關法規,正在推動ERI等大型回收商之間的跨境流程標準化。儘管在南美、中東和非洲,EPR立法仍在發展中,但巴西和南非正在起草相關立法,這可能為電子廢棄物管理市場的未來成長奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場洞察與市場動態

- 市場概覽

- 市場促進因素

- 2025 年加強《巴塞爾電子廢棄物公約》擬議修正案需要事先獲得全球同意。

- 歐盟、印度和中國:強制EPR回收目標為70-80%,並實施即時證書交易。

- 來自美國國際工業發展署 (IIJA) 和美國國際工業發展署 (BIL) 的大量資金正在推動電池回收產能擴張,投資超過 30 億美元。

- 經合組織國家因人工智慧工作負載資料中心伺服器退役而產生大量高品質電子廢料。

- 按需釋放黏合劑和模組化設計標準顯著降低了拆卸成本。

- 歐盟提議對WEEE指令進行修訂:引入優先回收CRM和單獨回收太陽能(PV)的回收目標

- 市場限制因素

- 南亞和東南亞地區非正式的拆除生態系統正在扭曲材料的流動。

- 2025 年《巴塞爾公約》的 PIC 法規將增加跨國電子廢棄物運輸的物流和合規成本。

- 固態電池的化學成分,目前尚未建立工業回收途徑及安全規程。

- 具有強黏合性能的小型化消費性電子產品正在超過新的塑膠污染閾值。

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 對電子廢棄物產生情況的深入了解

- 全球動盪對電子廢棄物管理產業的影響

- 產業吸引力—五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值,十億美元)

- 材料

- 金屬

- 塑膠

- 玻璃

- 其他

- 按供應來源

- 資訊科技/通訊設備

- 家用電子產品

- 家用電器

- 醫療設備

- 工業設備

- 電動汽車電池

- 終身發電面板

- 其他(農業機械、生活垃圾、建築垃圾等)

- 按服務類型

- 收集、運送、分類

- 處置和處理

- 回收/再利用

- 掩埋/焚燒

- 回收和收集

- 機械分離

- 濕式冶金工藝

- 火熔煉工藝

- 生物冶金工藝

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Veolia Environnement SA

- TES-Sustainable IT Lifecycle Services

- Sims Lifecycle Services

- Umicore SA

- Electronic Recyclers International(ERI)

- Stena Metall AB

- ALBA Group

- Capital Environment Holdings Ltd.

- Enviro-Hub Holdings Ltd.

- Sembcorp Industries

- Waste Management Inc.

- Li-Cycle Holdings Corp.

- Aurubis AG

- Boliden AB

- Glencore Recycling

- MBA Polymers Inc.

- Desco Electronic Recyclers

- Enviroserve(Dubai)

- Retriev Technologies(Toxco)

- Tetronics International

第7章 市場機會與未來展望

The E-waste Management Market size is expected to grow from USD 77.4 billion in 2025 to USD 83.98 billion in 2026 and is forecast to reach USD 128.33 billion by 2031 at 8.85% CAGR over 2026-2031. Tighter Prior Informed Consent (PIC) rules under the 2025 Basel Convention amendments, formal extended-producer-responsibility (EPR) mandates that set 70-80% recycling targets in the European Union (EU), India, and China, and more than USD 3 billion in U.S. federal grants for battery-recycling plants are together steering material flows away from informal yards toward licensed processors equipped with hydrometallurgical and pyrometallurgical lines. Formal recyclers are scaling robotics and debond-on-demand adhesives to lower disassembly costs, while hyperscale data-center refresh cycles are releasing high-grade printed-circuit boards rich in precious metals into Organization for Economic Cooperation and Development (OECD) markets. Strong commodity prices for copper, nickel, and lithium sustain urban-mining economics, and new provincial take-back rules in China, Canada, and Brazil are enlarging the legal collection pool, further supporting E-waste management market growth. Competitive rivalry is intensifying as metals refiners such as Umicore and Aurubis integrate upstream into collection and sorting in order to secure feedstock certainty.

Global E-waste Management Market Trends and Insights

Mandatory 70-80% EPR Recycling Targets & Real-time Certificate Trading in EU, India, China

The EU Waste Electrical and Electronic Equipment (WEEE) Directive, India's E-waste Management Rules 2022, and China's subsidy scheme now oblige producers to meet 70-80% collection ratios by weight. Real-time digital portals in Brussels, New Delhi, and Beijing let manufacturers buy electronic certificates from recyclers, converting compliance into a tradable asset and injecting liquidity into the E-waste management market. India's portal registered 1,200 Producer-Responsibility Organizations (PROs) by May 2024, trimming paperwork costs 20-30% and driving higher formal collections. China disbursed USD 390 million in 2025 to licensed dismantlers, raising throughput and depressing informal tonnage. The combined policies accelerate capital spending on automated plants and stimulate secondary-material supply chains.

Tightened 2025 Basel Convention E-waste Amendments Mandating Prior-Informed Consent Globally

The January 2025 Basel Convention revisions recategorize electronic scrap under hazardous (A1181) and non-hazardous (Y49) codes, forcing exporters to secure written clearance before shipment. Global transboundary flows fell 12% in the first half of 2025 versus 2024 as compliance paperwork extended transit by 4-8 weeks and raised freight bills 15-25%. Licensed processors in the EU and North America gained feedstock that previously leaked to informal hubs, lifting throughput rates and supporting the E-waste management market. Smaller brokers exited the trade due to the administrative load, prompting consolidation among large logistics providers. Over the medium term, the rule is expected to cement formal supply chains while shrinking the cost advantage of unregulated operators.

Entrenched Informal Dismantling Ecosystems in South & Southeast Asia Skewing Material Flows

Informal recyclers in India, Pakistan, Bangladesh, Vietnam, Indonesia, and the Philippines still treat 70-80% of discarded electronics in these countries, relying on open-burning and acid-leaching methods that expose laborers to toxic metals. Informal operators undercut licensed facilities by 20-30% because they skip environmental controls and taxes, diverting feedstock away from formal plants. Child involvement persists; the World Health Organization (WHO) estimates 18 million minors work in informal waste globally, many in e-waste. Enforcement of new EPR portals is uneven outside metro areas, allowing illegal yards to survive. Such leakage curbs collection for certified processors and drags on the E-waste management market revenue.

Other drivers and restraints analyzed in the detailed report include:

- U.S. IIJA & BIL Funding Waves Fueling USD 3 Billion Battery-Recycling Capacity Build-out

- Debond-On-Demand Adhesives & Modular Design Standards Slashing Disassembly Costs

- 2025 Basel PIC Rules Raising Logistics & Compliance Costs for Cross-border E-scrap Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metals secured 56.96% of the E-waste management market share in 2025, reflecting their superior intrinsic value relative to plastics and glass. Copper yields from end-of-life electronics now meet 15% of refined demand, and gold and palladium extracted from printed-circuit boards command premium spot prices. Aurubis processed more than 1 million t of electronic scrap at its Lunen and Hamburg complexes in 2025, recovering copper, gold, and silver for semiconductor and wire clients. Rare-earth magnets recovered from hard-disk drives add neodymium and dysprosium to the supply pool as China narrows export quotas.

Urban-mining economics benefit from persistent high LME (London Metal Exchange) prices and declining average ore grades in primary mines, which shift capital toward recycling plants. Hydrometallurgical leaching lines at Umicore's Hoboken site uplift lithium-ion black-mass recovery rates to 95% for lithium, cobalt, and nickel. ISO 14001 and R2v3 certifications have become procurement prerequisites, funneling high-grade feedstock into certified smelters. As critical-material quotas under the EU Critical Raw Materials Act firm up, metal recovery is projected to expand at a 10.45% CAGR, further enlarging the E-waste management market size for metals.

The E-Waste Management Market Report is Segmented by Material (Metals, Plastics and More), by Source (IT & Telecommunication Equipment, Consumer Electronics, and More), by Service Type (Collection, Transportation & Sorting, Disposal/Treatment, and More), and by Geography (North America, South America, Europe, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.45% of the E-waste management market share in 2025 and is forecast to rise at a 9.5% CAGR through 2031. China awarded USD 390 million of 2025 dismantling subsidies that pushed informal operators toward licensing and doubled annual throughput in its top ten cities. India's live EPR-certificate portal lets producers trade obligations instantly, accelerating formal collections and imposing penalties on non-compliant brands. Japan's Home Appliance Recycling Act and South Korea's producer-take-back scheme both exceed 70% collection, creating a mature flow for high-value metals. Emerging ASEAN economies are drafting national frameworks but still struggle with enforcement; informal yards persist in rural belts.

Europe ranked second in 2025, buoyed by the WEEE Directive and the Basel PIC clampdown that keeps material inside the bloc. Yet only three member states met the 65% collection target in 2023, and the EU-wide average stood at 37.5%. Brussels now proposes tougher fines and CRM-recovery quotas that could lift regional hydrometallurgical capacity. Market leaders Veolia, ALBA, and Stena Metall are buying smaller firms to secure feedstock as exports narrow. Separate PV obligations under Directive 2024/884 will unlock new glass-to-glass lines, diversifying revenue streams.

North America is undergoing a capacity surge, anchored by USD 3 billion of IIJA and BIL grants. Redwood Materials, Ascend Elements, and American Battery Technology opened or expanded sites, and Li-Cycle secured Glencore offtake for its black mass. State EPR mandates in California, New York, and Washington plus Canada's provincial rules encourage large collectors such as ERI to standardize processes across borders. South America, the Middle East, and Africa remain nascent but Brazil and South Africa are drafting EPR bills that could seed future growth for the E-waste management market.

List of Companies Covered in this Report:

- Veolia Environnement SA

- TES - Sustainable IT Lifecycle Services

- Sims Lifecycle Services

- Umicore SA

- Electronic Recyclers International (ERI)

- Stena Metall AB

- ALBA Group

- Capital Environment Holdings Ltd.

- Enviro-Hub Holdings Ltd.

- Sembcorp Industries

- Waste Management Inc.

- Li-Cycle Holdings Corp.

- Aurubis AG

- Boliden AB

- Glencore Recycling

- MBA Polymers Inc.

- Desco Electronic Recyclers

- Enviroserve (Dubai)

- Retriev Technologies (Toxco)

- Tetronics International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightened 2025 Basel Convention E-Waste Amendments Mandating Prior-Informed Consent Globally

- 4.2.2 Mandatory 70-80 % EPR Recycling Targets & Real-time Certificate Trading in EU, India, China

- 4.2.3 U.S. IIJA & BIL Funding Waves Fueling $3 B+ Battery-Recycling Capacity Build-out

- 4.2.4 Data-Center Server Decommissioning for AI Workloads Releasing High-Grade e-Scrap in OECD

- 4.2.5 Debond-On-Demand Adhesives & Modular Design Standards Slashing Disassembly Costs

- 4.2.6 EU WEEE Directive Revision Drafts Introducing CRM-Focused Recovery Targets & Separate PV Stream

- 4.3 Market Restraints

- 4.3.1 Entrenched Informal Dismantling Ecosystems in South & Southeast Asia Skewing Material Flows

- 4.3.2 2025 Basel PIC Rules Raising Logistics & Compliance Costs for Cross-Border e-Scrap Shipments

- 4.3.3 Solid-State Battery Chemistries Lacking Industrial Recycling Routes & Safety Protocols

- 4.3.4 High-Adhesive, Miniaturized Consumer Devices Breaching New Contamination Thresholds for Plastics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights on E-waste Production

- 4.8 Impact of Global Disruptions on the E-Waste Management Sector

- 4.9 Industry Attractiveness - Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Material

- 5.1.1 Metals

- 5.1.2 Plastics

- 5.1.3 Glass

- 5.1.4 Others

- 5.2 By Source

- 5.2.1 IT & Telecommunication Equipment

- 5.2.2 Consumer Electronics

- 5.2.3 Household Appliances

- 5.2.4 Medical Equipment

- 5.2.5 Industrial Equipment

- 5.2.6 EV Batteries

- 5.2.7 Solar PV Panels

- 5.2.8 Others (Agricultural Equipment, Curb-side waste, construction, etc.)

- 5.3 By Service Type

- 5.3.1 Collection, Trasportation & Sorting

- 5.3.2 Disposal/ Treatment

- 5.3.2.1 Refurbishment & Reuse

- 5.3.2.2 Landfill/ Incineration

- 5.3.3 Recycling & Recovery

- 5.3.3.1 Mechanical Separation

- 5.3.3.2 Hydrometallurgical Process

- 5.3.3.3 Pyrometallurgical Process

- 5.3.3.4 Biometallurgical Process

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Qatar

- 5.4.4.4 Kuwait

- 5.4.4.5 Turkey

- 5.4.4.6 Egypt

- 5.4.4.7 South Africa

- 5.4.4.8 Nigeria

- 5.4.4.9 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Veolia Environnement SA

- 6.4.2 TES - Sustainable IT Lifecycle Services

- 6.4.3 Sims Lifecycle Services

- 6.4.4 Umicore SA

- 6.4.5 Electronic Recyclers International (ERI)

- 6.4.6 Stena Metall AB

- 6.4.7 ALBA Group

- 6.4.8 Capital Environment Holdings Ltd.

- 6.4.9 Enviro-Hub Holdings Ltd.

- 6.4.10 Sembcorp Industries

- 6.4.11 Waste Management Inc.

- 6.4.12 Li-Cycle Holdings Corp.

- 6.4.13 Aurubis AG

- 6.4.14 Boliden AB

- 6.4.15 Glencore Recycling

- 6.4.16 MBA Polymers Inc.

- 6.4.17 Desco Electronic Recyclers

- 6.4.18 Enviroserve (Dubai)

- 6.4.19 Retriev Technologies (Toxco)

- 6.4.20 Tetronics International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

循環電子設計和可回收設計平台市場預測至2034年-全球分析(按設計方法、平台類型、材料、相關人員、最終用戶和地區分類)零廢棄物和減廢棄物服務市場預測至2034年-按服務類型、交付模式、最終用戶和地區分類的全球分析電子廢棄物回收和循環電子產品市場預測至2034年-全球電子廢棄物來源、回收技術、循環電子產品策略、回收材料、最終用戶和地區分析循環電子市場預測至2034年-全球分析(依產品形式、產品類型、生命週期階段、循環策略、技術、最終用戶、通路和地區分類)

循環電子設計和可回收設計平台市場預測至2034年-全球分析(按設計方法、平台類型、材料、相關人員、最終用戶和地區分類)零廢棄物和減廢棄物服務市場預測至2034年-按服務類型、交付模式、最終用戶和地區分類的全球分析電子廢棄物回收和循環電子產品市場預測至2034年-全球電子廢棄物來源、回收技術、循環電子產品策略、回收材料、最終用戶和地區分析循環電子市場預測至2034年-全球分析(依產品形式、產品類型、生命週期階段、循環策略、技術、最終用戶、通路和地區分類) 電子廢棄物管理市場:按類型、處理方法和最終用途分類-2026-2032年全球市場預測零浪費家居用品市場預測至2034年:全球產品類型、材料類型、包裝類型、配方類型、應用領域、最終用戶、分銷管道和區域分析燈泡和安定器回收市場:按燈具類型、安定器類型、收集方式、服務模式和最終用戶分類-2026-2032年全球預測

電子廢棄物管理市場:按類型、處理方法和最終用途分類-2026-2032年全球市場預測零浪費家居用品市場預測至2034年:全球產品類型、材料類型、包裝類型、配方類型、應用領域、最終用戶、分銷管道和區域分析燈泡和安定器回收市場:按燈具類型、安定器類型、收集方式、服務模式和最終用戶分類-2026-2032年全球預測 全球電子廢棄物管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球電子產品循環回收市場:預測(至2034年)-按產品、組件、通路、回收流程、最終用戶和地區進行分析

全球電子廢棄物管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球電子產品循環回收市場:預測(至2034年)-按產品、組件、通路、回收流程、最終用戶和地區進行分析 日本家用電器回收市場規模、佔有率、趨勢及預測(按供應來源、收集材料、回收商、應用和地區分類,2026-2034年)

日本家用電器回收市場規模、佔有率、趨勢及預測(按供應來源、收集材料、回收商、應用和地區分類,2026-2034年)