|

市場調查報告書

商品編碼

2044078

電子郵件行銷:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Email Marketing Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

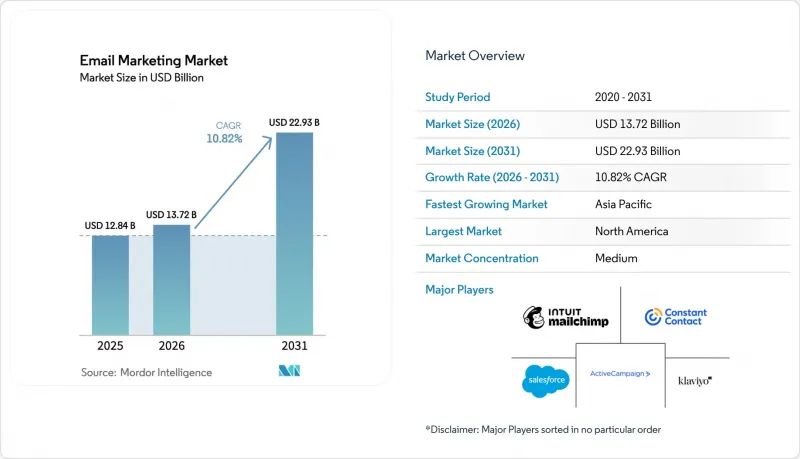

預計到 2025 年,電子郵件行銷市場將達到 128.4 億美元,到 2026 年將達到 137.2 億美元,到 2031 年將達到 229.3 億美元,2026 年至 2031 年的複合年成長率為 10.82%。

儘管隱私法規日益嚴格、收件匣演算法更加嚴苛,用戶在社群聊天應用程式上花費的時間也越來越多,但品牌仍持續加大投入,平均每投資1美元可獲得36美元的回報。供應商正在部署自動化和生成式人工智慧來維持送達率並提高用戶參與度,而中小企業則利用功能豐富的雲端原生套件來消除本地部署軟體的成本和維護負擔。北美地區率先採用DMARC和BIMI身份驗證、亞太地區電子商務基礎設施的快速擴張,以及醫療保健行業對符合HIPAA標準的患者體驗的需求,都推動了未來幾年電子郵件行銷市場的持續成長。市場競爭仍然激烈,排名前五的公司都在投資零方資料收集、跨通路整合和多語言分析,以維持其市場佔有率。

全球電子郵件行銷市場趨勢與洞察

宣傳活動自動化與受眾細分

即時決策引擎現在能夠根據瀏覽歷史記錄、預測流失率和客戶生命週期價值 (LTV) 模型發送訊息。與一次性發送相比,實施 Klaviyo 自動化流程的企業每位收件者的收入提高了 18 倍。 HubSpot 的 Breeze AI 可將創建時間縮短 40%,而 Salesforce Einstein 無需手動建立清單即可對微細分群體叢集,使品牌能夠實現大規模個人化。無程式碼自動化的普及推動了電子郵件行銷市場的進一步成長,即使是沒有資料科學團隊的中小型企業也能輕鬆使用。諸如一鍵退訂之類的合規性要求已作為標準功能內置,在減少監管摩擦的同時,也確保了良好的用戶體驗。

個人化功能可增強互動性

動態產品屏蔽和倒數計時器已發展成為預測性體驗,利用來自問卷調查和偏好中心的零方資料。 Klaviyo 用戶報告稱,由於建議引擎會根據他們的瀏覽模式展示客製化產品,轉換率提高了 15% 至 25%。 Adobe Marketo Engage 的人工智慧會為每位收件者選擇最佳主題、圖片和發送時間。同時,萬豪國際集團報告稱,得益於地理位置定向的優惠活動,直接預訂量增加了 12%。隨著第三方 Cookie 和行動識別碼的逐漸消失,第一方策略在電子郵件行銷市場中維持用戶參與度方面變得越來越重要。受監管產業確保符合 HIPAA 和 PCI DSS 要求,並確保引擎在未經明確同意的情況下排除敏感屬性。

投遞率問題和低開啟率

收件匣演算法會評估使用者互動情況並抑制垃圾郵件舉報,據預測,到 2025 年,行業平均郵件開啟率將降至 18%,而垃圾郵件資料夾的條目數將增加 9%。蘋果郵件的隱私功能會隱藏全球超過一半訊息的像素開啟情況,迫使行銷人員將成功指標轉向點擊量和轉換率。 Gmail 和雅虎對群發郵件的要求使得 DMARC 合規成為強制性要求,從而推動了對郵件清單清理、雙重確認和 BIMI 識別的投入。雖然這些措施保護了品牌形象,但也造成了用戶註冊的障礙。

細分市場分析

到2025年,解決方案將佔據電子郵件行銷市場佔有率的67.81%,這反映了企業在雲端套件和本地部署工具包方面的現有支出。然而,由於企業合併和合規性複雜性導致遷移支援需求不斷成長,專業服務和託管服務預計將以10.93%的複合年成長率成長,超過電子郵件行銷市場的整體成長軌跡。

像 Intuit 旗下的 Mailchimp 這樣的供應商正在將高級遷移服務捆綁銷售,以促進提升銷售;諮詢公司則利用零方資料策略研討會來維持收入。日益增多的隱私和身分驗證新要求也推動了對合規諮詢和送達率審計的需求。在醫療保健和銀行、金融及保險 (BFSI) 等行業,專業服務供應商正在提供符合 HIPAA 和 PCI DSS 標準的宣傳活動設計,以確保敏感通訊符合監管和品牌準則。

預計到2025年,雲端解決方案將佔據電子郵件行銷市場88.62%的佔有率,年複合成長率(CAGR)為11.08%,原因是品牌越來越重視訂閱式收費系統、靈活的容量和持續的功能發布。 Salesforce Marketing Cloud、HubSpot和Clavio透過向電商、資料倉儲和廣告平台合作夥伴提供強大的API ,正在推動這一趨勢。

然而,本地部署仍然十分重要,尤其是在金融服務、政府和國防領域,這些領域的資料居住、安全性和監管要求往往限制了多租戶雲端基礎設施的使用。 Oracle Eloqua 和 Adobe Marketo 繼續滿足此細分市場的需求,為具有嚴格合規要求的組織提供本地部署或私有雲端選項。兩種部署模式的並存反映了不同行業和地區在風險接受度和監管義務方面的差異。

區域分析

到2025年,北美將佔據全球整體收入的40.93%,佔據主導地位。在美國,DMARC的採用、傳輸時間預測引擎和自動化授權管理正被列為優先事項。在加拿大和墨西哥,隨著中小企業採用價格合理的雲端優先解決方案,區域需求不斷成長。

歐洲市場規模依然龐大,但合規性是其關注的重點。 GDPR推動了對偏好中心和資料主體存取工具的投資,尤其是在英國、德國和北歐國家。南歐新興的D2C(直接面對消費者)品牌透過利用多語言模板和在地化支付整合,在電子郵件行銷市場保持穩定成長。

亞太地區正以11.18%的複合年成長率引領成長,這主要得益於印度和中國不斷發展的電子商務生態系統、東南亞的金融科技繁榮以及日本向人工智慧測試的轉型。澳洲和新加坡正在成為區域行銷技術(MarTech)中心,而印尼和越南則實現了從傳統系統到API優先平台的跨越式發展。中東、非洲和拉丁美洲的絕對規模雖然落後於亞太地區,但隨著資料保護條例的完善和雲端基礎設施的日益普及,這些地區的成長率也保持穩定,達到中等個位數水準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 個人化功能可提升互動性

- 宣傳活動自動化與受眾細分

- 將電子郵件行銷工具與 CRM 和電子商務系統整合。

- 與替代管道相比,人們對投資報酬率的認知正在不斷提高

- 利用人工智慧進行傳輸時序預測與最佳化

- 引入以隱私為中心的身份驗證技術(DMARC、BIMI)

- 市場限制因素

- 分發方面的挑戰和低開啟率

- 嚴格的資料隱私法規和反垃圾郵件法

- 蘋果郵件的隱私功能導致郵件開啟率下降。

- Z世代對社群通訊平台的偏好

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按類型

- 解決方案

- 服務

- 不同的發展

- 雲

- 現場

- 按公司規模

- 中小企業

- 大公司

- 按最終用戶行業分類

- 零售與電子商務

- 旅遊與飯店

- 資訊科技和通訊

- BFSI

- 政府

- 衛生保健

- 教育

- 媒體與娛樂

- 其他最終用戶字段

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Intuit Inc.

- Constant Contact

- Klaviyo Group

- ActiveCampaign LLC

- HubSpot Email Marketing

- Salesforce Marketing Cloud

- Adobe Marketo Engage

- Oracle Eloqua

- Sendinblue(Brevo)

- Campaign Monitor

- Drip Inc.

- AWeber Communications

- GetResponse

- VerticalResponse

- Dotdigital Group

- iContact Inc.

- Mailjet(Sinch AB)

- Moosend Ltd.

- SparkPost Ltd.

- SendGrid(Twilio)

第7章 市場機會與未來展望

The Email marketing market size is projected to be USD 12.84 billion in 2025, USD 13.72 billion in 2026, and reach USD 22.93 billion by 2031, growing at a CAGR of 10.82% from 2026 to 203.

Consistent returns- averaging USD 36 for every dollar invested- keep brands invested even as privacy rules tighten, inbox algorithms grow stricter, and users spend more time on social chat apps. Vendors are embedding automation and generative artificial intelligence to preserve deliverability and raise engagement, while small and medium-sized enterprises (SMEs) enjoy feature-rich, cloud-native suites that remove the cost and maintenance burden of on-premise software. North America's early move to DMARC and BIMI authentication, Asia-Pacific's rapidly scaling e-commerce base, and healthcare's appetite for HIPAA-compliant patient journeys collectively reinforce a multiyear expansion path for the Email marketing market. Competitive intensity remains high as the leading five players invest in zero-party data capture, cross-channel orchestration, and multilingual analytics to defend share.

Global Email Marketing Market Trends and Insights

Automation of Campaigns And Audience Segmentation

Real-time decision engines now trigger messages off browsing histories, predictive churn scores, and lifetime-value models, driving 18-fold more revenue per recipient than one-time sends for merchants deploying Klaviyo's automated flows. HubSpot's Breeze AI trims creation time by 40%, and Salesforce Einstein clusters micro-segments without manual lists, letting brands personalize at scale. The democratization of no-code automation empowers SMEs that lack data-science teams, supporting the broader growth of the Email marketing market. Compliance obligations such as single-click opt-outs are now native, reducing regulatory friction while preserving user experience.

Personalization Capabilities To Enhance Engagement

Dynamic product blocks and countdown timers have evolved into predictive experiences that tap zero-party data from quizzes and preference centers. Klaviyo users report 15-25% conversion lifts when recommendation engines surface items aligned to browsing patterns. Adobe Marketo Engage's AI chooses the optimal subject line, image, and send time for each recipient, while Marriott International attributes a 12% rise in direct bookings to geo-targeted offers. First-party strategies gain importance as third-party cookies and mobile identifiers disappear, sustaining engagement within the Email marketing market. Regulated industries ensure engines exclude sensitive attributes unless explicit consent exists, aligning with HIPAA and PCI DSS mandates.

Deliverability Issues And Low Open Rates

Inbox algorithms reward engagement and punish spam complaints, driving average sector open rates down to 18% in 2025 and raising spam folder placement by 9%. Apple Mail Privacy Protection hides pixel opens for more than half the world's messages, forcing marketers to shift success metrics toward clicks and conversions. Bulk-sender requirements from Gmail and Yahoo make DMARC alignment mandatory, spurring investment in list hygiene, double opt-in, and BIMI logos that add onboarding friction even as they defend brand identity.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Email-Marketing Tools With CRM And E-Commerce Stacks

- AI-Driven Predictive Send-Time Optimization

- Stringent Data-Privacy Regulations And Anti-Spam Acts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 67.81% of the Email marketing market share in 2025, reflecting entrenched spend on cloud suites and on-premise toolkits. Yet professional and managed services are forecast to grow at 10.93% CAGR, exceeding the Email marketing market size trajectory as companies seek migration help after mergers and rising compliance complexity.

Vendors such as Intuit-owned Mailchimp bundle premium migration to accelerate upsell, and consultancies leverage zero-party data strategy workshops to defend billings. The proliferation of new privacy and authentication requirements has also driven up demand for compliance consulting and deliverability audits. In verticals such as healthcare and BFSI, specialized service providers offer HIPAA- and PCI DSS-compliant campaign design, ensuring that sensitive communications adhere to both regulatory and brand guidelines.

Cloud solutions controlled 88.62% of the Email marketing market size in 2025 and will climb at an 11.08% CAGR as brands value subscription pricing, elastic capacity, and continuous feature releases. Salesforce Marketing Cloud, HubSpot, and Klaviyo spearhead this adoption by exposing robust APIs to commerce, data-warehouse, and ad-platform partners.

However, on-premise deployments remain relevant- especially in financial services, government, and defense- where data residency, security, and regulatory requirements preclude the use of multi-tenant cloud infrastructure. Oracle Eloqua and Adobe Marketo continue to serve this niche, offering on-premise or private-cloud options for organizations with stringent compliance needs. The coexistence of both deployment models reflects the diversity of risk appetites and regulatory obligations across verticals and geographies.

The Email Marketing Market Report is Segmented by Type (Solutions and Services), Deployment (Cloud and On-Premise), Enterprise Size (Small and Medium-Sized Enterprises and Large Enterprises), End-User Vertical (Retail and E-Commerce, Travel and Hospitality, IT and Telecom, BFSI, Government, Healthcare, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a commanding 40.93% of global revenue in 2025, with the United States prioritizing DMARC adoption, predictive send-time engines, and consent-management automation. Canada and Mexico extend regional demand as SMEs adopt affordable, cloud-first suites.

Europe remains sizable but compliance-heavy. GDPR drives investment in preference centers and subject-access tooling, especially in the United Kingdom, Germany, and the Nordics. Southern Europe's up-and-coming direct-to-consumer brands leverage multilingual templates and localized payment integrations, sustaining incremental gains in the Email marketing market.

Asia-Pacific leads growth at an 11.18% CAGR, powered by India's and China's expanding e-commerce ecosystems, Southeast Asia's fintech wave, and Japan's switch to AI-based testing. Australia and Singapore host regional martech hubs, while Indonesia and Vietnam leapfrog legacy systems straight to API-first platforms. The Middle East and Africa and Latin America trail in absolute size but post robust mid-single-digit gains as data-protection rules mature and cloud infrastructure spreads.

- Intuit Inc.

- Constant Contact

- Klaviyo Group

- ActiveCampaign LLC

- HubSpot Email Marketing

- Salesforce Marketing Cloud

- Adobe Marketo Engage

- Oracle Eloqua

- Sendinblue (Brevo)

- Campaign Monitor

- Drip Inc.

- AWeber Communications

- GetResponse

- VerticalResponse

- Dotdigital Group

- iContact Inc.

- Mailjet (Sinch AB)

- Moosend Ltd.

- SparkPost Ltd.

- SendGrid (Twilio)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Personalization Capabilities to Enhance Engagement

- 4.2.2 Automation of Campaigns and Audience Segmentation

- 4.2.3 Integration of Email-Marketing Tools With CRM And E-Commerce Stacks

- 4.2.4 Growing ROI Recognition Versus Alternative Channels

- 4.2.5 AI-Driven Predictive Send-Time Optimization

- 4.2.6 Privacy-Centric Authentication Adoption (DMARC, BIMI)

- 4.3 Market Restraints

- 4.3.1 Deliverability Issues and Low Open Rates

- 4.3.2 Stringent Data-Privacy Regulations and Anti-Spam Acts

- 4.3.3 Apple Mail Privacy Protection Eroding Open-Rate Metrics

- 4.3.4 Gen Z Preference For Social-Messaging Platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium-sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 Retail and E-commerce

- 5.4.2 Travel and Hospitality

- 5.4.3 IT and Telecom

- 5.4.4 BFSI

- 5.4.5 Government

- 5.4.6 Healthcare

- 5.4.7 Education

- 5.4.8 Media and Entertainment

- 5.4.9 Other End-User Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Intuit Inc.

- 6.4.2 Constant Contact

- 6.4.3 Klaviyo Group

- 6.4.4 ActiveCampaign LLC

- 6.4.5 HubSpot Email Marketing

- 6.4.6 Salesforce Marketing Cloud

- 6.4.7 Adobe Marketo Engage

- 6.4.8 Oracle Eloqua

- 6.4.9 Sendinblue (Brevo)

- 6.4.10 Campaign Monitor

- 6.4.11 Drip Inc.

- 6.4.12 AWeber Communications

- 6.4.13 GetResponse

- 6.4.14 VerticalResponse

- 6.4.15 Dotdigital Group

- 6.4.16 iContact Inc.

- 6.4.17 Mailjet (Sinch AB)

- 6.4.18 Moosend Ltd.

- 6.4.19 SparkPost Ltd.

- 6.4.20 SendGrid (Twilio)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球交付和行銷電子郵件市場

2026-2030年全球交付和行銷電子郵件市場 需求產生軟體市場:依部署模式、組織規模、最終用戶和產業分類-2026-2032年全球市場預測

需求產生軟體市場:依部署模式、組織規模、最終用戶和產業分類-2026-2032年全球市場預測 2026-2030年全球數位行銷課程市場

2026-2030年全球數位行銷課程市場 2026年全球電子郵件檢驗軟體市場報告2026年全球電子郵件行銷市場報告2026年全球電子郵件送達率工具市場報告數位行銷市場:按組件、通路、買家類型、企業規模、部署模式和產業分類-2026年至2032年全球預測代理性能最佳化市場:按產品類型、技術、應用和分銷管道分類-2026-2032年全球預測

2026年全球電子郵件檢驗軟體市場報告2026年全球電子郵件行銷市場報告2026年全球電子郵件送達率工具市場報告數位行銷市場:按組件、通路、買家類型、企業規模、部署模式和產業分類-2026年至2032年全球預測代理性能最佳化市場:按產品類型、技術、應用和分銷管道分類-2026-2032年全球預測 數位行銷市場規模、佔有率、趨勢和預測:按數位管道、最終用戶產業和地區分類,2026-2034 年2026年全球沉浸式行銷市場報告

數位行銷市場規模、佔有率、趨勢和預測:按數位管道、最終用戶產業和地區分類,2026-2034 年2026年全球沉浸式行銷市場報告